GNTY - Guaranty Bancshares Q2 2023 Review: Dividends Valuation And Risks

2023-07-18 10:46:54 ET

Summary

- Guaranty Bancshares, Inc. reported mixed Q2 2023 results, with total assets falling due to decreases in Federal Home Loan Bank advances, deposits, Fed funds, securities portfolio, and loans.

- Despite these setbacks, the bank reported earnings per share of $0.81, surpassing estimates by $0.25, and revenues of $32.58 million, beating expectations by $3.17 million.

- Despite its strong dividend history and robust liquidity, concerns are raised about the bank's future profitability due to a slight dip in earnings and a slowdown in new loan origination.

Thesis

Guaranty Bancshares, Inc. (GNTY) reported a mixed quarter, experiencing both successes and setbacks with total assets falling 4.5% due to decreases in Federal Home Loan Bank advances, deposits, Fed funds, the securities portfolio, and loans. Despite these challenges, the bank reported earnings per share of $0.81, surpassing estimates by $0.25, and revenues of $32.58 million, a year-on-year decrease of 1.97% but still beating expectations by $3.17 million. In this article, I point out that despite its history of strong dividends and robust liquidity, the slight dip in earnings and a slowdown in new loan origination raise questions about the bank's future profitability. Therefore, I recommend Guaranty Bancshares as a "hold" at this time.

Brief Company Profile

Founded in 1913 and calling Addison, Texas, its home for over a century, Guaranty Bancshares Inc. functions as the holding company for Guaranty Bank & Trust, N.A. with a product suite that stretches across commercial and consumer banking, catering to the needs of small- to medium-sized businesses, seasoned professionals, and everyday individuals.

Guaranty Bancshares Q2 2023 Earnings Highlights

Guaranty Bancshares ushered out the quarter with a blend of victories and setbacks. The bank's total assets dipped by a notable $150 million, or 4.5%, wrapping up June with a standing balance of $3.21 billion. The key players in this slide were a $145 million downswing in Federal Home Loan Bank advances and a drop in deposits by $20 million. A shrinkage in Fed funds, the securities portfolio, and loans also played their part, trimming $50 million, $46 million, and $44 million respectively.

Notwithstanding the downsize in the securities portfolio, Guaranty Bancshares masterfully matured $25 million in short-term treasuries in the quarter. The bank stayed on its path of loan decrease, a $44 million or 1.8% period-to-period reduction, dragging the total loans to the tune of $2.3 billion. Yet, there was a silver lining as the pace of customer deposit shift decelerated relative to Q1, non-interest bearing deposits firmly holding their ground at 35% of total deposits.

While total equity took a slight hit of $3 million due to stock acquisitions - the bank buying back roughly $8.1 million of its own shares (2.7% of outstanding shares) - Guaranty Bancshares kept up its trend of dividend payments, registering 33 uninterrupted years of augmenting dividends, and maintained a healthy yield at 3.4%.

Guaranty notched up earnings of $9.6 million for the quarter, incorporating a one-off net gain of $2.2 million from selling a portion of correspondent bank stock. Stripping out this gain and a realized loss of $322,000 from portfolio restructuring, the core operating earnings for the quarter hit a respectable $7.7 million, translating to earnings per share of $0.65. The bank flaunted a return on assets ((ROA)) of 1.17% and a return on equity ((ROE)) of 12.87%.

Even against the backdrop of a slight dip in net interest income to $24.7 million, Guaranty marked a rise in loan yield by 24 basis points and securities yield by roughly 16 basis points. It demonstrated resilience in the competitive banking landscape by ramping up the cost of its interest-bearing liabilities to hold onto its customer deposit base, pushing up the total cost of deposits by 35 basis points to 1.53%.

As far as non-interest income is concerned, Guaranty recorded a solitary gain of $2.8 million before tax, while the core non-interest income for the quarter added up to $5.4 million. Expenses crept up by $504,000 over the quarter, primarily on the back of escalating FDIC insurance and software costs, as well as some one-time charges linked to the annual meeting. The bank sported an efficiency ratio of 62.84%.

In terms of lending, the quarter saw the origination of new loans worth $65 million, notwithstanding the decelerating activity courtesy of soaring interest rates and stringent underwriting. Non-performing assets stayed low, constituting a mere 0.11% of total assets. The bank declared zero provision for credit losses for the quarter, attributing it to the dwindling loan portfolio and the resolution of non-performing loans, eliminating the requirement for such a provision. The quarter-end allowance for credit losses ((ACL)) coverage was firm at 1.36%.

