GUG - GUG: Bad Timing For Launch But Future Looks Brighter

2023-03-17 02:28:33 ET

Summary

- GUG launched at the end of 2021, just in time to catch the historic bond drop and the weakness in the equity market.

- The fund has an "active allocation" approach where the managers can dynamically shift their portfolio.

- The fund's distribution is quite attractive, as well as the fund's discount, making it a worthy consideration for one's portfolio.

Written by Nick Ackerman, co-produced by Stanford Chemist. A version of this article was originally published to members of the CEF/ETF Income Laboratory on March 2nd, 2023.

Guggenheim Active Allocation Fund ( GUG ) is a relatively newer fund, launching towards the end of 2021. This was just in time to catch the incredible downward pressure that arose from rapidly rising interest rates. The fund isn't restricted to fixed-income investments but is currently oriented that way with the majority of its portfolio.

The same group offers this fund as the incredibly popular Guggenheim Strategic Opportunities Fund ( GOF ), including with the same exact managers. Yet, GUG trades at a discount while GOF gets to trade at some substantial - but not unusual - premium. The premium of GOF has been rising even further lately. I believe that GUG could be a cheaper alternative, with a more sustainable distribution currently. At the very least, it could be seen as a potentially attractive fund to consider for an investor's portfolio.

The Basics

- 1-Year Z-score: -0.83

- Discount: -12.83%

- Distribution Yield: 10.43%

- Expense Ratio: 1.92%

- Leverage: 27.76%

- Managed Assets: $725.3 million

- Structure: Term (anticipated liquidation date of November 22, 2033)

GUG's investment objective is "to maximize total return through a combination of current income and capital appreciation." To achieve this, the fund will "pursue both a tactical asset allocation strategy, dynamically allocating across asset classes, and a relative value-based investment strategy, utilizing quantitative and qualitative analysis to seek to identify securities with attractive relative value and risk/reward characteristics."

In doing this, the fund's "sub-adviser seeks to combine a credit-managed fixed-income portfolio with access to a diversified pool of alternative investments and equity strategies." Allowing them to invest in both fixed-income and equities means they are going to be quite a flexible fund, with limited guard rails on where and in what they can invest.

Some minor stipulations include that they will not have 25% or more invested in CCC or below-rated debt. Additionally, the fund will not invest more than 50% in equity positions or 30% in other investment companies. With that, they also will remain invested with a tilt towards U.S. allocations, with no more than 30% of assets outside of the U.S. They also impose that no more than 5% of the fund's assets will be in CLO equity tranches and limit total assets to no more than 15% in commodities, including energy and natural resources businesses.

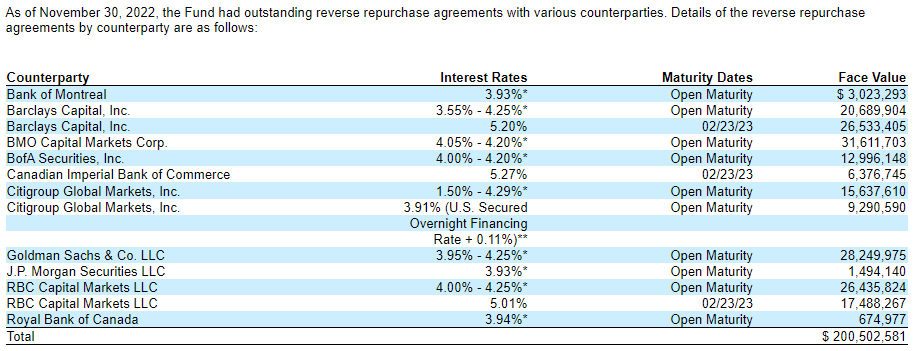

The fund's expense ratio is quite high, which means they have to do relatively better than its peers if they want to achieve attractive performance. The total expense ratio comes to 2.86% when including the fund's leverage expenses. That's quite the leap from the prior year and has to do with rising interest rates and taking on leverage as they get ramped up. The fund incorporates reverse repurchase agreements for its leverage. These are a fairly common way to leverage but are "adjusted periodically." At the end of November, the rates were anywhere between 1.5% and as high as 5.27%.

