GXO - GXO Logistics: Deep Dive Illustrates Balanced Growth Outlook

2023-11-29 20:25:37 ET

Summary

- Logistics and supply chain companies are attracting investment as companies review and implement supply chain changes.

- GXO Logistics, a contract logistics provider, has its core offerings in warehousing, distribution, and e-commerce.

- However, high multiples on a flat growth outlook make GXO a challenging investment at this point in time in my opinion.

Investment briefing

If the last 2.5 years taught us anything economically it is that resilient supply chains are no longer a ‘given’. Large sigma macroeconomic events across 2020–’21 showed they can jolt supply chain economics rapidly unless something changed across the board.

Thankfully, companies are taking notice. A recent S&P Global Intelligence report noted there is “ as supply chain activities have normalized, corporations are reviewing and implementing supply chain changes in the light of the past three years. The second half of 2023 should bring more announcements of long-term supply chain strategy choices” .

The stage is therefore set for logistics + supply chain companies to attract capital flows and investment, potentially driving valuations in the sector higher.

Moreover, freight and logistics is well positioned for sales and earnings growth. Text from the Global Freight & Logistics Market Outlook 2023–2030 projects a geometric growth of 7.4% into 2027 for the sector. Selective operators within the space may offer compelling investment opportunities, under the right economic assumptions.

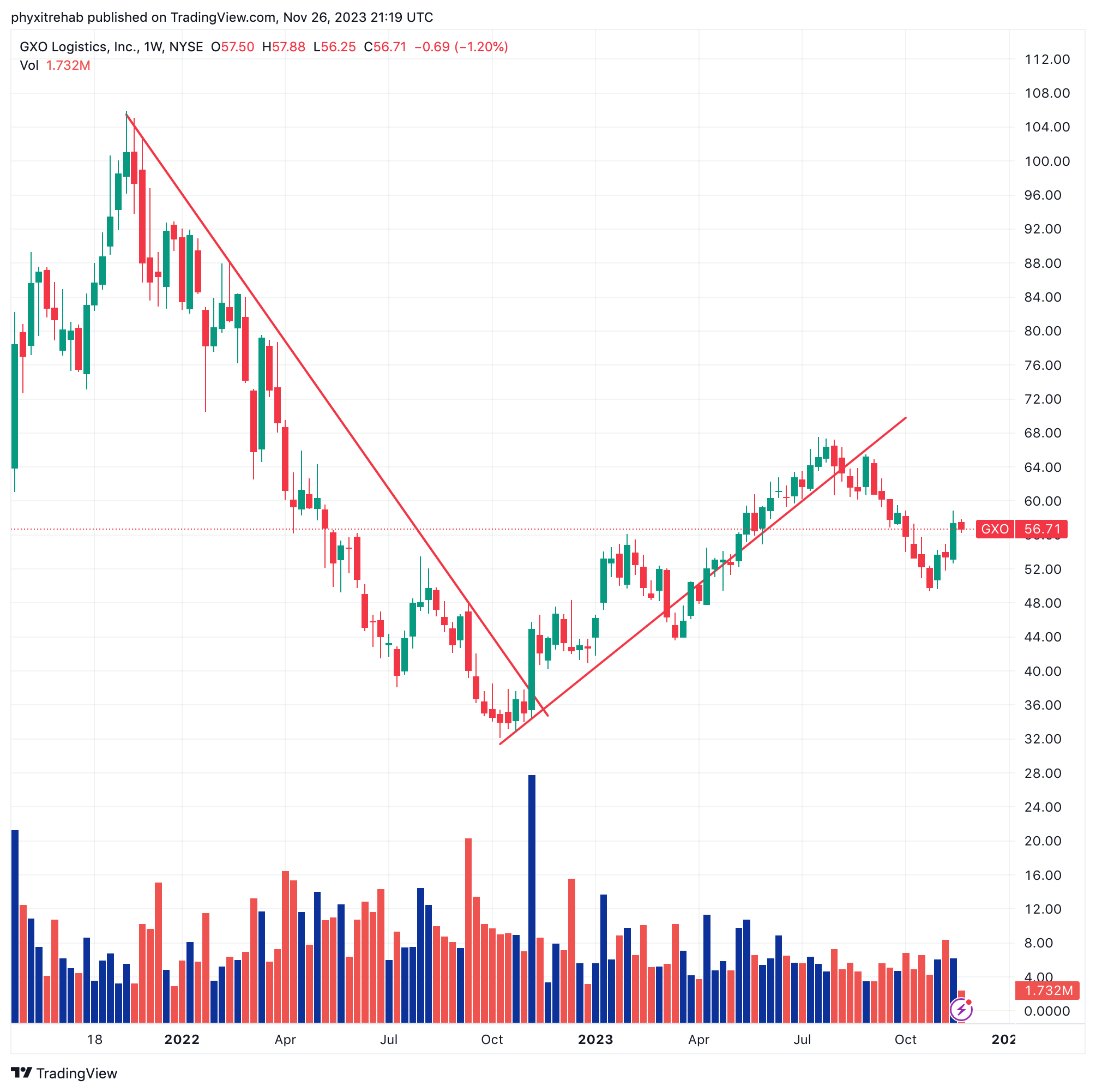

Trawling the space for selective opportunities, GXO Logistics ( GXO ) has come onto our radar seeing its bounce from October lows (Figure 1).

