AZNCF - GSK Vs. Bristol-Myers Squibb: Who's More Underrated By Mr. Market

2023-04-10 08:26:10 ET

Summary

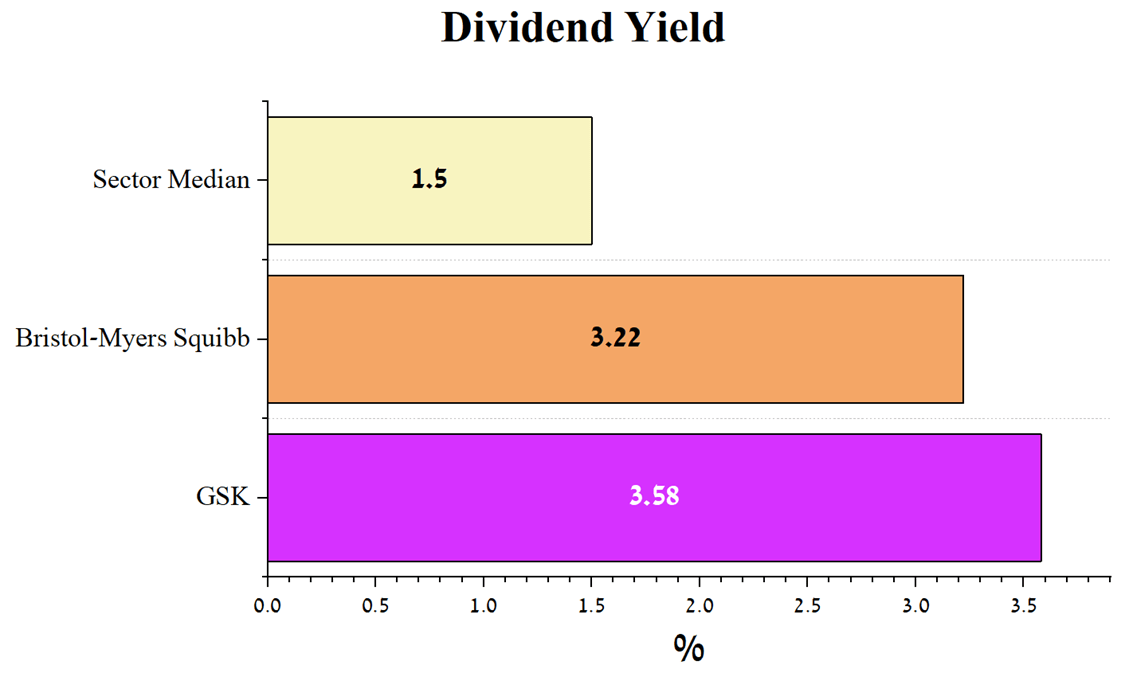

- GSK's dividend yield is 3.58%, slightly higher than Bristol-Myers Squibb's 3.22%.

- Bristol-Myers Squibb's total debt was about $40.8 billion at the end of 2022, down $4.78 billion from the previous year, thanks to the successful integration of Celgene and MyoKardia.

- Bristol-Myers Squibb's EBITDA margin was 43.7% for 2022, which is 11.4% more than GSK.

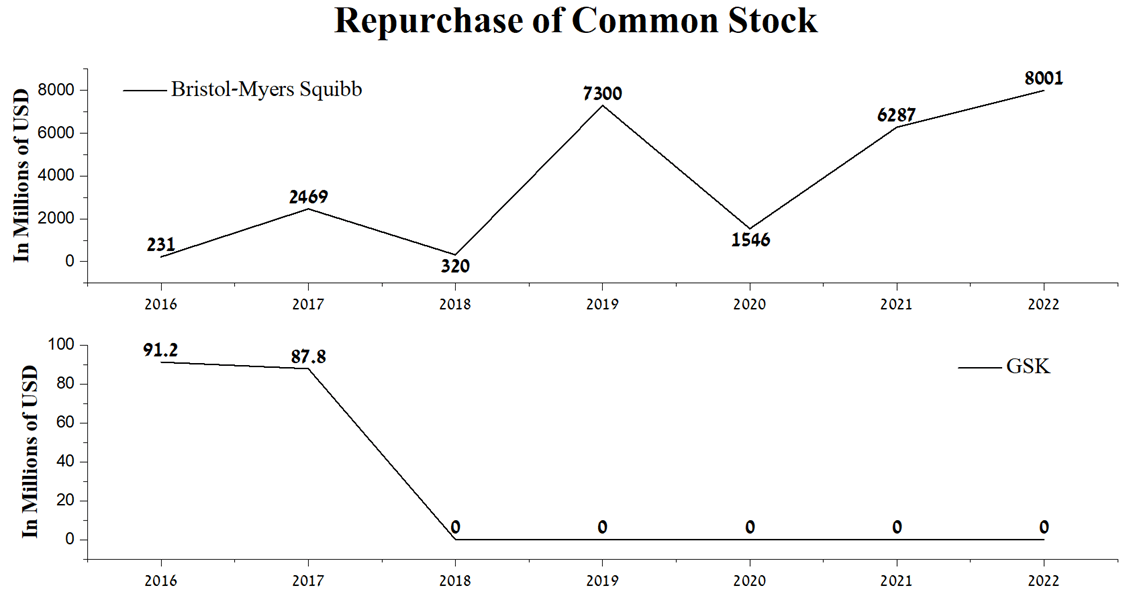

- Unlike GSK's management, Giovanni Caforio, CEO of Bristol-Myers Squibb, actively resorts using the company's share buyback policy. In 2022, BMY bought back $8,001 million worth of shares, a record high in the company's history, and still has $7.2 billion in reserves set aside for this purpose.

- Excluding sotrovimab sales, Specialty Medicines' revenue rose 9.3% QoQ, driven by more robust demand for HIV drugs. In our estimation, Cabenuva continues to be GSK's gem in the multibillion-dollar HIV drugs market, thanks to the FDA's approval of bimonthly dosing.

GSK ( GSK ) is one of the largest pharmaceutical companies in the UK, leading the development of medicines aimed at fighting respiratory and autoimmune diseases and offering some of the best therapies for HIV patients. While Bristol-Myers Squibb ( BMY ) is a leader in the treatment of oncological and hematological diseases, and after the acquisition of MyoKardia , it has strengthened its position in the multi-billion dollar cardiovascular drugs market.

Both companies have an extensive portfolio of product candidates and medicines, growing dividend payouts, and high margins, which make GSK and Bristol-Myers Squibb worthy of consideration as long-term assets during macroeconomic and geopolitical tensions. On the other hand, GSK's share price remains under pressure from the ongoing Zantac lawsuit, in which the plaintiffs allege that the company failed to warn them of the severe risks to their health from taking the drug. At the same time, the price of Bristol-Myers Squibb's shares fell 13% from a multi-year high due to increased financial risks caused by the sharp struggle between mega-blockbuster Revlimid and its generic versions in recent quarters.

We believe that despite these risks, both companies are attractive, but one is more promising in the long term and is more likely to outperform the S&P 500 ( SPY ) and iShares Biotechnology ETF ( IBB ) significantly.

