HRUFF - H&R REIT: Buy On The Dip

Summary

- I maintain my bullish outlook since my previous article.

- The stock trades at a 50% discount to NAV and has a 5% dividend yield.

- Management has done all the right things to position the REIT to increase NAV going forward.

All figures in CAD unless otherwise noted.

You may recall that I wrote on this Canadian REIT H&R Real Estate Investment Trust ( HRUFF ) which trades under the ticker HR.UN on the TSX in April 2022 with the following conclusion:

I believe H&R is as good an investment as any to take advantage of the inflationary environment as they should be able to redeploy funds from the Bow and Primaris sales into assets that can take advantage of more favourable lease rates and even if it takes 5 years for the market price of ~$13/share to reach its NAV of ~$18/share (and assuming NAV stays constant) that would equate to capital gains of at least 7% annually in addition to the 5% dividend. I believe that this REIT is well positioned for double digit returns that can easily keep pace and even beat inflation.

Unfortunately since then interest rates have risen and talks of a recession have escalated. Many REITs have seen at least a small loss in value ever since and H&R has been no exception being down ~20% since last writing.

Fear not as the REIT is an even more attractive buy at $11.30/share as of this writing and is showing even more promising results and therefore trades at one of its largest discounts to NAV in its history.

Net Asset Value

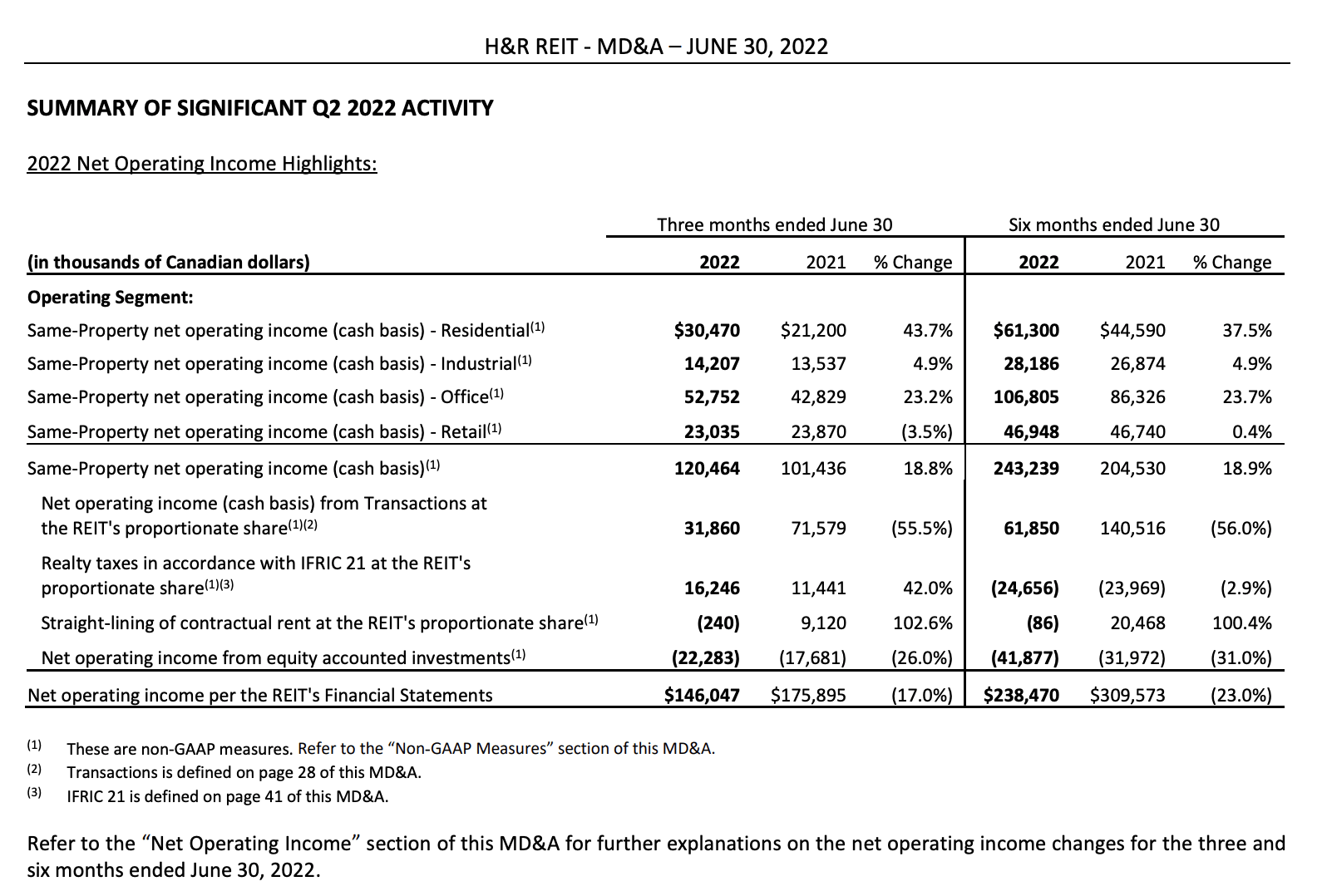

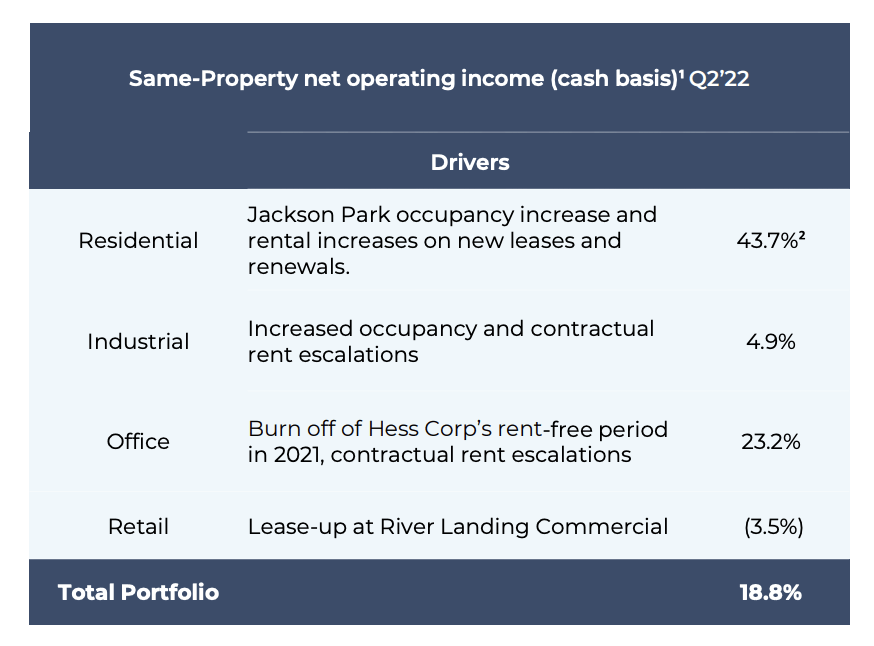

In the previous article I may not have had sufficient data to assess the potential of this repositioned portfolio as you may recall 2021 was a year of heightened activity on that front with the sale of the Bow Office in Calgary, the Bell Office Campus in Mississauga, ON and the Primaris spin-off. We now have two full quarters since all these activities took place and Q2-2022 results have not disappointed with same-property NOI up across the board on a QoQ and YoY basis in all property types except retail which showed some stagnation.

{kind=link}

Same?Property net operating income from residential properties increased by 43.7% YoY which was the segment with the largest YoY increase primarily due to an increase in occupancy at Jackson Park in New York. Excluding Jackson Park, Same?Property net operating income (cash basis) from residential properties increased by 24.8% YoY. Same?Property net operating income from office properties increased by 23.2% YoY primarily due to the 2021 free rent period granted to Hess Corporation ( HES ) as part of the extension of its lease, but the segment would have seen meager growth in its absence. Same?Property net operating income from industrial properties increased by 4.9% for both the three and six months ended June 30, 2022 compared to the respective 2021 periods, primarily due to an increase in occupancy and contractual rental escalations.

