GXO - GXO Logistics: Automation Drive For Margin Expansion

2023-12-15 15:03:42 ET

Summary

- GXO Logistics reported $2.47 billion in revenue for Q3 2023, an 8% increase from the previous year.

- Despite slower organic growth, GXO delivered strong operating margin and profitability, with operating income rising by 25%.

- GXO's strategic focus on automation and AI is expected to drive margin expansion and boost its long-term financial goals.

- We think that the company’s margin forecasts underestimate the impact of AI and suggest that it can achieve its $1.6 billion Adj. EBITDA goal ahead of FY 2027.

Investment Thesis

As one of the world’s leading supply chain outsourcers, GXO Logistics ( GXO ) provides comprehensive warehouse management, distribution and fulfillment services to global customers. The company reported $2.47 billion in revenue for the third quarter of 2023, an 8% increase from the same period last year, with 3% coming from organic growth. However, organic growth was lower than expected due to the challenging macroeconomic conditions. Consequently, GXO’s revenue growth rate slowed down to 8% in Q3 2023 from 11% in Q2 2023.

Despite the revenue decelerating in Q3 2023, GXO delivered strong operating margin and profitability. The company’s operating income rose by 25%, and its adjusted EBITDA reached $200 million, a 4% growth YoY. The company also boosted its free cash flow to $191 million from $43 million in Q3 2022. Furthermore, GXO increased its full-year adjusted EBITDA guidance to $730 -$755 million, up from the previous range of $725-755 million.

Despite the organic revenue growth slowdown, GXO seems optimistic about its future business performance and growth potential. The company aims to achieve an 8-12% organic revenue CAGR in the long term, driven by rising outsourcing demand, increased ecommerce spending and the global reshoring trends. The company also anticipates strong free cash flow conversion from its operations.