Financial position of Bristol-Myers Squibb vs. GSK

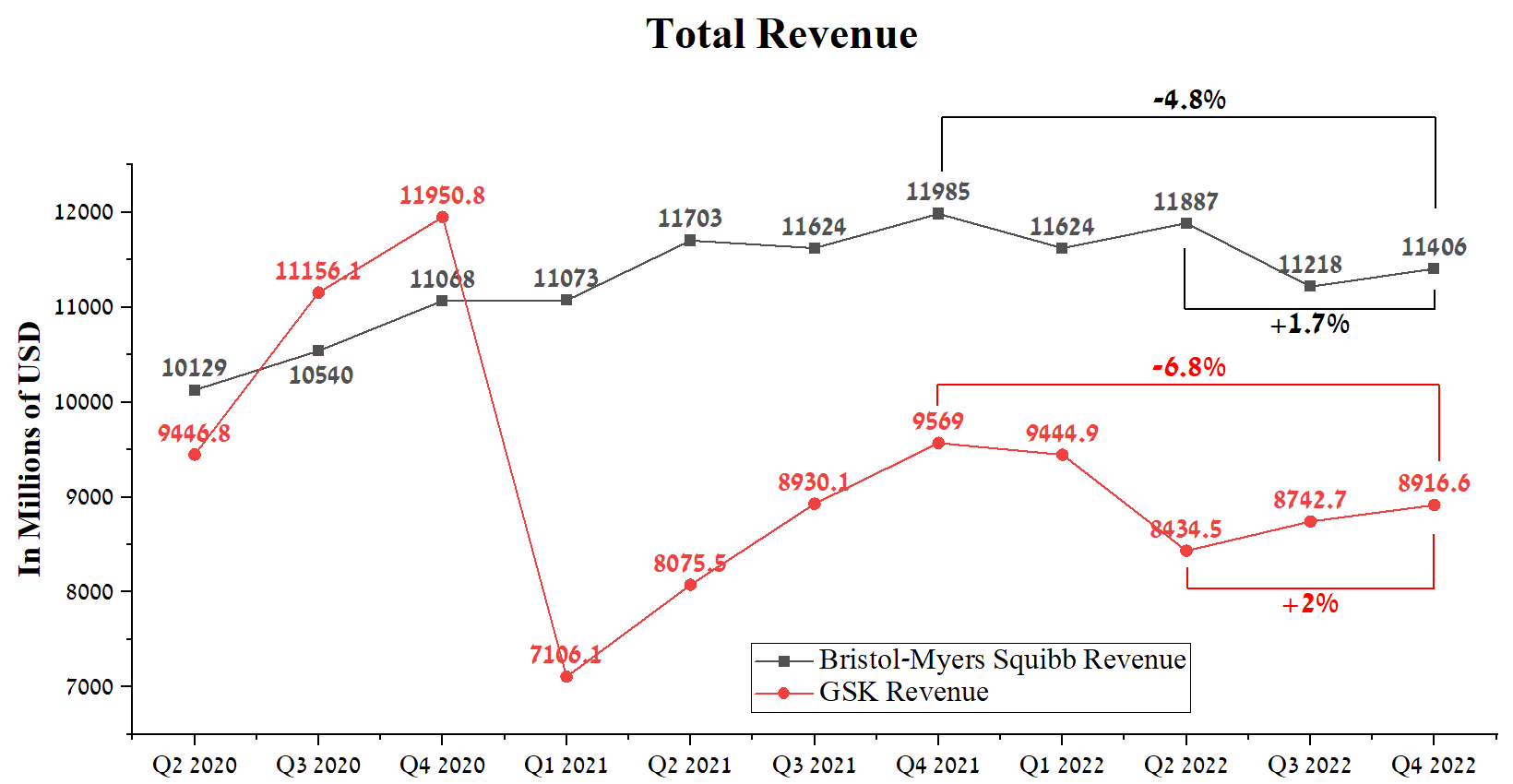

Bristol-Myers Squibb's revenue was $11,406 million in Q4 2022, up 1.7% QoQ but down 4.8% YoY. At the same time, GSK showed a worse trend, earning $8,916.6 million in the fourth quarter, showing a decrease of 6.8% compared to the 4th quarter of 2021.

Source: Author's elaboration, based on Seeking Alpha

{kind=link}

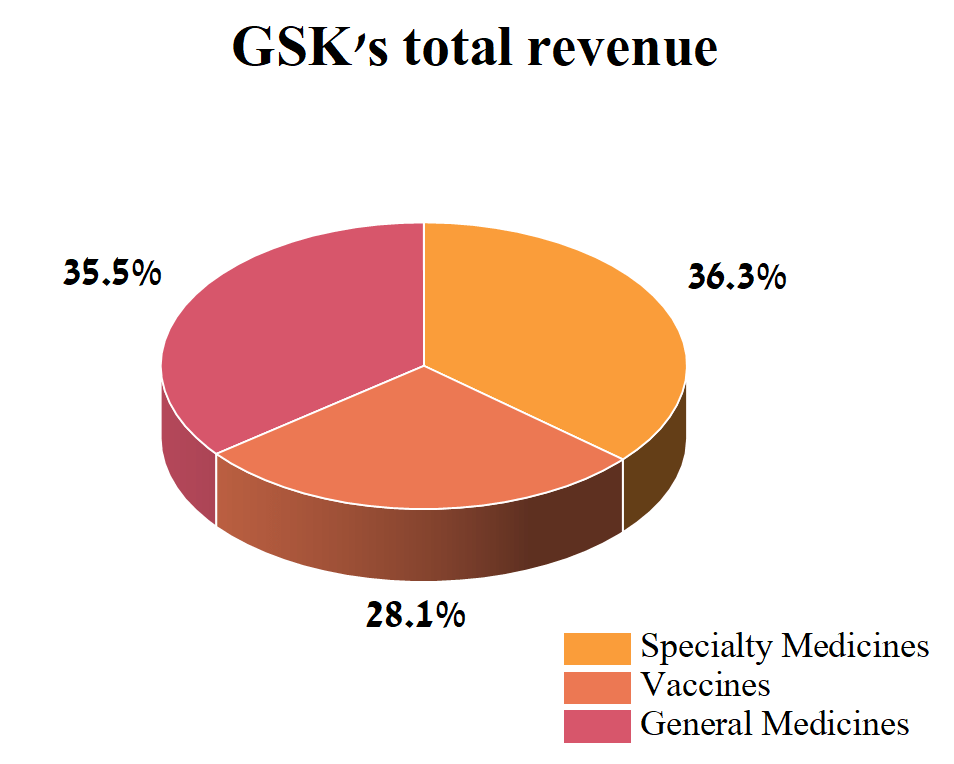

Both companies, being global pharmaceutical companies, have portfolios of dozens of approved drugs that bring in billions of dollars every year. But not all of them are equally important to the company's overall profit - some play a more critical role in its growth. GSK's business comprises three product groups: Vaccines, Specialty Medicines, and General Medicines.

Author's elaboration, based on quarterly securities reports

{kind=link}

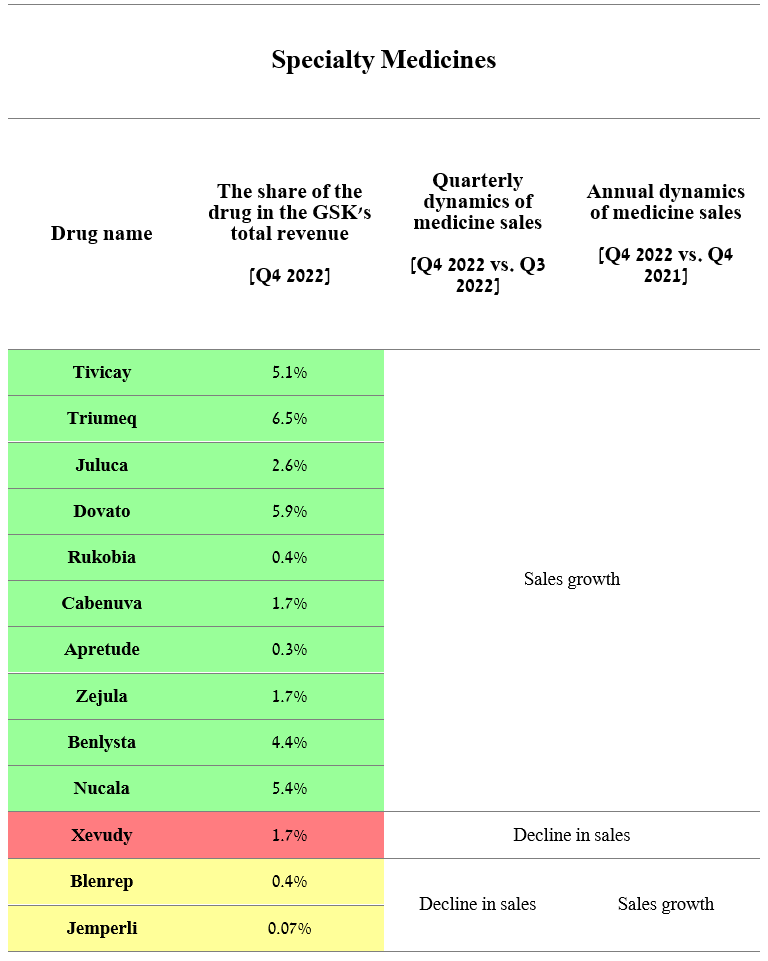

Sales of Specialty Medicines products, including medicines for treating respiratory diseases, HIV, oncology, and immune-mediated inflammatory diseases, were £2,681 in Q4 2022, down 3% from the previous year. This segment continues to be a key segment for the company, and therefore, the approved medicines and product candidates included in it play the most significant role in the company's future.

Author's elaboration, based on quarterly securities reports

{kind=link}

The decline in revenue in this segment was due to a sharp drop in sales of Xevudy (sotrovimab), a monoclonal antibody therapy used to treat COVID-19 and developed in partnership with Vir Biotechnology ( VIR ). The mechanism of action of this medicine is based on binding to the spike protein of SARS-CoV-2 with subsequent prevention of its entry into human cells and replication in them. However, due to the high emergence rate of new variants of COVID-19, this therapy has ceased to be effective against them, which led to a recommendation from the World Health Organization to suspend the use of Xevudy, and the FDA withdrew approval for its use in the United States. We believe that Xevudy sales will continue declining in the coming quarters due to lower COVID-19 cases and physician demand, reaching £95 million in 2023.

