HMRZF - H & M: Difficult To Evaluate The Future I Say 'Hold'

2023-06-05 05:54:46 ET

Summary

- Hennes & Mauritz (H&M) has been struggling with declining fundamentals for years, and its complicated ownership structure makes it incompatible with long-term ownership.

- The company's majority shareholder has been buying shares, potentially signaling a move to take the company private in the next 3-6 years.

- I suggest selling short-dated, conservative cash-secured Puts to take advantage of the stock's volatility, while holding off on buying the common shares until a fundamental turnaround is evident.

Dear readers/followers,

H & M Hennes & Mauritz AB (publ) ( OTCPK:HNNMY ) is a company that I've been using over the past 1-2 years to trade options with. The company is a popular native Swedish stock in consumer discretionary, but it's well-known across the world. However, the company has been struggling for years, and a complicated ownership structure has made the company, as I see it, incompatible with long-term ownership, at least for me. That does not mean I cannot "trade" in it, but it does mean that I usually don't want much to do with the company for a long time.

Hennes & Mauritz, or H&M, does have the advantage of global scale, a loyal following, and a long history in its field. But its fundamentals are a very clear tale of negative trends that I will run through with you here and show you how I personally approach this company as an investment.

Hennes & Mauritz - I'm not that impressed

There was a time when I started investing when H&M was lauded as a Swedish, super-safe dividend stock. It was a stock that many dividend investors owned forever because it wouldn't go anywhere.

Then came the drop-down in fundamentals, which has been going on for years at this time. The horror show came in 2020 though, when the company cut it's very long, storied dividend. let's take a look into the past.

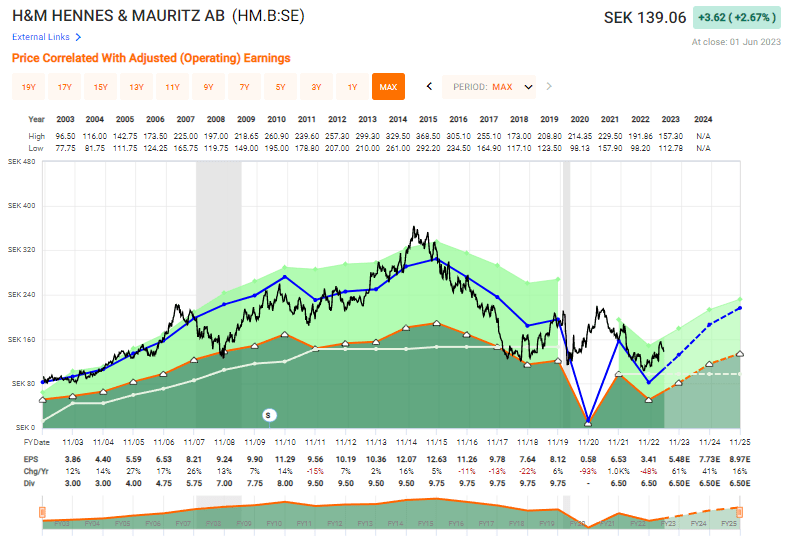

{kind=link}

As you can see, the company reached double-digit EPS back in 2010 - but they never really went much further than that, except a brief 12.63 in 2015. The dividend went up to 9.75 SEK/share back in 2015, then never moved from that until 2020. They even kept it much longer than they should, when the company's earnings back in 2017 and beyond, either definitely did not or barely supported that dividend, then finally zeroed it entirely in COVID-19.

I was out of the common share bay 2015/2016, not at a loss, but at not a good profit either. It was one of the last stocks in Sweden where I took what someone else said for granted.

H&M is BBB-rated, but has seen declining fundamentals for several years. Its Gross margins are 50%+, which is excellent. Its net margins are 1.7%, which based on that gross margin is absolutely abysmal. Like many discretionaries, the company has a large SG&A and OpEx spend, but unlike most, their spending is 47.5% to 49.3% in COGS. Almost as much SG&A as COGS. That's an incredibly inefficient organization, and it shows.

{kind=link}

Much of this is temporary to be sure, and likely to change as the company restructures and gets things more under control. The company's troubles are not unique - inflation, increased costs overall unrelated to inflation, exit from Russia. Also, a lot of restructuring going on.

Add to this that H&M's majority shareholder, who already owns 78.1% of votes and 54.9% of capital, seems to be ready to take the company private. Since 2023 beginning alone and through Ramsbury Invest, the major shareholder has bought around 22.4M shares in H&M for almost 3B SEK. There are many theories as to when exactly this is to happen, but most calculations point to somewhere in the next 3-6 years, if this pace of share purchasing continues, and unless something major happens. (Source: Dagens Industri )

Hennes & Mauritz is not a pleasant read if we want to look at profitability. Let's take a gander at some of the fundamentals we could be looking at to start seeing serious issues.