The River Landing Commercial in Miami, FL was negatively impacted due to the following higher non?recoverable operating expenses including property taxes and insurance as a result of vacant units, the occupancy of which is expected to commence in Q4 2022, as well as several retail units which have been leased but were not occupied as of June 30, 2022.

{kind=link}

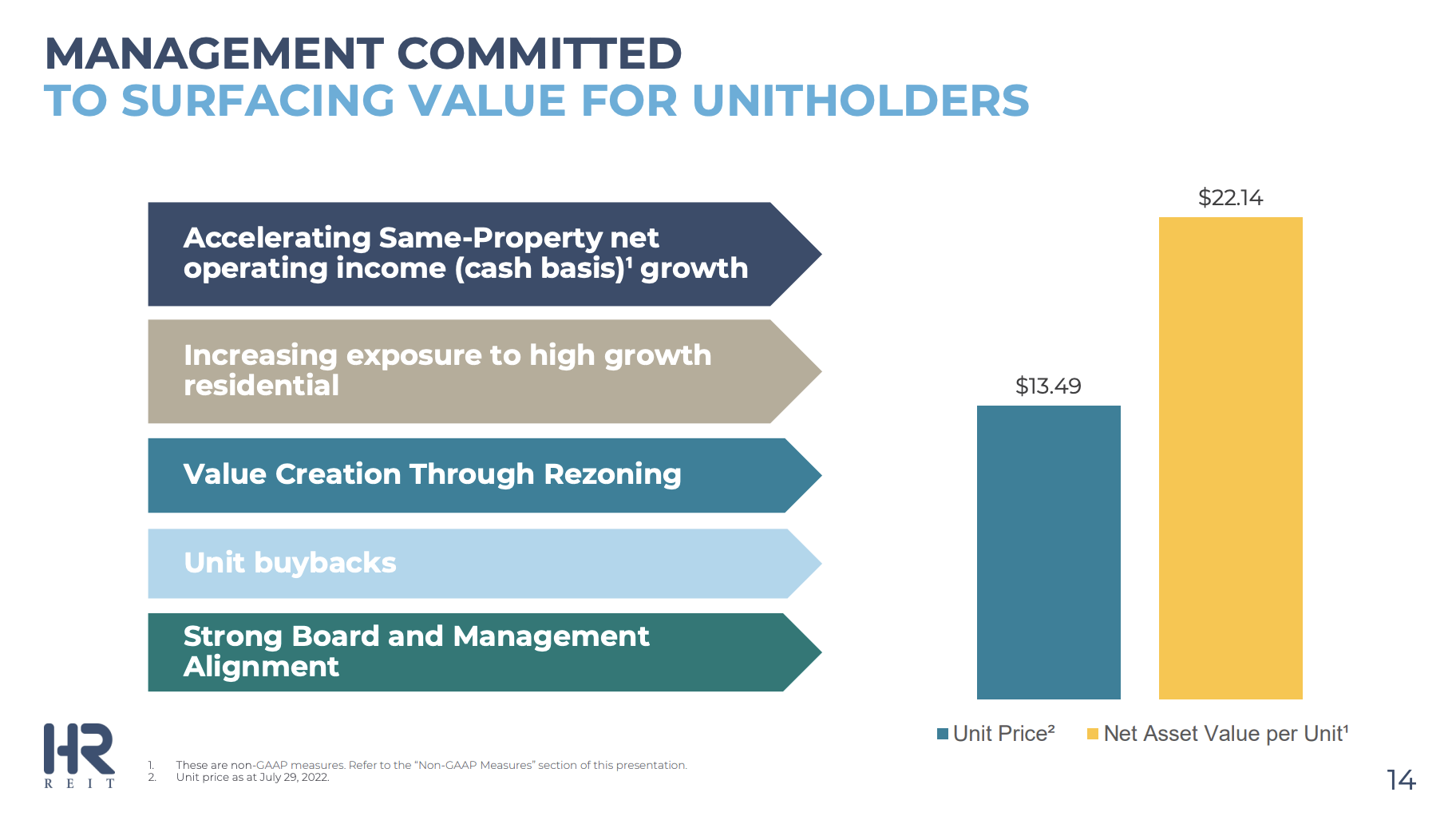

As a result of the increased portfolio strength management has since reported a 22% increase in its portfolio NAV since Q1-2022 to ~$22/share which would imply the units trade at a 49% discount to NAV.

