GLAXF - GSK: A Defensive With A Healthy Dividend Yield

Summary

- Pharmaceuticals company GSK has seen a nice run up in price in Q4 2022. But with a rotation in favour of consumer stocks, can this continue?

- Its upcoming results could be an indicator. With earnings growth expected for 2022, its dividends could rise, adding to its attractiveness.

- Its sales ex-Xevudy, its COVID-19 treatment, could also remain healthy, going by recent trends and news on its pipeline, which could indicate its medium-term prospects.

Since the time I first put a buy rating on the pharmaceuticals company GSK (GSK) (GLAXF) in October last year, its price is up by 17.5%. I reiterated the buy rating in November again, and since then it has gained over 11%. These gains wouldn’t be a surprise to anyone who has either followed the company recently or the stock markets in general.

A weak economy and high inflation made defensives like healthcare stocks more attractive than their cyclical counterparts until recently. GSK also had the advantage of de-merging from its consumer healthcare segment earlier last year, making it a pure-play biopharma company.

However, in January 2023, its price has barely moved. With inflation on the wane and Mr. Market in a better mood, there’s a clear rotation in favour of consumer discretionary stocks. Does this mean that the best is over for the likes of GSK in the current cycle? Or is this a temporary blip and its price rise will resume? Here I analyse it from the perspective of its upcoming results on February 1 for the full year 2022 to understand what we can expect and what that means for the ADR.

The sales growth question

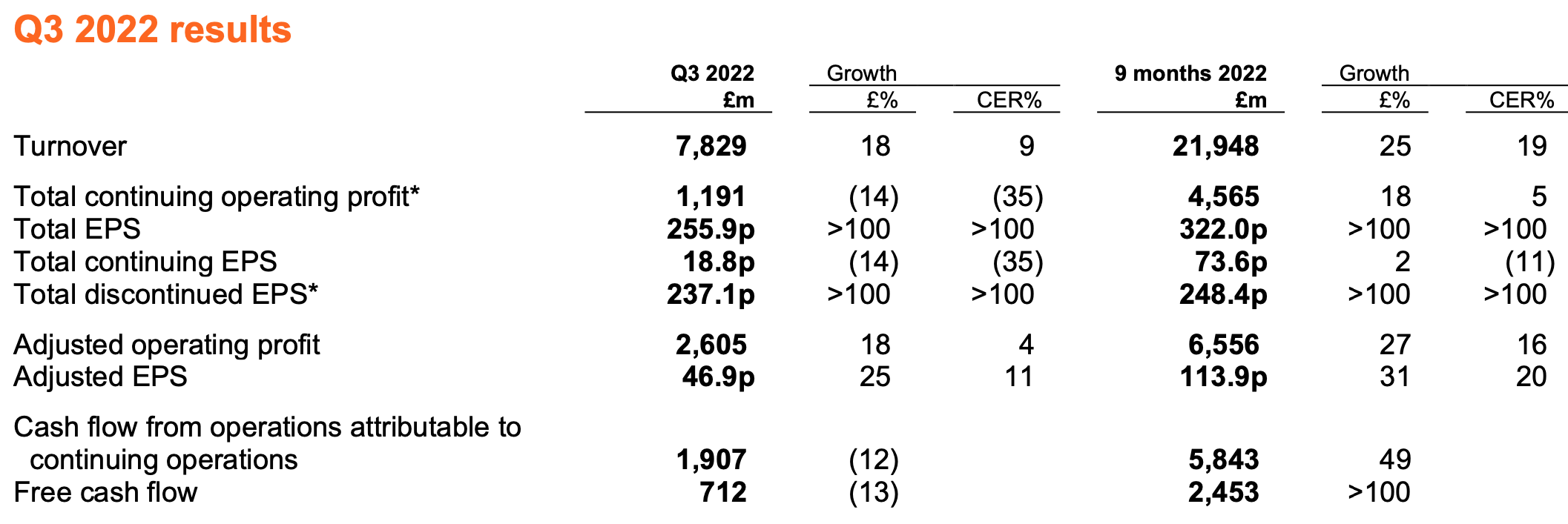

In my previous article on GSK following its third-quarter earnings update, I said that its sales can show higher-than-expected growth. Here I go look at why I think it’s likely, and also the flip side, why the sales projections might be on point. In its 2022 guidance, the company expects 8% to 10% growth in sales constant exchange rate [CER]. For the first nine months of 2022 (9M 2022), its turnover has risen by 19% year-on-year (YoY). This suggests that it expects growth to turn negative in Q4 2022.

