HMRZF - H & M: Challenged Present Hopeful Future

2023-03-23 11:35:02 ET

Summary

- The Swedish fashion brand H & M might be popular, but it is struggling in the stock markets right now.

- Its YTD price rise is less than that for the S&P Consumer Discretionary sector, as there appears to be uncertainty regarding its profits. The company's P/E ratio is elevated too.

- It is optimistic about 2023, notably expecting much improvement in operating margins. But it is a wait and watch situation for now.

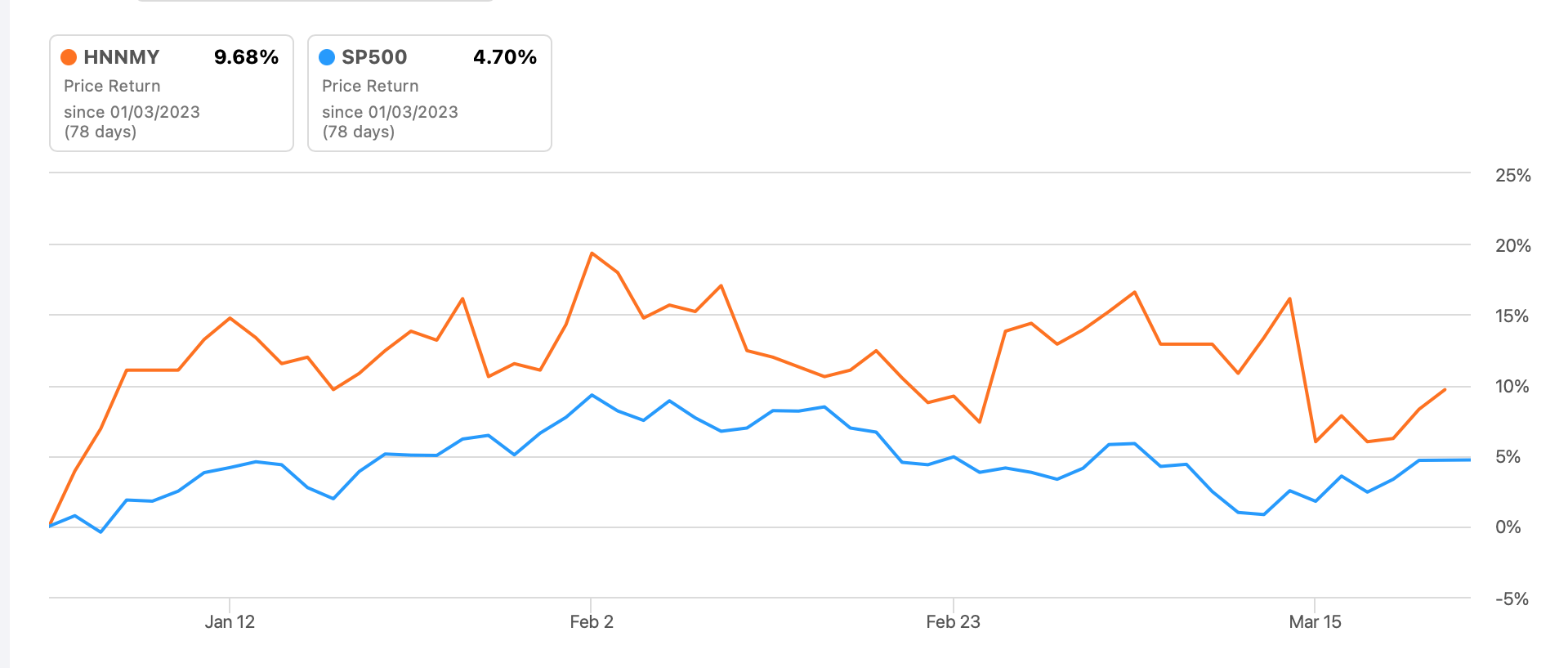

After a disappointing 2022, the popular Swedish fashion brand H & M Hennes & Mauritz AB ( HNNMY ) has seen some recovery in price year-to-date [YTD] with a rise of 9.7%. But it has lagged that of the S&P Consumer Discretionary Index, which is up by 12.6% . Here I unpack what is holding H & M back, what it means for its price and importantly, what it indicates for its considerable trailing twelve-month [TTM] dividend yield of 5.4%.