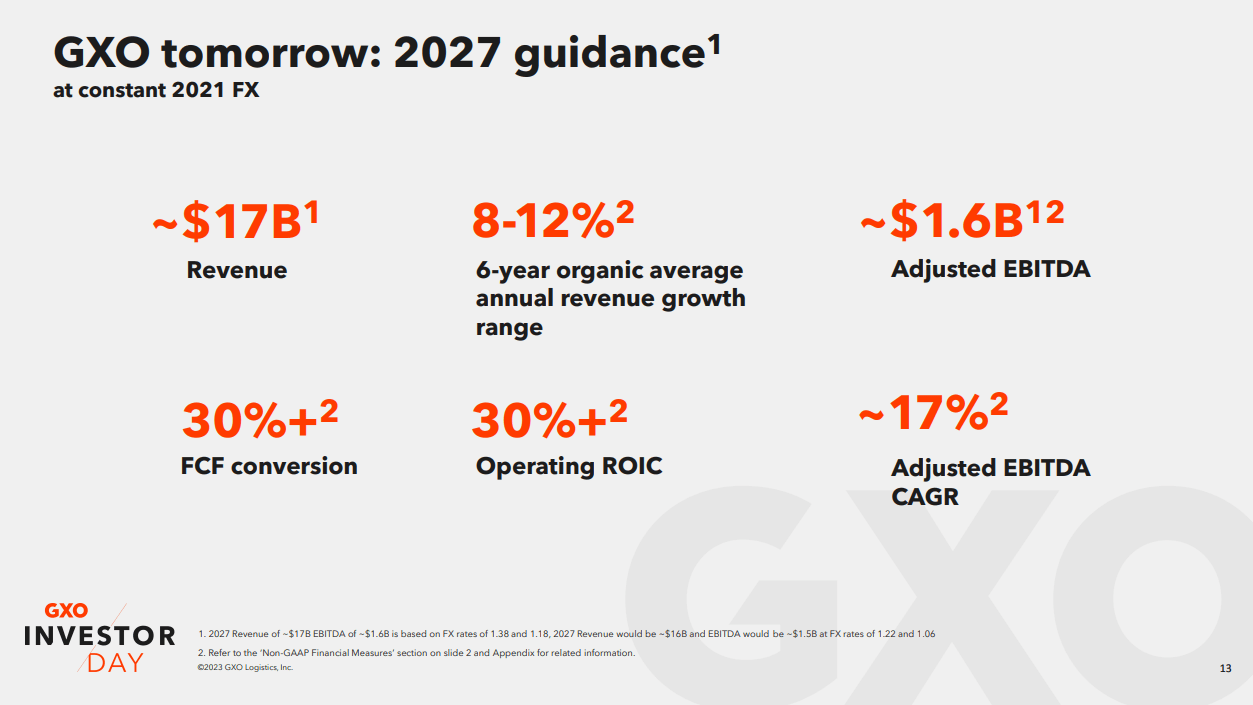

GXO’s strategic vision is to transform the supply chain industry with its advanced technology, global scale and deep expertise advantages. To realize this vision, GXO has shared its strategic long-term goals for the next five years at its investor day event earlier this year (see below).

GXO FY 2027 Targets (GXO Investor Day Presentation)

{kind=link}

The question is, can GXO meet these 2027 targets and what does its financial performance reveal? In this article, we will examine the company’s strategy and financials to assess if its long-term goals are achievable. We will also give our opinion on whether GXO is a worthwhile investment or not.

World's Largest Pure-Play Warehouse Outsourcer

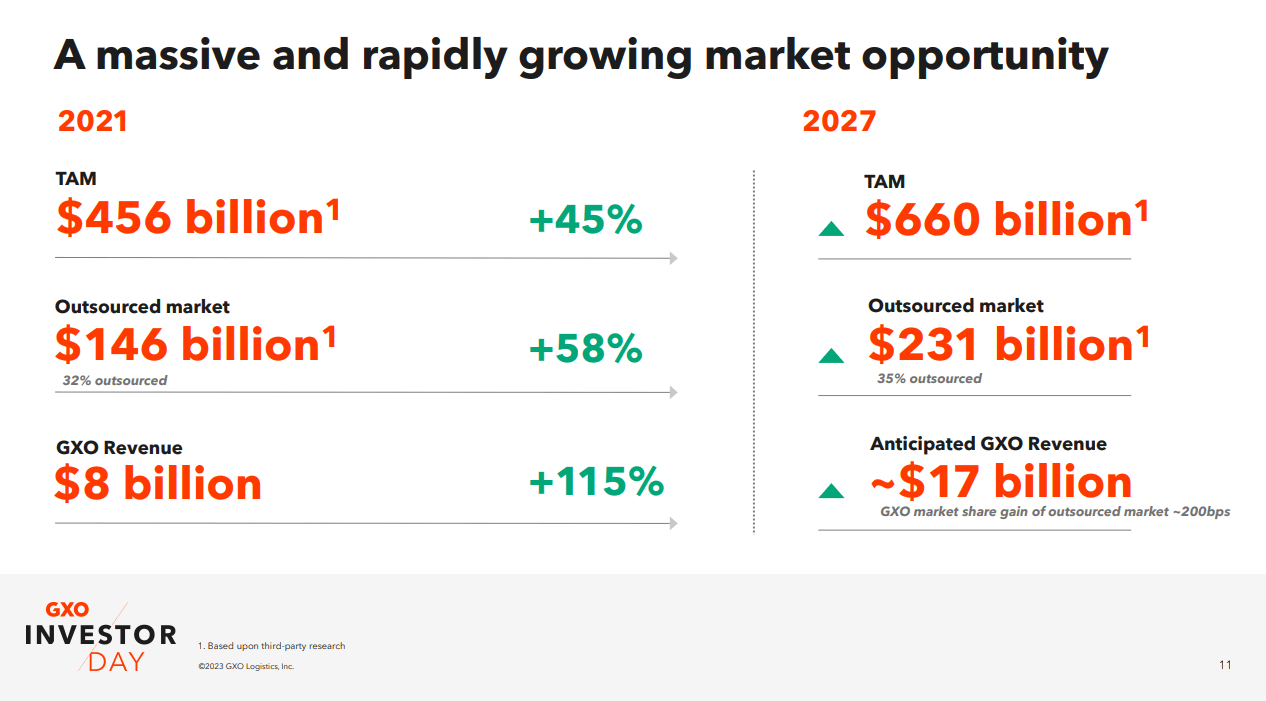

According to GXO, the global warehouse-outsourcing market is expected to grow to $231 billion by 2027, at a CAGR of 8% (see below). It is noticeable that the warehouse-outsourcing market is growing faster than the broader warehousing market, as customers look for more outsourcing opportunities to benefit from economies of scale and avoid technological complexities.

