GLAXF - GSK: Earnings Outlook Upgrade Attractive Valuations

2023-07-26 13:59:14 ET

Summary

- GSK plc's stock price has barely moved YTD. But with upgraded full-year expectations for both turnover and profits, coupled with attractive valuations, it looks set to rise.

- The outlook upgrade follows the better-than-expected 11% YoY sales increase in H1 2023. Its operating profit and EPS growth have picked up in Q2 2023, too.

- GSK's healthy dividend yield and reduced litigation risk on Zantac further back a Buy case for it.

Since the last time I wrote about the British bio-pharma company GSK plc (GSK) in January of this year, its price has barely moved. It has softened by under 2%. It's year-to-date [YTD] performance is similarly underwhelming, with a 1.3% rise. This lack of price movement is a definite a call to review my Buy rating on the stock. Especially today, after its second quarter 2023 (Q2 2023) results were released.

{kind=link}

Why the Buy case

They key reason for my rating on GSK stock was its dividends. Its price had already risen more than I had anticipated earlier, but with a 4.75% dividend yield it was a good stock to have in the portfolio anyway, as a defensive position in a weak economy. Added to this, I had expected a dividend increase, which didn't come through.

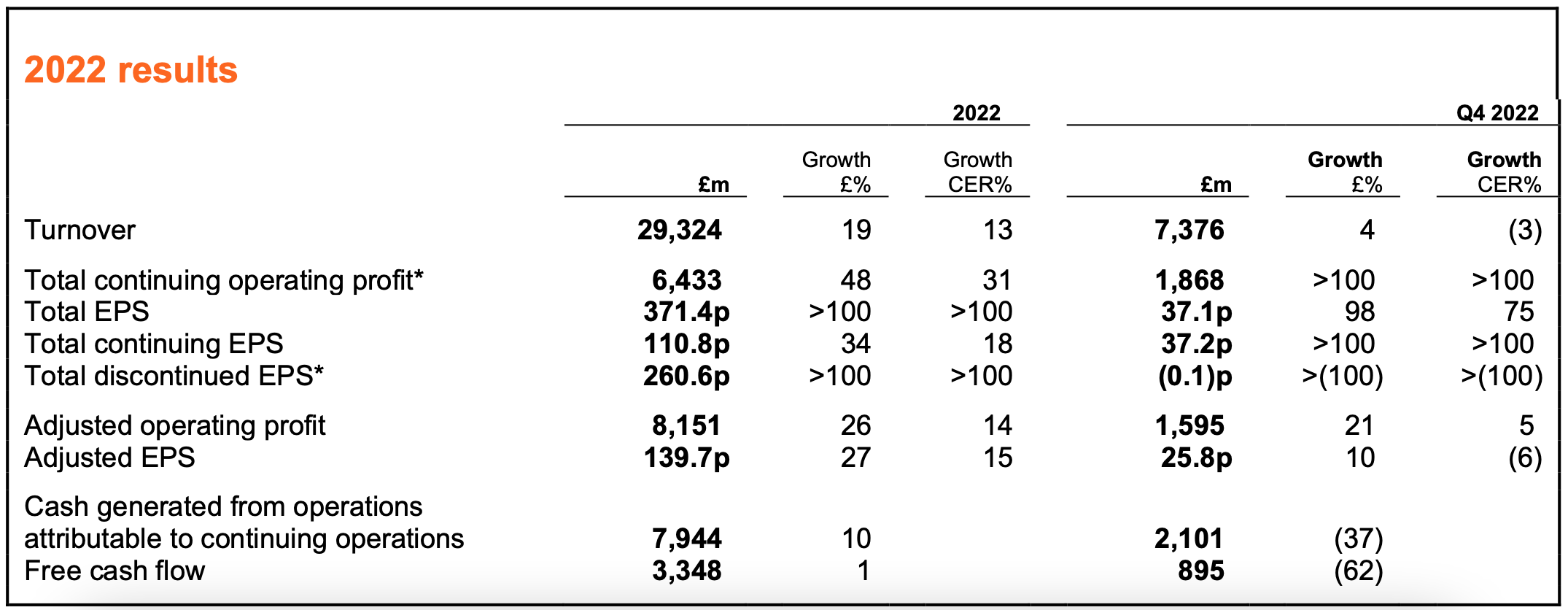

Further, I had anticipated that the company's revenue growth projections for 2022 looked conservative. They were. GSK surpassed its own sales guidance of 8-10% growth, with the actuals coming in at 13% at constant exchange rates [CER]. Its EPS grew as expected, even as adjusted operating profit growth came in a bit below expectations.