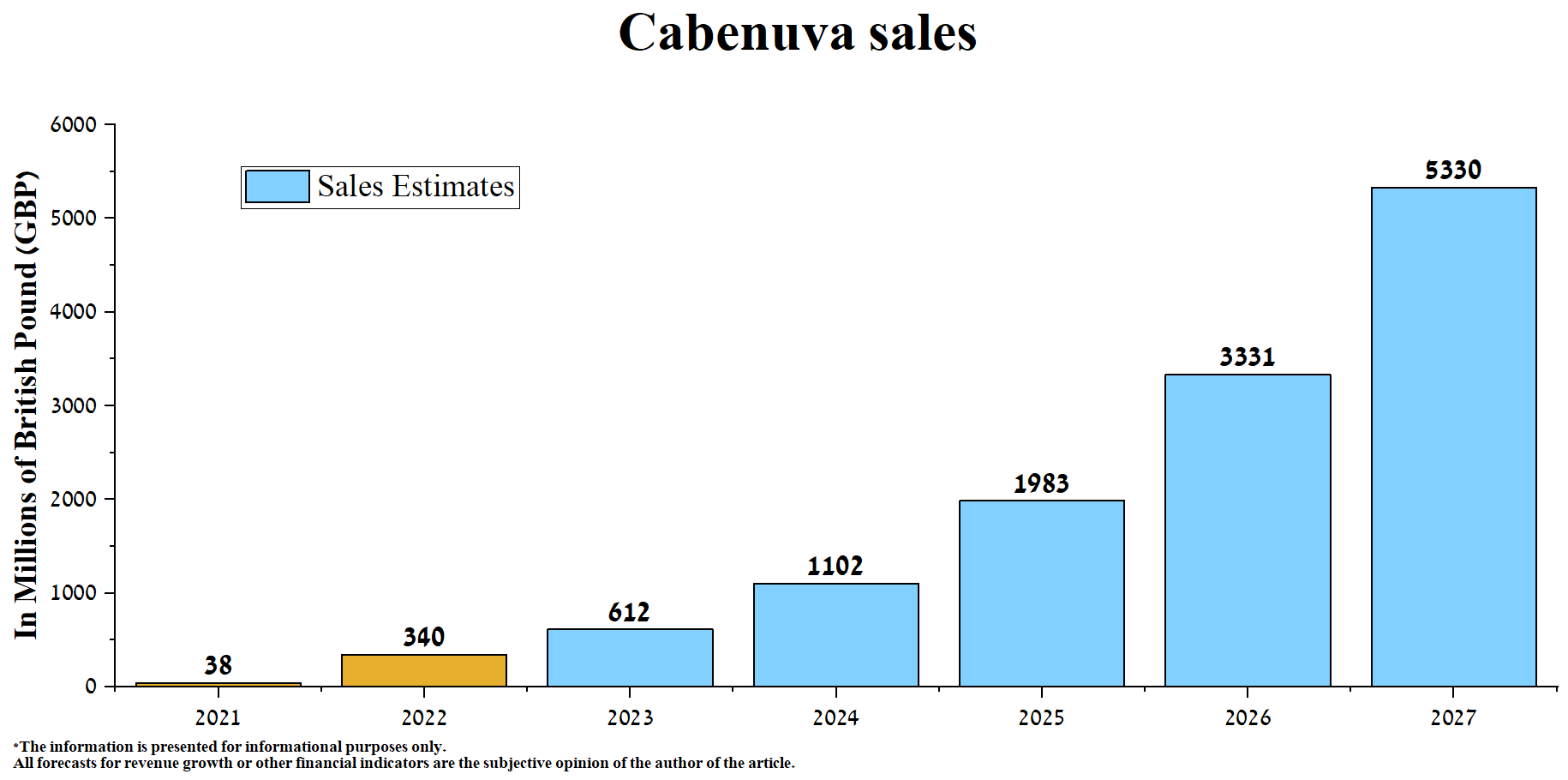

Excluding sotrovimab sales, Specialty Medicines' revenue rose 9.3% QoQ, driven by more robust demand for HIV drugs. In our estimation, Cabenuva continues to be GSK's gem in the multibillion-dollar HIV drugs market, thanks to the FDA's approval of bimonthly dosing. The FDA's favorable decision was based on a Phase 3b clinical trial demonstrating that bimonthly injections were as effective as monthly dosing. Decreased frequency of Cabenuva use will boost demand due to patients' desire to reduce the discomfort of daily oral pills like Biktarvy, which made Gilead Sciences ( GILD ) $10.39 billion in 2022. We expect Cabenuva to grow by 80% CAGR between 2023 and 2025 but will gradually decline from 2026 due to a label expansion of Sunlenca (lenacapavir), a long-acting HIV-1 capsid inhibitor given twice a year .

{kind=link}

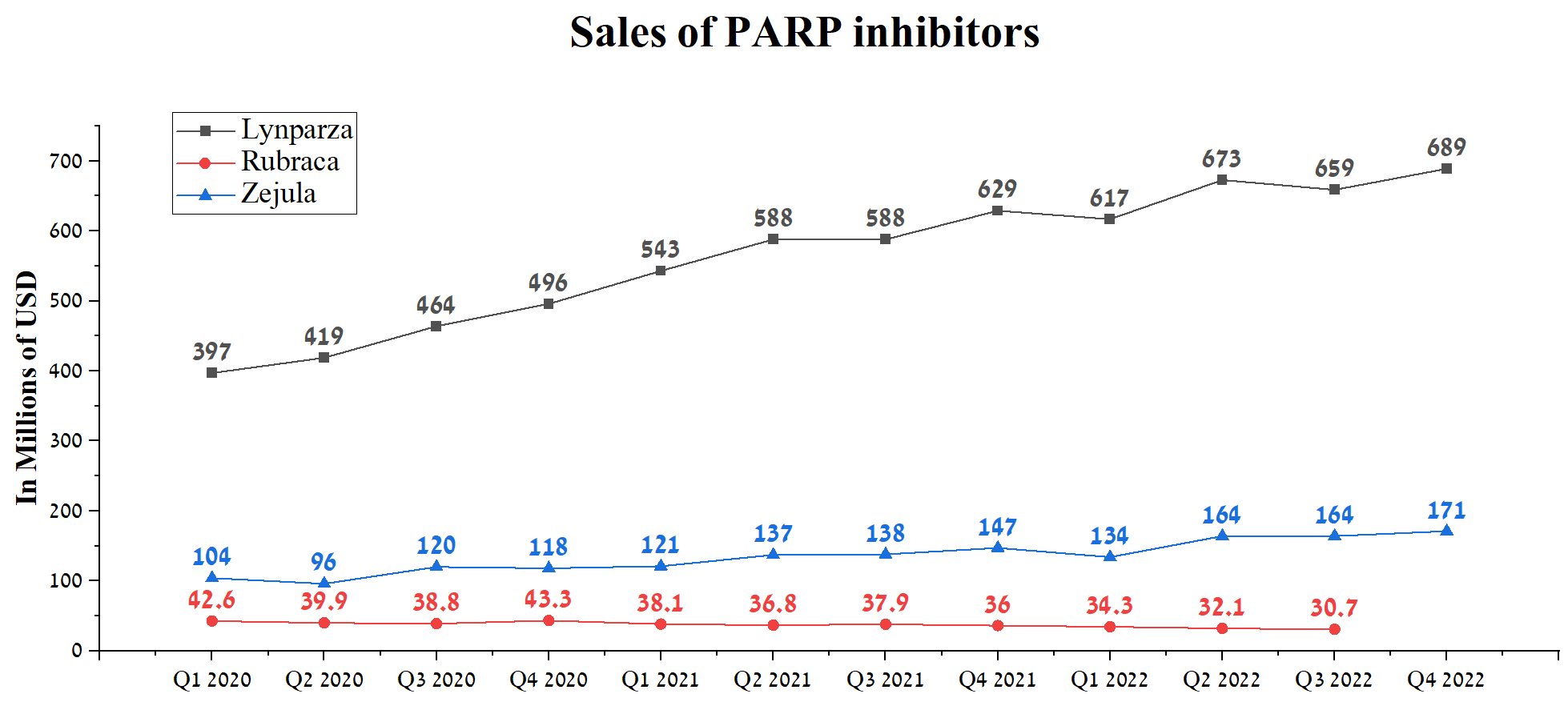

Unlike Bristol-Myers Squibb, the weak point of GSK's portfolio is anti-cancer drugs. GSK's best-selling oncology drug is Zejula, whose action is based on inhibiting the poly-ADP-ribose polymerase (PARP) enzyme, which plays a crucial role in repairing DNA damage. As a result of the inhibition of this enzyme, the cancer cells die, which in certain types of cancer leads to improved patient survival rates. The rate of sales of this medicine continues to be stable but has yet to begin to show a significant increase on a quarterly basis. In our estimation, the two main reasons are the discontinuation of Zejula sales in specific indications due to poor overall patient survival data in phase 3 clinical trial and high competition from AstraZeneca's Lynparza ( AZN ), Pfizer's Talzenna ( PFE ), and Clovis Oncology's Rubraca ( CLVSQ ).