Warehouse-Outsourcing Market Size (GXO Investor Day Presentation)

{kind=link}

The warehouse market is highly competitive and fragmented across local, regional, national and international companies which makes it very hard to compete and gain market share. GXO has a market share of 5% in this market (as per the investor presentation ) and is listing Deutsche Post, Kuehne & Nagel, Ryder, CMA-CGM, ID Logistics, Wincanton, Elanders as some of its key competitors.

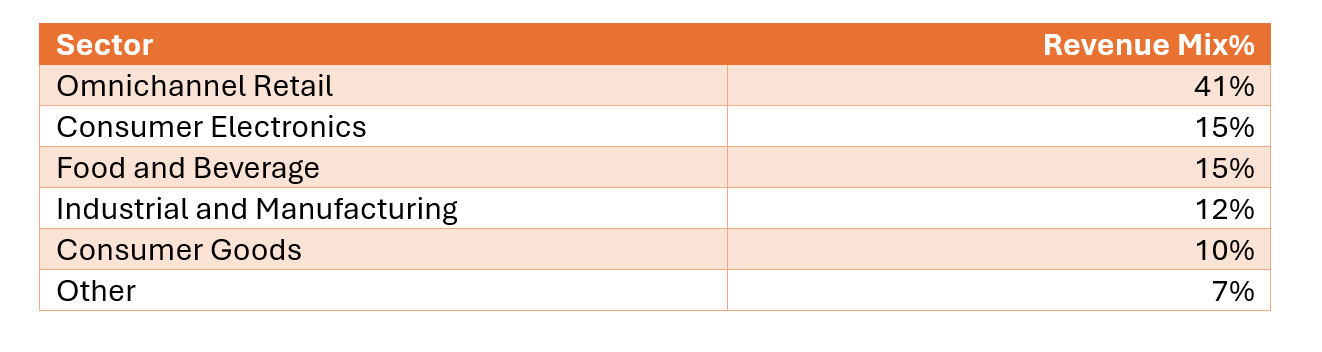

One positive aspect is that GXO’s customer base is quite diverse and demonstrates its expertise in various key sectors, which also safeguards its revenue from any industrial challenges or vulnerabilities (see below)

{kind=link}

GXO’s 2027 Plan and Progress so Far

At the start of 2023, GXO presented its long-term financial goals for 2027 to its investors, which we summarized earlier in the article. The company gave its outlook for FY 2023, expecting 6-8% organic revenue growth and $700-$730 million Adj. EBITDA.

However, 2023 was a challenging year in terms of revenue, as GXO had to revise its organic growth projection to 2-4% due to macroeconomic conditions and a retail slowdown, especially in the second half of the year. It is expected that this revenue softness may continue in the first half of 2024, as many sectors are experiencing a decline in consumer spending.

On the positive side, the EBITDA performance is progressing much better than expected, as the company raised its guidance to $730 - $755 million for the full year, which is a 4% increase from the initial estimate. The company attributed this improvement to its operational excellence, cost control, and automation efforts. It was able to improve its efficiency in various aspects, such as boosting labor productivity, streamlining procurement, consolidating operations and reorganizing the workforce structure. These actions resulted in higher EBITDA and stronger margins for the company.

The EPS progress is also on track, as the company expects to deliver $2.6 EPS for FY 2023, which is an 8% increase from the initial guidance. See below for the updated guidance for FY 2023.

FY 2023 Updated Guidance (GXO Q3 Earnings Presentation)

{kind=link}

We are confident in GXO’s 2027 plan, as the company is delivering solid results despite the difficult market conditions. We are not worried about the slower revenue growth, as we anticipate a return to normal levels with the economic rebound. We also think that EBITDA, rather than revenue, is the main source of GXO’s value creation which is what we want to focus on in the upcoming sections.