{kind=link}

Outlook upgrade

All in all, this sounds like a decent outcome, which begs the question of why GSK's stock hasn't performed better since January. As I see it, a key reason was its outlook for 2023. As it happens, Xevudy, the COVID-19 medication, had been a huge driver for the company's sales in the recent past. Take it out of the equation, now that the pandemic is done and dusted, sales growth naturally falls.

With this as the starting point, the company lowered is sales ex-Xevudy expectations to 6-8% for 2023. Adjusted operating profit growth was also expected to slow down to a growth of 10-12% and EPS growth to come in at 12-15%.

Two quarters into the current year, however, GSK has upgraded its initial guidance for both turnover and earnings (see text below), on improved expectations from both specialty and general medicines segments.

{kind=link}

Strong H1 2023 performance

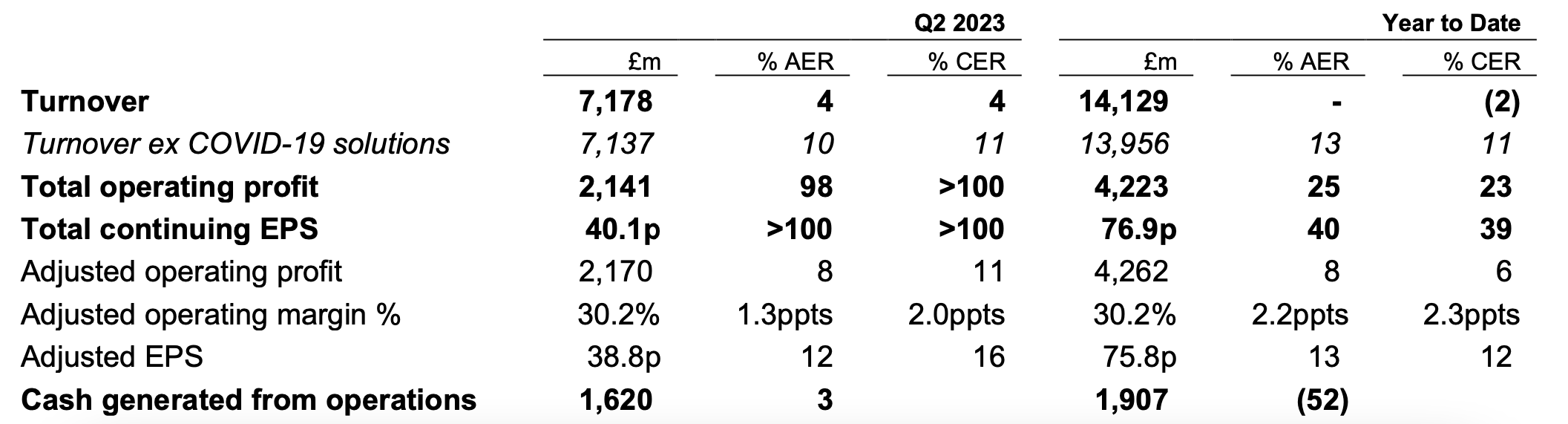

It's not hard to see why. The company's ex-COVID-19 solutions' sales have grown by 11% year-on-year (YoY) on a CER basis and by 13% in terms of actual exchange rates [AER] YTD, exceeding its initial expectations.

However, the improvement hasn't shown up in adjusted operating profit growth, which has risen by a muted 6% YTD . That said, this is essentially due to a weak first quarter, on the loss of Xevudy sales and legal provisions related to royalties.

In Q2, this profit figure grew by 11%, bringing it closer to the company's 2023 projected growth rate. The growth improvement is expected come as cost of sales and sales and selling, general and administrative [SGA] expenses are expected to grow broadly in line with the turnover. For context, they grew by 18% and 15% at CER in 2022, exceeding the 13% turnover rise.

Next, higher royalty income is expected, too. So far in the year, royalty income has grown by a healthy 36%. But improved growth isn't implausible considering that the head grew by 81% in 2022.