Author's elaboration, based on quarterly securities reports

{kind=link}

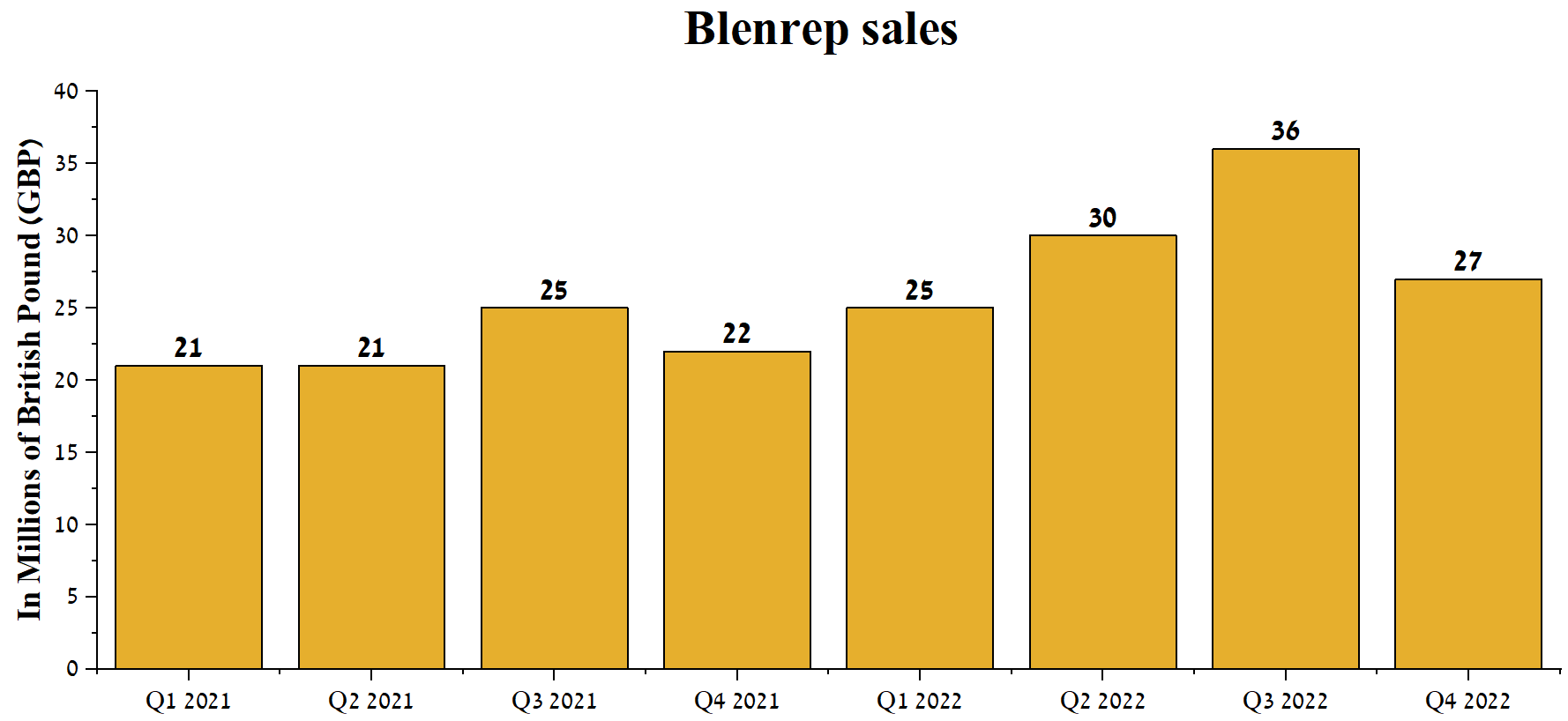

The second largest seller in GSK's oncology portfolio was Blenrep, used to treat certain patients with relapsed and refractory multiple myeloma (RRMM), and generated £27 million for the company.

Author's elaboration, based on quarterly securities reports

{kind=link}

In 2020, the FDA approved this drug under an accelerated approval pathway, but already in the 4th quarter of 2022, the company began the process of withdrawing Blenrep from the market due to the failed results of the phase 3 clinical trial in which the primary endpoint of the progression-free survival was not reached. As a result, we expect sales of this medicine to continue declining in the coming quarters. However, the situation may change only if the primary and secondary endpoints are achieved in two clinical trials, namely DREAMM-7 and DREAMM-8 , the results of which are expected in the second half of 2023.

