HRUFF - H&R REIT: Possibly The Only Office Bet You Should Consider

2023-05-15 09:00:00 ET

Summary

- We moved to the sidelines on our last update on H&R REIT.

- The timing was good and the REIT succumbed to broader sector pressures.

- We look at the Q1-2023 results and update our view.

Market performance have a big dose of luck and sometimes that really helps you out. We moved to the sidelines on our last update on H&R REIT ( HRUFF ) ( HR.UN:CA ). We literally told you that even in the title. It would be lie if we told you that we expected such a drop.

Seeking Alpha

No. We just expected the risk-reward to be awful and here that worked in our favor. We look at the Q1-2023 results and tell you why things are looking a little better in some ways for this REIT.

The Drama Before The results

H&R was in the news just before the results.

H&R Real Estate Investment Trust’s units sank on Thursday morning after the REIT parted ways with its president, who also ran its U.S. residential division, in a surprise move with little explanation.

Philippe Lapointe, a Canadian based in Texas, joined H&R a decade ago and rose through the ranks of the REIT’s U.S. multi-family division, known as Lantower Residential. Lantower is one of H&R’s bright spots amid a tough market for commercial real estate and in May, 2022, Mr. Lapointe was promoted to president of the entire REIT.

One year later, Mr. Lapointe is gone, effective immediately, and Lantower’s chief operating officer Emily Watson is taking over his responsibilities in the United States. A new president for the entire REIT has not been named. H&R’s units dropped 7 per cent on the Toronto Stock Exchange by late morning Thursday.

Source: Globe & Mail

Lantower has been the backbone of H&R's strategy and has actually outperformed most expectations over the last two years. Philippe Lapointe guided this performance and his departure has scared the bulls. We did see some downgrades on the back of this news, even before the results were released . Our take is that H&R has a deep bench and while the key person departure tends to spook stocks, we don't think the impact will be substantial.