Readers might recall the GXO spin-off from XPO ( XPO ) in August 2021. The newly-listed company specializes in contract logistics services. Per the 10–Q, it is “ the largest pure-play contract logistics provider in the world ”. The critical facts are as follows:

- GXO’s core offerings are in warehousing, distribution, order fulfillment, e-commerce, and so forth. Its core geographies encompass the Americas, APAC, the UK, and Europe.

- It operates 197 million sq. ft of facility real estate across 979 facilities globally. Customer-wise, it caters mostly to major corporations outsourcing their warehousing and distribution needs. These include e-commerce, retail, technology, food and beverage and such, just to list a few.

- The company’s “asset light” model is leaning towards 40% of all revenue earned from automation. In a high-inflation/rates world, this is a smart move to reduce capital intensity and free up cash flow in my opinion.

- The company sells at 22x forward earnings , 2.3x book value and 22x forward EBIT. You receive net assets producing 7.5% trailing ROE and capital producing 6% ROIC at these prices.

- Cash spun off to shareholders has flattened since 2020. There’s been no growth in FCF per share since then.

Figure 1.

{kind=link}

The question is whether the market is forecasting a period of better business for GXO. With the advance in market value, this may be so. Naturally, the next question is how much of this is already reflected in current market prices.

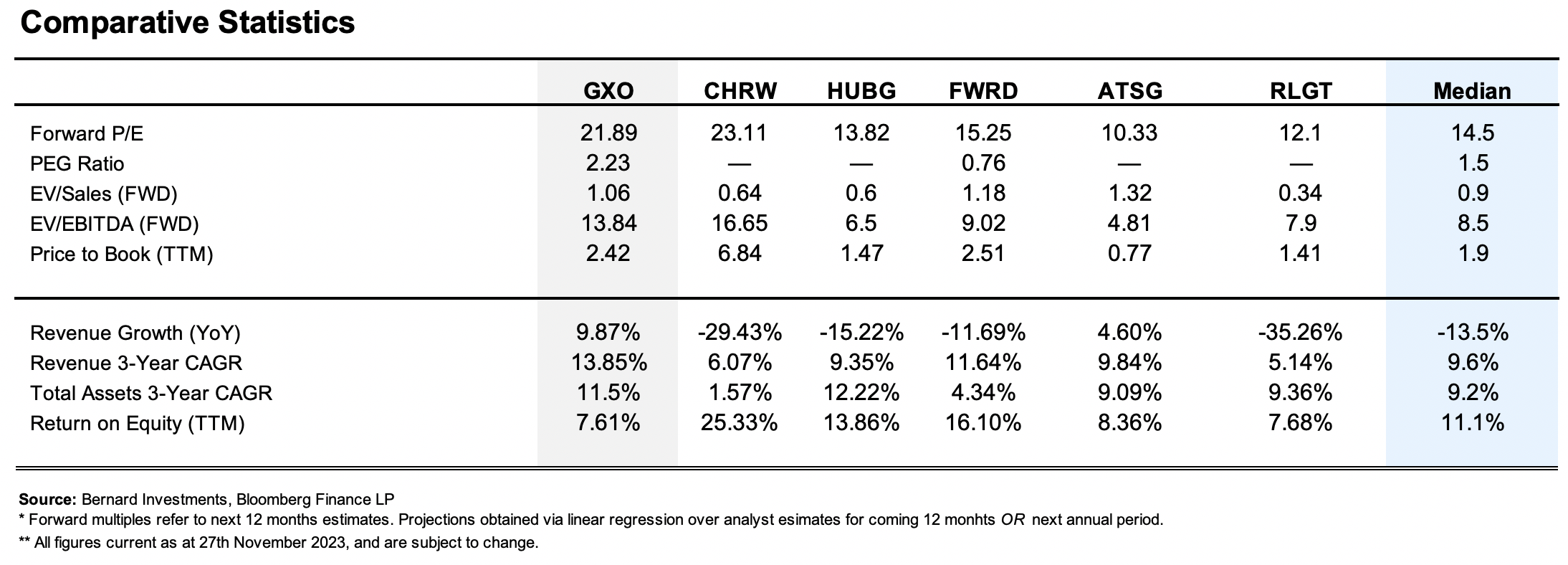

A more thoughtful analysis of the economic assumptions underneath it all reveals an absence of ‘bank for the buck’. Comparative statistics of the firm’s value drivers + market multiples are observed in Figure 2.