First off, ROIC net of WACC. Since 2011, when the company was massively profitable with an ROIC of over 50% and a WACC of less than 4%, we're now down to an ROIC of less than 3%, and a WACC of 6%, meaning a negative 3% ROIC-WACC. It's been a steady decline for over a decade.

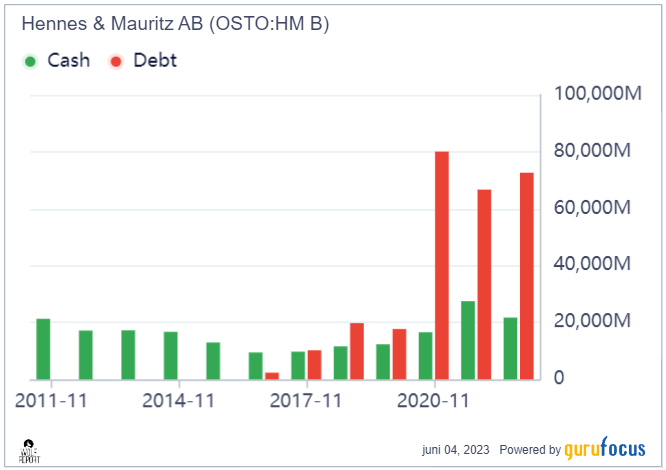

Cash/debt? Take a look.

{kind=link}

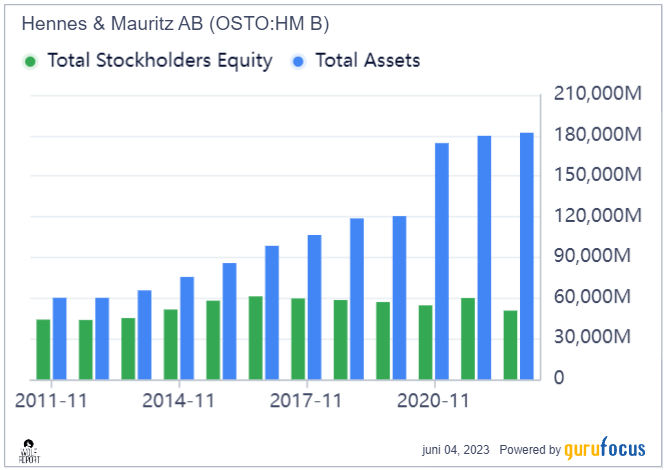

How about something like Shareholder equity related to total assets? In a good company, it should remain stable, or at least a growing percentage of SE in relation to TA. In this company, it's a never-ending negative development for 10 years.

{kind=link}

This is the equivalent of a car that might look shiny and polished, but when you pop the hood and checks things out, you find a hole in the exhaust the size of your thumb. The car may run, but exhaust leaks are dangerous. Investors in H&M are angry/worried about the dividend not reaching its storied historical levels. They should be far more worried about other things than that dividend.

I don't need to tell you that the company has managed relatively growing amounts of revenue, but the share of that's been actual net profit, has been declining for a decade as well. When the issue is this systemic, it shows up across the entire fundamental board of a company. It's the equivalent of every light flashing red on a dashboard.

Does this mean that this company is uninvestable, unbuyable, and should be ignored entirely?

Yes and No. I don't believe Hennes & Mauritz should be bought until they can prove that they can fundamentally turn around their business, and I don't see that happening in the next 1-2 years. A simple good year won't convince me of anything.

However, at the same time, I don't believe a company that's run by a multi-billionaire shareholder family with a global presence and a brand loved by many consumers, is worthless. My choice has been to sell short-dated, conservative cash-secured Puts, at no more than 5% of my total available buying power. It's been an easy way to make 10-20% off the volatility in the stock, as long as I've taken advantage of those drops properly. I have not come close to getting assigned, and even if I was assigned at the prices I was selling strikes at, I would not be that bothered by it, because the company is likely to go up and down on a forward basis, enabling me to rotate again if needed.

The company doesn't provide much analyst/investor clarity unless you dig deeper in the earnings calls. What we want to look at is the gross/general margin pressure, and when this trend abates. While the trend has been showing promising signs in 1Q23, they also said clearly that they do not give quarter-to-quarter guidance, but only say themselves "confident" that there is going to be a recovery this year. How big a recovery, and where the results will be, that's a different thing though, and no guidance there.

Sales results in 1Q23 were actually not that good, despite what the company would like to say. In March of 2023, trading was up 4%. This was despite a cold month, which really should have seen better results despite the coming spring collection. This sort of answer we see below was the standardized answer to anything having to do with what the company is confident in projecting.

