FUL - H.B. Fuller: Disappointing Quarterly Results

2023-10-04 02:01:43 ET

Summary

- H.B. Fuller Company posted Q3 FY23 results with a decline in net revenue and net income compared to the previous year.

- The company continues to face headwinds, particularly in the HHC and construction adhesives segments, which are expected to impact future quarters.

- The stock is trading at a higher valuation than its historical average and sector median, suggesting a potential adjustment in the future. It is better to avoid it.

H.B. Fuller Company ( FUL ) markets adhesives, polymers, encapsulants, and other chemicals globally. In my last report , I told to avoid it, and the stock hasn’t moved much since then. I am still firm on my stance. It recently posted its Q3 FY23 results. The company continues to face the same headwinds that it faced in the previous quarter, and it is expected to affect them in the coming quarters. So I think it will be wise to avoid it. The price action and valuation indicate that one can get it at a better price level. So, I assign a hold rating.

Financial Analysis

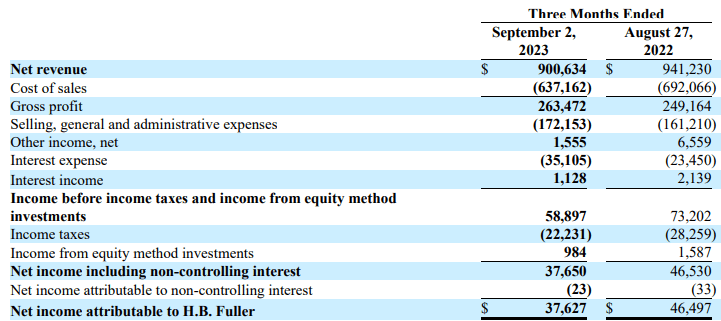

It recently posted its Q3 FY23 results . The net revenue for Q3 FY23 was $900.6 million, a decline of 4.3% compared to Q3 FY22. Underperformance in its HHC and construction adhesives segments was the major reason behind the decline. The revenue from the HHC and construction adhesives segment declined by 5.3% and 4% in Q3 FY23 compared to Q3 FY22. The company faced the same issues that it faced in the previous quarter. Both these segments were affected by the customer destocking actions, which led to a decline in demand and volume. However, the management used its pricing power to improve the gross margins. Its gross margin for Q3 FY23 was 29.2%, which was 26.4% in Q3 FY22.

{kind=link}

The net income for Q3 FY23 was $37.6 million, a decline of 19% compared to Q3 FY22. The company’s short-term future is not looking good, as I think the adverse economic situation is weakening the company's financial position. In the previous quarter, it faced destocking headwinds and is continuing to face, especially in the health and consumable adhesives [HHC] segment, and it is expected to affect this segment in the next quarter, too. Talking about the other two segments, construction adhesives [CA] and engineering adhesives [EA], neither of these segments was affected by the destocking activities on a large scale and is expected to diminish by the fourth quarter. However, these two segments are mainly affected by weakness in the construction-related end markets, and I don't see the construction market recovering soon, especially in North America and Europe, due to higher interest and mortgage rates. Hence, I expect weakness to continue in the coming quarters, which might affect the upcoming financial results.