Critically:

- GXO is priced above peers on median,

- Growth projections look well captured at current prices,

- Historical growth relative to net assets employed is less attractive,

- Asset growth matching sales growth (11.5% to 13.8% respectively), in contradiction to management’s “asset light” comments

Bloomberg Finance LP, BIG Insights

{kind=link}

Consequently, given (i) the premium multiples, (ii) the mediocre sales + earnings growth to the entire stock universe, and (iii) unattractive business returns, it may be a period of difficult investment returns for the company’s owners. Net-net, I rate GXO a hold across all investment horizons.

Critical facts to investment thesis

-

Multiples; Sales + earnings growth

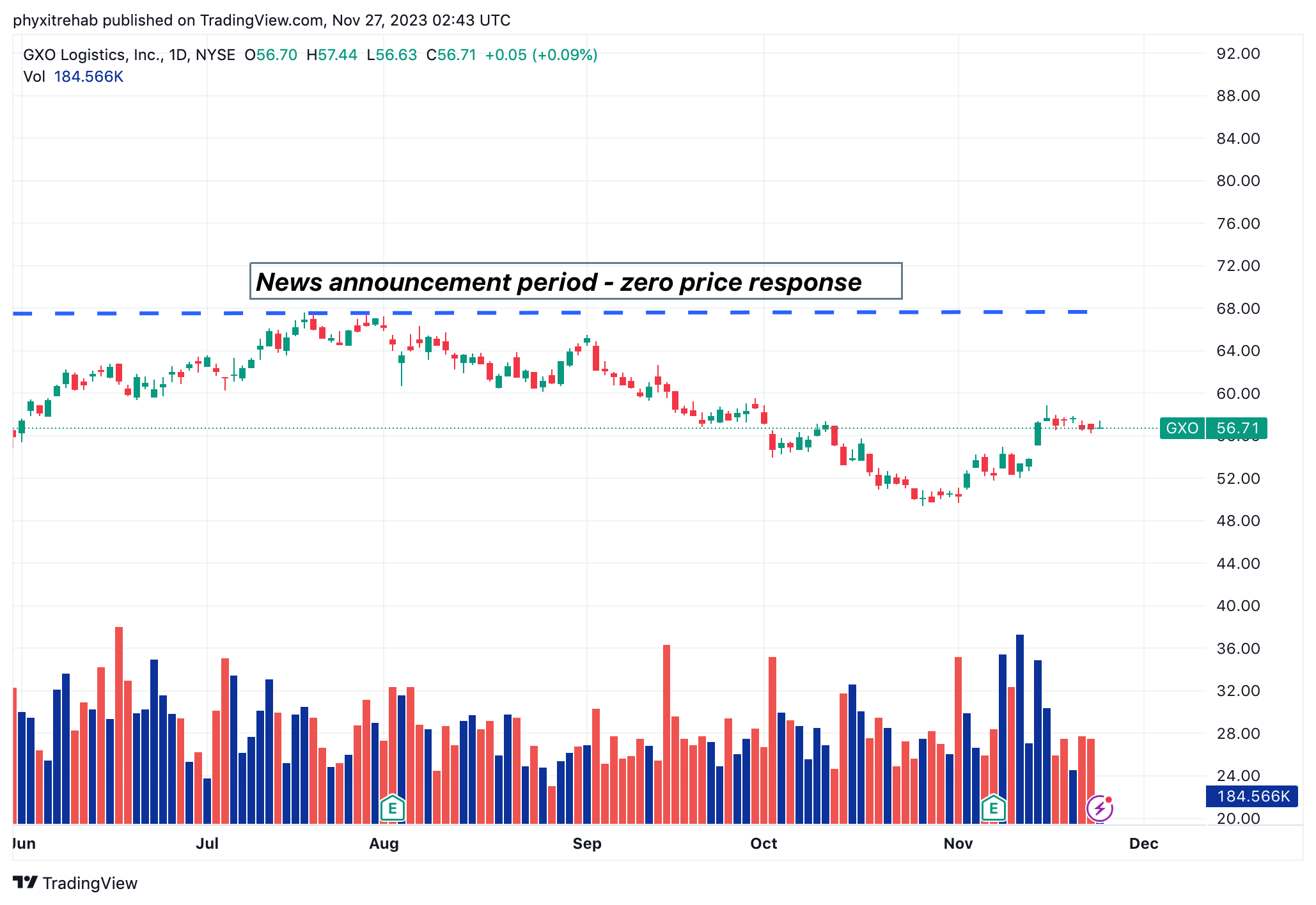

The stock trades at ~22x forward earnings and 22x forward EBIT, premiums of 25% and 44% to the sector, respectively. Growth is well captured with the PEG ratio of 2.2x. The market has also valued its net assets at 2.4x book value at the time of writing. There have been several potential price catalysts in the last few months, as seen in Figure 3. None of which have received tremendous praise from the market, as seen in Figure 3a.

Figure 3. Seeking Alpha news headlines announcing GXO’s business updates, Jun–Nov 2023

{kind=link}

Figure 3a.

