GLAXF - GSK: Strong Positioning And Trading At Historical Discount

2023-09-29 14:27:37 ET

Summary

- GSK is a leading biopharmaceutical company with a focus on vaccines and products for major diseases.

- GSK's drug line-up is safe and profitable, with competitors facing larger sales loss exposure due to patent expirations.

- GSK has a strong balance sheet, high margins, and a sound revenue track record, making it a compelling value investment.

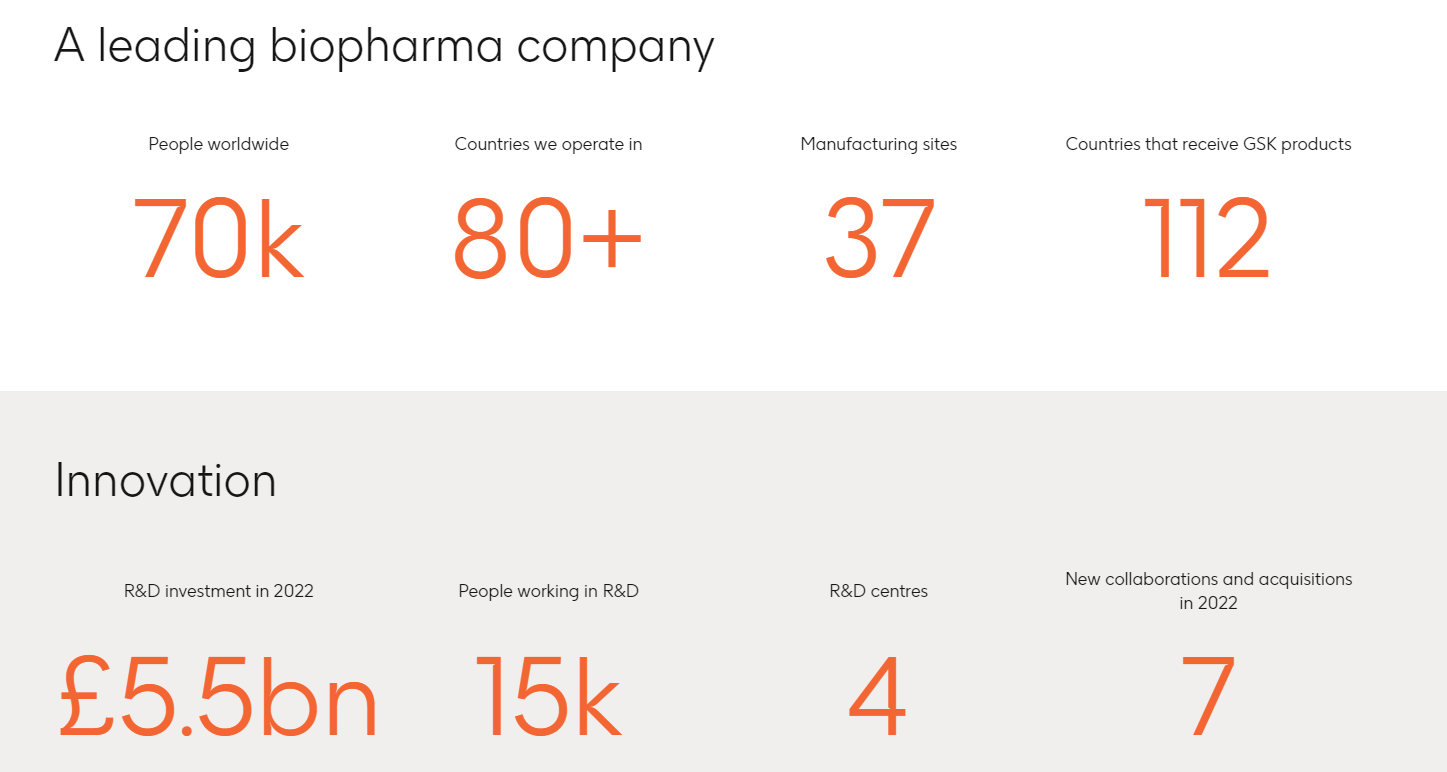

I remember driving by the GSK ( GSK ) plant near Toronto, Ontario every weekend - back when it was GlaxoSmithKline - and marveling at the true scale and size of the manufacturing facility, where millions of medicines and vaccines are produced that make a positive change in the healthcare systems of the world.