Automation and AI to Drive Margin Expansion

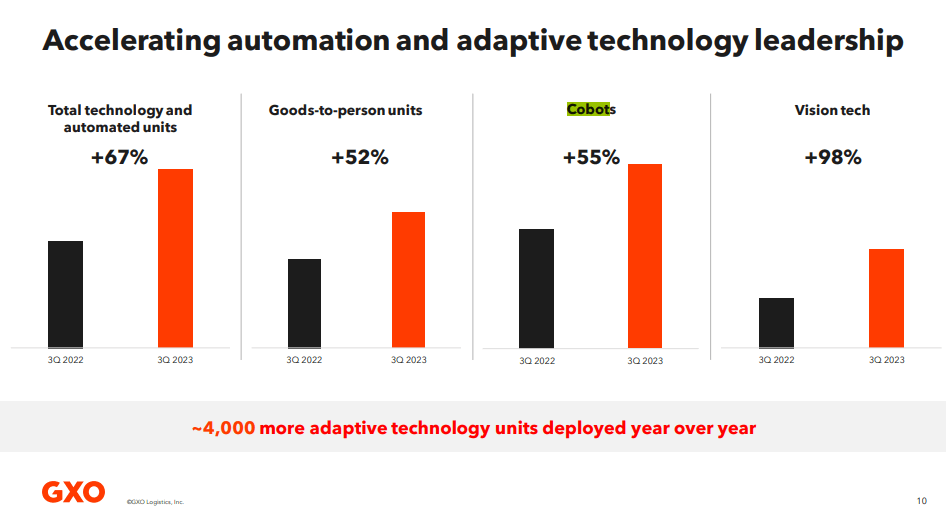

A key driver of GXO's growth potential is its focus on automation and AI to optimize its operations and improve its productivity. GXO has deployed thousands of automation technologies at customer sites, including roots, cobots, vision scanners and autonomous vehicles which collectively drive better customer outcomes and higher margins. Its automation and adaptive technology deployment has increased 67% year over year (see below) and what is remarkable is that 30% of the company’s revenue is coming from its automated operations. This is a big differentiation when compared to other companies and the market average of 8%

GXO Technology Adoption (GXO Q3 Earnings Presentation)

{kind=link}

GXO’s next phase of automation is to leverage the power of AI and integrate it with their operations and automation infrastructure. This will help the company automate more complex supply chain scenarios and replace more manual tasks, and thereby increase their automation revenue even further.

To double-down on its automation priority, the company has assigned a Chief Automation Officer role (Mr. Adrian Stoch) to strategize and oversee its automation and AI initiatives. Mr. Stoch believes that automation and AI are not only enhancing GXO’s operational efficiency and quality, but also creating new value propositions and competitive advantages for the company. From the Q3 Earnings call :

Adrian Stoch ((CAO)):

I'm very optimistic on the ability for automation and AI to help improve our margins and our efficiencies is because when we have a successful pilot, and there's many of these just this is one example I am mentioning. We have the opportunity to then standardize and take it to our global sites close to 1,000 sites. So absolutely, I do see it both as a growth lever and a margin improvement level.

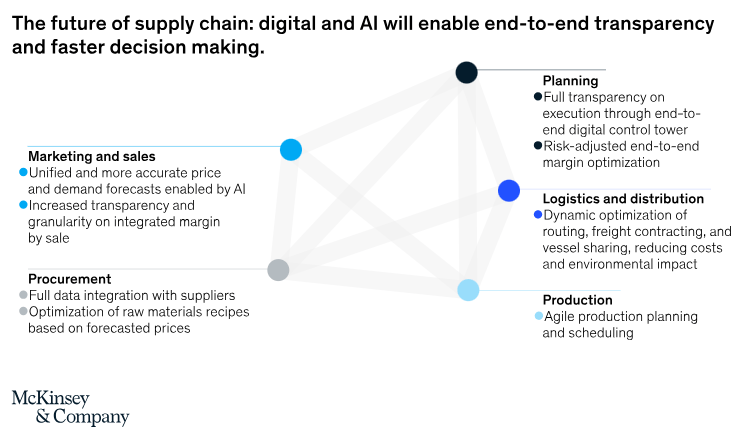

According to a McKinsey research, AI can have a significant impact on supply chain performance, as well as create new sources of value and growth. The research estimates that AI-enabled supply-chain management can improve logistics costs by 15%, inventory levels by 35%, and service levels by 65%.