{kind=link}

It may seem almost too good to be true to spend $1 for $2 worth of real estate but there are reasons to believe this NAV is justified as management made the following dispositions in Q2-2022.

- In June 2022, H&R sold a 312 residential rental unit property in San Antonio, TX for U.S. $69.3 Million at a capitalization rate of 3.6%. H&R acquired this property in November 2016 for U.S. $56.8 Million.

- In June 2022, H&R sold seven automotive?tenanted retail properties in the United States totaling 94,205 square feet for approximately U.S. $58.1 Million at a weighted average capitalization rate of 5.2% which is 119 bps below their weighted average capitalization rate for their retail portfolio.

- In July 2022, the REIT entered into an agreement to sell 100 Wynford Drive, an office property in Toronto, ON including 100% of the future income stream derived from the Bell lease (“Bell lease”) until the end of the lease term in April 2036 to an arm’s length third party, for approximately $120.7 Million which approximates the June 30, 2022 IFRS values.

For the last one mentioned, H&R will legally sell the property, the transaction will not meet the criteria of a transfer of control under IFRS 15 as H&R will have an option to repurchase 100% of the property for approximately $159.5 Million in 2036 or earlier under certain circumstances. In essence H&R will retain a call option on the sale which they can take advantage of if inflation persists.

H&R has recognized a $35 Million gain on sale of assets through the first six month which not only increases BV but also validates the management's estimate for the higher NAV. This large gain on sale figure was certainly helped by the strong US dollar relative to the CAD which is the REITs reporting currency. If that isn't enough to convince the markets that the shares are undervalued the REIT repurchased 10,516,100 Units during Q2-2022 at a weighted average price of $13.01 per Unit, for a total cost of $136.8 Million bring total share purchases for the year to 22,125,300 Units.

In addition I foresee improved NOI growth over the next 12 months as a result of the following developments:

- The REIT currently has two Canadian properties under development at its industrial business park in Caledon, ON which are expected to be completed in Q3 2022. H&R has fully leased both of these properties: 34 Speirs Giffen Ave., totalling 105,014 square feet to Lindstrom Fastener (Canada) Ltd. for a term of 10 years expected to commence in October 2022, and 140 Speirs Giffen Ave, totalling 77,754 square feet to Coast Holding Limited Partnership for a term of 10 years expected to commence in October 2022. Both properties have annual contractual rental escalations.

- H&R has a 31.2% non?managing ownership interest in Shoreline in Long Beach, CA. In June 2022, the project reached substantial completion and was transferred from properties under development to investment properties within equity accounted investments. As at June 30, 2022, occupancy was 50.2% and committed occupancy was 61.9%.

- H&R has a 31.7% non?managing ownership interest in The Grand at Bayfront in Hercules, CA. In June 2022, the project reached substantial completion and was transferred from properties under development to investment properties. As at June 30, 2022, occupancy was 44.4% and committed occupancy was 54.3%.

- In Q2 2022, H&R completed a 5?year lease renewal at 2300 Rue Senkus in Montreal, QC, an industrial property totalling 371,000 square feet, at H&R’s ownership interest. The original lease was set to expire in December 2022 and rent will increase by 125% commencing in January 2023 with annual contractual rent escalations.

- H&R has leased approximately 76.7% of the office space at River Landing Commercial in Miami, FL to two major tenants which include Miami?Dade County for the Office of the State Attorney whose lease is expected to commence in Q4 2022 and Public Health Trust of Miami?Dade County, whose lease is expected to commence in Q1 2023.