The company is one of the leading biopharmaceutical companies worldwide and currently ranks as the 10th largest right on the heels of AstraZeneca (AZN):

{kind=link}

The British multinational pharmaceutical company is based in London and has 37 manufacturing sites, and a presence globally with a focus on vaccines and products for major diseases including asthma, cancer, infections, diabetes, and mental health.

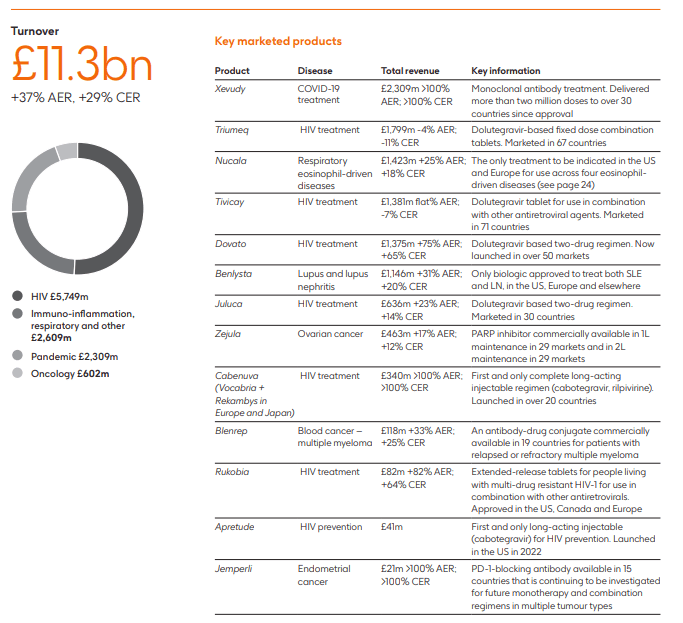

Let's get straight into the business and understand what GSK does. They have three core service lines and the breakdown is as follows:

- Specialty Medicines - £11.3bn.

- General Medicines - £10.1bn.

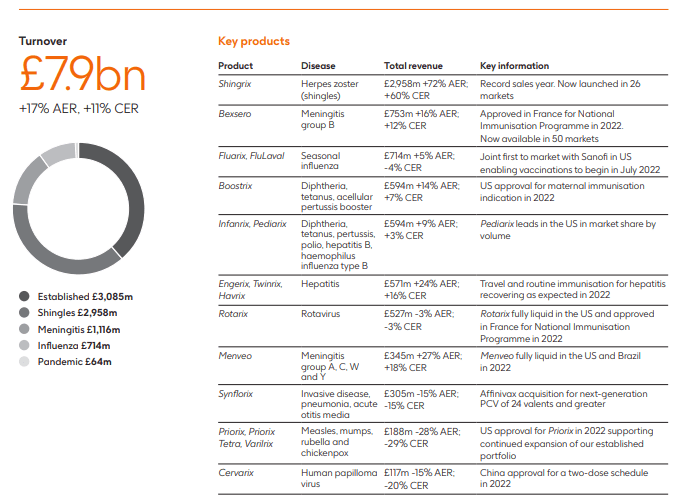

- Vaccines - £7.9bn.

{kind=link}

{kind=link}

Patent Expiration

It's difficult to comment on every drug. However, having done the research I thought of a creative way of expressing how safe and profitable GSK's drug line-up is. Have a look at this list of the biggest major drug patents that are due to expire in less than 10 years, or by 2030:

Moody's and company filings. By Randy Leonard

Notice something interesting here? AbbVie (ABBV), Merck (MRK), Bristol Myers (BMY), Regeneron (REGN), Johnson & Johnson (JNJ), and basically all of GSK's competitors have larger sales loss exposure to major drugs that are going off-patent. When we look at Dolutegravir, which is owned by ViiV Healthcare (GSK has a 73% interest), it doesn't even factor in the top 12 products for the business. ViiV Healthcare has a small contribution to GSK's profit in 2022 and Dolutegravir is one of 17 drugs that the business manages in turn.