AI & Supply Chain (McKinsey & Company)

{kind=link}

Our view is that GXO’s AI and automation strategy will boost its margins significantly. We also think that the company’s margin forecasts underestimate the impact of AI and suggest that it can achieve its $1.6 billion Adj. EBITDA goal ahead of FY 2027.

GXO's Future Revenue and EBITDA Projection

During Q3, GXO revised its Q4 FY2023 organic revenue guidance down to 2-4% but raised its adj. EBITDA outlook to $730-$755 million. As a result, we estimate that the company will deliver $9.75 billion of revenue and $750M of EBITDA for FY2023, in line with the market consensus.

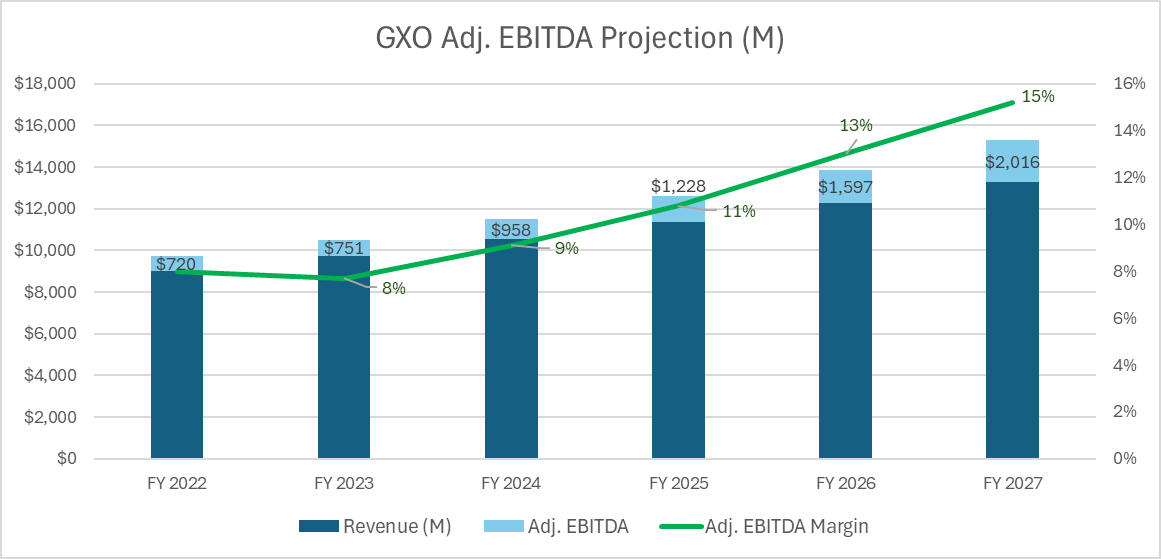

Based on these figures, we want to do an EBITDA projection for the next several years as we believe that the company will outperform its 2027 target of $1.6 billion adj. EBITDA. Hereby, we assume GXO will grow revenue at the market rate (8% CAGR) and estimate that it will expand its EBIDTA margin by at least 200 basis points each year. As a result, the company will be able to reach $1.6 billion adj. EBITDA in FY 2026 and $2 billion EBITDA in FY 2027 (see below)

GXO Adj. EBITDA Projection (Author)

{kind=link}

Note: The 200 basis point margin upside for automation was referred by CAO Adrian Stoch during the Q3 earnings call .

