DBI - Guess? Makes For A Mediocre Fit

2023-09-28 17:40:02 ET

Summary

- Guess? has a history of volatile financial results and is considered a mediocre company in the apparel and accessories space.

- The company's revenue, profits, and cash flows fluctuate, and there are concerns about consumer spending moving forward.

- While the stock is cheap on an absolute basis, there are better prospects in the industry, leading to a 'hold' rating for Guess?.

The apparel and accessories space is known for being incredibly challenging. While the companies that do succeed here can capture tremendous growth, there are many more firms that either struggle or achieve only mediocre results. In the mediocre category, one company that I would like to point to is Guess? ( GES ). For those who don't know, Guess? Operates as a lifestyle collections company that focuses on the production, sale, and marketing, of apparel and accessories for men, women, and children.

For the most part, the enterprise targets the youngest generations, though it does have a line of clothing for those aged 40 and older. The reason why I call the enterprise mediocre stems from the fact that revenue, profits, and cash flows, are all over the map. In any given quarter or year, you will see some volatility that places one particular metric worse than the year prior, while another metric is better. On an absolute basis, shares of the company are cheap. But when you compare the enterprise to similar firms, you will see that there are better prospects that can be had. To make matters worse, while consumer spending has so far been robust this year, there are concerns about what the picture might look like moving forward. So to have a company post mediocre results in good times indicates that the picture during bad times might not be so pleasant. Given these factors and offset, to some extent, by how cheap shares are on an absolute basis, I have decided to keep the enterprise rated a 'hold' for now.

Nothing special

In early January of this year, I found myself wondering what the picture might look like for Guess? moving forward. Leading up to that point, I had the enterprise rated a 'buy'. And in the months in which that rating applied, performance achieved by shares was quite positive. The stock had generated a return for investors of 12.7% at a time when the S&P 500 had dropped by 6.8%. But after factoring that appreciation in and looking at updated financial data, I felt as though a downgrade to a 'hold' rating made the most sense. Since that downgrade, the stock has pulled back about 1.4%. This drop occurred at the same time that the S&P 500 has risen by 9.9%. So while the enterprise did perform worse than what I would have anticipated following my downgrade, the general idea of downgrading it seems to have been correct.