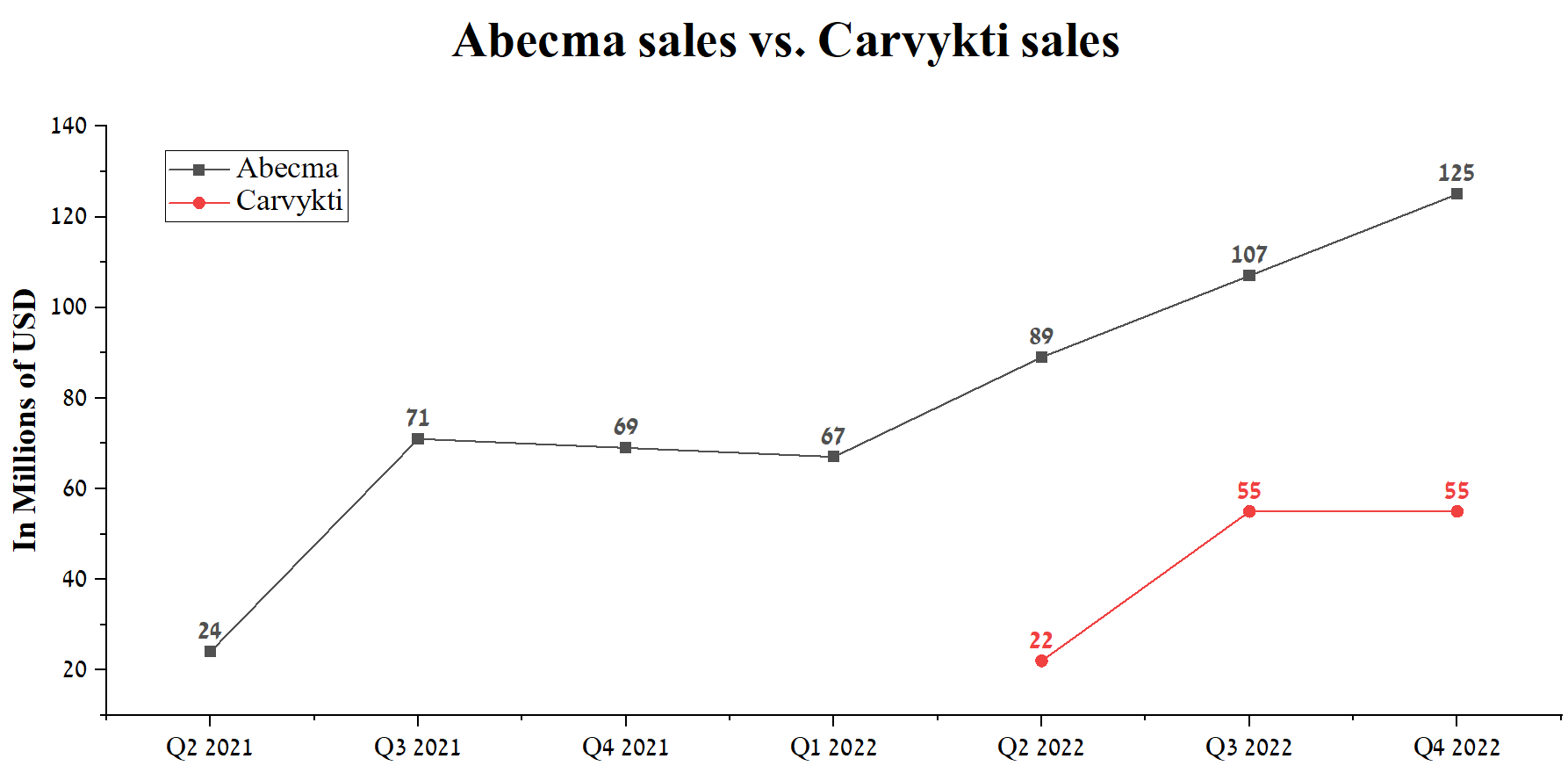

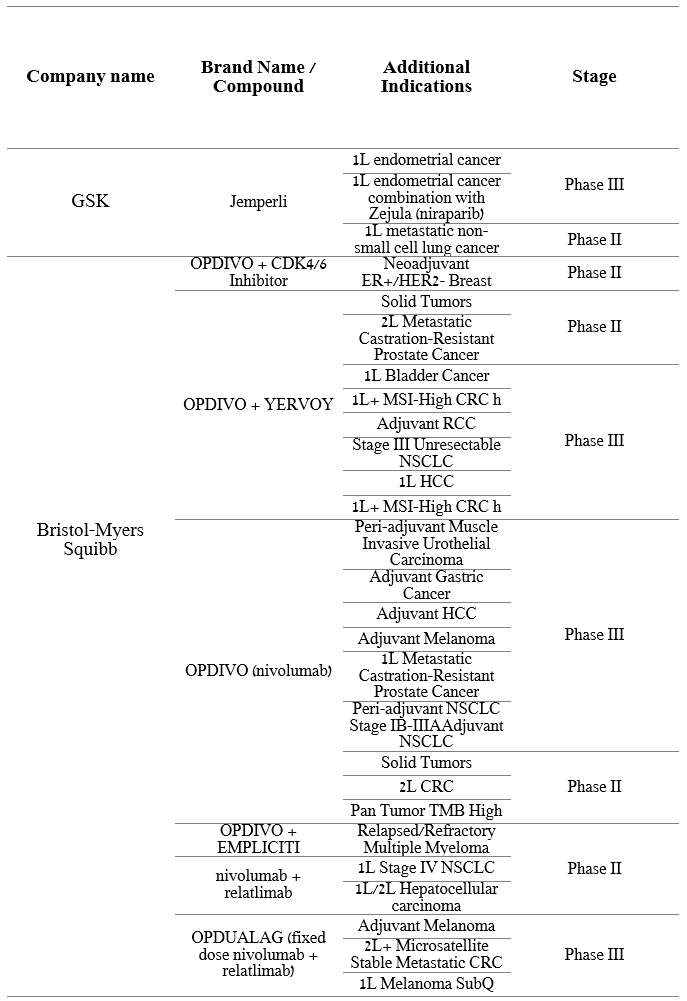

But it is already clear that GSK's failure is a positive development for Bristol-Myers Squibb/2seventy bio's Abecma ( TSVT ), J&J's Tecvayli ( JNJ ), and J&J/Legend Biotech's Carvykti ( LEGN ). Regulatory authorities have approved all three of these drugs for late-line multiple myeloma. Abecma sales were $125 million in the 4th quarter of 2022, up 16.8% from the previous quarter.

Author's elaboration, based on quarterly securities reports

{kind=link}

But more importantly, on February 10, 2023 , Bristol-Myers Squibb published the results of phase 3 clinical trial demonstrating that a group of patients with RRMM after two to four previous lines of therapy and taking Abecma showed a statistically significant improvement in PFS compared with a group of patients who received standard treatment regimens. The results of this clinical study were discussed in detail in the article "What To Expect From Bristol-Myers Squibb In 2023" . We believe there is a strong possibility that regulators will approve the use of Abecma in earlier lines of therapy for patients with this type of blood cancer, ultimately leading to a sharp increase in its sales.

Overall, Bristol-Myers Squibb is focused on drug development for patients suffering from diseases in rapidly growing therapeutic areas such as neurology, oncology, hematology, cardiology, and immunology.

Author's elaboration, based on quarterly securities reports

{kind=link}

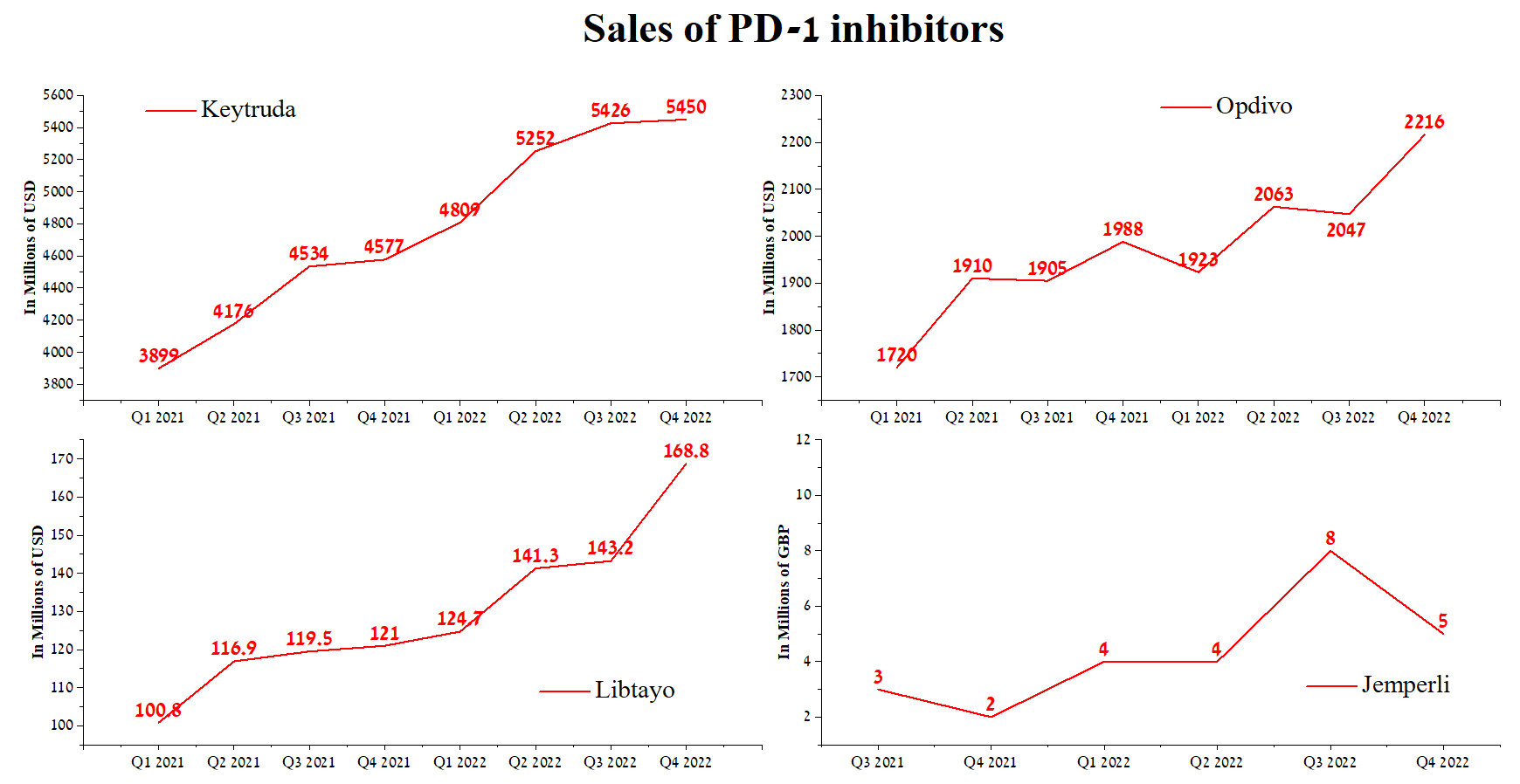

One of BMY's top-selling drugs is Opdivo, an immunotherapy drug whose mechanism of action is based on blocking the action of the PD-1 protein on T cells. As a result, the ability of cancer cells to mask is significantly reduced, and the activity of T-cells, which play one of the critical roles in the ability of the human immune system to kill cancer cells, increases. Opdivo sales were $2,216 million in Q4 2022, up 11.5% year-over-year, driven by expanded indications and increased demand for the combination of Opdivo with Exelixis' Cabometyx ( EXEL ), used to treat kidney, bladder, and gastric and esophageal cancers. The FDA and other regulatory agencies have approved several PD-1 inhibitors, including Merck's Keytruda ( MRK ), Regeneron Pharmaceuticals/Sanofi's Libtayo ( REGN ) ( SNY ), and GSK's Jemperli. Except for Jemperli, all three other medicines show quarterly and yearly sales growth.

Author's elaboration, based on quarterly securities reports

{kind=link}

We believe the main reason for the lack of significant growth in sales of GSK's drug is the high competition among immune checkpoint inhibitors and only two indications for use. At the same time, the program of clinical trials in which the active ingredient of Opdivo is involved is much richer than Jemperli, which once again confirms the status of Bristol-Myers Squibb as one of the leaders in the anti-cancer drug market.