{kind=link}

Can H & M’s profits rise?

The starting point for this analysis is its trading update on sales for the first quarter (December 1, 2022- February 28, 2023) of the financial year 2022, released a few days ago. The numbers are not bad. Its net sales are up by 12% year-on-year [YoY], consistent with growth seen in the final quarter of its financial 2022.

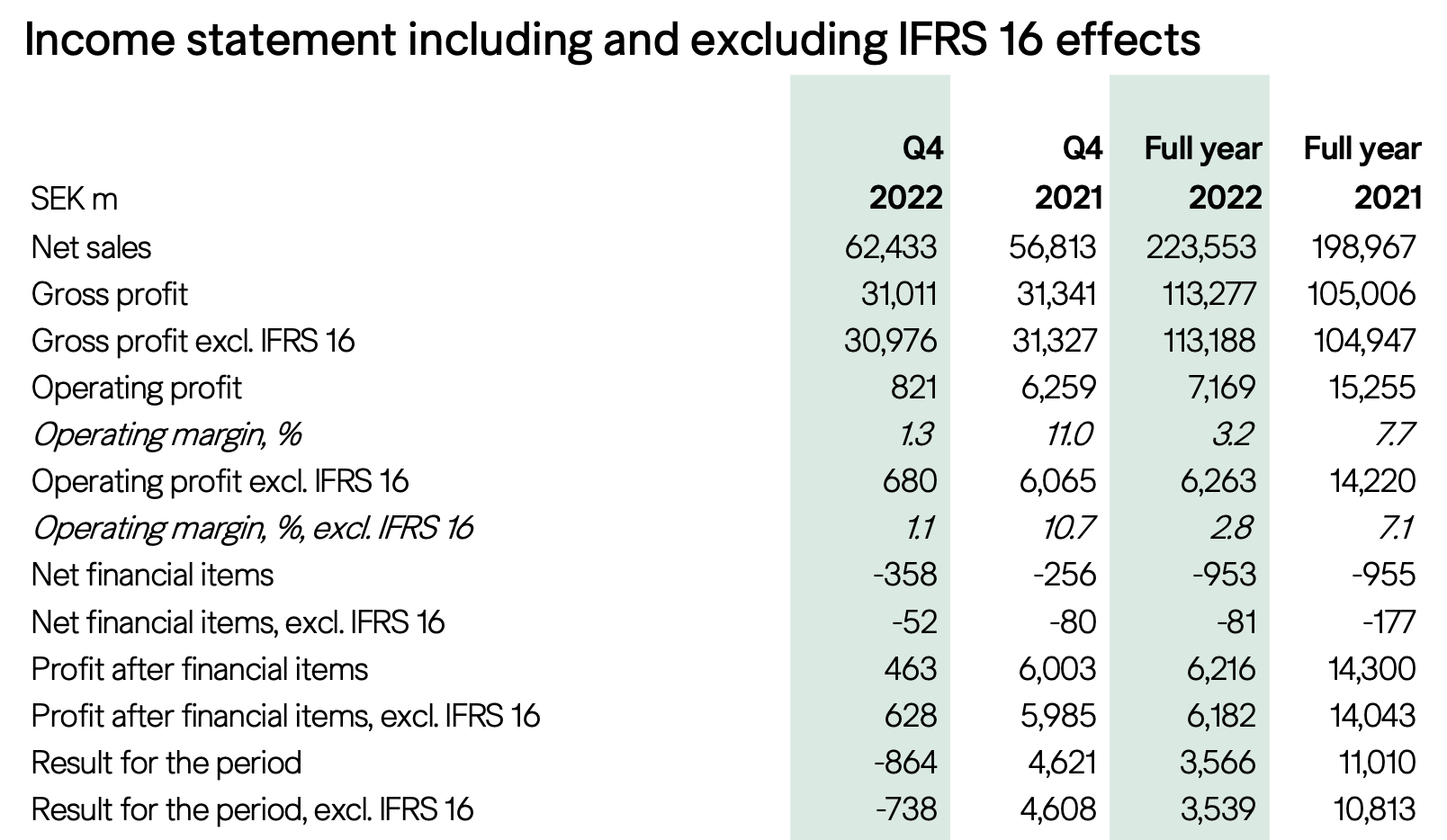

When it releases its full quarterly report on March 30, we will know more about how far this translates into its bottom line. This is one to watch out for even more keenly than usual after it reported a net loss last quarter. There were several reasons for this, including the loss of profit from its Russian operations and a one-time cost for its cost and efficiency program. But the biggest drag was cost inflation and exchange rate fluctuations, which cost it SEK 3.6 billion . If it were not for these drags, H&M’s net profit would have been in excess of its SEK 4.6 billion level in Q4 2021.