{kind=link}

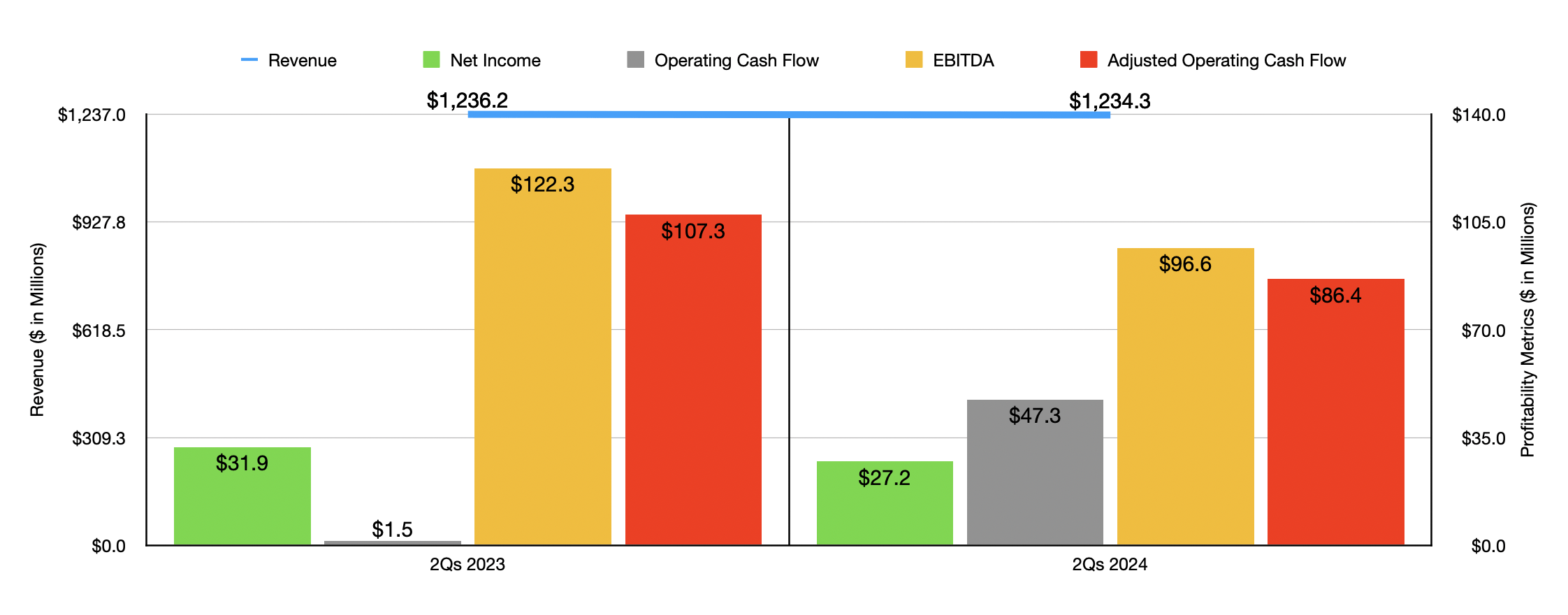

Fast-forward to today, and we have an interesting picture. Financial performance has been very volatile. As an example, we need only look at data covering the first half of the 2024 fiscal year . Revenue for the company totaled $1.23 billion. That was down slightly from the $1.24 billion reported one year earlier. The decrease was driven by foreign currency fluctuations. Without that, revenue would have risen by 1%, thanks to a combination of positive comparable store sales and net new concession revenues. Unfortunately, some of this was offset by a 2% decline in wholesale revenue.

On the bottom line, the picture for the company worsened. Net income dropped from $31.9 million to $27.2 million. Despite the increase in sales, Guess? suffered from multiple issues. But the biggest, by far, was a surge in selling, general, and administrative expenses from 34.4% of revenue to 37.3%. Management attributed this, for the most part, to $27 million of higher costs related to store labor, investments made in infrastructure, and inflationary pressures. A change in business mix impacted this crossed item by about $3 million, and the company did not have the benefit of COVID-related government subsidies that it enjoyed the year prior. Last year, those helped the firm to the tune of $11 million during the first half. Other profitability metrics have been volatile as well. It is true that operating cash flow shot up from $1.5 million to $47.3 million. But if we adjust for changes in working capital, we get a decline from $107.3 million to $86.4 million. Meanwhile, EBITDA for the company fell from $122.3 million to $96.6 million.

