UNLYF - Haleon: Leading Business In An Attractive Industry

2023-06-29 05:41:44 ET

Summary

- Haleon is one of the largest consumer healthcare businesses in the world, with leading brands in many of the key segments.

- We expect a healthy increase in demand going forward, as OTC healthcare products continue to be seen as a required part of an increasing number of consumers' lives.

- Haleon's margins are comparably strong in the market.

- Based on the valuation of its peers, we believe Haleon to be undervalued at its current share price.

Investment thesis

Our current investment thesis is that Haleon plc ( HLN ) is one of the strongest businesses in the consumer healthcare market, with leading brands and deep expertise. The industry is experiencing tailwinds across the globe, as social and economic factors contribute to increased usage. We believe the business is fundamentally attractive based on both financials and commercials. Relative to peers, the business looks undervalued, owing to good profitability.

Company description

Haleon is involved in the development, production, and sale of consumer healthcare products globally.

Its offerings encompass various categories such as oral health, pain relief, respiratory health, digestive health, vitamins, minerals, and supplements.

The company's well-known brands include Advil, Sensodyne, Panadol, Voltaren, Theraflu, Otrivin, Polident, parodontax, and Centrum.

The company is a recent spin-off from GSK ( GSK ), the global British Pharmaceutical business. GSK retains c.14% ownership of the business, with Pfizer ( PFE ) having a further c.26%.

It is one of the 2 largest consumer healthcare businesses in the World, alongside Kenvue ( KVUE ), the Johnson & Johnson ( JNJ ) spin-off.

Share price

Since listing, Haleon's share price has moved broadly in line with the market, although with a slight degree of additional weakness.

Financial analysis

Haleon Financials (Tikr Terminal)

Presented above is Haleon's financial performance since FY19.

Revenue & Commercial Factors

Haleon/GSK's former consumer healthcare business has generated impressive growth in the last few years. Covid-19 has contributed to robust demand while current economic conditions have supported pricing.

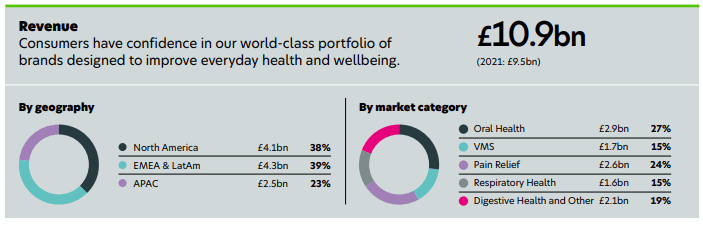

Haleon is a global leader across several healthcare verticals, with Oral Health, Pain Relief, and Digestive Health representing the company's largest revenue streams. Further, the company generates revenue fairly evenly across the globe.

{kind=link}

This high level of differentiation protects the business against any external shocks while allowing shared competencies and developed brands to deliver growth.

Business Model and OTC healthcare industry

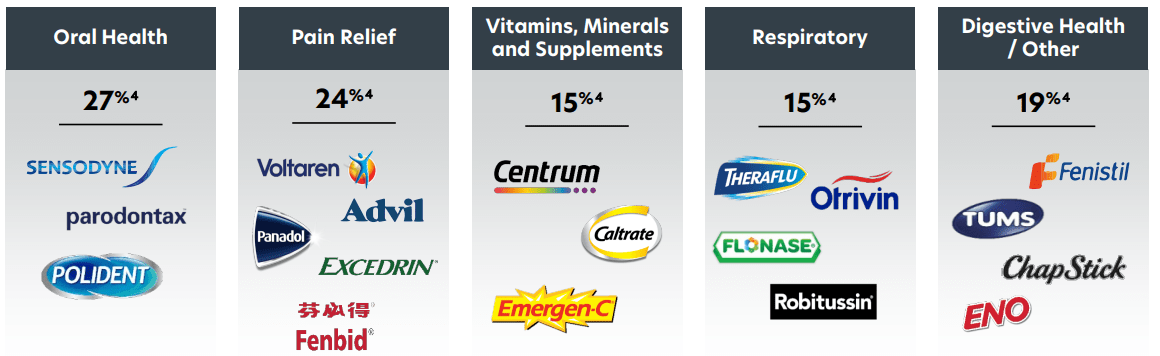

Haleon's strategy is to utilize its market-leading brands and deep expertise to continually develop important healthcare products for consumers. The company's objective is to achieve sticky revenue, enhancing the lives of its customers via its products to generate repeat purchases. The significance of its brands is predicated on the effectiveness of the problem solved, as well as intelligent brand development. Haleon operates a range of leading brands in all of its key segments.