Q1-2023

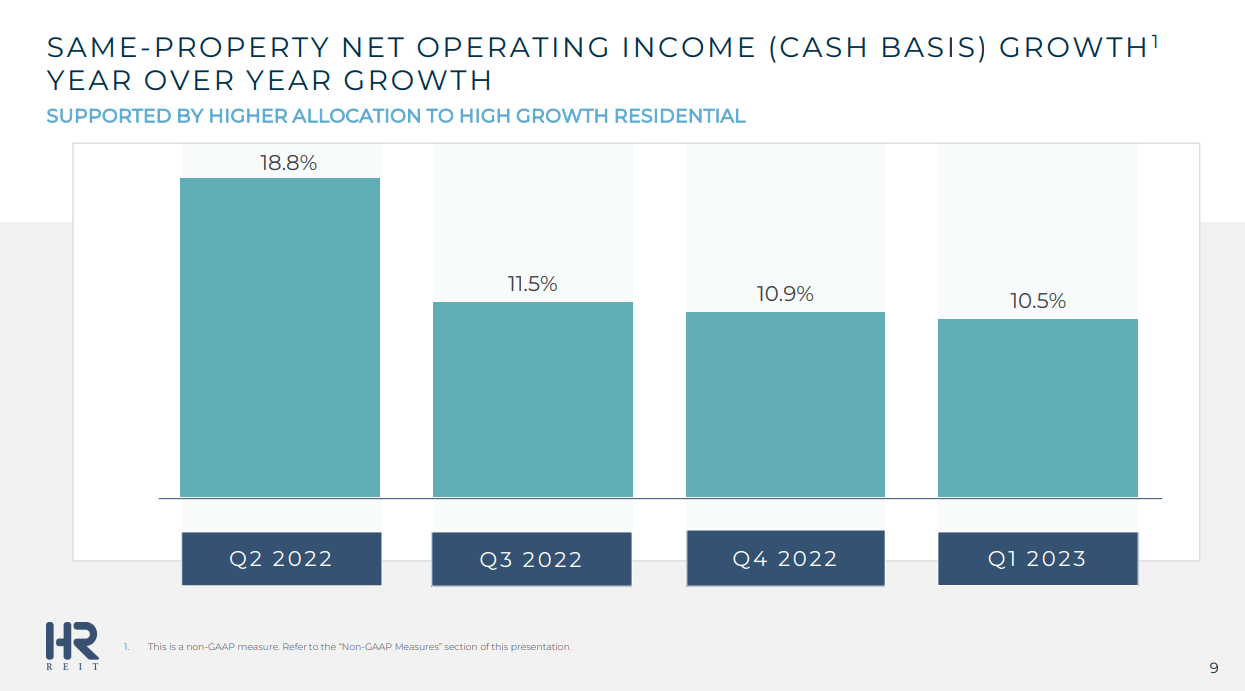

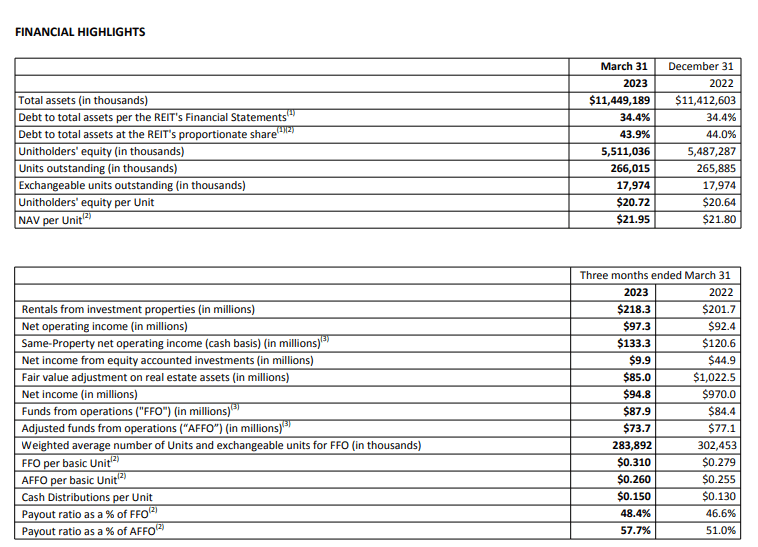

With that news out just before the Q1-2023 results, H&R moved the timing of its conference call. The actual results were released during the market hours on May 12, 2023 and were quite impressive. All segments showed another quarter of extremely strong same property net operating income (NOI) growth. 10.5% year over year is impressive and especially as it comes on the back of multiple quarters of double digit growth.

