GUG - GUG: Discount Remains Attractive For This 'Active Allocation' Fund

2023-06-20 20:08:44 ET

Summary

- Guggenheim Active Allocation Fund is an interesting fund, focusing on 'active allocation,' though they haven't appeared too active thus far.

- GUG has a higher emphasis on fixed-income assets and provides a more reasonable and sustainable distribution than GOF at a much better valuation, making it a potential swap alternative.

- The fund's performance improved in 2023 after a period that was rough for almost all equities and fixed-income investments, and its discount has shown signs of stabilizing.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on June 19th, 2023.

We last took a look at Guggenheim Active Allocation Fund ( GUG ) earlier this year. This relatively newer fund launched in 2021, so they've had some more time to get under their belt. We noted that the worst feature of the fund was simply the timing of the launch.

By launching at the end of 2021, it came in just in time to catch both fixed-income and equities declining simultaneously. This generally doesn't happen, but it was thanks to the Fed aggressively hiking interest rates to combat inflation. So the overall environment for 2022 was obviously a huge factor; still, both assets declining hadn't happened since 1969 . Not only that, but it was the worst year ever for U.S. bonds , which this fund places a heavy emphasis on.

Then you put on top of that a closed-end fund that generally sees a wide discount open up after the first year or two. In 2021, CEFs were at historically narrow discounts and are now trading at historically wide discounts. In hindsight, it was about the worst of the worst environment for a new CEF to launch - that's any CEF that launched in 2021 for the most part.

Otherwise, this was a fairly interesting fund that Guggenheim offers. Guggenheim in the CEF space is probably most famous for their Guggenheim Strategic Opportunities Fund ( GOF ), which I believe GUG is a great replacement for that doesn't carry a historically high premium with an elevated NAV distribution rate. Duff & Phelps Utility and Infrastructure Fund ( DPG ) is our latest reminder that you don't mix premiums with unsustainable distributions and see good times last forever.

GUG has even provided some positive returns since our prior update.

GUG Performance Since Prior Update (Seeking Alpha)

The Basics

- 1-Year Z-score: 0.16

- Discount: -11.56%

- Distribution Yield: 10.06%

- Expense Ratio: 1.92%

- Leverage: 26.53%

- Managed Assets: $725.3 million

- Structure: Term (anticipated liquidation date of November 22, 2033)

GUG's investment objective is "to maximize total return through a combination of current income and capital appreciation." To achieve this, the fund will "pursue both a tactical asset allocation strategy, dynamically allocating across asset classes, and a relative value-based investment strategy, utilizing quantitative and qualitative analysis to seek to identify securities with attractive relative value and risk/reward characteristics."

In doing this, the fund's "sub-adviser seeks to combine a credit-managed fixed-income portfolio with access to a diversified pool of alternative investments and equity strategies." Allowing them to invest in both fixed-income and equities means they are going to be quite a flexible fund, with limited guard rails on where and in what they can invest. Guggenheim's other funds, including GOF, have generally favored fixed-income, so I suspect this fund will remain heavier in fixed-income allocations for the most part.

The fund's expense ratio is on the higher end, which is generally negative to consider before investing. When looking at the total expense ratio with the inclusion of leverage costs, the expense ratio came to 2.86%. The fund isn't as leveraged as some of its fixed-income-oriented peers. That said, leverage adds risks and makes funds more volatile. Even worse, in a rising rate environment, it also means that borrowing costs have been increasing.

Fortunately for GUG investors, they had hedged through interest rate swaps on a portion of their borrowings. The fund also carries a fairly meaningful weighting to underlying positions carrying floating rates. They are also heading currency risks through various derivatives as well, which all helped contribute to gains for the fund.

Performance - Discount Widens And Showing Signs Of Stabilizing

As is generally the case with new CEFs, the fund's discount widened substantially after launching. However, as the overall equity and the fixed-income market started to stabilize and make a recovery from last October's lows, GUG's discount has also shown to be more stable lately.

With a short history, there really isn't much in terms of a track record, but we are now floating between the fund's average discount since launch and its low. The low discount touched nearly 16% around October, coinciding when most everything else also hit the lows of last year's bear market.

YCharts

2023 overall has been a brighter year for the fixed-income space. Total return performances aren't blowing anyone away, but it's a nice change from declines last year. GUG has been the better performer on a YTD total NAV return basis compared to its older sister GOF. Even more recently, the fund has also started to outperform on a total share price basis.

Both have outperformed iShares iBoxx $ Investment Grade Corp Bond ETF ( LQD ) and iShares iBoxx $ High Yield Corp Bond ETF ( HYG ), which have been included for a broader look at the bond performances YTD. They aren't exactly benchmarks or peers, but they can help provide some context for the results.

YCharts

Distribution - Double-Digit Distribution Rate

The fund launched and started paying a monthly distribution of $0.11875, which they've maintained despite losses experienced shortly after launch. Based on the last closing price, that puts the distribution rate just into the double-digit level at 10.06%. Thanks to the fund's discount, the NAV distribution rate comes to 8.90%.