Author's elaboration, based on quarterly securities reports

{kind=link}

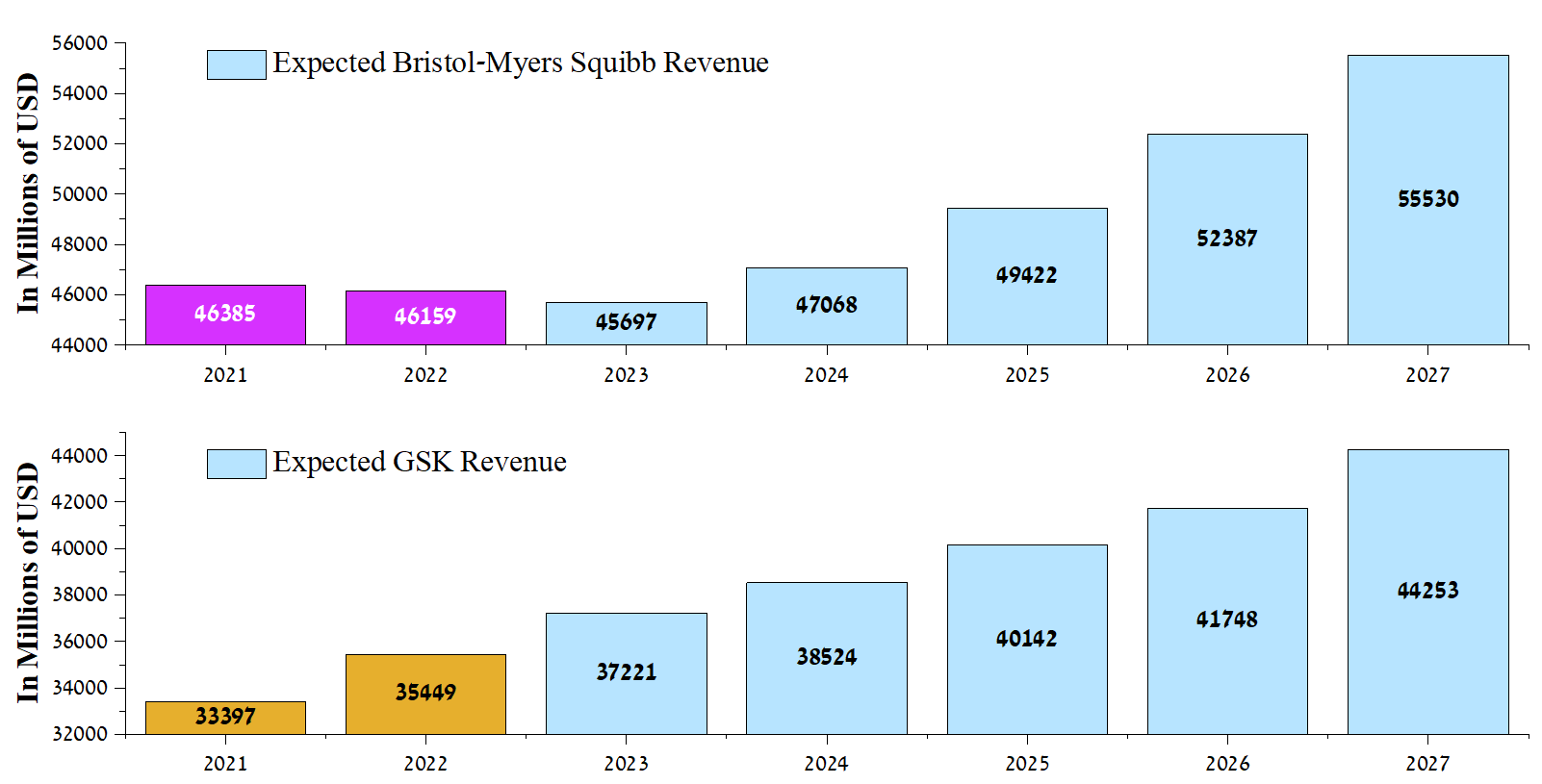

Given the portfolio of medicines and the product candidates of Bristol-Myers Squibb, we expect that the company's revenue will decrease slightly in 2023 and will begin to grow from 2024 due to the launch of new products and an increase in demand for newly approved drugs that will offset the impact of generic versions of Revlimid on the financial position of the company. At the same time, the British company's revenue will continue to grow from 2023 due to the growth in the share of its medicines in the HIV drug market and an increase in demand for GSK's vaccines.

{kind=link}

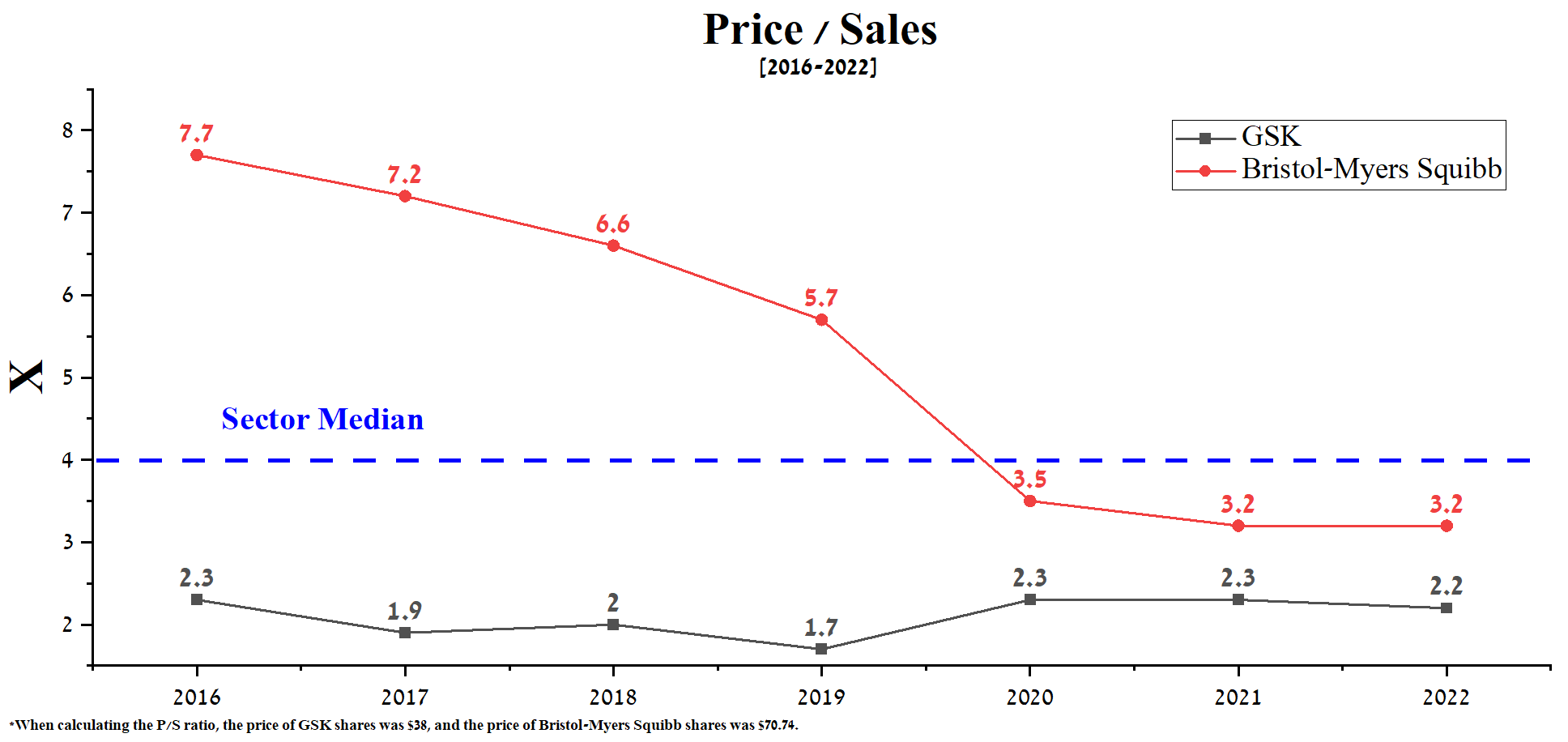

Both companies' price-to-sales (P/S) ratio is significantly lower than the average value for the healthcare sector. This suggests that the market underestimates Bristol-Myers Squibb and GSK, and the shares of these companies have upside potential in the future. Currently, GSK's P/S ratio is 2.2x, which is 45.6% lower than that of BMY, which means that one of the leaders in the UK pharmaceutical industry is an even more undervalued asset in the sector.