Valuation

GSK trades at a trailing PE of 11.8 and a forward PE of 9.6. There are healthy margins as you'd expect from a major pharma company, as they have a profit margin of 53% and operating margin of 27%.

As we have in previous analyses, including my recommendation for Merck, I take an unbiased and data-driven approach to assessing the balance sheet, income, and cash flow statements of the firm. This follows the principles laid out in Warren Buffett and the Interpretation of Financial Statements (by Mary Buffett).

David Huston

GSK is in very good shape. The company has a sound revenue track record, high margins, and relatively decent SG&A and R&D expenses. I have marked these as amber because proportionally SG&A is still high at 43.6% of revenue. However, I was surprised to see that both categories are lower than Merck (which is a good thing) albeit Merck has a higher gross margin.

Part of the issue investors have had with GSK is that its EBIT margin - at 19.2% is lower than its peers. Merck is 35%, Johnson & Johnson is 22.5%, and Pfizer ( PFE ) manages a somewhat worse 16.5% (partially explaining why their shares have lagged). I have marked this green because objectively speaking it's a good performance measure, but relative to peers this is more towards low-to-average.

The balance sheet is sound. Looking at the ratio of Property, Plant & Equipment, compared to Total Debt and Net Income is a very useful tool to understand how good the business is at cash conversion. In the case of GSK they have $20.1bn in PPE, require $21.0bn in Long & Short term debt to operate, and produce $4.46bn in net income. That's a cash generative business and sort of dispels the notion that they have "too much debt".

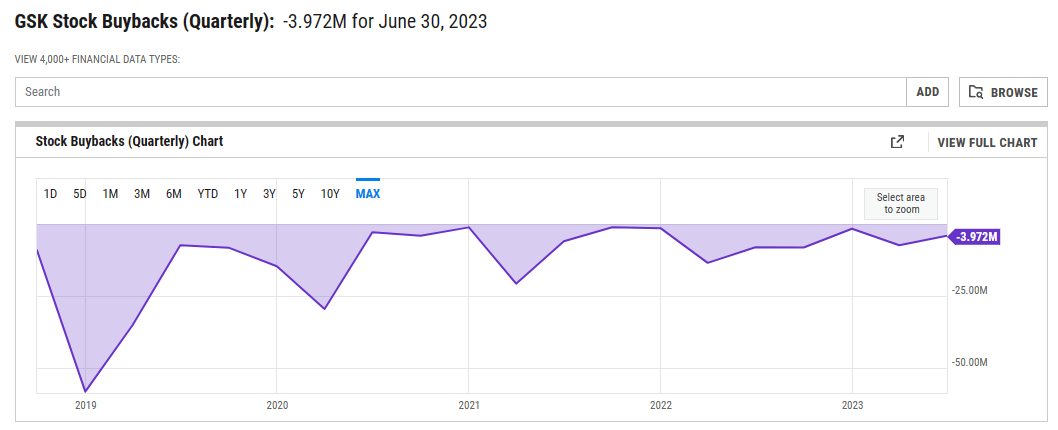

There is no issue with debt - long-term debt can be paid off in less than four years of net income, so it's not really a major concern or burden for the company. I have marked Debt to Shareholder Equity ratio as red, but that's principally because it doesn't include stock buybacks. This does raise an issue because part of the problem the shares have faced is that stock buybacks look like they are drying up:

{kind=link}

GSK could benefit from buying back shares and looking for further ways to drive shareholder value.

Overall the return on shareholders' equity is quite strong when compared to net income. I advised buying Merck in the $75-80 range and it has since appreciated to $104-$110. I now believe that GSK represents more compelling value and trades on a very cheap multiple for the growth on offer, with a strong balance sheet and market position.

Finally, to top it off GSK sports a 3.9% dividend yield that is very well covered with a 37% payout ratio.