{kind=link}

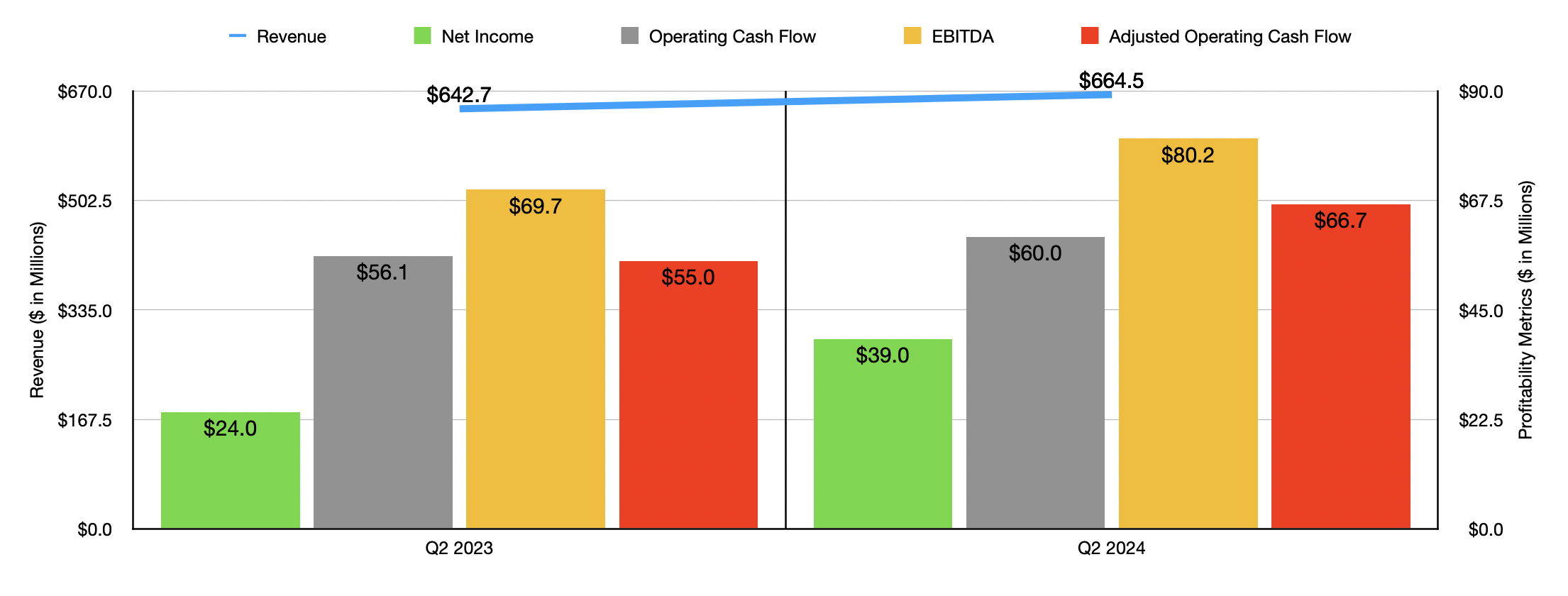

To be perfectly fair to the company, the second quarter of the fiscal year looked a lot better than the first quarter did. Revenue in the second quarter totaled $664.5 million. That's an increase of 3.4% over the $642.7 million reported one year earlier. The same factors that helped to offset a lot of the pain in foreign currency fluctuations during the first half of the year in its entirety were responsible for this increase. With revenue rising, all the company's profitability metrics also improved. Net income jumped from $24 million to $39 million. As the chart above illustrates, operating cash flow, adjusted operating cash flow, and EBITDA all increased year over year as well. The company benefited during this time not only from the increase in sales, but also from a favorable product mix, price increases, and lower markdowns, all of which more than offset the higher selling, general, and administrative expenses.