Risks

There are always risks to consider when a stock trades at such a low valuation so as to not get caught in a "value trap" which we will discuss.

Leverage

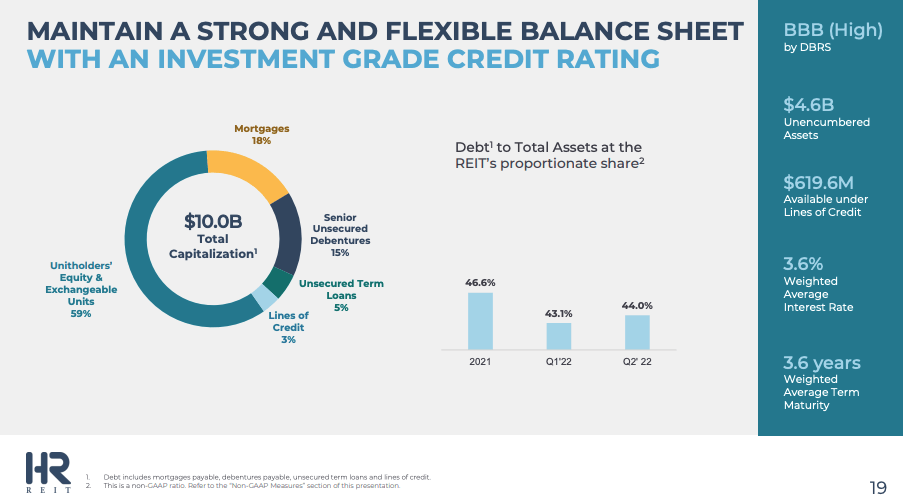

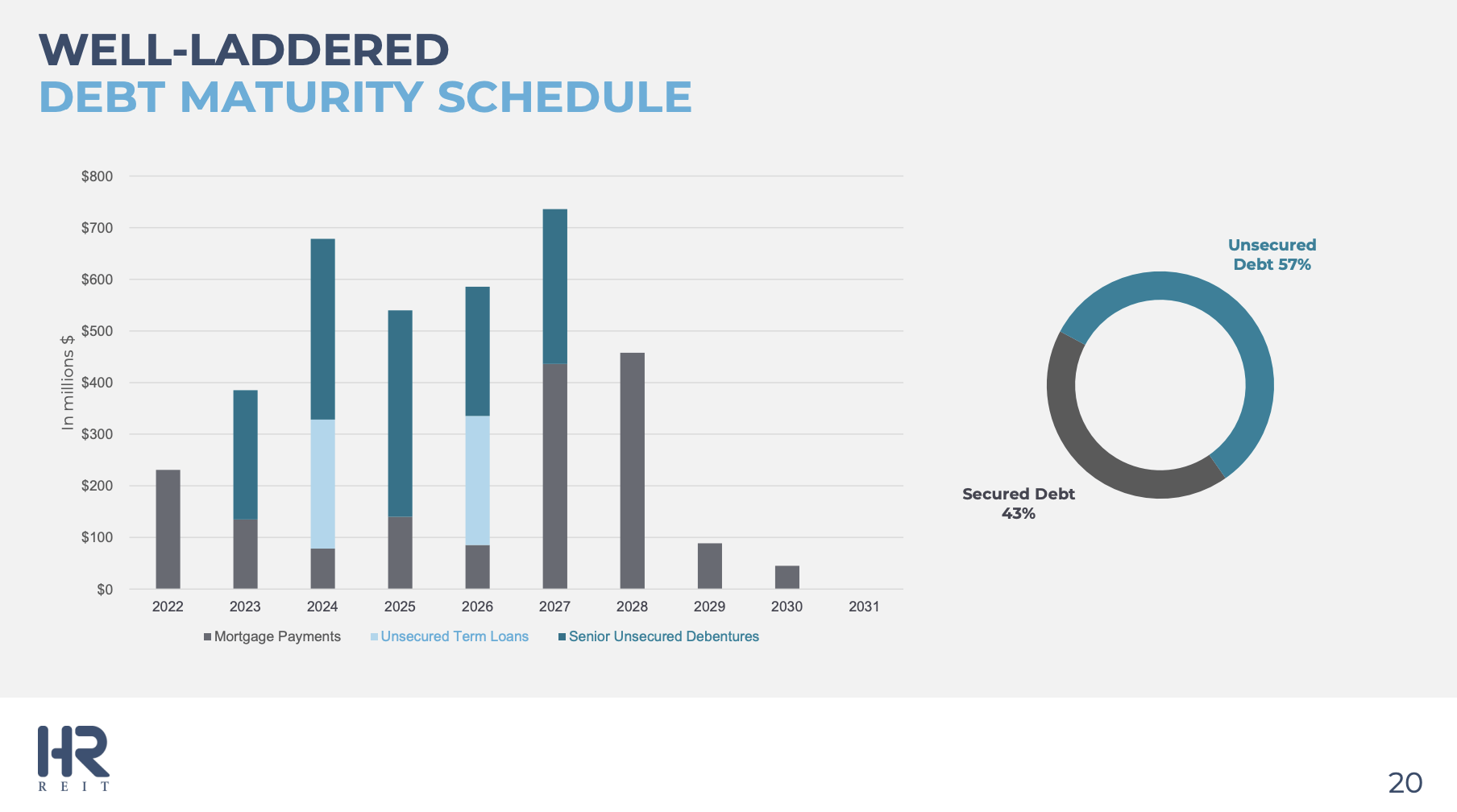

Annualizing 6-month FFO at $167 Million would imply ~12x net debt/FFO. This is not exactly low but relative to other Canadian REITs in the residential/industrial space this isn't high either. In addition the analyst community expects a decline in leverage as a result of rent escalations from lease renewals and as leasing activity increases at Caledon, Shoreline, The Grand at Bayfront for 2022 FYE. In addition 57% of debt is unsecured and there is $4.6 Billion in unencumbered assets.

Unfortunately this level of leverage could prove to be punishing if the Fed continues its hawkish pace at raising rates. The weighted average term to maturity is only 3.6 years at a meager weighted average interest rate of 3.6%, while 5-year fixed rate mortgages have been going for as high as 7% in Canada. 21% of mortgage debt is due before the end of 2023 which will have to be financed into higher rates where interest expense could almost double. On the bright side the $750 Million OLOC which is the only OLOC with any meaningful balance is not up for renewal until 2026.

{kind=link}

{kind=link}

H&R has proven that they can increase lease rates on an annual basis to offset the impacts of inflation and have confidence they will do so in the future.

Office Space

Anyone who knows anything about this REIT knows that they have been repositioning the portfolio away from office buildings. In part because of workers choosing to spend more time working from home which does not require companies to lease so much office space, but also because the market does not tend to favor too much diversification among one REIT.

