GSK - GSK: Positive Financial Developments Expected For Q3 2023

2023-10-28 08:35:57 ET

Summary

- GSK's stock price has dropped by 6.7% since July, but still outperformed the S&P 500 and the healthcare sector.

- This could change, as the company's Q3 2023 earnings are expected to show good financial performance, with double-digit growth expected in turnover, operating profit, and EPS.

- GSK's market multiples are attractive, too. While legal issues related to Zantac are holding the stock back, some upside is still likely.

Since I last wrote about the pharmaceutical company GSK (GSK) (GLAXF) in July its price has dropped by 6.7%. Disappointing as this is, considering my Buy rating on it, it's still better than the 9.8% decline in the S&P 500 ( SP500 ) during this time. But that's not all. GSK has also performed better than the S&P 500 Health Care sector, which has declined by 7.7% in this time.

Ahead of its third quarter (Q3 2023) earnings due next week, here I take a look at whether there is genuine upside to the stock, and not just better performance than broader indices. But first, a look at where GSK was when I last checked.

A look back

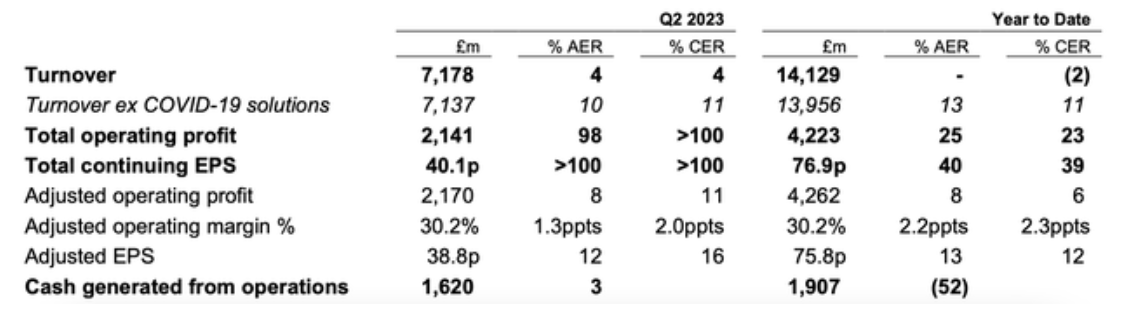

At that time, it had just released its first half (H1 2023) results, which weren't bad at all, with its turnover ex-COVID-19 solutions growing by 13% year-on-year (YoY) at actual exchange rates [AER]. Its adjusted operating profit margin was a 30.2% at AER, a 2.2 YoY percentage point increase and its adjusted EPS at AER had seen a 13% rise too.

Financial Highlights, H1 2023 (Source: GSK)

{kind=link}

Significantly, the company upgraded both its sales and profit guidance (see table below) along with its results and its forward dividend yield at 4% was decent too.