{kind=link}

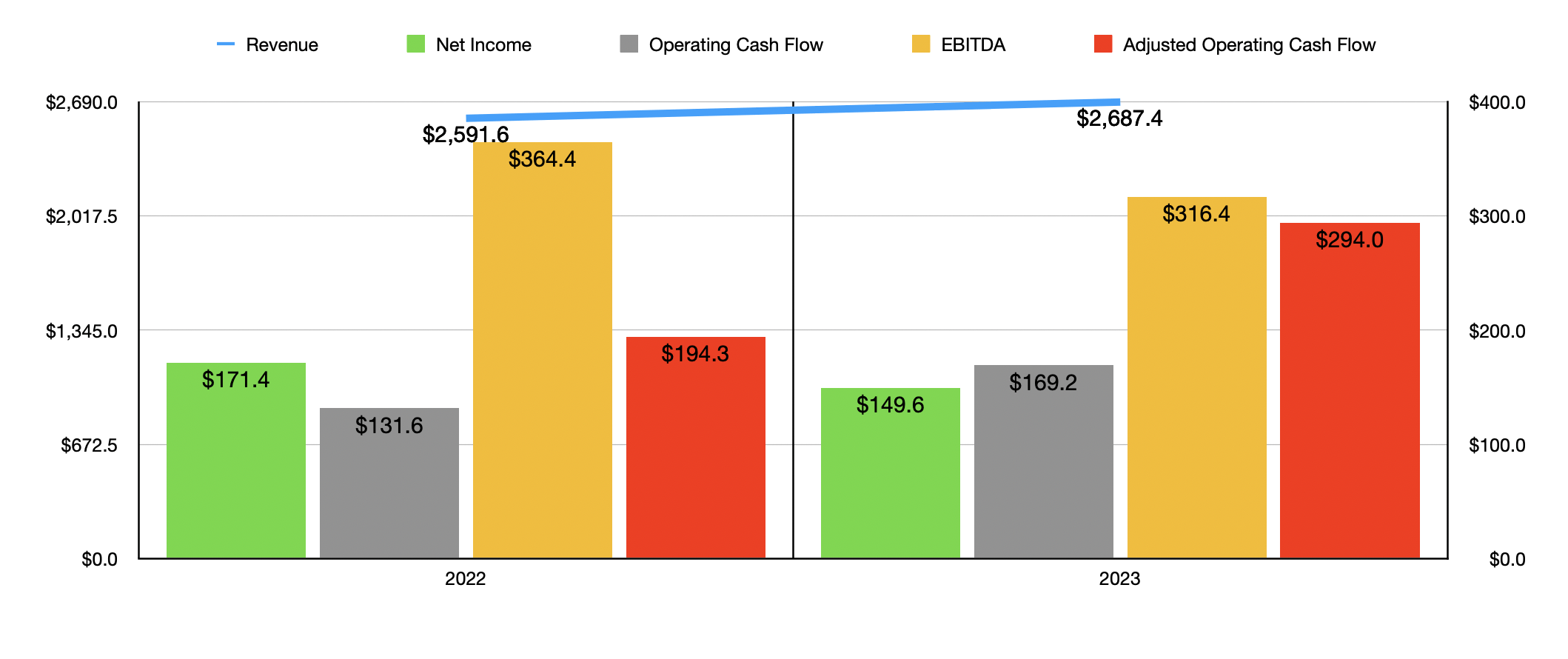

For the current fiscal year, management has forecasted revenue growth of between 2.5% and 4%. Earnings per share should be somewhere between $2.22 and $2.37, with adjusted earnings of between $2.88 and $3.08. Sticking with GAAP earnings, I calculated net profits for the year of roughly $160.3 million. That would be a bit above the $149.6 million reported for 2023 but still below the $171.4 million reported the year prior. Management forecasted an operating cash flow of $240 million. While this would be an improvement over the $169.2 million reported for 2023, it would be lower than the $294 million adjusted figure for that year. No guidance was given when it came to EBITDA. But based on performance during the first half of the year, I have this estimate coming in at around $249.9 million.