{kind=link}

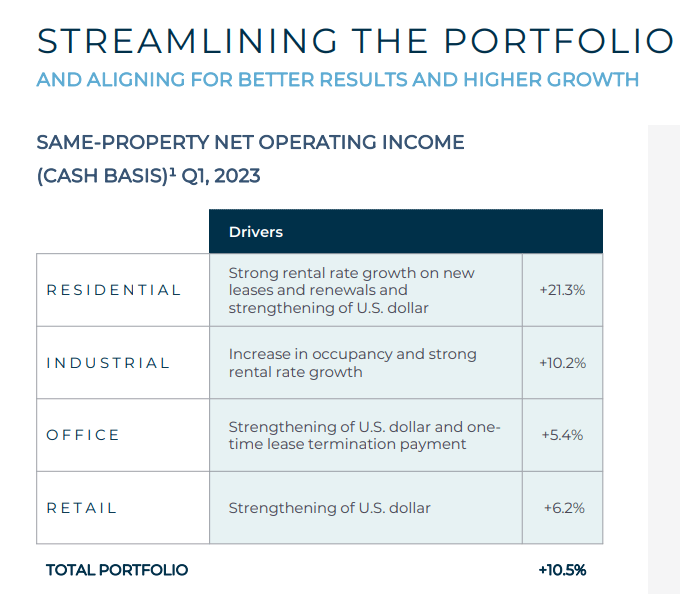

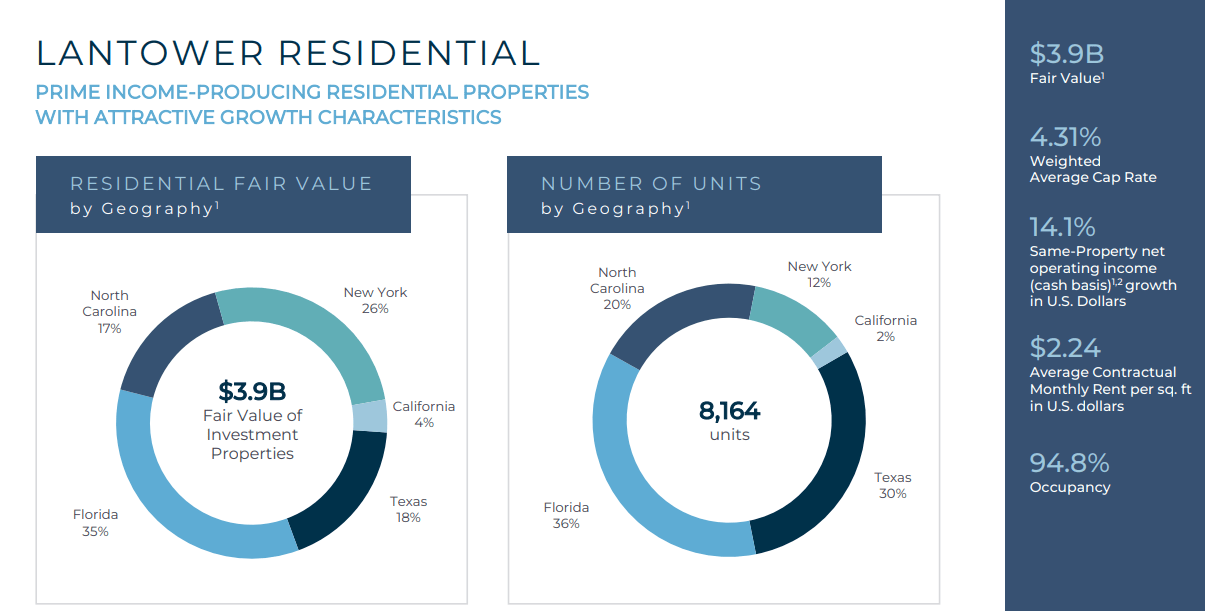

Residential was the star here with a 21.3% increase. Lantower was not fully leased last year, so this was expected to a large extent.