{kind=link}

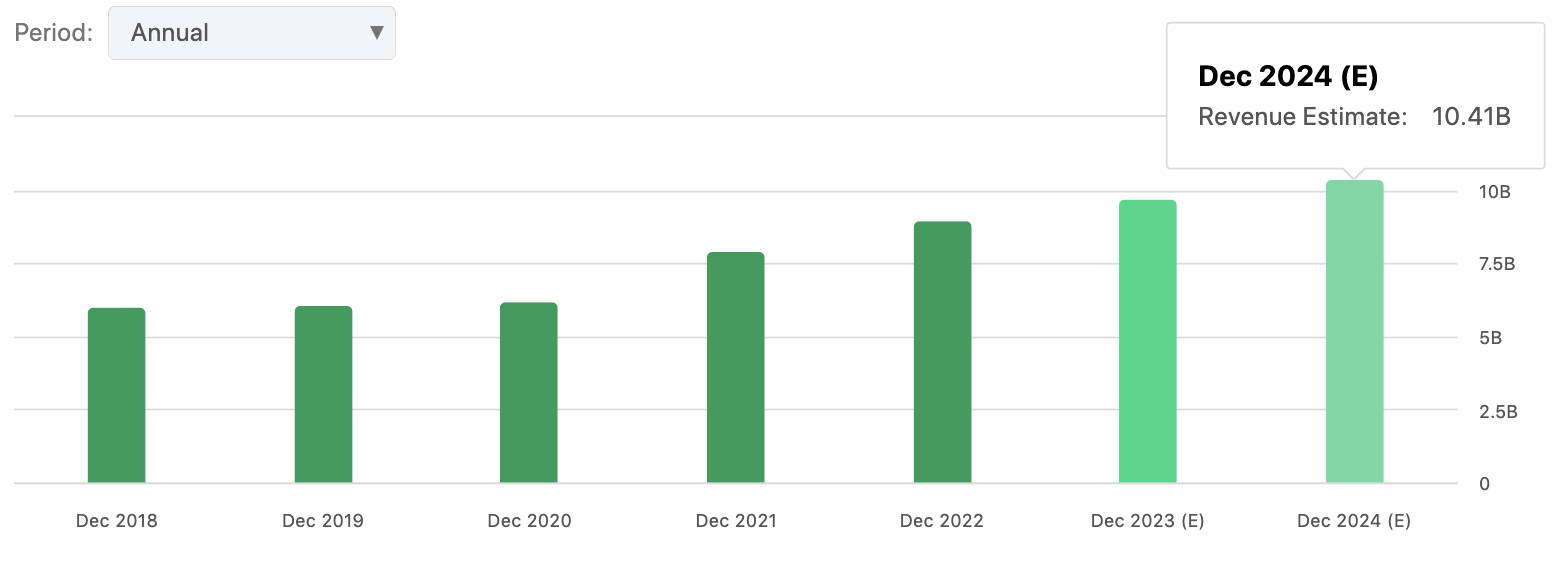

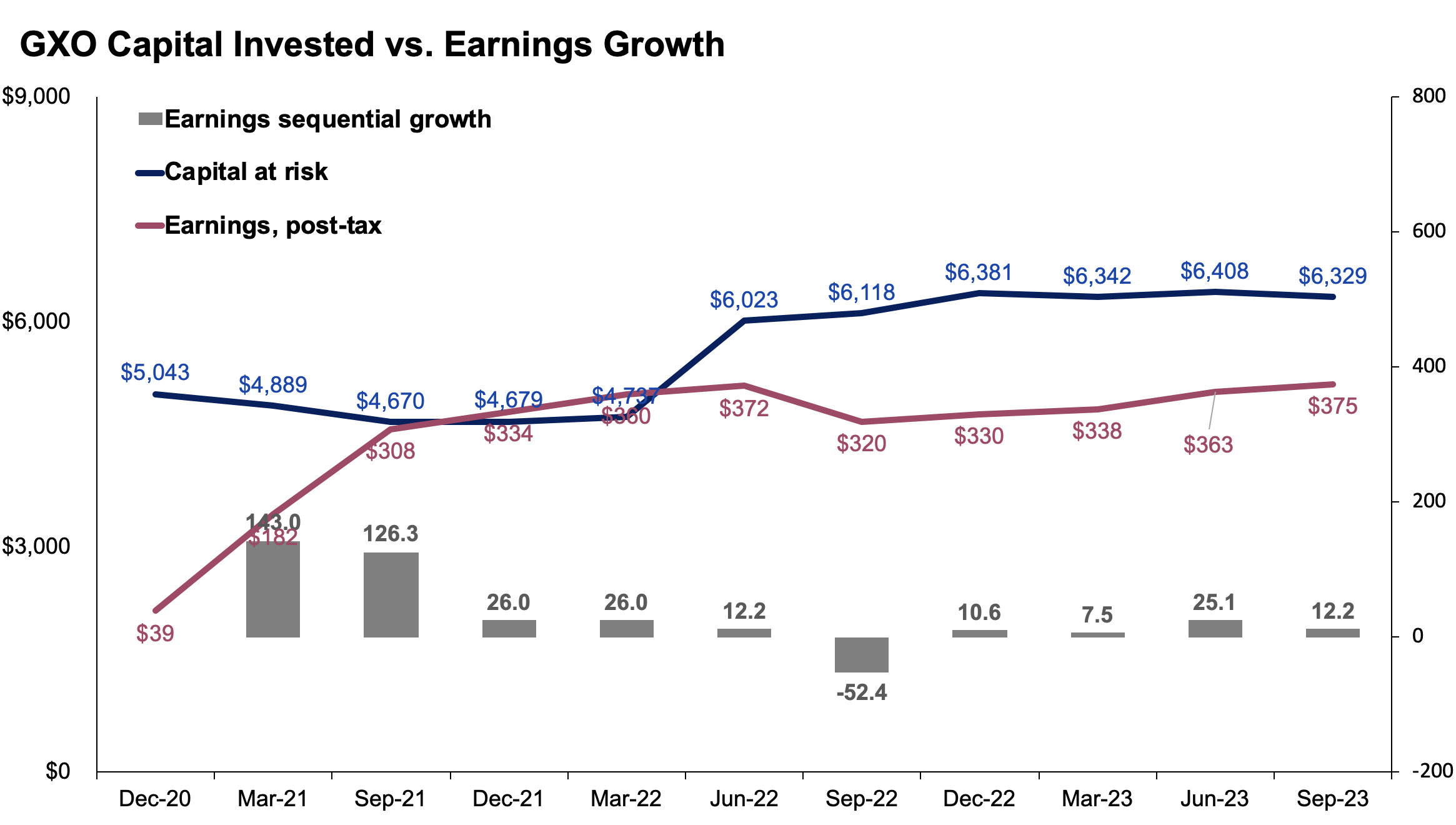

Meanwhile, the sales ramp from 2020 has been linear (Figure 4). Analysts are eyeing $10.4Bn or 8.5% growth in sales by FY’24, on earnings growth of 12.4% and 14.7% in FY’24 and ’25, respectively. Linear regression of analyst estimates illustrates the market has a required rate of 26% to own GXO today, ranging from 24–37% depending on various inputs (discussed later). This is perceived as a high-risk affair, due to the high compensation demanded for owning the company.

Earnings growth been lumpy. Since its listing, pre-tax income is up 11-12% on TTM earnings (post-tax) of $1.68 per share. Forward growth is for 12–14% in the next 2 years, as mentioned earlier—but this may not be accretive to shareholder value, unless the earnings relative to assets and equity (and share price) start to improve.

The following investment conclusions are drawn from these insights:

- Scope for forward 12-month returns is narrowed by the high asking multiples of 22x forward earnings/EBIT. With the projected growth rates and premiums to sector, growing beyond these ratios looks to be a challenge.

- Forward growth projections do not justify the high premiums in my opinion. Sales growth is in line with sector averages, whilst earnings is forecast above-average—not at a rate sufficient to justify 22x forward earnings, however.

- Meshing these two points together, the prospects for investment returns in owning GXO for the next 12 months – 3 years looks potentially clamped, unless either a sharp change in valuation or major catalyst.

Figure 4.

{kind=link}

2. Economics of shareholder value

Return on equity (Shareholder returns)