{kind=link}

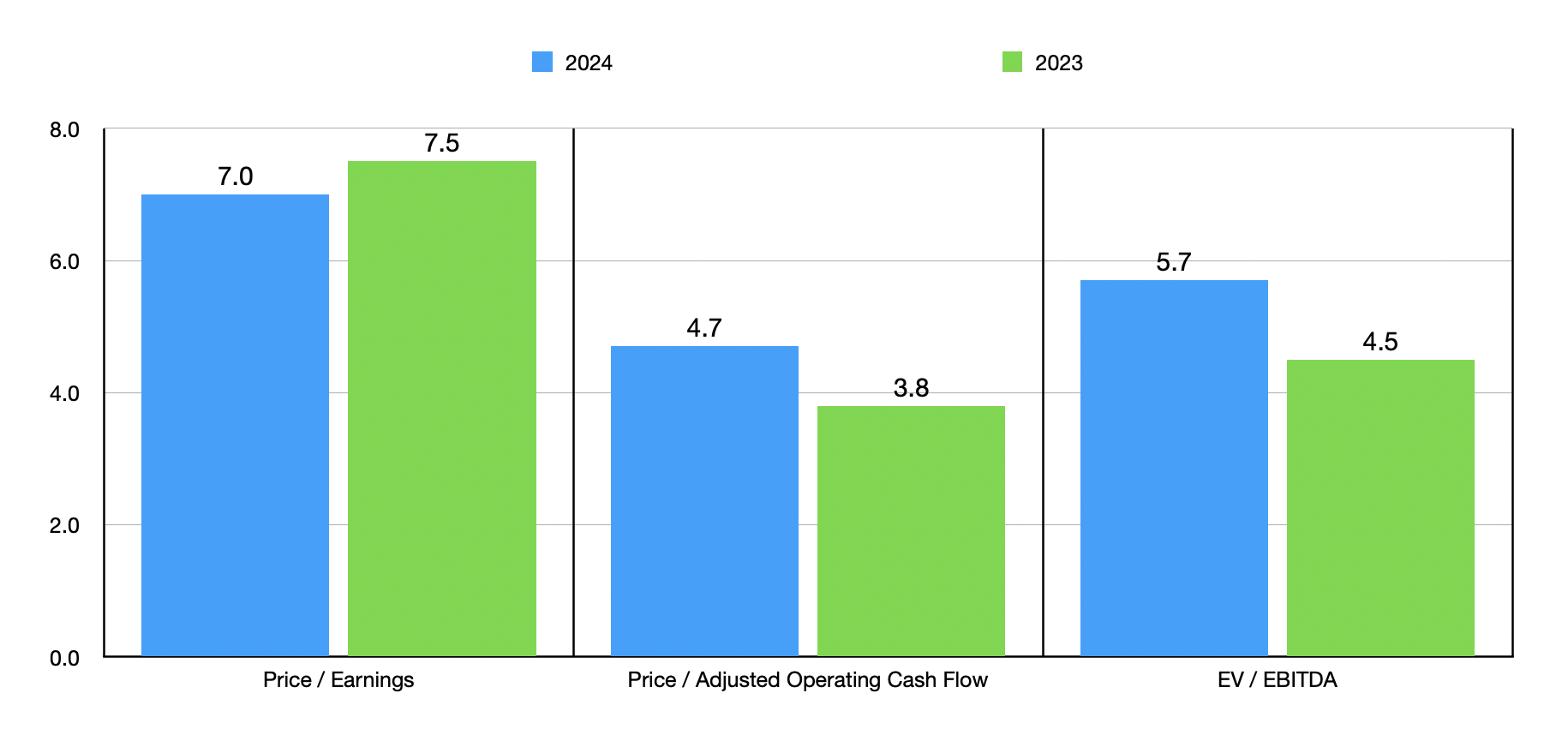

Using these figures, I was able to price the company as shown in the chart above. Using a price to earnings approach, the stock is trading at a multiple of 7.0 on a forward basis. This is slightly lower than the 7.5 reading that we would get using data from 2023. The price to adjusted operating cash flow multiple should rise from 3.8 to 4.7, while the EV to EBITDA multiple should climb from 4.5 to 5.7. As you can see in the table below, I compared Guess? to five similar firms using the price to operating cash flow approach and using the EV to EBITDA approach. Using the former, I found that two of the five companies were cheaper than it, while another was tied with it. And when it came to the EV to EBITDA approach, four of the five companies ended up being cheaper than our prospect.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Guess? |

| 4.7 |

| 5.7 |

| Designer Brands ( DBI ) |

| 2.5 |

| 4.5 |

| Abercrombie & Fitch ( ANF ) |

| 6.0 |

| 6.2 |

| Caleres ( CAL ) |

| 4.2 |

| 4.9 |

| American Eagle Outfitters ( AEO ) |

| 4.7 |

| 5.5 |

| The Buckle ( BKE ) |

| 6.4 |

| 4.2 |

While some investors may feel more comfortable with companies that have inconsistent financial results from one window of time to another, I believe that such inconsistencies drastically increase the probability of underperformance. But what this also suggests is that, should economic conditions worsen, volatility would be likely to increase further. According to one source , real consumer spending so far this year has been quite strong. In the first quarter of the year, it was up 4.3% year over year. In the second quarter, it was considerably weaker at 1.7%. But early estimates for the third quarter have pegged it at a robust 3%. That source, Fitch Ratings, even went so far as to revise higher its annual consumer spending growth forecast from the 1% it was at before to 1.9% now. But they don't expect this strength to continue. In fact, their current expectation is for consumer spending, on an inflation adjusted basis, to contract by 0.8% in the first quarter of next year before contracting even further to the tune of 3% in the second quarter.

There are multiple reasons behind this more pessimistic approach. The resumption of student loan payments, the organization said, will likely have some small impact on consumer spending. But rising interest rates aimed at curtailing wage growth should also be a major contributor. Fitch Ratings also cited the fact that consumer savings continue to drop. And with that decline should eventually come a scaling back of spending.

Takeaway

At this moment in time, I believe that while Guess? is not a bad prospect, it's not a fantastic one either. The apparel and accessories enterprise has a history of volatile financial results and, when coupled with pricing relative to similar firms and concerns about consumer spending moving forward, a case could be made that the risk to reward ratio for this enterprise is not all that great. Of course, the stock is still cheap on an absolute basis and management is forecasting growth this year. But to me, that's not quite enough for an upgrade to be justified. So because of that, I've decided to keep the company rated a 'hold' for now.

For further details see:

Guess? Makes For A Mediocre Fit