{kind=link}

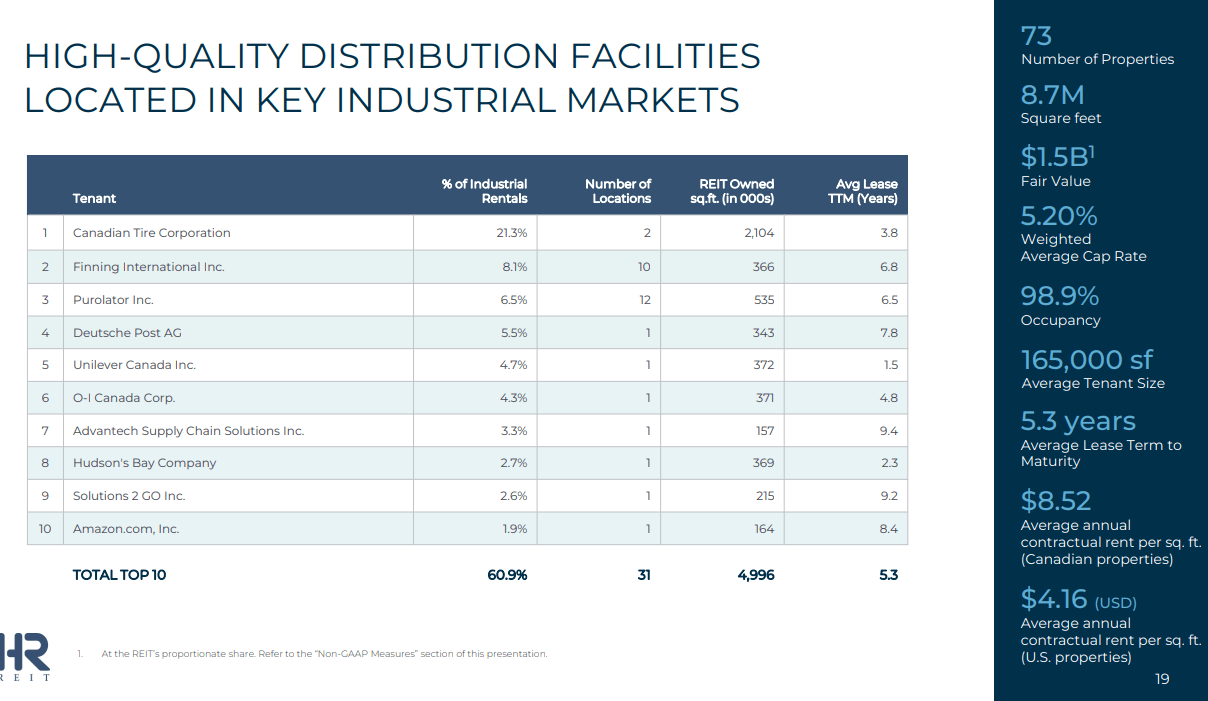

Industrial was pretty strong as well and these are the only two segments that H&R wants to be exposed to by the end of 2026 (80% residential, 20% industrial). The other two segments did not manage the flourish of residential and industrial. But they were impressive in light of the environment we do have today. One point to note here is the stronger US Dollar (weaker Canadian dollar) did drive a lot of the NOI growth of these two segments.

Funds from operations (FFO) was up 11.11% year over year and the net asset value or NAV, held steady quarter over quarter.

{kind=link}

Note that H&R did not do any buybacks during the last quarter. Total units outstanding went up from December 31, 2022.

Outlook

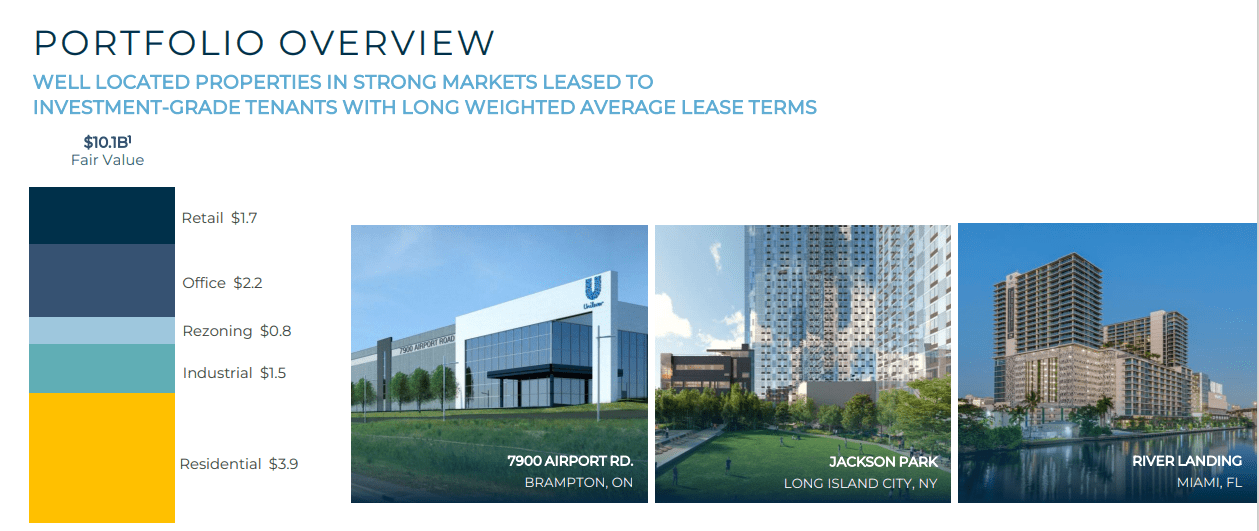

The portfolio continues to move rapidly towards residential exposure with nearly $4.0 billion coming from that segment. An additional $800 million is from the office segment that is being rezoned for residential replacement.

{kind=link}

Bears might argue that the valuations here are a tad optimistic with a 4.31% cap rate.

{kind=link}

We agree that there is room for a dislocation here and 5% cap rates might make a reappearance at some point. There is also a ton of supply coming on as absolutely everyone apparently sees this as an asset class which cannot produce bad returns.

US Census

So you have to be cautious here in running with the bulls.

On the industrial side we think the cap rates used in valuations are actually a bit high.

{kind=link}

The rents in most of these markets are jumping quite quickly as old leases rollover. Unlike in residential properties, here you can get numbers that would be impossible to fathom with apartments. H&R put out two little snippets here to show how powerful the lease rollovers were.