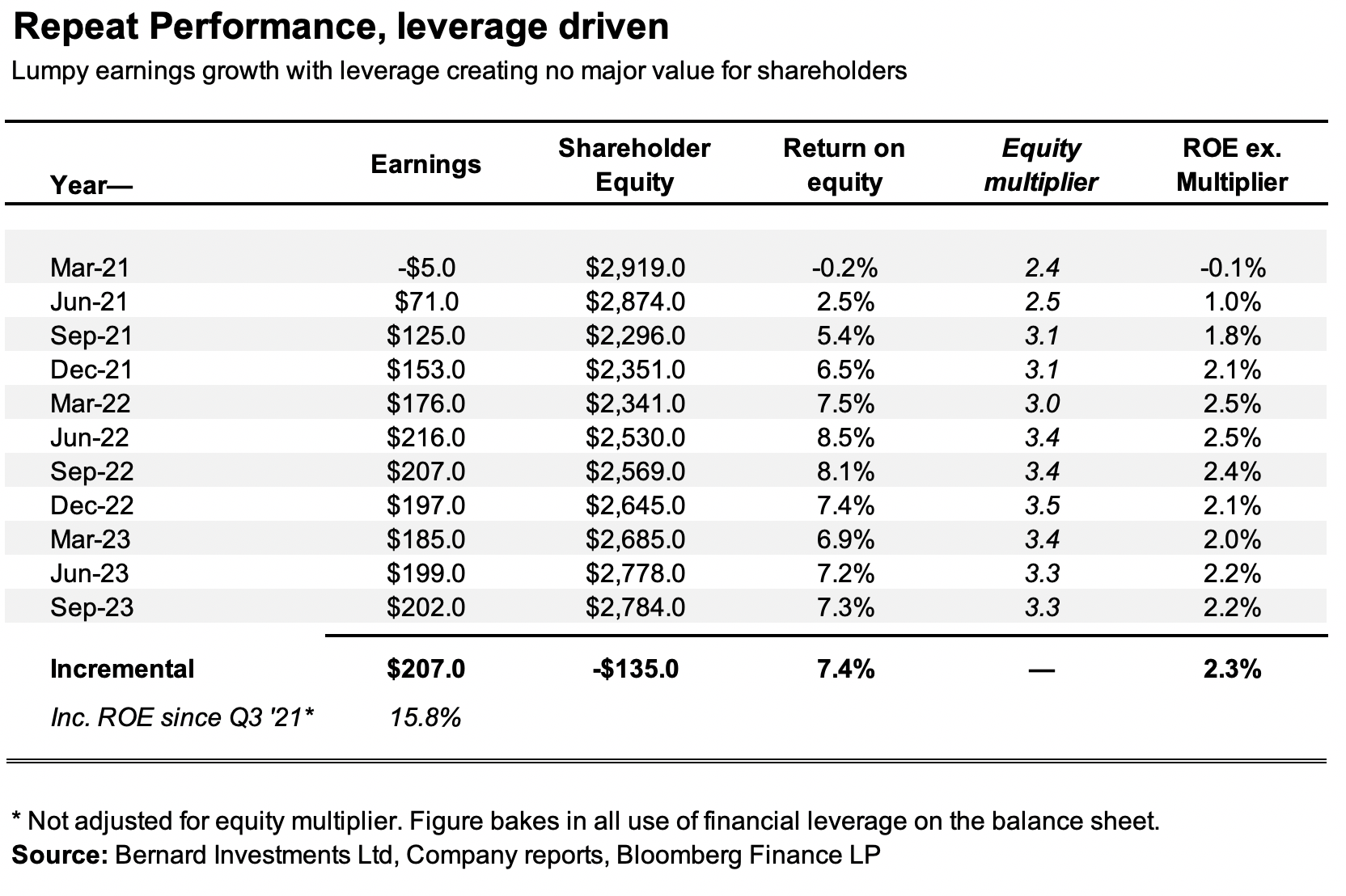

The company has retained negative $135mm in additional equity since 2021, with earnings up $207mm in that time (TTM values). Since Q3 2021, the return on incremental equity is 15.8%, indicating a $0.15 gain in earnings for every $1 gain in shareholder equity.

Return on equity has averaged around 7% since 2021, as seen in Figure 5. With single-digit returns on net assets supporting earnings growth, it is unsurprising to see the lumpy profits.

Critically, the use of leverage has increased the rate on equity substantially. Removing the equity multiplier (assets/equity) across the time series, the average ROE produced for GXO’s owners since 2021 was 2.2%. The value created for equity holders was therefore minimal.

Figure 5.

{kind=link}

The above is a classic example of ‘not all growth is created equally’. It is crucial the earnings growth produced each YoY is matched to assets, capital, plus market value. GXO currently trades at the price of 2.4x net asset value (book value).

Paying this multiple implies the following:

(i) You are paying 2.4x the company’s equity value to receive an avg. c.7% rate of return ((TTM)),

(ii) This works to be (2.4 x $2,784 = $6,682), where the company trades as I write,

(iii) The TTM ROE—already tight—is 7.3%, but reduces to 3% for the investor if paying 2.4x (2.4 x 2,784 = 6,682; $202 / 6,682 = ~3%),

(iv) Consequently, you are actually paying 2.4x forward to receive a c.3% return on equity as the investor.

Consequently, whilst the consensus has reasonable bottom-line growth projections for GXO, with the combination of 1) today’s multiples and 2) the forward rates on equity, the investor ROE may only amount to 4–6% on earnings growth of 12–14%. How this translates to the shareholder remains to be seen in my view.

Figure 6.