{kind=link}

Fortunately, the fund has also incorporated interest rate swaps. At the end of November 2022, the average notional amount was $44.833 million, meaning that some of the leverage is being hedged. On top of this, the fund isn't afraid of incorporating other derivatives, such as forward foreign currency exchange contracts, credit default swaps or purchasing and writing options.

The fund can also incorporate a credit facility with an agreement to borrow up to $165 million. This is also based on a floating rate of SOFT + 0.95%. Any unused portion is charged a commitment fee of 0.50%. At the end of November, they didn't have anything borrowed on this facility, which was a decline from the $69 million they reported at the end of their fiscal year. So, unfortunately, this is just a commitment fee cost that is going out and isn't being recouped.

Limited Term Structure

As is the case with the majority of funds after ~2018 , the fund is a limited-term fund. That means they are expected to liquidate in the future and return NAV back to shareholders, whatever NAV might be at that time. It isn't a target-term fund with a specific NAV goal in mind.

For GUG, this was a twelve-year term , so they are set to liquidate towards the end of 2033. As is also the case with these limited-term funds, there is a way for the Board to extend the term to prevent liquidating during a downturn. They can extend it up to two years without shareholder approval.

An additional common feature that is also included with GUG is the chance to go perpetual. In that scenario, the fund would conduct a tender offer within 6-18 months of the preceding dissolution date. The tender offer would be for 100% of shares at 100% of NAV. That means an investor could cash out at that time at NAV. If there are still $200 million in net assets after such a tender offer, the Board can remove the dissolution date and become a perpetual fund. If less than that amount of assets would remain after the tender offer, the tender offer can be canceled, and the fund will liquidate as expected.

Performance - Bad Timing

As mentioned, the fund launched in November of 2021. The launch timing probably couldn't be worse as it was when the Fed began talking about interest rate hikes. Then through 2022, we saw that the pace of interest rate hikes was steepened substantially. 2022 ended up being the worst year on record for bonds .

Now, in 2023, we are still grappling with sticky inflation and even a strong jobs market. This has meant that the Fed can continue to be more aggressive. However, it's also expected that the Fed is still nearer to the end of hiking interest rates than the beginning. With the stabilization of interest rates, fixed-income funds and even the equity market could look much better going forward.

Of course, the cause for a pause in hiking interest rates or even a cut in interest rates would probably be the product of a recession. At that time, it will be determining how deep or how long such a recession could last. So either way, 2023 could shape up to be another quite volatile year, and that's what we've seen in the first couple of months already.

With that being said, GUG has fallen quite far since its launch. The fund going to a deep discount exaggerated those moves, as well as the incorporation of leverage. Still, it wasn't as if equities or bonds during that time did anything spectacular. In fact, on a total NAV return basis, GUG had outperformed both as measured by SPY and BND .

Ycharts

It was merely on a total share price return basis that the fund underperformed. That was only the result of the fund going to a discount.

Additionally, GOF had performed well during this time - even beating out GUG. However, these two correlated quite closely. It was more in the last couple of months that GOF had pulled away on a total NAV return basis. Due to the substantial expansion of GOF's premium, the total return basis was no contest.

That's primarily why GUG looks like a more attractive fund today based on valuation relative to GOF. GOF will have to continue performing better and look to keep or extend its current premium to outperform going forward. It makes it more of an uphill battle for GOF compared to GUG. A premium for GOF isn't anything new, but the recent level had it pushing an all-time high. With some volatility shaking things up in the last week, it's come off from those elevated levels but remains heightened.

Distribution - Looking Attractive

The fund launched with a monthly distribution of $0.1188, and they continue to pay at that level. If GOF is any indication, a level distribution will be a strong focus of the fund, maintaining the same distribution for years and years.

While GUG's 9.86% distribution might not seem as attractive as GOF's 12.85% level, there are some concerns that I continue to have about GOF. For GOF trading at such a large premium, the underlying NAV distribution rate actually comes to 17.13%. That's incredibly high, even for the higher interest rate environment that we are in now. GUG's 8.89% distribution rate seems much more sustainable.