Valuation

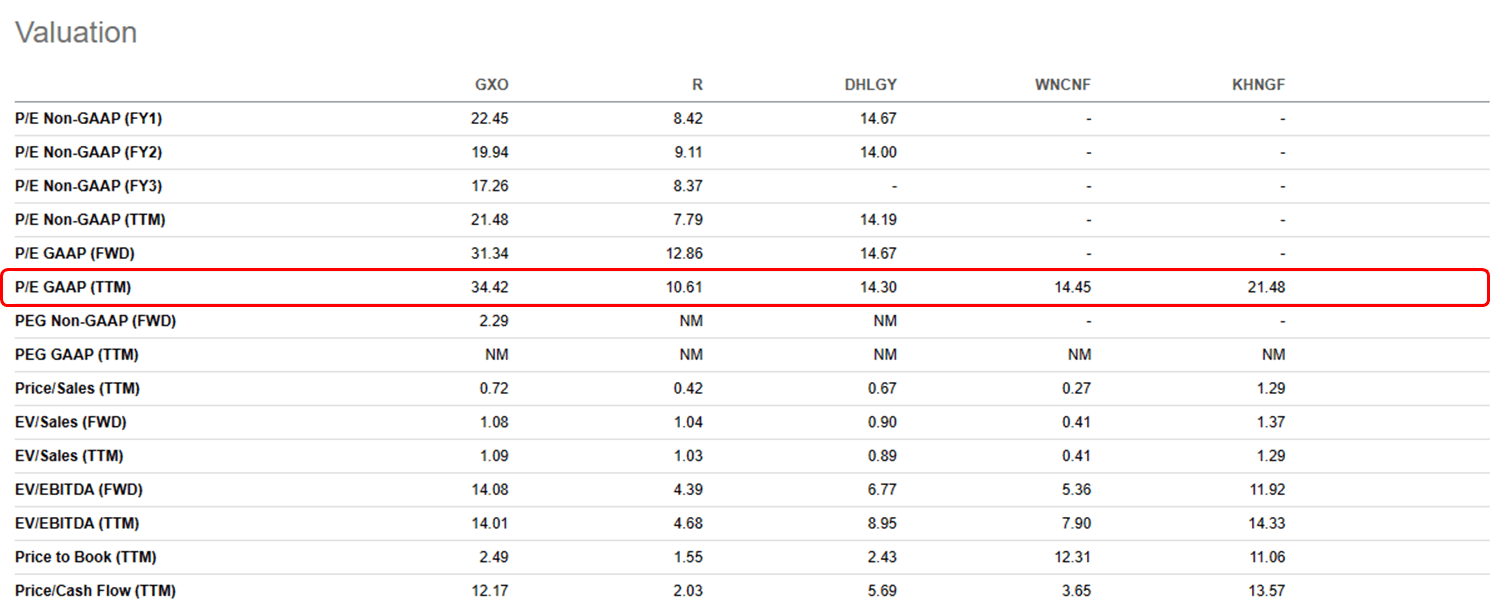

Based on our model, we estimate that GXO will reach an adjusted EBITDA of $1.6 billion by FY 2026. This implies that GXO can boost its FY 2023 EPS of $2.6 by at least 130% over the next three years, which would result in a 3 year price target of $86 based on a peer median P/E multiple of 14.3 (see below).

Peer Comparison Valuation Metrics (Seeking Alpha)

{kind=link}

We believe that this is a fair valuation, as we expect GXO to also benefit from improved market conditions starting from second half of fiscal year 2024.

Risks

We see the following risks for GXO’s valuation:

Macro Uncertainties : GXO is a global company and is exposed to macroeconomic uncertainties, geopolitical conflicts and trade disputes that may affect its customer demand and operational efficiency.

Competition : The transportation and logistics industry is highly competitive and GXO has to deal with many different types of competitors at various levels. Some of these competitors are more localized and may have an advantage over GXO in terms of cost efficiency, customer loyalty, or market insight.

Conclusion

Our analysis shows that GXO is currently undervalued, as its current share price does not reflect its strong margin expansion potential. We think GXO deserves a higher valuation multiple, given its leadership position in the logistics industry, its innovative use of automation and AI, its margin expansion potential and its ability to generate higher returns on invested capital. When we assign GXO a peer median P/E multiple, we derive a 3 year price target of $86, which represents a 43% upside from current levels.

We rate GXO as a buy and recommend investors to take advantage of this opportunity.

For further details see:

GXO Logistics: Automation Drive For Margin Expansion