HMRZF - H & M: Let Down By Market Multiples

2023-10-23 01:26:26 ET

Summary

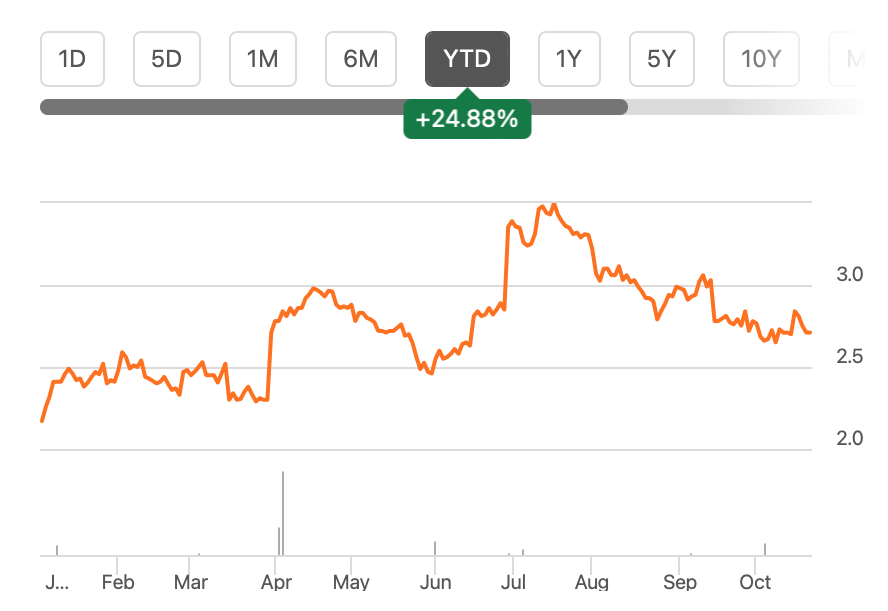

- H & M's stock price has risen by 15.7% since March and 25% YTD, outperforming the S&P Consumer Discretionary Index.

- The company has seen a significant improvement in profits, with a rise in reported earnings by over 1.5x in the first nine months of 2023, which indicates the potential for dividend growth.

- However, its TTM and forward P/E aren't convincing enough to make it an outright buy right now.

Since the last time I wrote about the Swedish fashion brand H & M Hennes & Mauritz AB ([[HNNMY]], [[HMRZF]]) in March this year, its price has risen by 15.7%. Year-to-date [YTD], HNNMY has risen by almost 25%, exceeding the rise in the S&P Consumer Discretionary Index, which is up by 19%. This is significant since it was lagging behind the index seven months ago.

{kind=link}

Here I take a closer look at the H & M story to assess what's behind the accelerated rise. This is especially so in the context of its trailing twelve months [TTM] dividend yield, which has declined from 5.4% when I last checked, to 4.5% now.