And of course, we don't give that kind of a prognosis for the quarter. But it's very clear to us that sales is stronger where spring has arrived. So for example, regions such as southern parts of Europe, so spring collections are well received.

(Source: Hennes & Mauritz Earnings Call, Helena Helmersson)

Beyond saying that the company is directionally pleased with results, there really wasn't a big takeaway that would cause me to say with confidence one thing or another here.

Let's move on to valuation, a difficult prospect.

Hennes & Mauritz Valuation - Difficult and not that great

How do you value a company that's seen a decade's worth of declines? It's not easy. Recovery is given for this year, but that's recovery from results below 4 SEK, which is lower than the company, ex-COVID, has been since 2003.

Even if the company were to 100% this year in EPS, that wouldn't put it close to historical figures - and 100% is a pipe dream. Current S&P global forecasts and FactSet analyst figures are 60%. I'm estimating 40-45%, as I don't see the reversal coming as clearly as they do - especially with China and Russia.

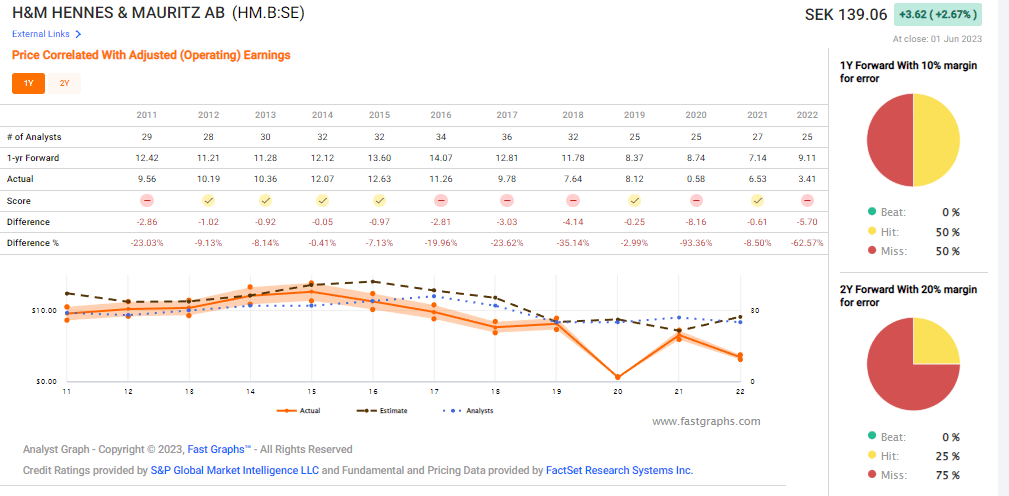

I also refer you to the complete failure on the part of analysts to forecast this business.

{kind=link}

What I, as an analyst, see here is a failure to "do the work" and perhaps listening too much to positive company expectations - because naturally, H&M has said for years that they're turning things around - only they haven't, not really.

So 40-45% is, as I see it, actually granting the company some leeway.

What else? Street targets from analysts are characteristically exuberant, to give you an idea of where these people see the company. 24 analysts follow it, and give it a PT range of 97 SEK to 185 SEK with an average of 143 SEK, making it a "BUY" here. Of course, those are the same analysts that around a year ago called the company to be worth 200 SEK. If you had invested then, you'd have lost almost 40% of your invested capital. 5 of the analysts are at "BUY" - 6 are at "SELL" or "outperform." This should give you an idea of the split down the middle here.

I come down on the other side of the fence, the more negative one. I don't believe H&M will easily turn this around, and I would look for fundamental signs of a turnaround before even considering entering money into the common share here. Any argument that a buy-out could cause the share price to jump should be muted by the fact that any buy-out would likely come at a bottom, sending the share price up to levels we view as low today, such as 95-100 SEK. The owners have a long time to wait if need be - they already have a vote and majority ownership of the company, and speculating on that is risky.

Based on everything presented here, I view the thesis and the high-level case to be made for Hennes & Mauritz as problematic, and my current thesis reflects this.

Thesis

- I view Hennes & Mauritz as a problematic business to invest in. The company has seen a decade's worth of declines, and any fundamental sign of a turnaround isn't really currently in the books. While the company is cheap to normalize long-term results, I remain ever-cautious about a company such as this and give it a conservative PT.

- I work with cash-secured Puts to make some extra cash on the side, typically annualizing 10-20% on a 30-45 day put with a conservative strike.

- For the common, I say that this company is a definite "HOLD".

- I give H&M a PT of 105 SEK/share, but that's as high as I'll go here.

Remember, I'm all about : 1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company is at 2/5 out of my criteria, and so is a "HOLD" here with a PT of 105 SEK/share for the native.

For further details see:

H & M: Difficult To Evaluate The Future, I Say 'Hold'