{kind=link}

EPS growth and competitive market valuations

Adjusted EPS growth so far in the year has also been lower at 12% compared to the upgraded full year expectations of 14-17%. But this is on account of slower growth in Q1 of 7% compared with an increase of 16% in Q2. This latest number indicates that GSK's EPS growth can reach the upgraded guidance for the full year.

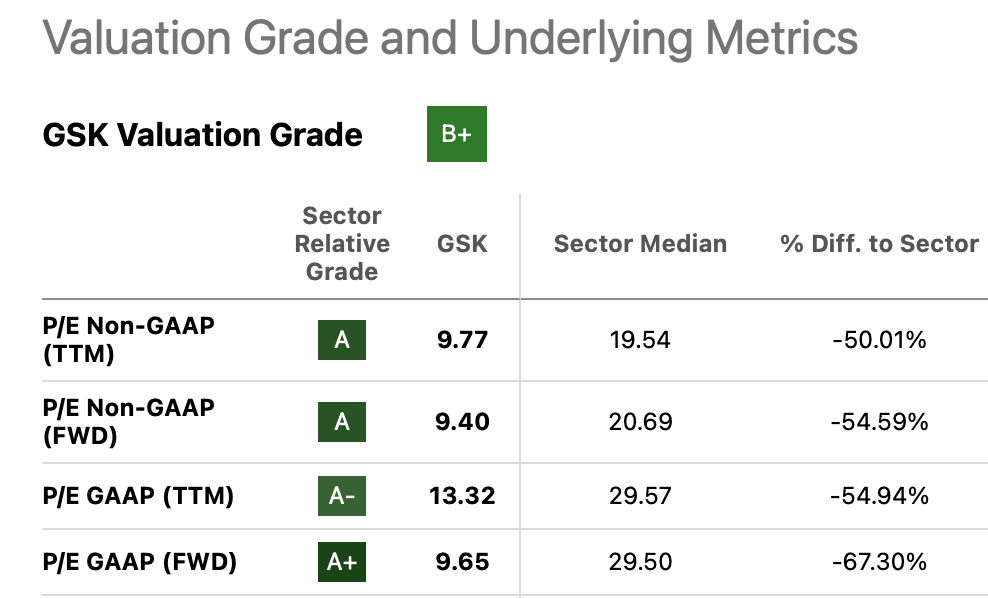

However, the earnings increase isn't adequately captured in the company's market valuations yet, which makes them competitive. GSK's trailing twelve months [TTM] price-to-earnings ratio on a reported basis is at 13.3x, which is less than half of that for the Health Care sector (see table below). And the same is true for its adjusted or non-GAAP P/E.

Analysts expect EPS growth in 2023 at 10.4% , which is lower than GSK's own projections. But it's interesting to note that even then, its forward non-GAAP P/E is a low 9.4x, compared to the sector average at 20.7x.

{kind=link}

The big gap in the company's and sector's valuations indicate that GSK is set for a significant price rise. I think it can certainly see a rise of 30%, which will take it back to its highs of early 2022. A big risk factor in the past has been the uncertainty around litigation over its heartburn drug Zantac, that is alleged to be cancer causing. But developments on the same show that GSK might just win this one.

Healthy dividend yield

There's also the dividend to consider. While the absolute amount has stayed static at GBP 56.5 in 2023 from last year, the forward dividend yield is not too bad at 4%. It's also significantly higher than the 1.45% for the Health Care sector. Further, the company has paid dividends consecutively for the last 21 years, making it a safe dividend stock. Its TTM dividend payout ratio at 21% is also quite comfortable, indicating that it can continue to pay them in the foreseeable future.

What next?

There's a whole lot to like about GSK right now. With the upgraded outlook, its sales figures are expected to grow closer to the rates seen in 2022, despite little contribution from COVID-19 solutions' sales. The upgraded earnings growth looks good too, and going by its Q2 numbers, the company is well on the way to achieving its projections.

In glaring contrast to this are its low valuations, especially now that the risk associated with litigation on Zantac has reduced. Added to this is its healthy dividend yield. It's not the most lucrative, but it far outstrips the health care sector's median yield and the company's long history of dividend payouts goes in its favor, too.

I'd be very surprised if GSK's price doesn't rise now. I'm retaining a Buy on it.

For further details see:

GSK: Earnings Outlook Upgrade, Attractive Valuations