The progress so far

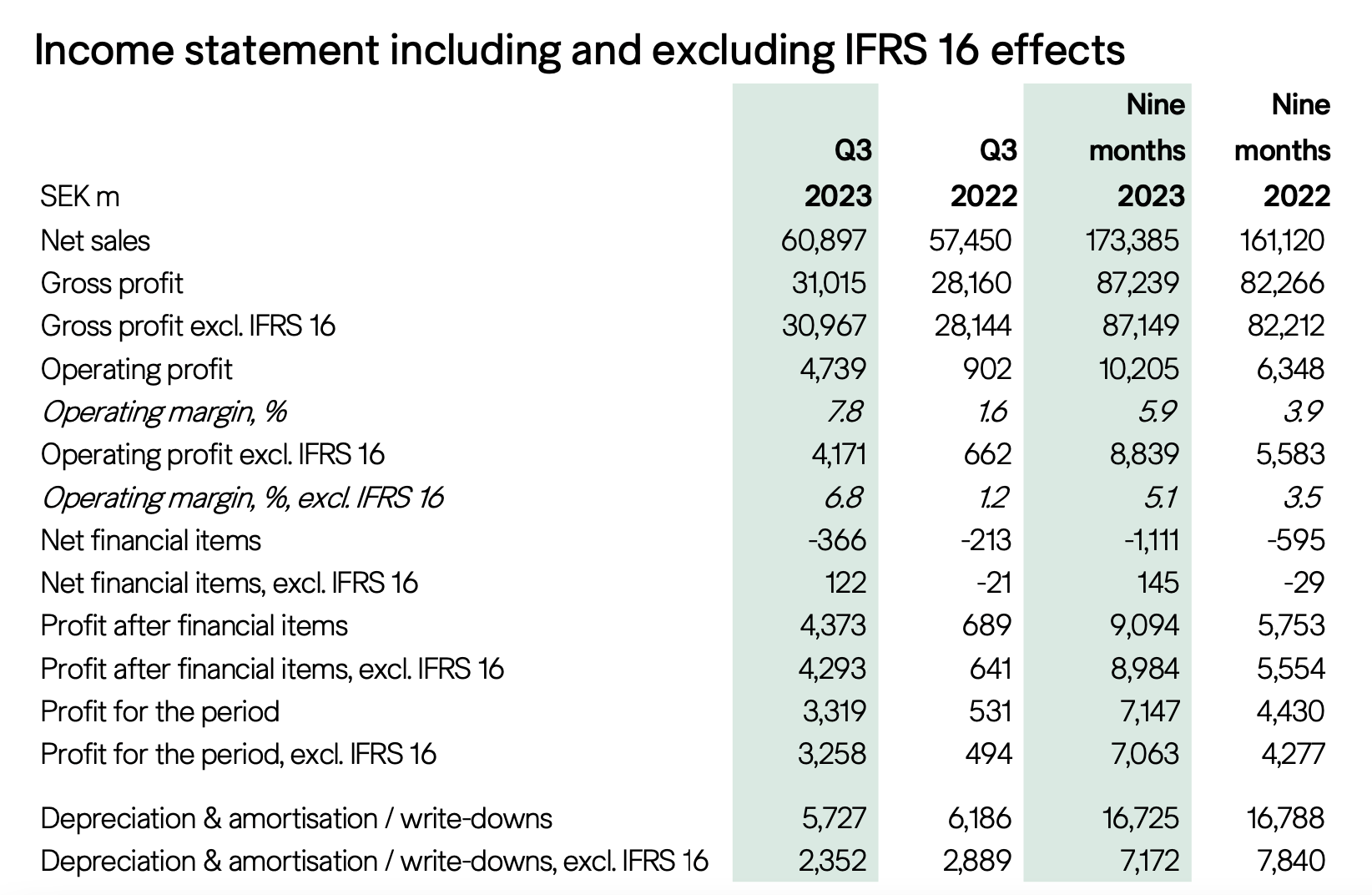

The latest data available for H & M in March was its first quarter trading update (Q1 2023, December 1, 2022- February 28, 2023) for the financial year 2023 (2023, ending November 30, 2023). It wasn't bad, with net sales up by 12% year-on-year [YoY], consistent with those for the full year 2022.

Since this was a trading update, profit figures weren't available. But I wanted to look out for them in subsequent releases since it reported a loss reported in Q4 2022. And it did swing back into profits (see table below), with a rise in reported earnings by over 1.5x in the first nine months of 2023 (9M 2023). This was the result of a cooling off in cost growth, even as revenue growth softened to 8%.

{kind=link}

The reported operating margin was also improved, coming in at 5.9% (9M 2022: 3.9%, 2022: 3.2%). While this is still a far cry from its target of a double-digit operating margin in 2024, the first signs that it can be achieved are here. In Q3 2023, the margin came in at 7.8%, vastly improved from the 1.6% in Q3 2022.

The key takeaway here is that there's some softening in sales for H & M, which isn't surprising. There's a slowing down in the consumer economy in its big market of Western Europe accounting for over 30% of its revenues. This shows up even more clearly in the Q3 net sales growth of 6%. But there's still hope of a bounce back as the period leading up to its financial year end will see the rise of festive shopping. Further, it's encouraging to see the massive jump in profits.

The outlook

Assuming that the company’s revenue continues to grow at the same 8% rate in Q4 2023, as seen in 9M 2023, its year-end revenue will be at around USD 22 billion. The company's reporting currency is SEK, but I've made the conversion here, to give a better perspective on H & M's US listing.

Further, if its reported net profit margin remains unchanged at 4.1%, the net profit will amount to USD 906 million for the full financial year. This is over 2.5x the profit clocked in 2022.

As massive as the rise sounds, it’s plausible considering that the company was dragged back by high costs last year and even reported a loss in Q4 2022, as mentioned earlier.

Moreover, for the trailing twelve months [TTM], which covers 9M 2023 and the loss-making Q4 2022, H & M has already exceeded last year’s profit of USD 340 million by 70%.

What the outlook means for dividends

Existing positive trends for the company’s profits and even better year-end projections indicate that dividends are very likely to increase. Its policy is that “the ordinary dividend over time is to exceed 50 percent of profit after tax”.

In actual fact, it’s actually much higher, with the dividend payout ratio at 300% as of 2022. This is clearly unsustainable. But even if it were to maintain its dividends in line with its stated policy of a 50% payout, the dividend for next year can come in at USD 0.28 per share. This is over double the present level.