{kind=link}

The global consumer healthcare market has grown healthily over the last decade, reaching an estimated £160bn in 2022. The largest geographical market within this is the US, comprising c.27% of the market. The market is relatively fragmented, with a high level of competition given the attractive economics. As previously established, the ability to innovate and develop a distinguished brand is critical to success (Source for statistics: Haleon) .

The value of brands is critical in this market and is relatively easy to assess. The ability to successfully innovate (the second critical success factor) is less so. Haleon has a c.1400-person team of scientists with a deep understanding of regulatory requirements. In the last 3 years, Haleon generated 19,000 regulatory approvals, underpinning its significant commitment to product development (Source: Haleon) .

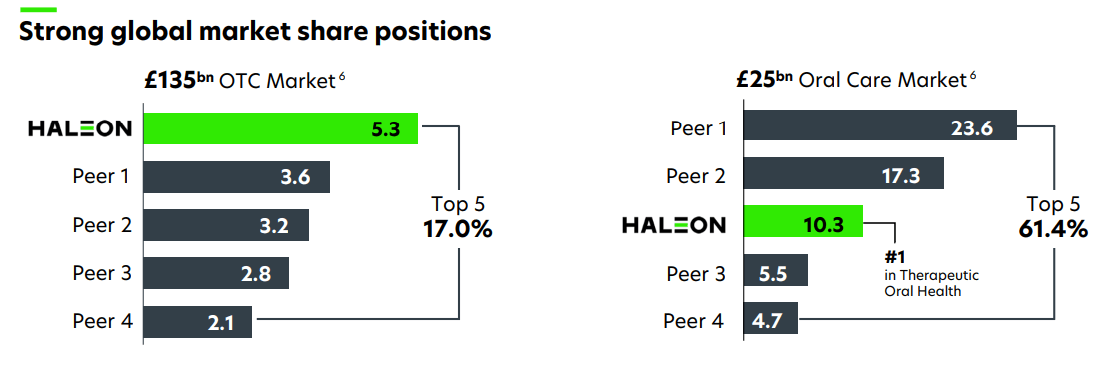

Our view is that Haleon is potentially the best-placed business in the market. The reason for this is the strength of its brands across the key healthcare segments. When considering market share, Haleon is the leader in the OTC market and 3rd in the Oral care market.

{kind=link}

Industry trends/development

Further, we believe the market to be quite attractive, with scope for good growth in the coming years.

Although the point is fairly obvious, it is worth initially mentioning the stickiness of healthcare demand. Most consumers, especially in the West, have a range of healthcare products they purchase regularly for the entirety of their life. A classic example of this is Oral Health products (Toothpaste, etc), but also other such items as painkillers and digestive aids. The demand for said products will not readily dissipate and when prices are increased, consumers are forced to accept.

Western populations (in particular) are aging, leading to an increased prevalence of chronic diseases and age-related conditions. As a result of this, there is a growing need for healthcare products that address the specific needs of elderly individuals, including medications and nutritional supplements. Haleon's brands, and the business as a whole, are positioned perfectly to benefit from this market growth. We suspect the business will position itself in the M&A market to grow its exposure to this segment, such as through the acquisition of vitamin businesses, in the coming years.

Consumers are increasingly taking charge of their own health and seeking self-care solutions. They are looking for products that enable them to manage minor ailments, maintain their well-being, and enhance their quality of life. This is driven by social pressures to maintain appearances, ease of access to remedies, as well as a greater understanding of wellness. This trend has contributed to growth in the OTC market, a segment that Haleon leads. We expect this trend to continue in the coming years.

In conjunction with this, there is a growing emphasis on preventive healthcare, with consumers becoming more proactive in managing their health and well-being rather than letting issues develop. The reasons for this are selfish in nature, as discussed, but also due to the current pressures on public health systems (and the associated costs). In the UK, for example, people prefer to avoid the healthcare system for minor issues due to the time cost. In the US, it is due to the financial cost. Similar to the above, this will contribute to continued strength in the OTC market.

Finally, a key market driver is the continued economic development of emerging markets. As these countries experience an emerging middle class, the demand for such products, especially in the premium segment, will only increase. We suspect the consumer healthcare market in these countries will begin to mirror that of the West, which means a substantial increase in usage. The critical success factor for Haleon is the development of its brands in these regions, as well as the intelligent acquisition of successful brands.

Margins

Haleon's margins are attractive. It has a GPM of 62%, EBITDA-M of 24%, and a NIM of 10%.