In Q1 2023, H&R completed a 5-year lease renewal on a 132,735 square foot industrial property in Mississauga, ON, at H&R’s ownership interest. The original lease expired in February 2023 and rent increased by 269% commencing in March 2023 with annual contractual rent escalations. The tenant had a free rent period for March and April 2023.

In Q1 2023, H&R completed a 5-year lease renewal on a 37,600 square foot industrial property in Mississauga, ON, at H&R’s ownership interest. The original lease will expire in July 2023 and rent will increase by 232% commencing in August 2023 with contractual rent escalations. The tenant has a free rent period for the months of August 2023, August 2024 and August 2025.

Source: H&R REIT Q1-2023 Press Release

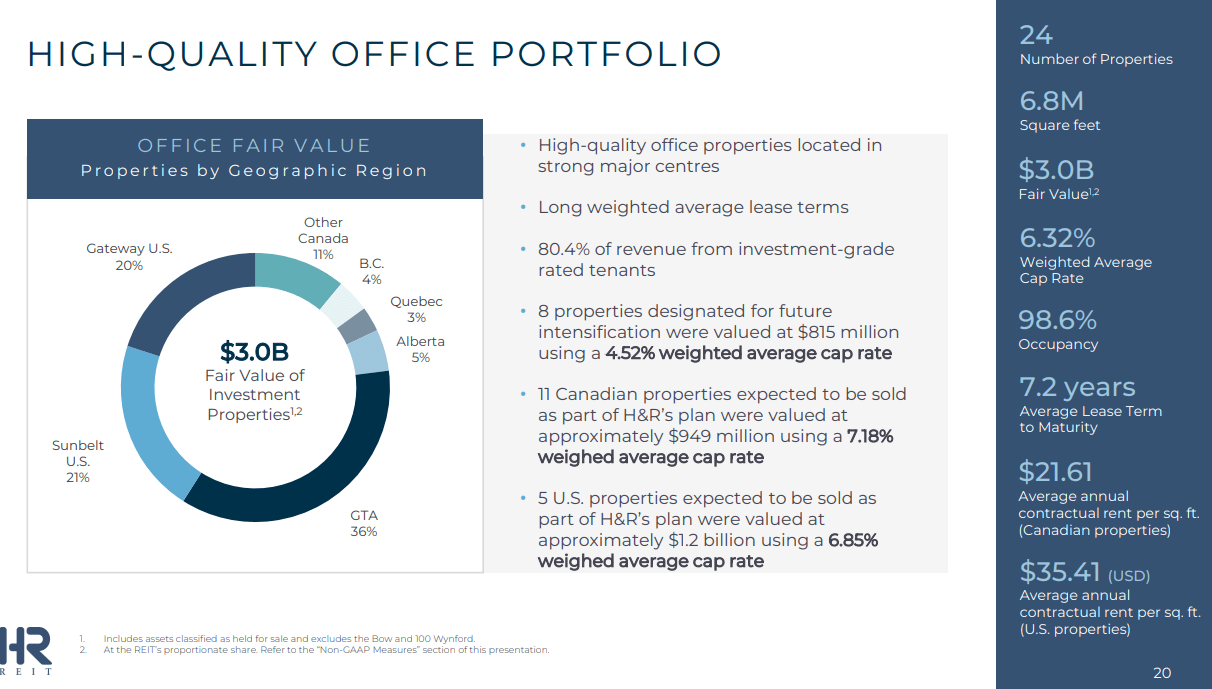

On the office side, H&R NAV already reflects the uplift from rezoning where it is using a 4.52% cap rate for those properties. The Canadian and US office cap rates for the remaining properties near 7% are a mixed bag.

{kind=link}

On one hand H&R is using higher cap rates (lower property values) than all the office focused REITs like Dream Office REIT (D.UN:CA ) and Allied Properties ( AP.UN:CA ). H&R also has far longer lease terms than either of these two. So if you have to be critical about H&R, you would go to town on the others. But from our point of view, these are still optimistic. That said, H&R sold one property at a very solid price.

