GLAXF - GSK: Haleon Demerger Retrospective

Summary

- A little over a year ago is our last coverage on GSK.

- We looked at implied split in value between GSK's biopharma division and the consumer division, now called Haleon, when it was supposed to split off.

- Haleon seems to be valued fully, but the implied value based on pre-demerger market caps is a lot lower than where GSK actually is.

- The explanation is that, in the meantime, another one of our points on GSK came true, which is that they'd come over the LoE hump and have growers.

- Blenrep is coming in with growth, as is Shingrix which was long beleaguered. Things look pretty good for GSK's residual biopharma business.

Published on the Value Lab 30/8/22

It's been over a year since we last covered GlaxoSmithKline ( GSK ) ( OTCPK:GLAXF ) with our scenario analysis over the debt offloading onto the new consumer vehicle. They ended up dishing out less rather than more debt, and the valuation for Haleon ( HLN ) appears to be about full, and for good reason. Based on pre-spinoff market caps, lots of value seems to have been created, because GSK should have been valued quite a bit less than it is based on a simple residual value calculation. Despite that, the growth profile has become more clear, and its growth engines have outshone previous issues to create a decent profile once accounting for one-offs. Resumption in typical treatment in a world that is ignoring COVID-19 increasingly has helped the company. The biopharma multiple looks fine, and we like what we see.

A Look At Our Old Scenarios

If you're curious about exactly what we were saying about GSK when considering the demerger, refer to the article here . For your convenience, we've updated the chart with more recent figures.

Scenarios ((VTS))

The concept was that a certain amount of debt would be put on Haleon at the demerger, and using the Kimberly-Clark ( KMB ) multiple at the time as one typical of a brand-endowed consumer products company, we could split the value of a comprehensive pre-demerger GSK into a biopharma and consumer component. Haleon is valued at about 24 billion GBP, so they are trading more or less at the pre-inflation KMB multiple. That looks like a pretty full valuation for them based on the 10 billion GBP in net debt they got from GSK.

GSK residual currently has around 22 billion GBP in net debt . Using that figure, we can see what the implied valuations are for GSK's residual biopharma business. This was based on GSK's 68 billion GBP market cap from just before the de-merger. What's odd is that the residual GSK trades at around 56 billion GBP currently, which is a lot higher than the 40 billion GBP that would have been residually implied. The combined market caps add up to much more than the pre-merger market cap at 80 billion rather than 68 billion. It appears the hackneyed idea of splitting up companies for each to gain value independently actually worked this time.

Does that make the residual GSK undervalued, given that it can be easily argued that Haleon has a full valuation?

GSK Q2 Results Discussion

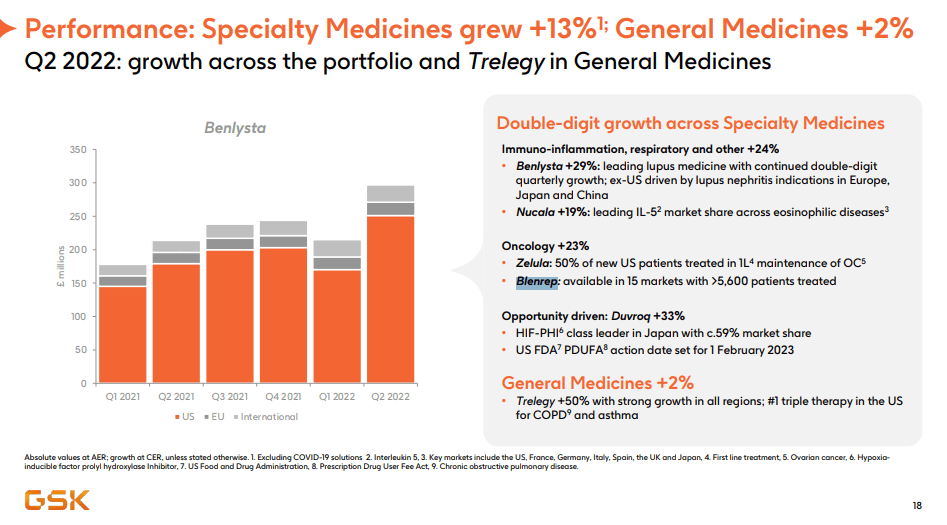

I think it comes down to the other coverage we had done on GSK, which is that as the LoE deadweights petered off of results, the veritable growth engines could take center stage. Its current vehicles at the time were Nucala, Trelegy, Benlysta and Zejula which were 10% of the revenue a year ago, including Haleon revenues. Oncology was a weak area for GSK for a while, and they were slow on that train, which was the bane of previous management. They had launched Blenrep when we covered the stock last. Let's see how this ensemble is doing .