I touched on the coverage shortfall of GOF previously , but it should also be noted that GUG also carries a shortfall. This is at least according to their last semi-annual report. However, due to floating rate exposure, NII could continue to increase. GOF can also benefit from their floating rate exposure, but with such an elevated NAV rate, it remains a high hurdle to achieve.

{kind=link}

GUG also crossed over the 1-year mark after this report. At this point, they should be mostly invested now, and future reports will be a better indicator of coverage. Due to the fund being a dynamic approach, investing in equity positions in the future could see capital gains become an important factor for the fund. Though I tend to suspect they'll lean into the fixed-income space regularly, as their funds tend to be focused on that asset class.

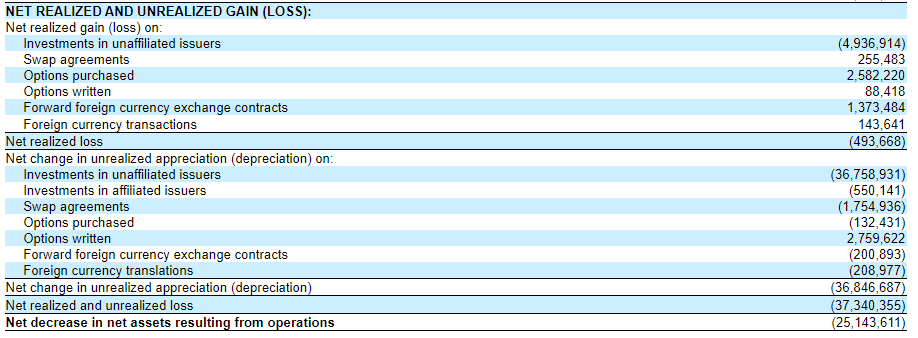

Worth noting is that besides equity positioning when we were touching on the fund utilizing various derivatives above, it also means potential gains from those sources. In this case, their swaps, options purchased, and written and forward foreign currency exchange contracts all contributed to offsetting the majority of the losses realized from the underlying portfolio.

{kind=link}

It wasn't nearly enough to offset the unrealized depreciation, thus, why we saw a decline in the NAV in the first place.

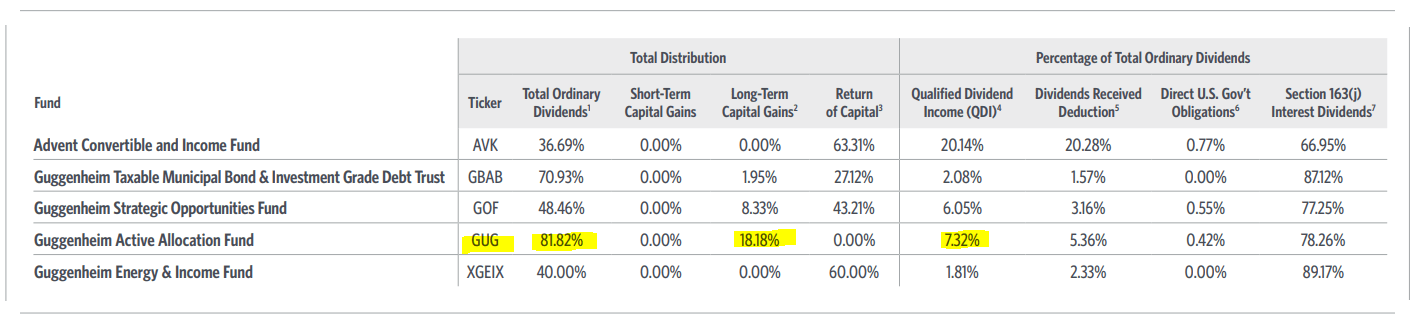

For tax purposes, by being exposed significantly to fixed income, ordinary dividends/income will generally be a meaningful part of the fund's tax classifications. For 2022 , that was the case, with only 7.32% considered qualified. However, the 18.18% classified as long-term capital gains is also tax-beneficial as it's taxed at a reduced rate for investors.