Source: Author's elaboration, based on Seeking Alpha

{kind=link}

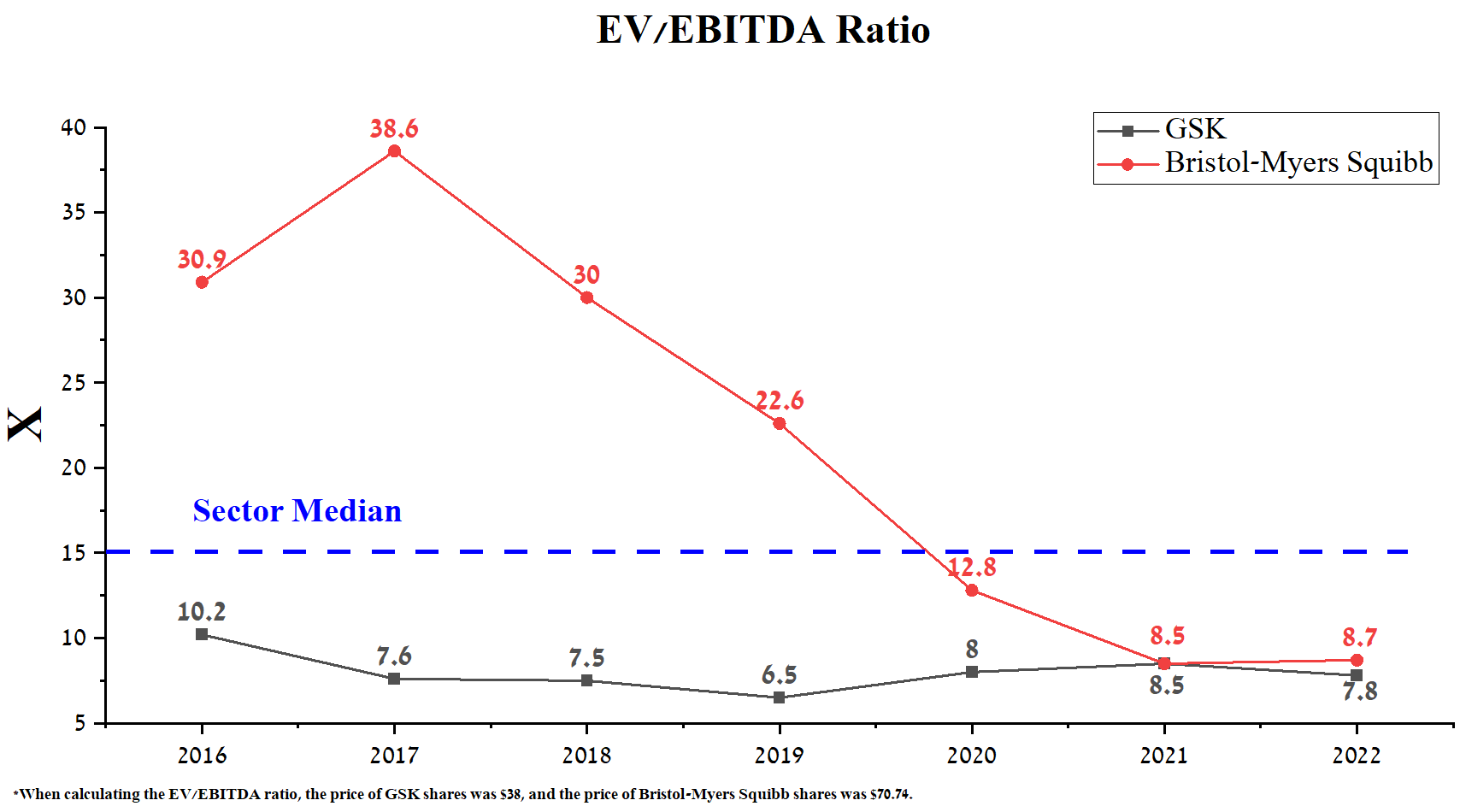

At the same time, Bristol-Myers Squibb's EV/EBITDA ratio is 8.7x, slightly higher than GSK's financial indicator. On the other hand, the EV/EBITDA ratio of the healthcare sector is 15.11x, which is significantly higher than both companies, which once again indicates that they are undervalued by the market relative to other players.

Source: Author's elaboration, based on Seeking Alpha

{kind=link}

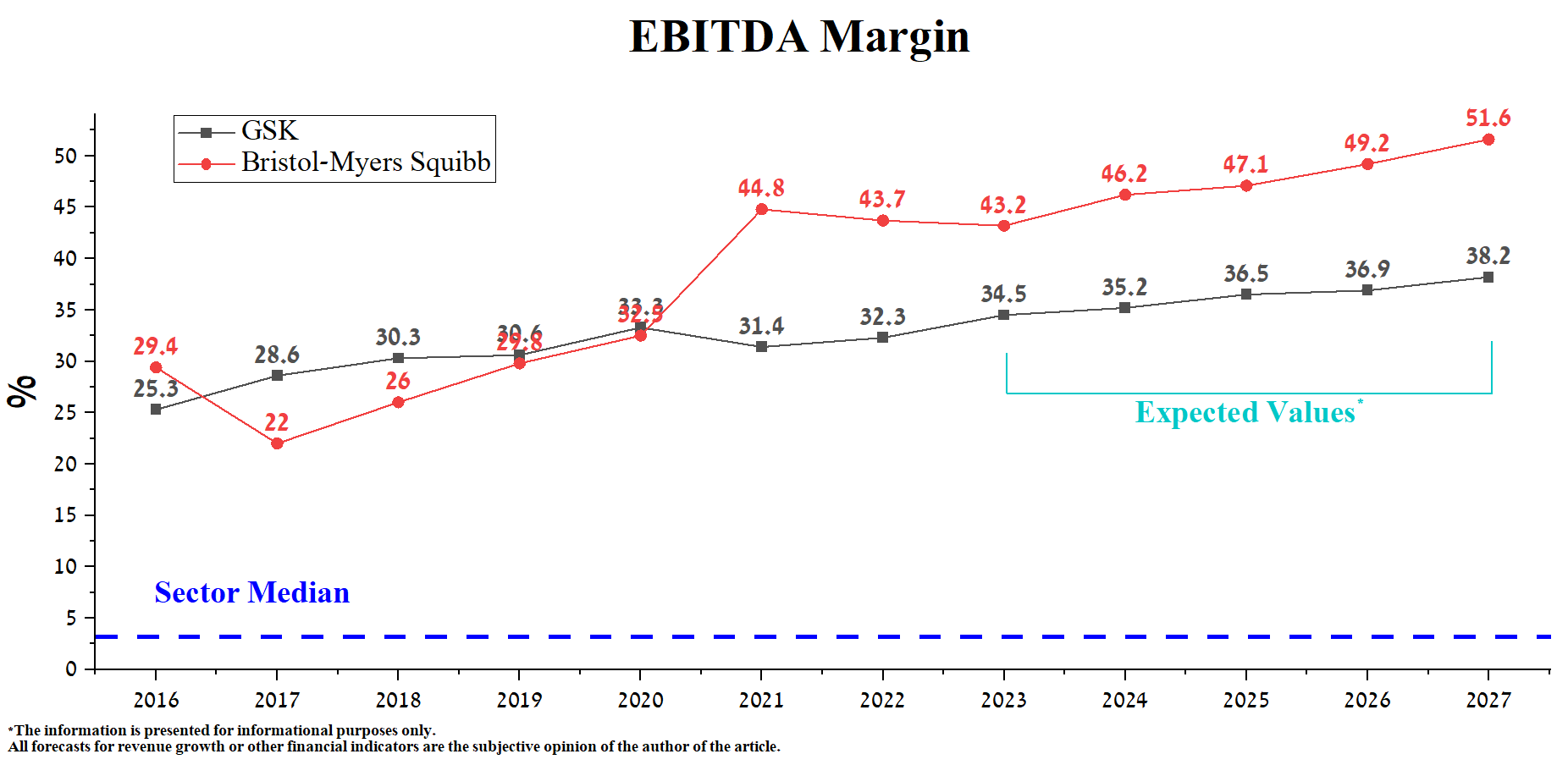

Bristol-Myers Squibb's EBITDA margin was 43.7% for 2022, which is 11.4% more than GSK. Bristol-Myers Squibb's higher business margin, coupled with more robust drug sales, is helping the company's ability to increase R&D spending and pursue a more aggressive M&A policy needed to maintain a leading position in oncology and hematology. We expect this figure to rise to 51.6% by 2027, driven by increased demand for Reblozyl, Opdivo, and Onureg and expanding indications for Abecma, Sotyktu, and Breyanzi.

On the other hand, there is a tendency for GSK's EBITDA margin to increase from year to year, and according to our estimates, it will grow to 38.2% by 2028. The key contributors to the growth of this financial indicator are the increase in demand for Cabenuva, Rukobia, and Nucala and the launch of new vaccines, including the respiratory syncytial virus vaccine candidate, which showed excellent results in protecting patients participating in the pivotal trial. The respiratory syncytial virus causes more than 470,000 hospitalizations and 33,000 adult deaths each year in high-income countries, according to information provided by GSK .