That's one of the more appealing parts of GUG over GOF. For GOF, the distribution rate may come to 14%, but the NAV rate is nearly 18% of what the fund has to earn. Even at 14%, it would be quite elevated. It makes GUG's distribution much more reasonable, and it should be more sustainable.

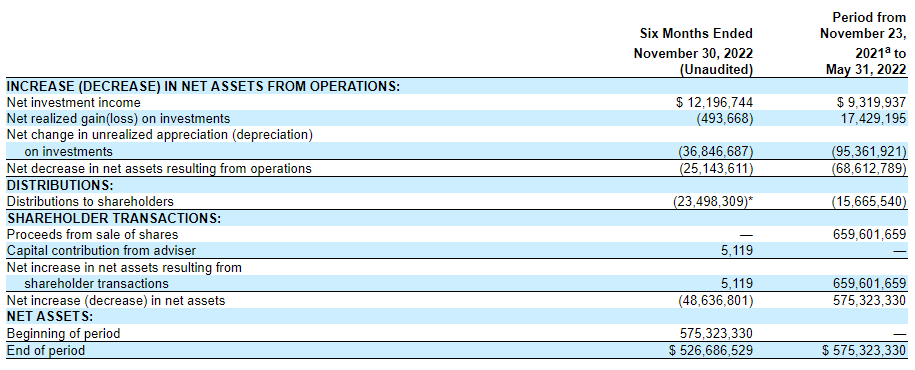

That said, GUG will still require significant capital gains to fund its distribution as well. Just a bit less than GOF requires. As the portfolio was ramped up in the latest semi-annual report from the prior abbreviated fiscal year-end, we saw net investment income increase. The fund's NII went from $0.28 to $0.37 on a per-share basis. That put NII coverage at around 50%.

{kind=link}

Based on the fund's semi-annual report and how the breakdown of the portfolio is listed more recently, at least around 30% of the portfolio should be in floating rate investments. Therefore, we could see coverage improve with NII increasing in the next report. That would certainly be welcomed, as we generally want to see fixed-income-oriented funds earning their distributions from income generated in the portfolio.

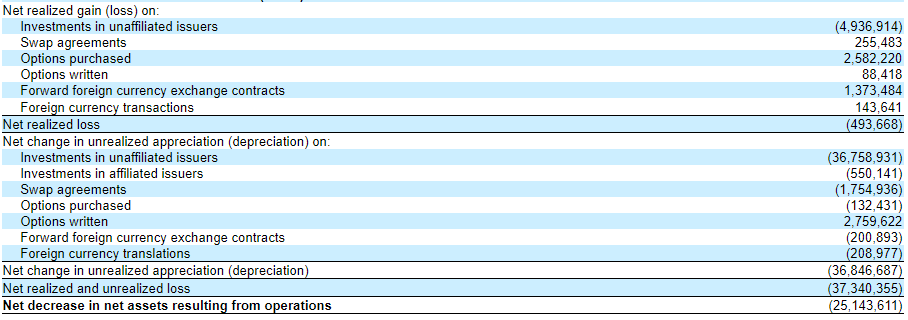

The fund realized losses, but these were more limited thanks to the fund's derivatives that contributed positively to performance. That includes the fund's utilization of purchasing and writing options.

{kind=link}

For tax purposes, they listed that 2022's breakdown showed an overwhelming majority as ordinary income. As a fixed-income heavy fund, this is quite normal and would indicate that the fund could be best held in a tax-sheltered account.

{kind=link}

GUG's Portfolio

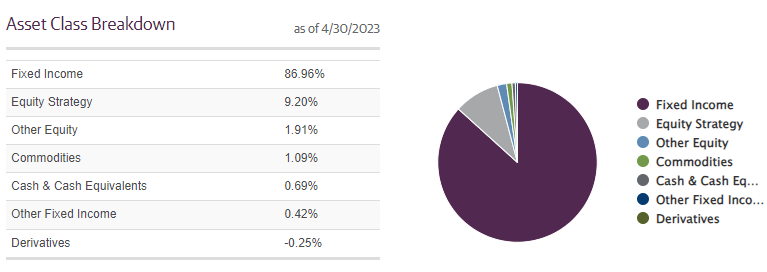

Since our last update, their portfolio didn't change too dramatically. The weighting to fixed-income moved even higher from an already overweight position. This was previously ~85.5% of the fund's allocation.