{kind=link}

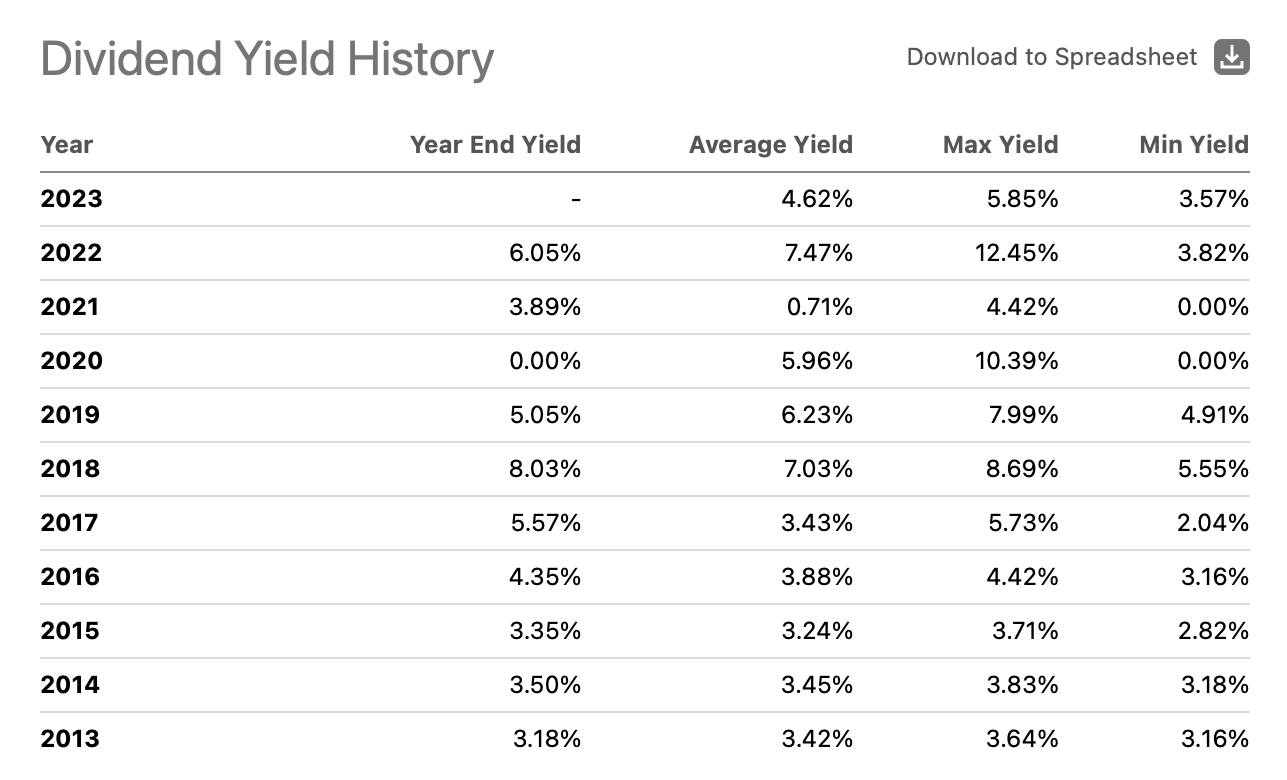

The forward dividend yield comes to 10.2%, which is far higher than the present levels. If this were to happen, it would be the highest yield in the past decade (see table above). But even if the extent of profits was lower and the dividend didn't increase as much, this exercise only demonstrates that there's a very good likelihood of a dividend rise.

Incidentally, with no dividend announcement since I last checked, even the drop in the TTM dividend yield is only due to the price rise for H & M.

The market multiples

The market multiples, however, are a mixed bag. The TTM price-to-earnings (P/E) ratio has improved significantly to 39.8x now, from the 57.3x it was at the last I checked.

The ratio is still much higher than that for consumer discretionary stocks at 15x and its own median P/E for the past decade at 23.9x . However, considering that the past twelve months still capture the loss in Q4 2022, it looks higher than it would have otherwise.

For this reason, let's also look at the forward P/E. H & M looks much better at 24.6x than its past five years’ average of 49x . However, compared with peers like Zara owner Industria de Diseño Textil (IDEXY), with a forward P/E of 19.5x it still looks highly priced. And that’s after IDEXY has seen a much bigger 32% share price rise YTD. Its dividend yield at 3.2% isn’t much farther behind H & M either.

What next?

The market multiples leave the picture muddled for H & M right now. While there are sure signs of rising competitiveness, it’s still not a convincing enough buy based on them.

This is a pity really, considering the company’s performance for 9M 2023, with sustained revenue growth and a significant improvement in its profits. Its operating margin also looks like it's on the path to the 2024 target of 10%.

The big positive for H & M though is the potentially substantial dividend increase it can offer for next year. But it might not be enough to make up for potential price correction, as past trends show.

Still, if the company continues to make better-than-expected profits for another quarter, it can look more attractive going forward even from its market multiples' perspective. But that’s a wait-and-watch. I’m retaining a Hold rating on H & M.

For further details see:

H & M: Let Down By Market Multiples