Technical Analysis

{kind=link}

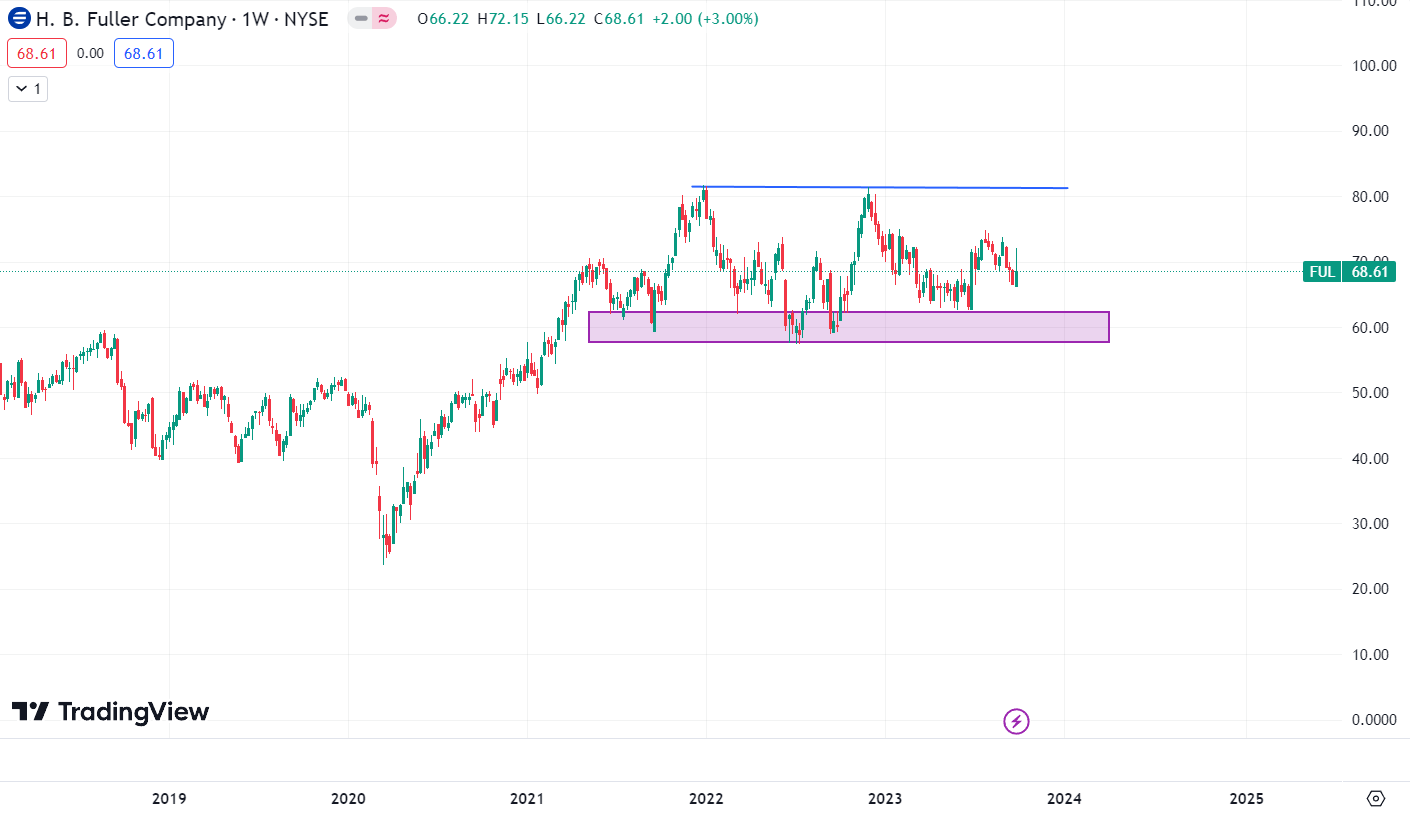

It is trading at $68.6. Well, the stock hasn’t moved much since the last time I covered it. The most recent weekly candle has a huge wick, which shows selling pressure. Talking about the downside possibility, looking at the selling pressure, I think the stock price might fall up to the support zone of $58-$62. Buying at the current level might not be smart, as I think one can get this stock at a discount price. The stock has taken support from the $58-$62 level six times in the past two years. So, I think one can accumulate the stock when it reaches the support zone, but until then, it is better to avoid it.

Should One Invest In FUL?

First, look at the company’s valuation . It is trading at a P/E [FWD] ratio of 17.89X, which is higher than its five-year average of 16.61x and the sector median of 13.54x. It has an EV / Sales [FWD] ratio of 1.57x compared to the sector median of 1.46x. The company reported results that showed weakness, and the future outlook isn’t positive. So, I think the high valuation might get adjusted in the coming times. If we take its EPS [FWD] of $3.82, I think it can trade around a P/E of 16.6x. This gives us a share price of $63.4. So, it shows a slight downfall from the current level, and I believe buying the stock at $63.4 is a better decision because I think it is the true value of the company according to its performance, and the technical chart also shows solid support around this price. So, looking at all the factors, I assign a hold rating.

Risk

About 75% of their cost of sales in 2022 came from the cost of raw materials. Based on 2022 financial results, a fictitious 1% change in their raw material costs would have affected net income by about $15.7 million, or $0.28 per diluted share. As a result, fluctuations in the price of raw materials caused by inflation, supplier disruptions, scarcity, and other factors may greatly influence their income. Many of the raw ingredients used in product manufacturing come from different vendors and are petroleum and natural gas derivatives. These raw materials are often offered on the open market by a range of producers under typical market conditions. Although alternatives exist for most essential raw materials, supplier production interruptions could cause supply-demand imbalances for some raw resources. In order to replace important raw materials, they must find new suppliers, reformulate their products, conduct new tests, and possibly ask their existing clients for reapproval. Changes may occasionally hamper their capacity to get necessary resources or the cost of producing goods in the prices. They could be unable to pass on these increases to their consumers in a timely manner if raw material prices rise quickly, which could result in a decline in their profit margins.

Bottom Line

The quarterly results have shown weakness, and the future outlook isn’t positive, which might affect the share price. In addition, I think one can get this stock at a better-discounted price, and both the technicals and valuation show a slight downside. Hence, I assign a hold rating on H.B. Fuller.

For further details see:

H.B. Fuller: Disappointing Quarterly Results