Zejula and Blenrep are both doing very well, with high double-digit growth. Overall, oncology grew 23% thanks to their contributions. Benlysta and Nucala, which were GSK's growth drivers previously offsetting LoE declines, both continue to grow in the double digits. Trelegy also gains and adds a nice recurring revenue base to the results.

{kind=link}

Most of these drugs were acquired inorganically. GSK had been very judicious in these purchases, and with few choices, they got many winners. It's an accomplishment.

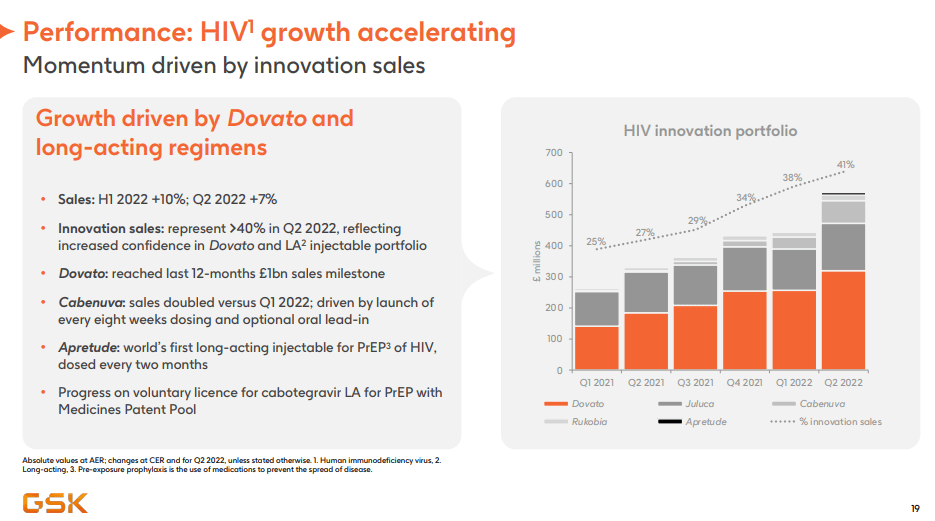

In vaccines, which had slumped a bit on account of COVID-19 (alternative infections became less common and the co-circulation risk did not materialize), are also on the recovery. In particular, Shingrix, which was a major product that had its thunder stolen by COVID-19 shortly after its debut, is back on growth now and living up to its potential. This was a major gut-punch to GSK that it has gotten over. YoY revenues have more than doubled and the overall vaccine performance is strong at 24%. Finally, for the topline discussion, the HIV portfolio is also seeing accelerated growth. A nice portfolio to have when looking at a recession and wanting high necessity products.

{kind=link}

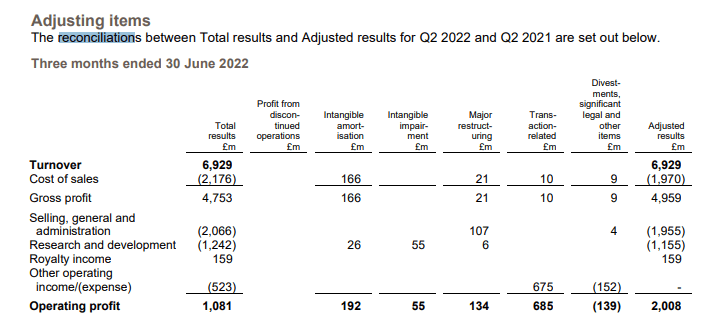

On the profit side, once accounting for one-offs, mainly the transaction-related expenses around the demerger, improvement is there up 22% YoY for the Q2, up 26% for the H1. Overall turnover went up 25%.

Operating Profit Reconciliation (Q2 2022 PR)

{kind=link}

Conclusions

Overall, the biopharma business ends up looking quite cheap as it is delivering solid growth thanks to the release of pent-up demand. Particularly, Shingrix is major, which is going towards blockbuster status possibly. Moreover, the long laggard oncology stigma might be becoming broken for GSK as its products continue to win share on non-CAR-T platforms. HIV products are nice too. Patent cliffs are far off. For some vaccines, they come in 3 years, but the majority are 5 years or 7 years from now. That's a lot of time in the pharma world. The multiple for GSK is a little above 8x now on EBITDA. That's close to Gilead's value , but we think GSK is much keener in terms of growth, where Gilead needs to deal with Veklury erosion. Overall, GSK's time is now, and it still trades at only a modest 10% premium to Gilead, which still has the stuff to prove. Looks like a fair exposure. A buy.

For further details see:

GSK: Haleon Demerger Retrospective