{kind=link}

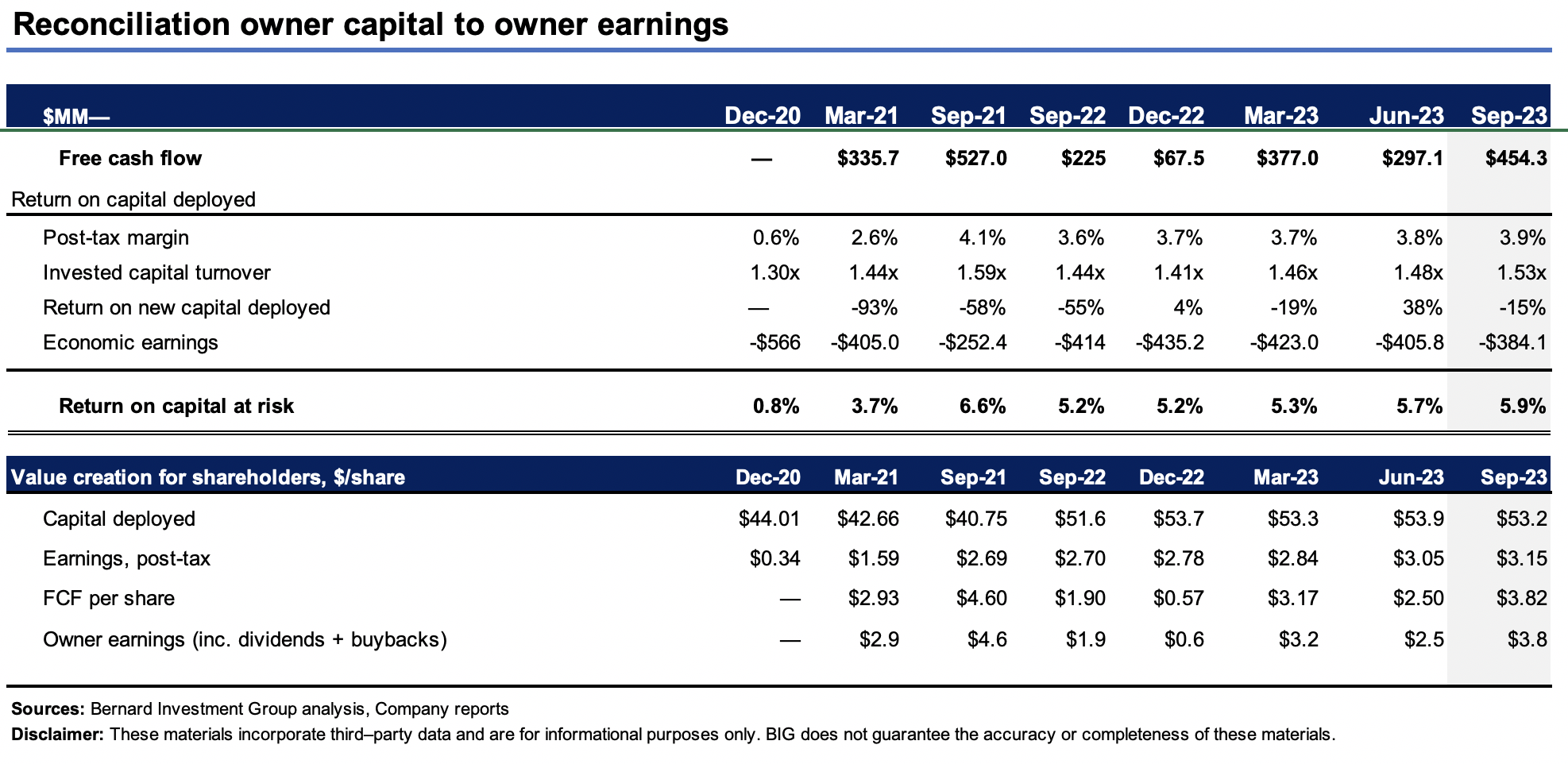

Unit capital + FCF per share (Business Returns)

GXO’s business returns lag similar to its shareholder returns. On close examination, this is a low margin, high capital turnover business. Post-tax margins are <5%, with capital turnover of 1.5x not enough to overcome this at the return level (Figure 7).

The situation on business returns is:

- GXO has $53/share of capital invested in the business as of Q3 ’23. It produced $3.15 in trailing NOPAT on this last period—6% return on investment, in line with averages (Figure 7).

- Long-term market averages are around 12% return.

- As a result, the company’s earnings are not ‘economically’ valuable to us, seeing as we use this 12% threshold margin for all equities.

- Those economic earnings (above the 12%) are quintessential to compound GXO’s intrinsic value.

In summary:

A long-term average 6% ROIC vs. 12% hurdle rate, producing no economic earnings per share to compound intrinsic value.

Figure 7.

{kind=link}

The company has produced the following direct value for shareholders:

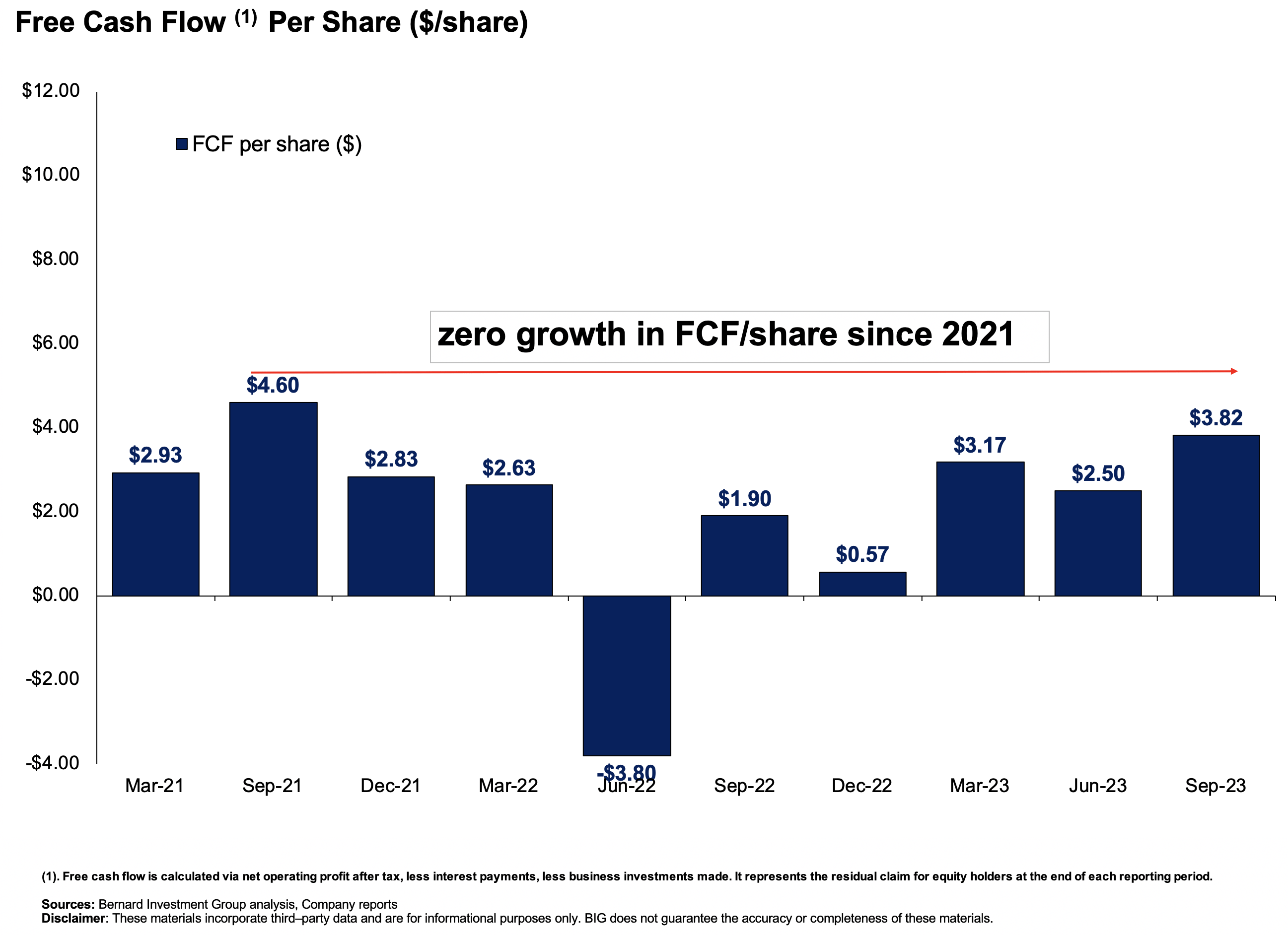

- It has thrown off $21.14 per share in cumulative free cash flow (“FCF”) since Q1 2021 (rolling TTM basis). The change in market value since listing in July is ~$2.20/share on writing.

- Critically, there has been no growth in FCF per share since late 2021. This would be acceptable if business returns were high, indicating the cash has been redeployed into the business to create more profits. We aren’t seeing evidence of this here.

- Going forward, my judgement is this trend could continue going forward. The company is not growing earnings at a pace that outmatches the capital cost it requires to expand. This is choking up resources and suggests potential inefficiency. The ratio of sales to capital in the business doesn't outweigh the tight margins, as discussed earlier.

Figure 8.

{kind=link}

Valuation + conclusion

The stock sells at 22x forward earnings and EBIT as mentioned earlier. Growth has to also be factored in here. The PEG ratio is 2.2x forward indicating the valuation captures growth and then some. In Figure 9, you also see (1) GXO's sequential earnings growth taper off alongside (2) the rate of earnings/cash flow reinvestment.

Paying 2.4x book value is not a kind proposition as discussed earlier and similar logic applies to earnings. Therefore, on asset factors and earnings power, GXO might be a little stretched here at 22x earnings/2.4x book. A pullback to the sector multiple of 17x might have more interested so I'll be eyeing this level closely moving forward..

Figure 9.

Source: BIG Insights, Company reports,

{kind=link}

In short, there are positives that lift up the case for GXO. These include:

1) Free cash flow positive, stable and positive ROE,

2) Projected sales + earnings growth out the next 2 years,

3) Multiple potential news catalysts (yet to be seen in price change).

But these points are balanced. On my analysis, the company's growth hasn't provided economic value for shareholders, yet. The reasons are three fold as well. One, shareholder returns on equity—below 10%, and more than halved without leverage. Two, business returns are similar, lacking economic profits. Three, cash is there, but not recycled at high rates of return, and less attractive at 22x earnings.

Collectively, the negatives outweigh the positives here. Net-net, rate hold.

For further details see:

GXO Logistics: Deep Dive Illustrates Balanced Growth Outlook