{kind=link}

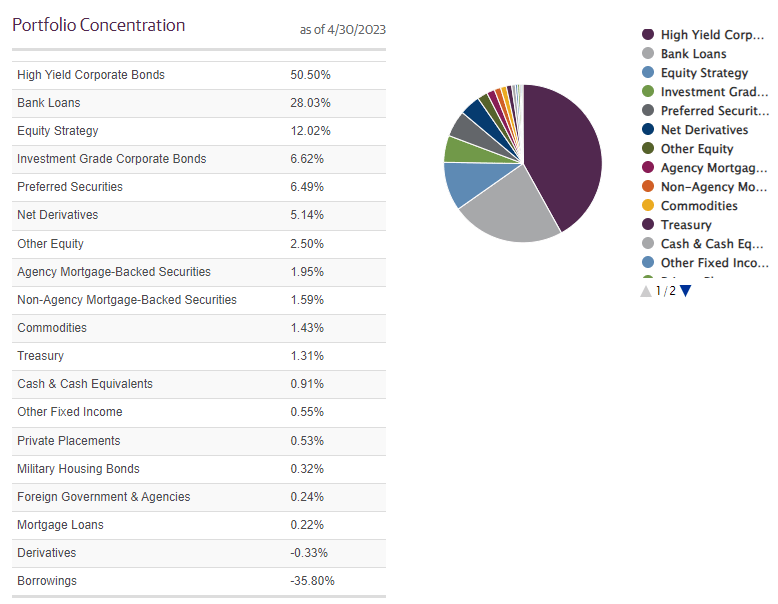

The duration of the portfolio had also inched a bit lower to 4.08 years from 4.36 years. This really wasn't a significant change either, and it doesn't indicate any drastic difference we should expect in the fund going forward. High-yield corporate bonds command the highest weighting in the fund.

However, this is followed by bank loans at a meaningful weight as well. The bank loans are where the portfolio is going to get most of its floating rate exposure - and, thus, where the portfolio's duration can be limited.

{kind=link}

Bank loans aren't the only place to find debt offerings based on a floating rate, but that also includes their other asset-backed security allocations. That includes the collateralized loan obligations that the fund carries in its portfolio. They even have some of their MBS in floating rate issued securities when you dig into the listed holdings in their semi-annual report.

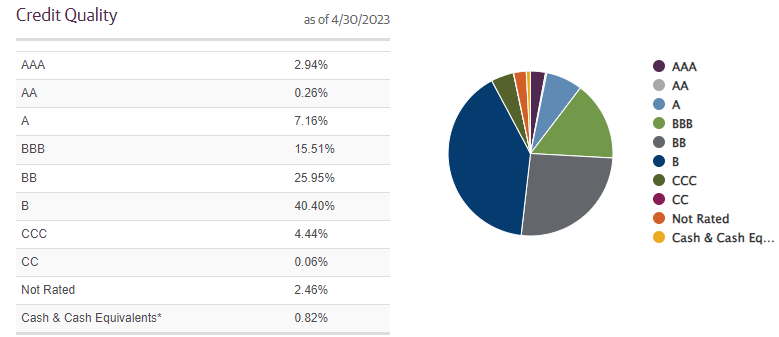

When looking at the credit quality, it's mostly the same as we saw previously as well. However, it is worth noting once again that GUG is a bit different from other multi-sector bond funds in terms of its allocation by including a fair bit of investment-grade bonds. Usually, when looking at the more popular PIMCO funds, they tend to choose to stick with junk-rated holdings.

{kind=link}

One area that they keep the same is the significant diversification in terms of the fund's number of holdings. CEFConnect lists it at 1378 holdings.

Interestingly, when looking at the fund's common stock holdings, they list hundreds of positions. The listing for common stock positions goes from page 30 of their semi-annual report to part way through 57. There are roughly 35 listed on each page, resulting in nearly 1000 holdings. Most of these are less than $1000 invested.

In fact, Digital Media Solutions ( DMS ), as one example, listed that they held 19 shares for a total value of $32. They held a HyreCar (HYREQ) position (which is in bankruptcy now) of 104 shares with a $62 value. The report shows that they held a whopping 5 shares of Greenlane Holdings ( GNLN ) with a value of $2.

These are all risky penny stocks, and these are only some of the examples. There are hundreds and hundreds more of these. So it would seem part of their position is to hold hundreds of penny stocks to see if any of them work out. The problem with that is that it's within such a diverse portfolio that it doesn't matter. Even if a few of these positions run up thousands of percentages, it is unlikely to offset the losses or move the needle for GUG overall.

This isn't their entire strategy, and they hold several larger equity positions in real companies such as Starbucks ( SBUX ), Home Depot ( HD ), and Domino's Pizza ( DPZ ). That said, even these investments only make up around $400k investments. A lot for an individual but not so much for a fund that has $719 million in total managed assets. It's just something interesting to note that I hadn't caught when I first looked at the fund. The fund could be more appealing by getting rid of the penny stock plays and investing in real securities, in my opinion. That could be whether they stick with other equity positions or more fixed-income that have real earnings with higher potential for returns.

The top ten weightings make up only around 11% of the fund, and those weights drop swiftly by number 10. And as we noted above, the position sizes can be as small as $2 in value, so we know how small things can get.

GUG Top Ten Holdings (Guggenheim)

Conclusion

GUG sports an emphasis on "active allocation." That active allocation has chosen to sit materially in the fixed-income asset class, but they do carry plenty of diversification even within that space. At this time, the fund mirrors and is positioned more like a multi-sector bond fund rather than an overly tactical fund. This will be interesting to continue to see how it develops over time. That said, I believe it still represents an attractive alternative for GOF investors if they want Guggenheim exposure. Additionally, the fund, on its own merits, is fairly interesting and, given the current discount, could be worth exploring.

For further details see:

GUG: Discount Remains Attractive For This 'Active Allocation' Fund