{kind=link}

So what does this tell us about its potential profits for the first quarter? If we remove the impact of the restructuring charge , which is related to administrative and overhead costs and workforce reduction, of SEK 836 million, that alone is enough to bring the company close to profits, considering its Q4 2022 numbers. With some cooling off in inflation, operating costs of raw materials and energy, which have played a substantial role in H&M reporting a loss in the past quarter, it could even report a profit.

However, that is one way of looking at it. Whether it happens would depend largely on how far it is still being impacted by cost inflation. Until the last quarter, operating costs were going strong, increasing by 20.4% year-on-year (YoY). If we assume that they continue to rise at the average of the last four quarters’ increase of 18.1% , it turns out that the company could report an operating loss even with the latest increase in sales. In other words, it cannot be said for sure that H&M made a profit in the last quarter.

What does the outlook indicate?

However, the company is far from pessimistic. In fact, in its guidance for this year, it says “….there are very good prerequisites for 2023 to be a year of increased sales, and improved profitability. Thus, our goal of achieving a double-digit operating margin for full-year 2024 remains in place”.

The outlook on operating margin is particularly notable. For the last year, it has a low operating margin of 3.2% and it has not reported a double-digit margin since its financial year 2017.

Can its market valuations improve?

If it does manage to bring its operating margin up to 10%, and assuming it continues to show the 12% growth seen in Q1 2023 as well as a constant ratio of operating income to net income in the next year, its forward price-to-earnings (P/E) ratio looks significantly improved at 16.3x.