In April 2023, H&R sold 160 Elgin Street, a 973,661 square foot office property in Ottawa, ON for $277.0 million, which was classified as held for sale as at March 31, 2023. H&R provided two vendor take-back mortgages to the purchaser upon closing: 1) $180.0 million secured by a first mortgage on the property, bearing interest at 6.5% per annum for 90 days, maturing July 20, 2023 and 2) $30.0 million which will be subordinate to the first mortgage on the property, bearing interest at 4.5% per annum for a five-year term, maturing April 20, 2028. The remaining proceeds of $67.0 million were primarily used to repay debt and fund closing costs. Approximately $33.0 million of the $67.0 million will be used to repurchase Units, under the REIT’s normal course issuer bid, which are currently trading at a significant discount to the REIT’s NAV per Unit.

Source: H&R REIT Q1-2023 Press Release

Verdict

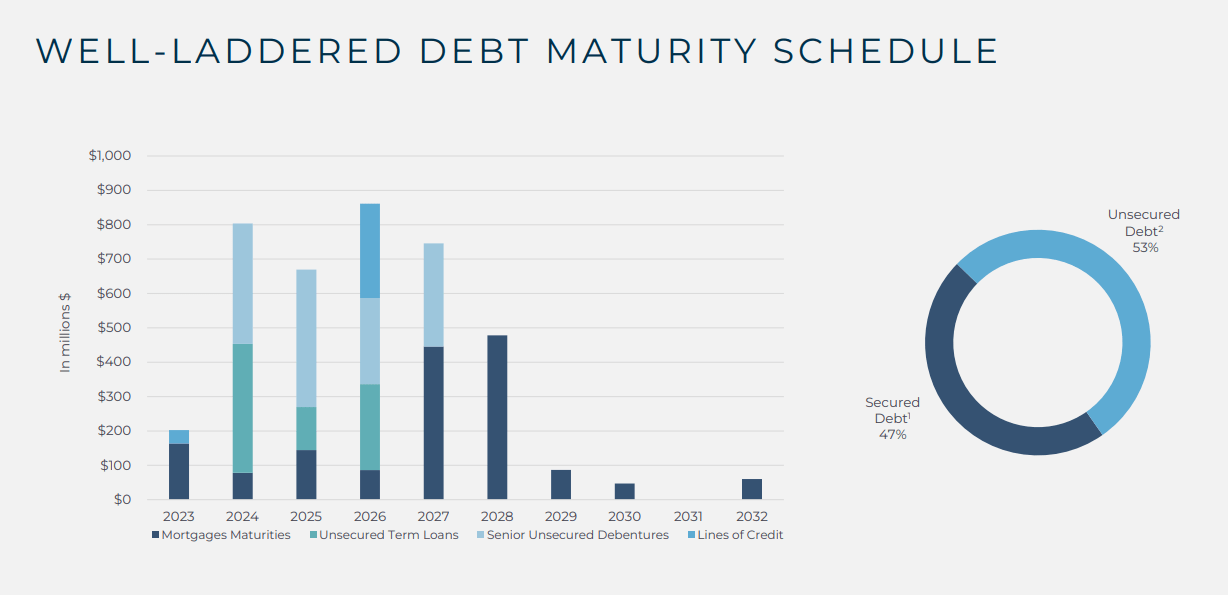

If you wanted some office exposure, even in passing, this would be the place to get it. H&R's NAV reflects practically a zero valuation for the office side with the NAV being twice the share price. So if you apply 12% cap rates on office properties and adjust for the long leases in place, we think H&R is worth at least $14 a share. The offset here is their debt maturity schedule.

{kind=link}

We are guessing the "well-laddered" here refers to the fact that about equal amounts mature between 2024 and 2027. But this is a bad maturity schedule and many Canadian REITs have gotten themselves into this mess. H&R's situation is not as bad as Artis REIT ( AX.UN:CA ) ( ARESF ) where weighted average debt maturity was slight more than 2.0 years on last check , but the 3.1 years is hardly something to be proud of. Note that the interest rate keeps rising as well.

The weighted average interest rate of H&R’s debt as at March 31, 2023 was 4.0% with an average term to maturity of 3.1 years. The weighted average interest rate of H&R’s debt as at December 31, 2022 was 3.8% with an average term to maturity of 3.2 years.

Source: H&R REIT Q1-2023 Press Release

In balance we rate it as hold/neutral, while noting that it would be very hard to get negative long term returns from this point combining the 8X FFO multiple and 50% NAV discount.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

H&R REIT: Possibly The Only Office Bet You Should Consider