Growth Plans

GSK made a bold announcement last year to invest £1 billion in R&D to get ahead in infectious diseases treatments, with a focus on lower income countries. This includes focusing on new treatments for malaria, tuberculosis, HIV (through ViiV Healthcare), tropical diseases and anti-microbial resistant diseases.

The company's chief scientist has made public plans to focus more on vaccines and infectious diseases and to pivot away from growth in oncology. What's interesting is that this is a fundamentally pragmatic pivot: GSK's teams are now quicker to cut their losses when a drug or discovery is not working, and they have woven in CRISPR and gene-editing technology and genetic validation in drug discovery.

For investors that set the compass: GSK is saying that they are going to dominate infectious disease R&D and HIV treatment, while presumably maintaining what they are doing in their other domains.

How is that going?

They have a number of newer specialty treatments including:

- Nucala (severe eosinophilic asthma).

- Bexsero (meningitis vaccine).

- Shingrix (shingles vaccines).

- Trelegy Ellipta (three medicines in a single inhaler to treat COPD).

- Juluca (dolutegravir+ rilpivirine once-daily, single pill for HIV).

This is a huge pivot. The company expects that new products like this with strong top line growth will account for up to 60% of GSK's sales growth during this period (2022-2027) as they crank out new drug discoveries and treatments with a focus on infectious diseases and HIV.

The following drugs are in the hopper for 2023:

- Duvroq/daprodustat for anemia associated with chronic renal disease was approved in February by the US FDA.

- AREXVY RSV vaccines for older adults were approved in August 2023 in time for fall/winter.

- Momelotinib for myelofibrosis with anemia was approved in the US on 15th September.

The last three approvals support the thesis that their strategy is working. Fundamentally, there is chronic underinvestment in certain segments of infectious disease research. According to a paper in the Lancet that assessed infectious disease research between 1997 and 2013, they found that pneumonia, shigellosis, cholera, syphilis, HIV, tuberculosis and malaria were chronically underfunded by researchers globally. Herein lies the opportunity for GSK to put some serious money behind that research, and to launch treatments and products that add real value to an area that requires further investment.

Risks & Issues

From a valuation and fundamental perspective GSK is an enticing company that appears to be executing well.

I see three key issues that could impact GSK:

R&D Pipeline Priorities Wrong

- Issue: They have clearly pivoted away from treatments in oncology in their R&D approach. Have they assessed the market right and are they confident that infectious diseases and vaccines can continue to deliver the growth they expect?

Moat and Competitive Position

- Issue: I would argue that GSK has a wide moat, but one that is under the threat of competition. Any slippage in their operating performance from here could suggest that they are succumbing to competition in key markets that could be damaging to the company's performance.

Patent Expiration

- Issue: Although the near-term picture is very strong, GSK does have key HIV drugs Tivicay, Triumeq, and Dovato (collectively representing close to 15% of total sales) coming off patent by 2028-29. There is pressure to ensure that the revenue from those is replaced before we get there.

- HIV patent expiration will start to be an issue in 2027.

Overall Assessment

It's been fun pulling through this company for weeks and drilling down into what makes GSK tick. I was fortunate to pick up shares before their Momelotinib announcement, but they have since come back down and represent compelling value at today's pricing levels.

The company has used its vast resources to differentiate itself with a focus on world-leading and future facing drugs in the HIV, vaccine, and respiratory segments of the market, setting the business up for success for the next decade. They have near-term visibility over revenue from big hitters like Shingrix vaccine, and virtually no near-term patent losses to worry about. Their economic moat is secure for now and looks solid against the competition.

There appear to be more potential tailwinds than headwinds. If GSK were to introduce a share buyback program, that would greatly accelerate the share price. They have easy room to maneuver with the dividend and time to focus on "being great" at R&D and also incrementally improving their medicines.

It's a wide-moat business, executing in an area of business that we all need (who doesn't want to remain healthy!) with economies of scale and a powerful distribution network. We will be tracking this company very closely in the coming quarters.

For further details see:

GSK: Strong Positioning And Trading At Historical Discount