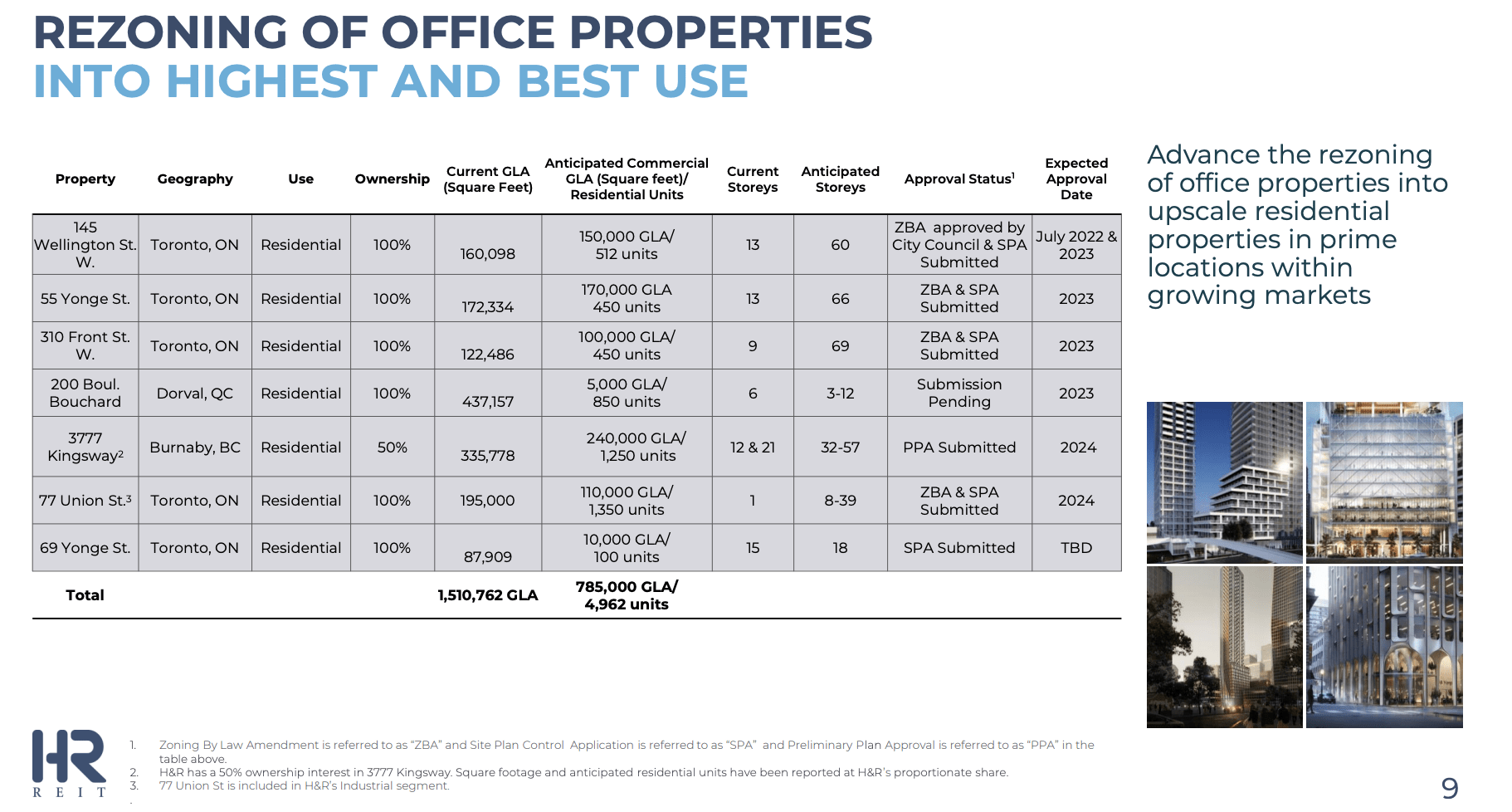

As noted throughout this article H&R has gotten rid of spaces above their recorded book value, but cannot be expected to do so for all properties, only the more high quality properties. That is why 26% of office properties are held for rezoning.

Unfortunately it can take years to obtain rezoning approvals to redevelop office space to residential. In July 2022, the City of Toronto adopted the final report recommending approval of the rezoning application for 145 Wellington St. W., which provides for the re-development of the current 13 story office property into a 60-story mixed-use property consisting of 512 residential units, 149,000 square feet of office space and 1,000 square feet of retail space. Aside from that there are no rezoning approvals expected until at least 2023 so may take at least a couple years before we see these properties get redeveloped.