{kind=link}

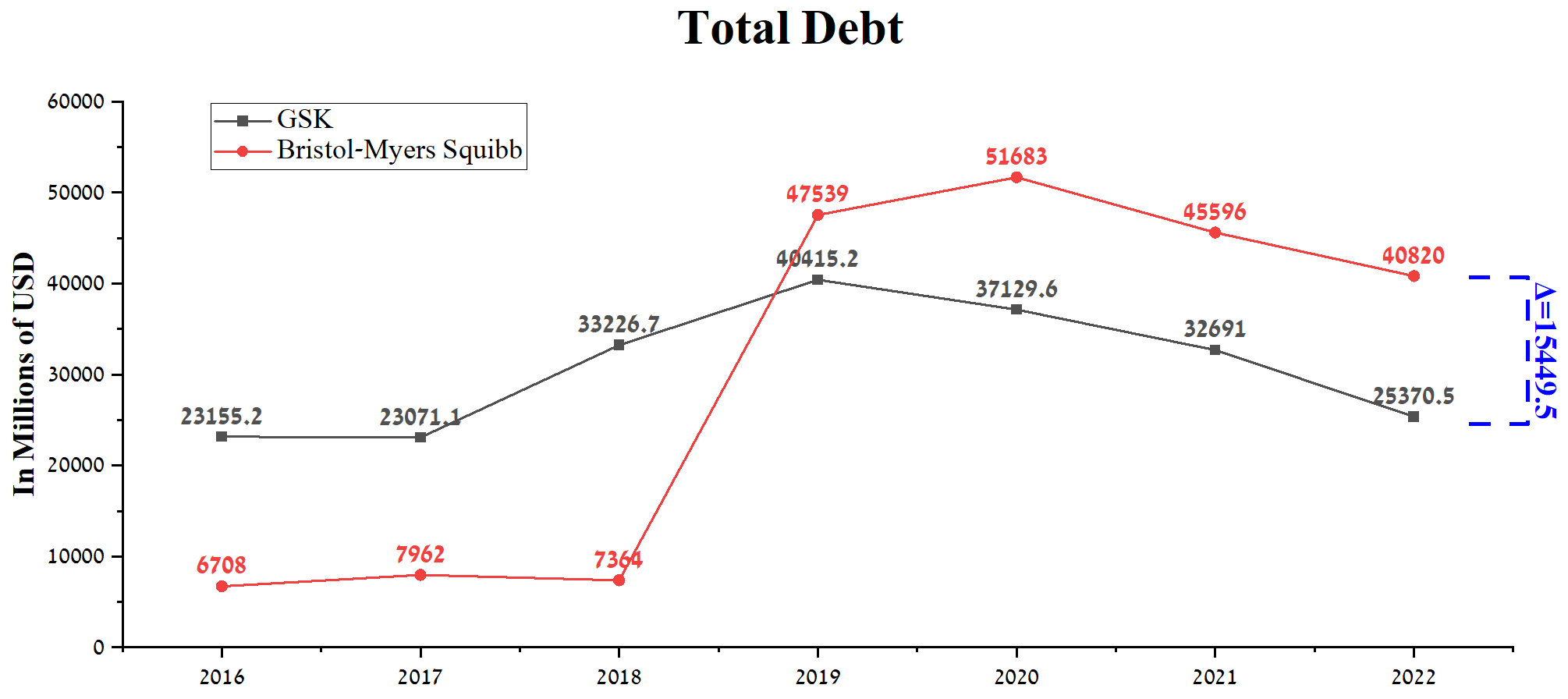

Bristol-Myers Squibb's total debt was about $40.8 billion at the end of 2022, down $4.78 billion from the previous year, thanks to the successful integration of Turning Point Therapeutics, Celgene, and MyoKardia. In contrast, GSK's total debt was about $25.4 billion at the end of Q4 2022, down $7.3 billion from Q4 2021. BMY's debt exceeds that of GSK by approximately $15.5 billion, one of the factors pointing to a stronger financial position for the British pharmaceutical company. In addition, given the lower interest rates on GSK's bonds, this positively affects lower cash flow spending on coupon payments to their holders.

Source: Author's elaboration, based on Seeking Alpha

{kind=link}

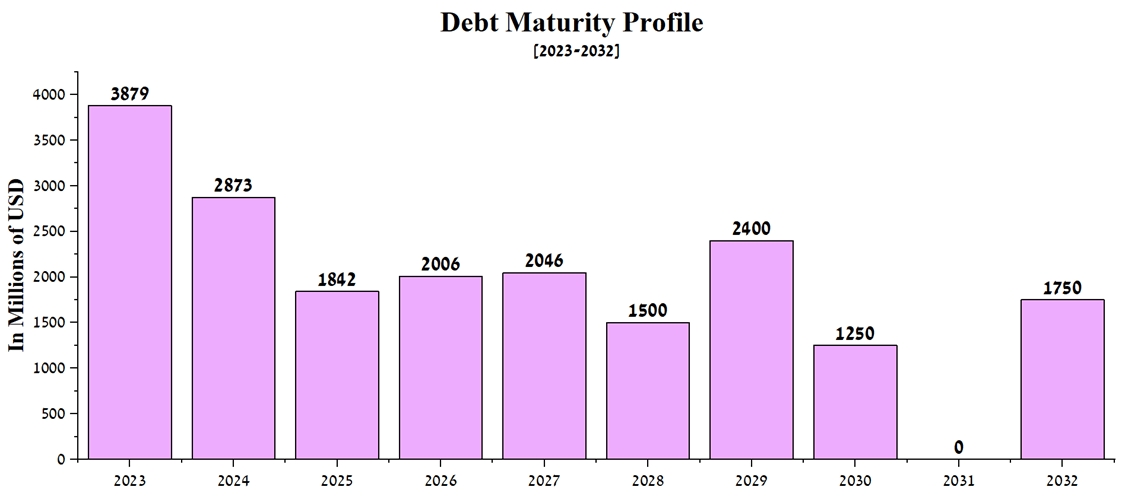

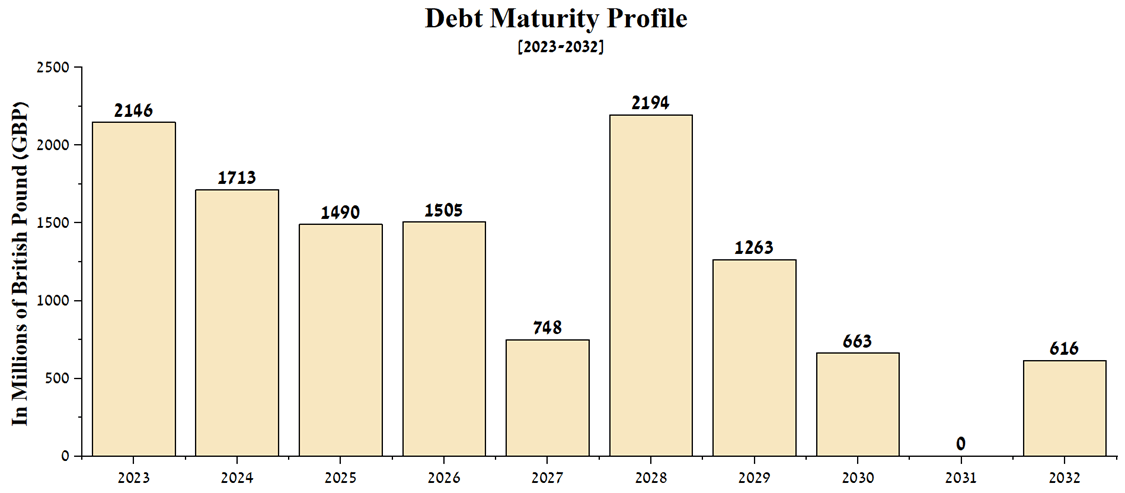

But at the same time, Bristol-Myers Squibb's EBIT amounted to $9,879 million, and, according to our estimates, the company will not have any difficulties with the redemption of senior notes in the period we analyze from 2023 to 2032.

Source: Author's elaboration, based on 10-K

{kind=link}

GSK is in a similar situation, with an EBIT of $8,851.3 million in 2022, up more than $1 billion from the previous year. According to our estimates, the British company will be able to redeem the bonds until 2032 without any problems.

Source: Author's elaboration, based on 20-F

{kind=link}

GSK's dividend yield is 3.58%, slightly higher than Bristol-Myers Squibb's 3.22%. These values are significantly higher than the average dividend yield of the healthcare sector, which is another factor that makes both companies attractive to long-term investors.

Source: Author's elaboration, based on Seeking Alpha

{kind=link}

But unlike GSK's management, Giovanni Caforio, CEO of Bristol-Myers Squibb, actively resorts to using the company's share buyback policy. In 2022, BMY bought back $8,001 million worth of shares, a record high in the company's history, and still has $7.2 billion in reserves set aside for this purpose. On the other hand, the British pharmaceutical company does not plan to carry out a repurchase of common stock until at least the end of 2023, which, in our estimation, makes GSK less attractive to investors relative to Bristol-Myers Squibb, especially in the current period of macroeconomic turmoil.

Source: Author's elaboration, based on Seeking Alpha

{kind=link}

Conclusion

GSK is one of the UK's largest pharmaceutical companies and is a leader in the treatment of respiratory and immune diseases, as well as offering one of the best therapies for HIV patients. On the other hand, Bristol-Myers Squibb is a leader in the treatment of oncological and hematological diseases. With the acquisition of MyoKardia, the company has strengthened its position in the multi-billion dollar cardiovascular drugs market, thereby reducing the financial risks associated with the loss of exclusivity of some blockbusters in the next six years.

Both companies have an extensive portfolio of product candidates and medicines, growing dividend payouts, and high margins, which make GSK and Bristol-Myers Squibb worthy of consideration as long-term assets during macroeconomic and geopolitical tensions. With a more diversified pipeline of product candidates targeting cancer and autoimmune diseases, higher business margins, an aggressive share buyback policy, and continued acquisitions of promising products in the pharmaceutical industry, we believe that Bristol-Myers Squibb is more favorable in the long-term and more likely to outperform the S&P 500 and the iShares Biotechnology ETF significantly.

For further details see:

GSK Vs. Bristol-Myers Squibb: Who's More Underrated By Mr. Market