{kind=link}

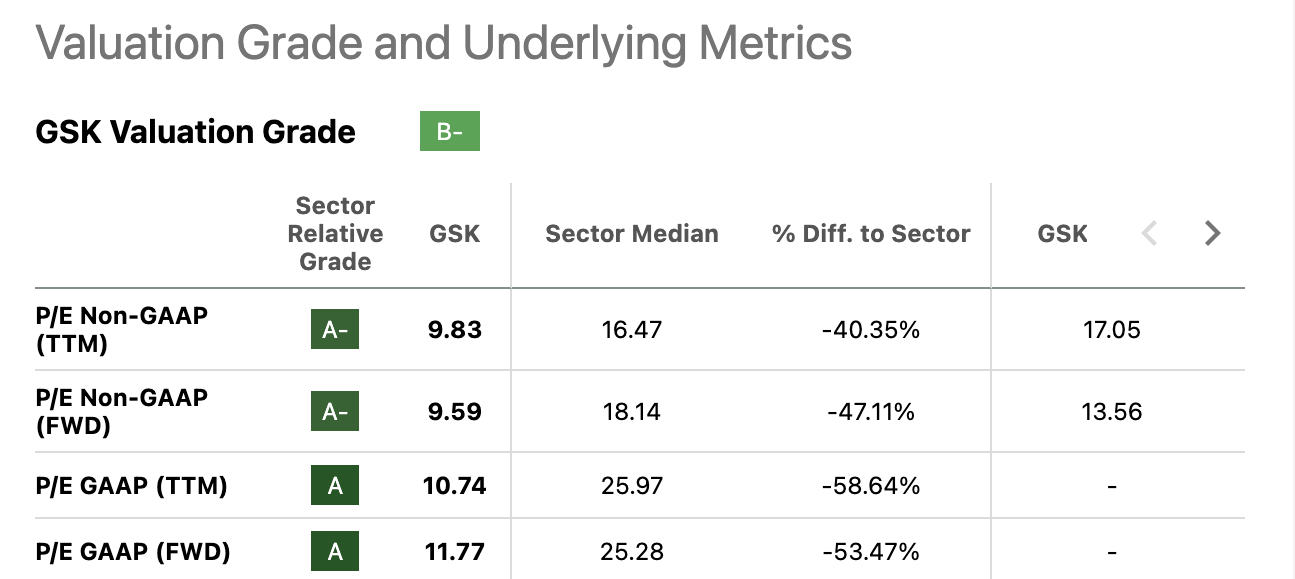

GSK's market multiples were competitive too. Its trailing twelve months reported [TTM] price-to-earnings ratio at 13.3x, was less than half of that for the Health Care sector. And forward non-GAAP P/E at 9.4x, compared favourably to the sector average at 20.7x as well.

In a nutshell, its healthy financials, upgraded 2023 outlook, good dividend yield, and attractive market multiples all worked in its favour, which led me to reiterate a Buy rating on the stock.

What to expect in Q3 2023

With this as the backdrop, all indications suggest that GSK's financial performance in Q3 2023 would be good too. According to my estimates, its turnover growth can pick up speed now, to 17.3% YoY, making up for the contraction in sales in H1 2023 when turnover inclusive of COVID-19 solutions is taken into account.

The assumptions for this estimate are as follows:

- The full year 2023 turnover growth would be at the midpoint of the forecast range. From this, the H2 2023 figure is calculated by netting the H1 2023 turnover already available.

- Q3 turnover is assumed to be 51.9% of the H2 2023 turnover, in line with the proportion seen as last year.

These same assumptions are made to estimate the Q3 adjusted operating profit and EPS. Adjusted operating profit is forecast to grow at 15.9%, also a higher growth rate from H1 2023, when it grew by 8% at AER. Further, the operating margin, as per these estimates rises to 32.9%, up from 30.2% at the time. The adjusted EPS is expected to grow by 17.7% (H1 2023: 13% at AER).

The market multiples

In absolute terms, the adjusted EPS is expected to be at USD 1.33 in Q3 2023, which is a more bullish estimated compared to the average USD 1.14 level analysts' estimates provided by Seeking Alpha. This then gives us the inputs for not one but two estimates for what would soon be GSK's trailing twelve months [TTM] non-GAAP price-to-earnings (P/E) ratio.

Based on my estimates, the TTM P/E would be 8.7x and based on the average of analysts' estimates it would be at 9.1x. This is significantly lower than the 16.5x level for the Health Care sector. Incidentally, this is also lower than GSK's current P/E of 9.8x as well.

{kind=link}

Now let's also look at the forward P/E for 2023. For the full year 2023, my estimates give an EPS of USD 3.9 and the average of analysts' estimates on Seeking Alpha are at USD 3.72. Neither of the two change the perception of GSK's undervaluation though. My estimates result in a forward non-GAAP P/E of 9x while that based on analysts' average figures puts it at 9.4x. By comparison, the health care sector's median P/E is at 18.1x.

The story of attractive market multiples then continues from when I last checked, with significant upside for the stock persisting.

What's holding GSK back?

This begs the question, so what's holding GSK back? How is it trading so low even with everything going right for it? In one word, Zantac. The company's heartburn medication has opened a can of worms, with accusations of it being carcinogenic and a plethora of lawsuits have followed.

The company recently settled a case in California on the matter. While it maintains in its statement that the settlement is based on the desire to "avoid the distraction related to protracted litigation", it isn't the best possible outcome for the stock. Moreover, the legal troubles continue for GSK, with 75,000 cases outstanding in Delaware.

Whether the company goes to trial or settles these cases, there's likely to be a financial impact on the company going forward, which of course, dims the shine from its current and expected progress. And if they do get proven right, there's real potential loss of credibility involved as well.

This is so, even as it continues to make strides in other areas. For instance, it has recently partnered with China's Chongqing Zhifei Biological Products for distribution of its shingles vaccine Shingrix in the country. GSK's presence in China is limited, and Shingrix, which accounts for 12% of its sales already, can be a good way to expand into the market.

What next?

The earnings update next week should continue to confirm GSK's good financial health. The company's continued EPS growth in estimated to be in high-double digits, appears particularly encouraging. Not only does it make its P/E ratio more attractive than it already is, strong profit growth indicates potential for dividend increase.

The only real stumbling block to the otherwise solid GSK story is Zantac related litigation. It has dragged on for a while, holding the stock back, and as of now, there appears to be no end in sight. If it were to be resolved favourably, investors could be rewarded with a share price rise. Even without a resolution, however, there's definite upside to the stock for now. I'm reiterating a Buy, though investors should brace for price fluctuations on Zantac related developments.

For further details see:

GSK: Positive Financial Developments Expected For Q3 2023