To round off, in spite of a drop in deposits, Guaranty managed to uphold robust liquidity, with a liquidity ratio of 12.9% and contingent liquidity around the ballpark of $1.5 billion. Furthermore, the capital ratios stayed sturdy, factoring in the repurchase of shares. The total equity to average assets ratio remained at 9.1%, and even accounting for all probable losses in the portfolio, the ratio would still hold its ground at a commendable 8.3%.

Expectations

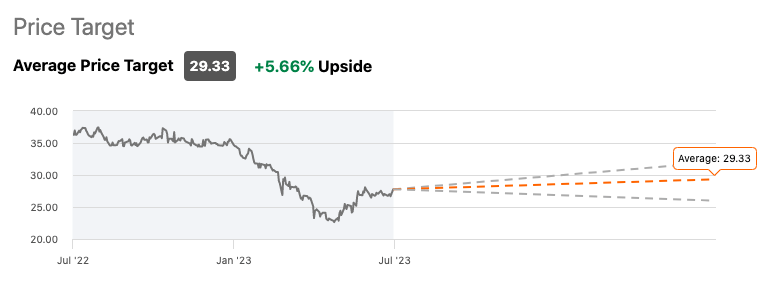

Guaranty Bancshares is currently covered by four Wall Street analysts who have an average weighted " Buy " rating on the stock with a rather meager price target upside outlook of only +5.66%.

{kind=link}

Performance

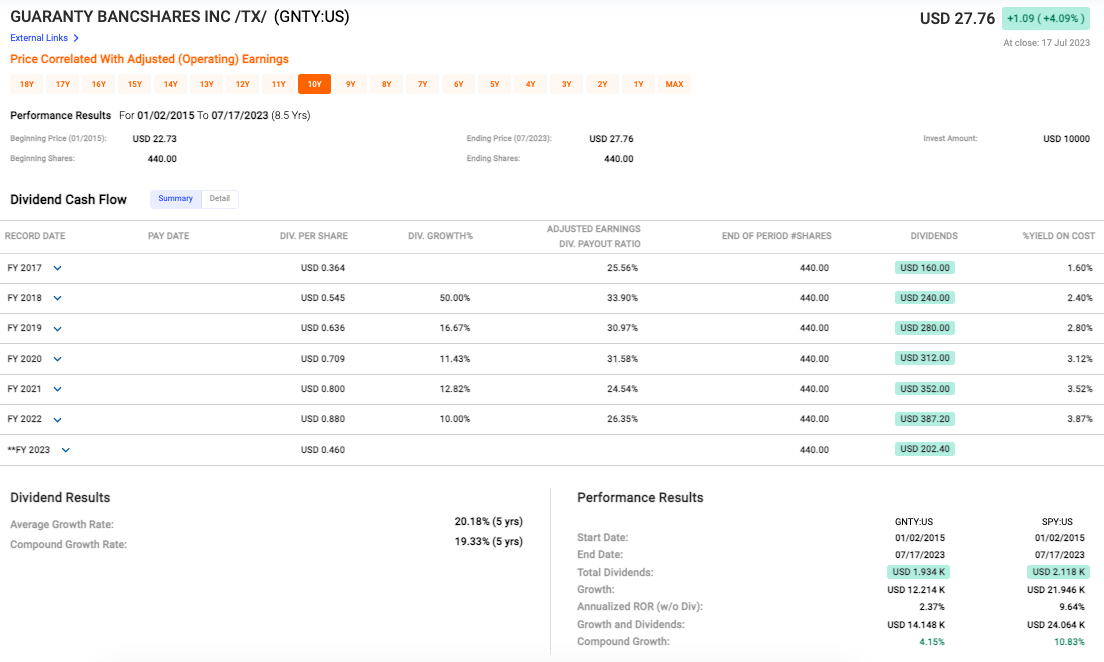

First, the bank's share price has appreciated by 22% since 2015 (see data below) compared to its performance relative to broader markets ( S&P 500 Index ). While this growth is somewhat commendable, its relative progress to that of wider market conditions may not be. The S&P has seen more than double the growth of GNTY in the same period.

{kind=link}

When we examine dividends, it's clear GNTY has a solid dividend policy, with a five-year average growth rate of 20.18%. In fact, the dividends have grown consistently up until FY 2023. Moreover, the Dividend Payout Ratio has remained reasonably stable over the years, hovering around the 24-33% range until FY 2022. This demonstrates a balance between reinvestment in the business and payout to shareholders, which is a positive sign of healthy capital allocation.