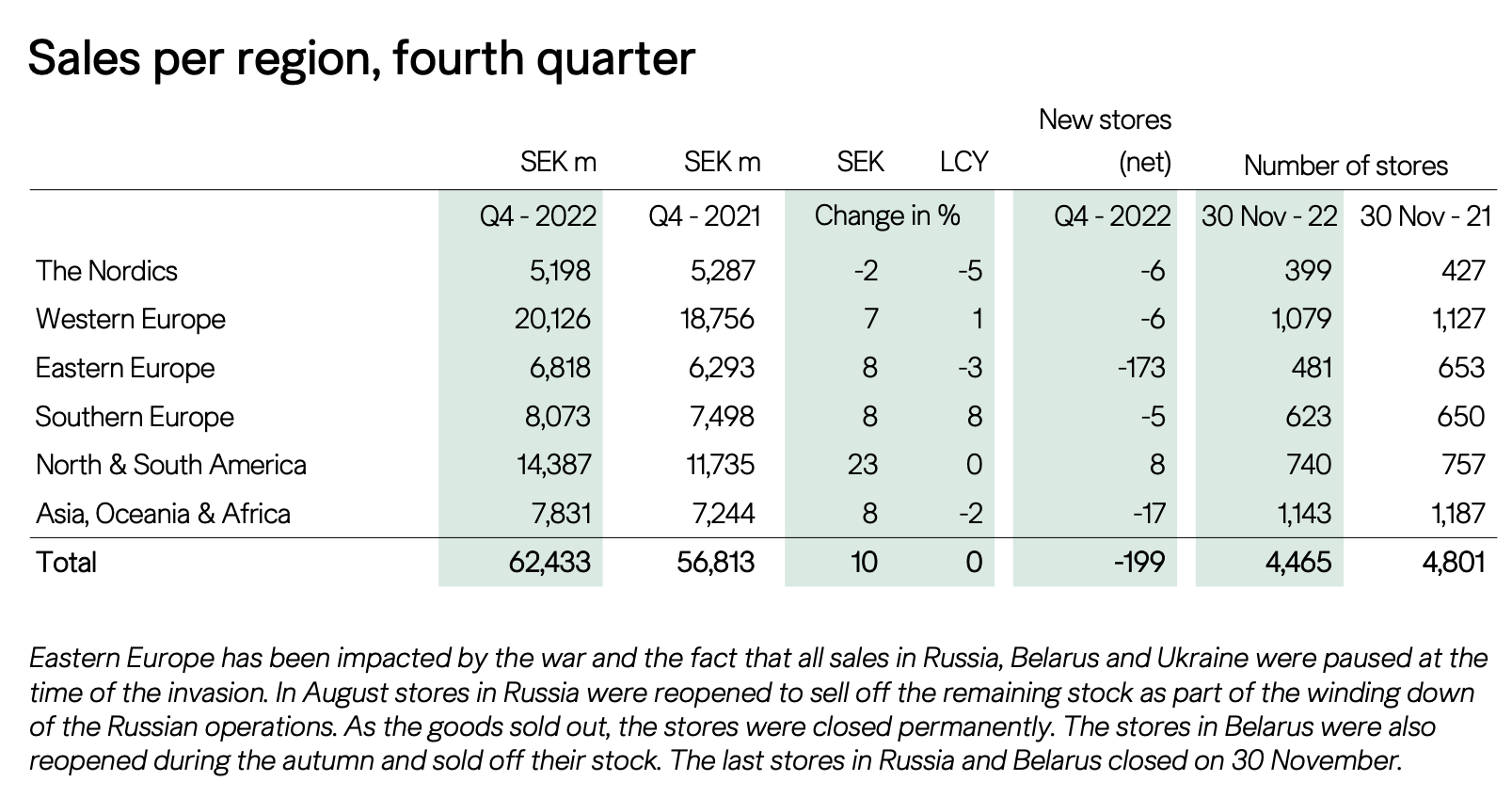

However, the assumptions in this calculation have to be accurate. As I see it the one big risk to the company this year is the slowdown in its key markets of Western Europe and North and South America (see table below). With a persistent cost-of-living crisis and an expected slowdown in growth, it is possible that demand could slow down.

{kind=link}

Moreover, as of now, it appears unclear if the company’s earnings are going to improve immediately. This of course does not bode well for its valuations in the near term. The company’s trailing twelve months [TTM] price-to-earnings (P/E) ratio currently stands at 57.3x, which is significantly in excess of the 14.8x for the consumer discretionary sector. This of course is explained by its loss in the last quarter. And considering that there is little to suggest clear signs of a big revival in its profits in Q1 2023 either, it is to be expected that the company’s P/E will remain elevated in the foreseeable future too.

What of its dividends?

At present, the company’s TTM dividend yield is at a healthy 5.4%. But there is a risk to it if its profits do not improve. Consider this. Its dividend payout ratio is at a massive 300% at present. This is unsustainable by any standards since it shows that dividends are significantly higher than its net income.

To be fair, though, the company has always had an elevated dividend payout ratio. Even before the pandemic, in its financial year 2019, H&M’s ratio was at 120%. Also, in its guidance for this year, the company has maintained its dividend levels from the year before so far, and if its profits improve as it expects, the payout ratio could look improved over time as well.

What next?

In essence, the H&M story can be divided into two parts. The first is the immediate future and the second is a view over the rest of its financial year 2023. At present, there is nothing to suggest that its profits can improve significantly immediately, especially as inflation remains elevated. Its restructuring program will have benefits and its sales growth in Q1 2023 is strong, which could have a positive impact, but how much, remains to be seen. With a high TTM P/E ratio, right now, an increase in its price seems unlikely.

Over the course of the year, however, it seems optimistic about its prospects. Notably, a return to an operating margin in double-digits suggests healthy improvements in profit. This can make its P/E ratio far more attractive and also support its dividend pay-outs. But we have to wait for an indication of improvements there.

If it happens as early as later this month when it releases its full quarterly report, H&M can start rising. If the improvements do not happen until later, it can languish some more. There is some solace from its expected dividend payout for this year, but I would look out for its profits to ascertain the risk related to them, or not. In light of its uncertain situation, I am putting a Hold rating on H&M.

For further details see:

H & M: Challenged Present, Hopeful Future