I reckon there could be a surprise in the numbers going by the company’s own expectations on Q4 2022 sales. It says “We have delivered a strong nine-month performance ahead of our full-year guidance. In the fourth quarter, we anticipate continued strong sales growth…”. Continued sales growth indicates that it will likely exceed the target.

Except if sales of its COVID-19 medication, Xevudy drop dramatically in Q4 2022. This is possible considering that no alarms have been raised because of it this winter. These sales have had an outsized impact on overall sales so far. For 9M 2022, specialty medicines of which this treatment is part, grew by 56% at market exchange rates. The segment’s sales ex-Xevudy also grew at a healthy pace, but by a much slower 22%, even though it accounts for just 10% of GSK’s total sales.

{kind=link}

But then that does not look like a fundamental cause for concern about GSK’s sales anyway. I’d look out for the figure for sales ex-Xevudy, which I reckon would probably still look alright.

Dividends could rise

Next, its guidance for adjusted operating profit is a growth of 15% to 17%. This is easier to comprehend, going by the fact that the number has grown by 16% for 9M 2022 at CER. So it has to increase the figure at exactly the average rate in Q4 2022. At the time I last wrote, my sense was that there could be a margin decline, but considering again that COVID-19 hasn’t made a comeback in winter months, margins could stay alright. Xevudy is low margin business for GSK, which would otherwise drag the overall number down.

{kind=link}

The company adds that “Adjusted Earnings per share is expected to grow around 1 per cent lower than Operating Profit.” This suggests a significant slowing down in growth from 20% for 9M 2022. At the same time, it does confirm continued growth in the figure. Considering that its dividend payout ratio is also healthy at 27.5% for the last trailing twelve months [TTM], an increase in dividends could be in the offing in the results statement.

GSK already has a healthy dividend yield of 4.75% , which doesn’t sound like much in this time of high inflation but compared to the healthcare sector average at 1.45%, it’s still very good. In any case, for the long-term investor, inflation fluctuations will even out over time, so they can still come out ahead from a passive income perspective by investing in GSK.

What the market multiples say

But what of its price? It has already run up in the past few months, but over the past year, it’s still down by 25%. Its valuations are also subdued compared to peers. GSK’s price-to-earnings (P/E) ratio is at 14.3x compared to 25.4x for the healthcare sector. With no downward earnings surprises expected in the final quarter of 2022, at least going by the company’s projections for adjusted operating earnings, its P/E could look even more attractive soon. Its price-to-sales (P/S) at 1.6x is also significantly below the 4.5x for the sector. Even if sales were to dip, there’s still enough margin for it to stay lower than that for the sector.

Relief on Zantac

There’s also good news for GSK on the Zantac front. Allegations that its heartburn medicine caused cancer led to lawsuits against the company, which were recently dismissed in Florida. This isn’t the end of the story, but at least it indicates that the whole affair could go in its favour. Progress on its pipeline of treatments also looks healthy since my last update on the company.

What next?

Overall, the GSK story continues to look fine. There could be an impact on Q4 figures from a dip in COVID-19 treatment sales, but how much by remains to be seen. It’s possible that the company’s projections are conservative. Its earnings also look set to grow, so I would look out for the dividend announcement. If dividends rise, that in itself can be an impetus for the ADR. I’d also look out for its 2023 guidance, which will give more clarity on where its price is headed in the next year. It has shown even more upside than I had initially expected, of 15%.

I still maintain a Buy rating on it, but now from the perspective of dividend payouts and the fact that it’s a defensive to hold on to during a weak economy. Never mind the current rotation in favour of consumer stocks.

For further details see:

GSK: A Defensive With A Healthy Dividend Yield