Valuation

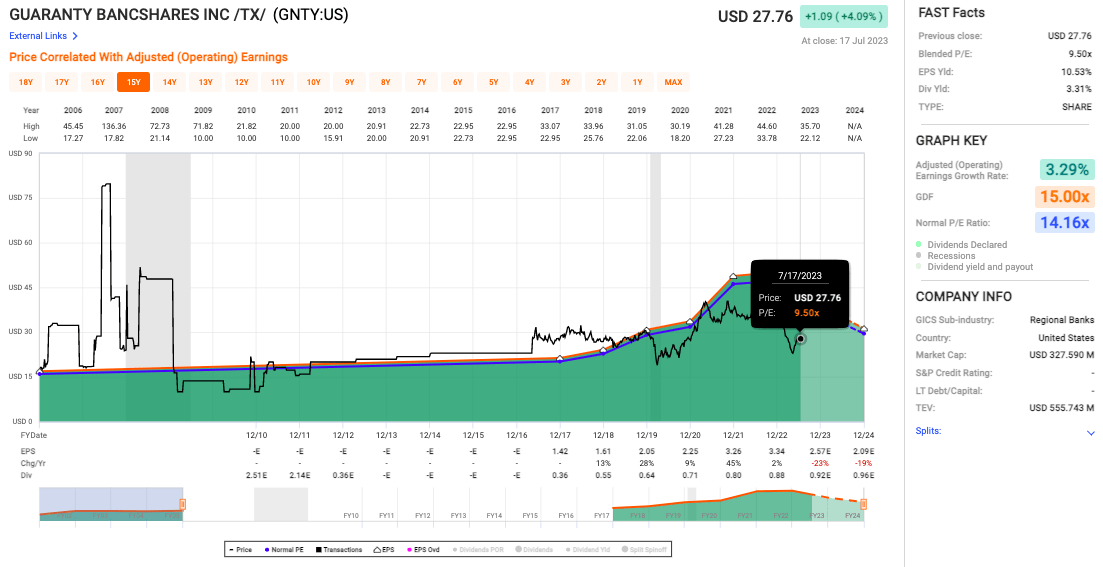

Starting off with the blended P/E ratio of 9.50x (see chart below) seems somewhat low when compared to the historical standard of around 15.00x for this sector. Generally, a lower P/E ratio may indicate that the stock is undervalued.

{kind=link}

Also, the bank's adjusted operating earnings growth rate is reported to be 3.29%, a somewhat modest figure. This slow growth, however, is juxtaposed against an EPS yield that registers at a healthy 10.53%. Generally, a high EPS yield can mean the company is generating a good level of earnings relative to its share price, which might suggest undervaluation. Combine this with the dividend yield of 3.31%, and it seems that Guaranty Bancshares is providing a decent return to shareholders, which, again, conflicts with the low P/E ratio and the modest earnings growth rate.

Risks & Headwinds

First off, the Federal Home Loan Bank advances and deposits' contraction can signal a curtailed reliance on these traditionally stable funding sources. Simultaneously, the contraction in the securities portfolio and loans might suggest the bank is taking a conservative stance towards risk management, perhaps in response to macroeconomic uncertainties or potentially even changes in their strategic focus.

The financials appear to echo this, as the bank reported a dip in earnings. The total earnings stood at a modest $9.6 million, whereas the core operating earnings amounted to $7.7 million. This earnings decline is an undeniable red flag, showcasing a noticeable downward trend in profitability. To add insult to injury, the bank also recorded a contraction in the net interest margin by 5 basis points, suggesting a compression in the bank's core lending business, which could impact the long-term sustainability of their earnings.

And then there's the slowdown in new loan originations. The bank seems to be experiencing setbacks in its lending operations with loan volumes down nearly $44 million during this quarter compared to last. This may signal a reduction in lending business which could have serious ramifications on core profitability and future growth prospects of the bank.

As well, bank deposits have seen a substantial decline, particularly non-interest bearing accounts. Such an event might hinder funding cost management strategies by forcing it to use more costly funding sources and, ultimately, diminish its profitability.

Final Takeaway

I would rate Guaranty Bancshares shares as a "hold." While the bank exhibits commendable resilience amid falling assets, a notable reduction in loan volume, the contraction of deposits, and a decrease in net interest income suggest potential future challenges. Despite its strong dividend history and strong liquidity, the slight dip in earnings, alongside the general slowdown in new loan origination, also raises concerns about profitability.

For further details see:

Guaranty Bancshares Q2 2023 Review: Dividends, Valuation, And Risks