{kind=link}

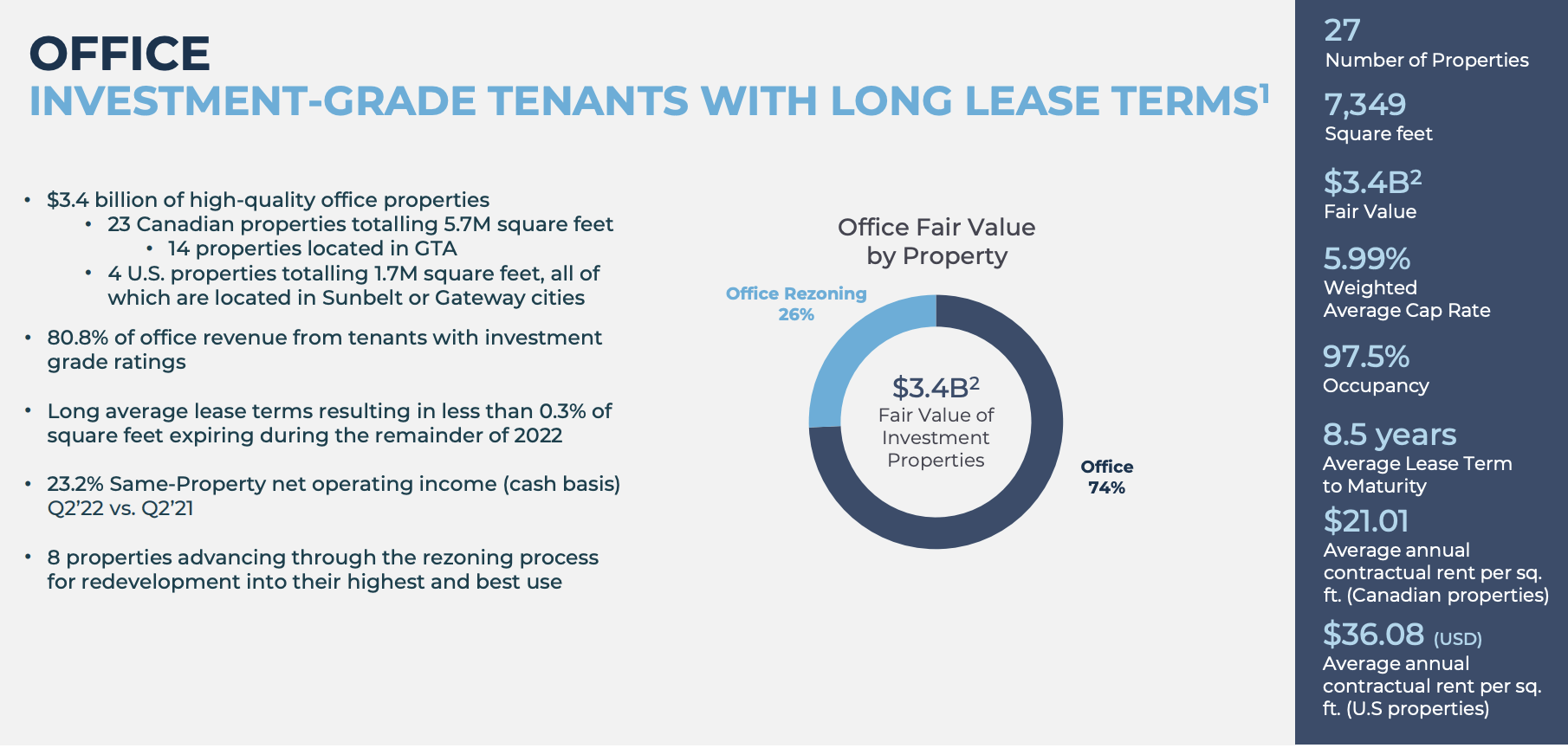

H&R will have to make due with their office portfolio in the near term. That being said it is far from the worst portfolio in the REIT space with 98% occupancy, a weighted average lease term to maturity of ~8.5 years, and 81% of tenants are investment grade like Hess Corporation ( HES ), New York City Department of Health, Bell Canada ( BCE ), and TC Energy Corporation ( TRP ).

{kind=link}

Conclusion

This is one of my favorite REITs with management interests fully aligned with shareholders by taking advantage of opportunities to increase book value by selling assets at accretive valuations and repurchasing shares at low valuations. This is a low risk play to realize double digit returns as I maintain my $18/share price target and investors can enjoy the 5% dividend yield while waiting. The dividend is well covered as the FFO payout ratio has been between 45-55% annually.

For further details see:

H&R REIT: Buy On The Dip