GUG Distribution Tax Classifications (Guggenheim (highlights from author))

{kind=link}

GUG's Portfolio

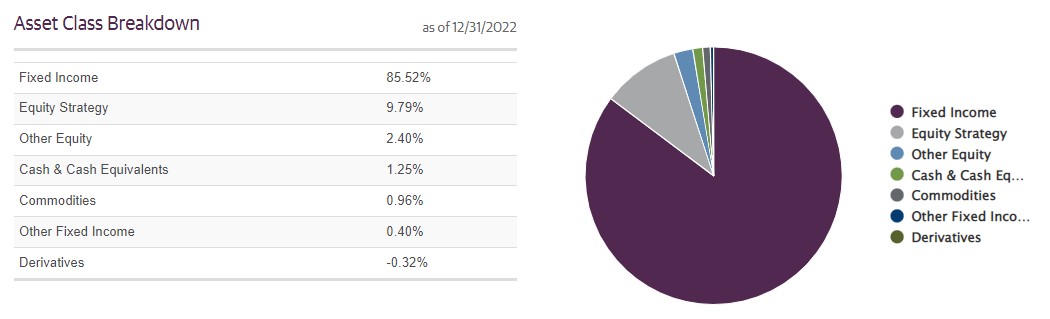

GUG and GOF aren't perfect replicas of each other; they do have some differences in their allocations. Both focus heavily on fixed-income exposure, but GUG ekes out a relatively larger allocation to an equity strategy.

{kind=link}

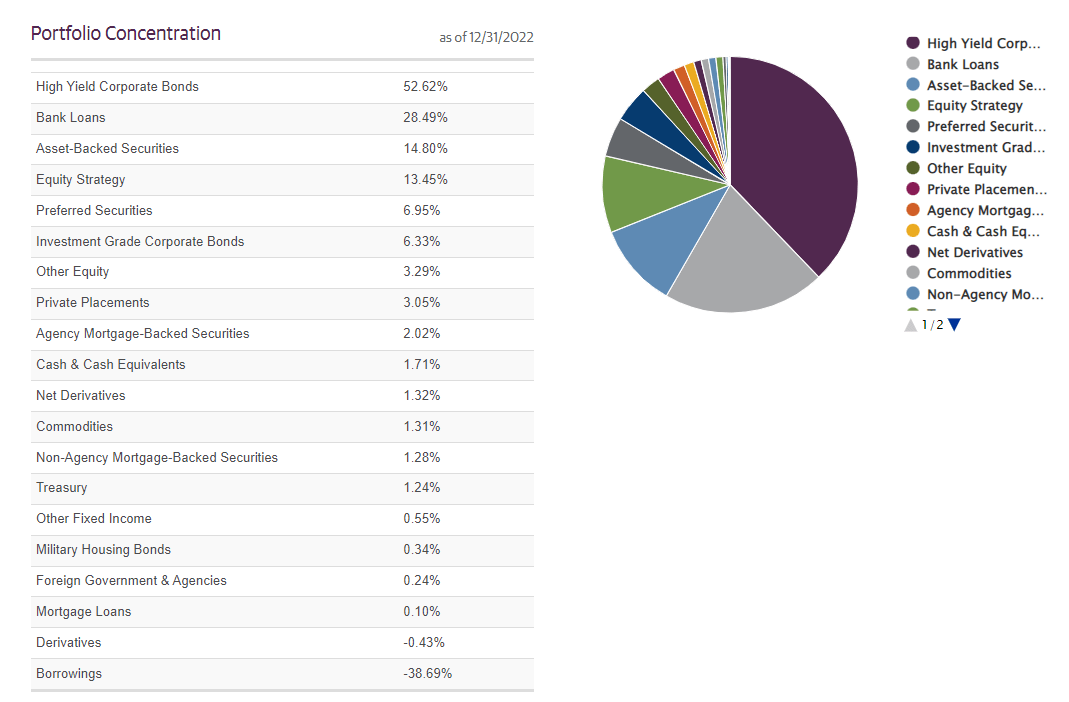

To break it down further, the fund's fixed income is heavily invested in high-yield corporate bonds. A smaller but still meaningful allocation follows this allocated to bank loans.