Strong margins are a reflection of the industry, with low production costs and innovation allowing for aggressive pricing. The recent improvement in margins has been driven by inflationary pressures, with Haleon increasing prices (as well as a degree of impact from the demerger).

{kind=link}

Balance sheet

Haleon has a ND/EBITDA ratio of 3.6x, an elevated level in our view. We are not overly concerned, however, as the substantial cash flows of the business (Current FCF-M of 16%) should mean a rapid deleveraging process. We believe a 3x level is sufficient to operate sustainably.

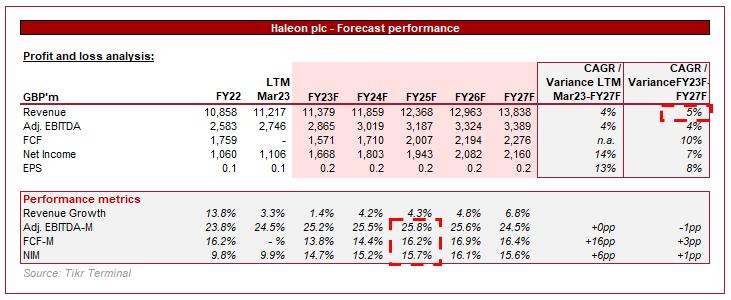

Outlook

{kind=link}

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting a healthy growth rate for what is a mature business, forecasting a CAGR of 5%. Management's current medium-term guidance is 4-6%, implying analysts currently buy into Management's vision. This is a reasonable estimate, although is susceptible to FX fluctuations given the global nature of the business.

Margins are expected to remain flat, which is a reasonable estimate given the maturity of the business.

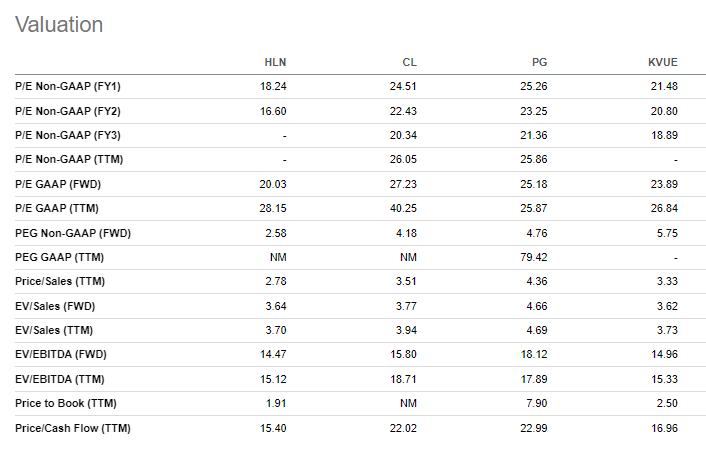

Valuation

Haleon Valuation Overview ( Tikr Terminal)

Haleon is currently trading at 14.5x LTM EBITDA and 14x NTM EBITDA. In order to value the business, we have assessed it on a relative basis via a comparison to Kenvue, Procter & Gamble ( PG ), and Colgate-Palmolive ( CL ), all businesses with a substantial portion of consumer healthcare exposure.

{kind=link}

Haleon is currently trading at a discount to all 3 businesses while being marginally the second most profitable of the 4. Further, the company has the lowest Debt/FCF yield, and as we have discussed, its holistic exposure to consumer healthcare should support good growth. This contrasts with CL , which is highly levered through excessive distributions and is experiencing a stagnation in growth. PG and Kenuve are strong businesses in their own right with potential upside (analyst estimates of 10%/7%).

These factors imply Haleon is undervalued at its current share price.

Key risks with our thesis

The risk to our current thesis is:

- A potential weakness in branded goods following a period of heightened inflation. Although volume remains strong for Haleon (muddied by demerger considerations), the medium-term impact of aggressive pricing actions by FMCGs is yet to be seen (Consumers switching to generic alternatives). In our coverage of other FMCGs, we have continually heightened this as a key risk, with some FMCGs feeling the impact as volume begins declining QoQ.

Final thoughts

Haleon is a leading business in the consumer healthcare business. Through its brands and deep expertise, the business has a wide moat and almost unchallengeable position.

With continued tailwinds in the industry, we suspect Haleon will grow well, and potentially even improve margins. Regardless, we believe an upward trajectory is likely.

Haleon is trading at a discount to its peers despite the strong performance, implying upside at the current share price. Unilever ( UL ) famously offered £50bn for what became Haleon and was lambasted by shareholders (Its boss subsequently departed ). At the time, I felt GSK was crazy for rejecting this but based on its current trajectory, this may work out well for shareholders.

For further details see:

Haleon: Leading Business In An Attractive Industry