{kind=link}

The bank loan allocation is slightly lower than GOF's allocation at 31.98%. Bank loans and CLO exposure or collateralized loan obligations are important factors in the exposure of GUG and GOF. These are particularly important and attractive at this time because they are floating rate exposure. With higher interest rates, the floating rate loans benefit as yields rise.

Despite the differences between the funds, their duration of them is nearly identical. GUG's weighted average duration is 4.36 years, and GOF is 4.41 years. That would indicate that the expectations of changes in interest rates will have nearly identical impacts on these funds.

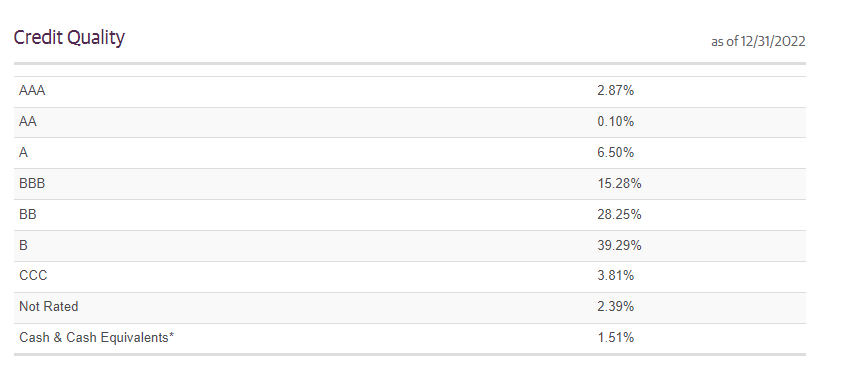

When looking at the portfolio's credit quality, they carry a fairly meaningful allocation to investment-grade debt. BBB debt and higher was nearly 25% of the fund. While investment-grade debt can generally be more interest rate sensitive, it will also carry less credit risk. Still, below-investment-grade debt remains the most significant allocation for the fund, which is often the case with fixed-income CEFs.

{kind=link}

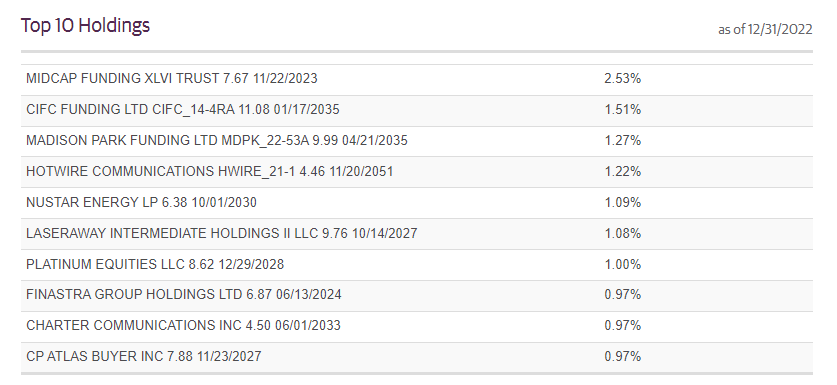

The top ten holdings in the fund make up 12.61% of the portfolio. CEFConnect reports that the fund carried 1432 different holdings at the end of November 2022. Thus, we know there is a ton of diversification in the underlying portfolio, spreading out tons of exposure to various entities. That can be important for below-investment-grade heavy funds to diversify out to limit risk.

{kind=link}

Conclusion

GUG appears to be an attractive fund that follows a similar strategy as GOF. That means a lot of flexibility to invest in just about anything they want. At the same time, while the distribution yield is smaller, the valuation difference between the two makes GUG more compelling at this time. GOF can continue to trade at a premium, as it has historically, but the premium has become quite elevated.

On its own, GUG is an interesting fund regardless, even if we aren't directly comparing it to GOF. The discount is quite attractive, and while distribution coverage is lacking, they have many moving parts in their strategy that could see coverage improve. That improvement can come from capital gains in its derivatives or equity strategy.

For further details see:

GUG: Bad Timing For Launch, But Future Looks Brighter