HAL - Halliburton: Getting A Bigger Piece Of A Growing Market

2023-10-09 21:56:46 ET

Summary

- Halliburton's shares have risen about 30% in the past year and are still inexpensive, making it a good buy recommendation.

- The company's international operations now account for the majority of its revenue, with revenue per international rig increasing by 33% in the past three years.

- Halliburton's strong balance sheet and growing market share position it for further revenue growth, margin expansion, and the ability to return more cash flow to shareholders.

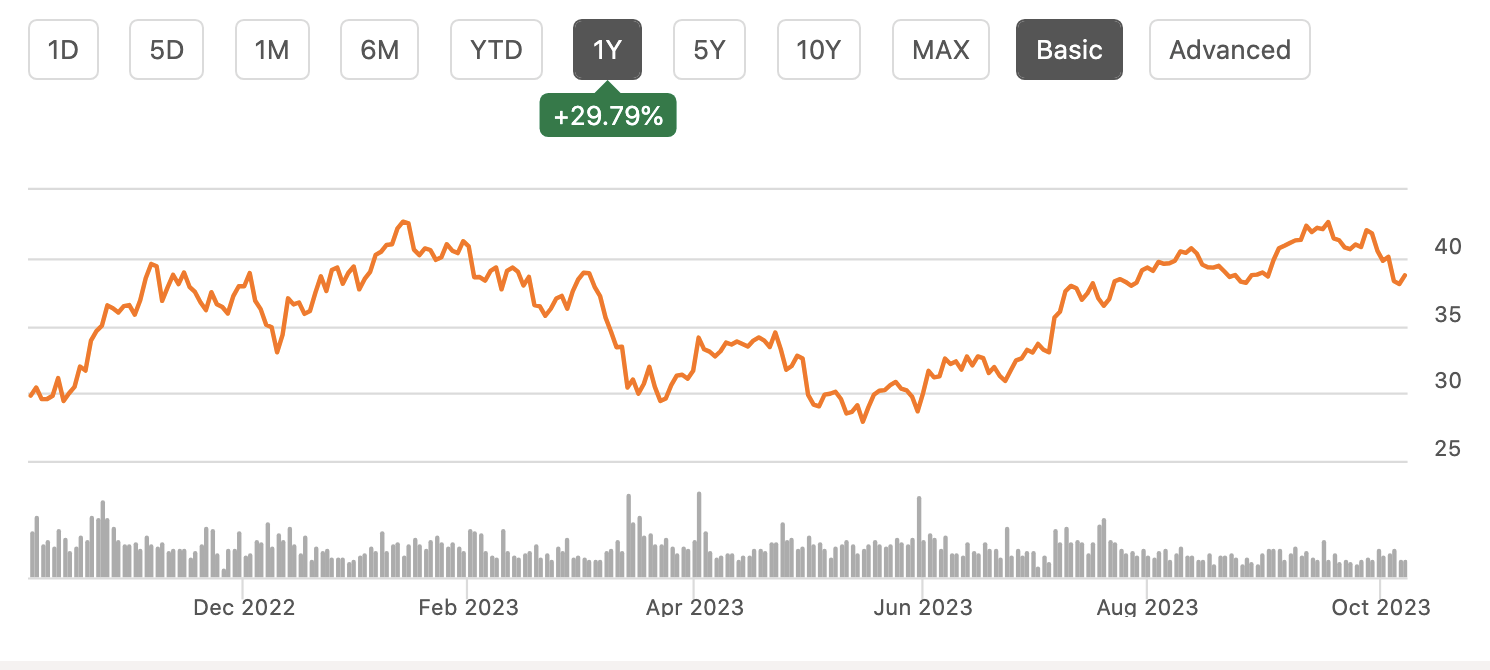

Shares of Halliburton (HAL) have been a strong performer over the past year, rising about 30% as oil & gas capital investment has continued to rise. Since recommending investors buy shares last October , the stock has returned about 36%. Even after this run, shares are inexpensive, considering the ongoing need for investment, and I would reiterate a buy recommendation.

{kind=link}

In the company’s second quarter , Halliburton earned $0.77 in adjusted EPS as revenue rose by 14% to $5.8 billion. EPS rose by over 50% as operating margins also expanded by 329bp to 17.4%, due to the operating leverage inherent in the business. This has been a stronger margin capture than even I had hoped for last year as strong demand for Halliburton services has provided pricing power.

Halliburton also develops and sells software to assist in evaluating wells, reserves, managing production flows, etc. As with a technology company, this software development cost is relatively fixed whether one customer or a dozen is signed up, so as drilling activity has increased and more have adopted HAL’s offerings, we have seen substantial margin accretion. This pivot to less capital-intensive offerings has also helped Halliburton bring cap-ex spending down to about 5-6% of revenues, from 8+% in years prior.

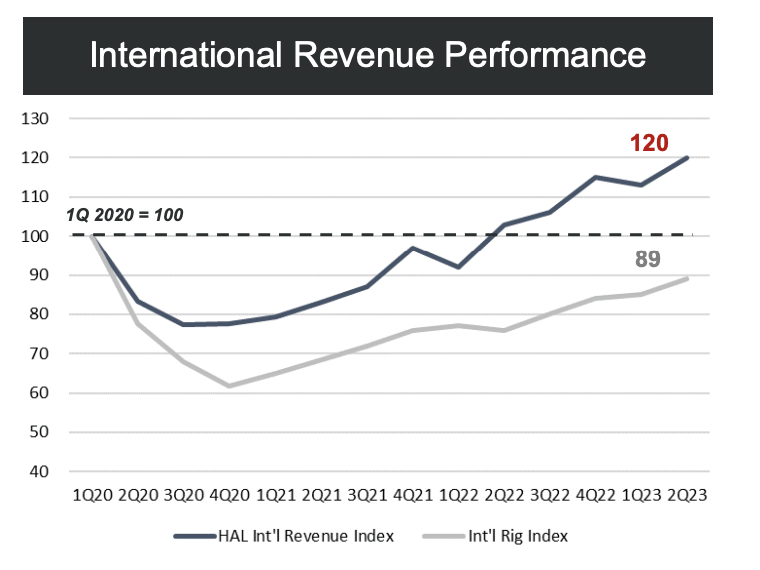

These offerings have helped Halliburton gain market share within the oil field services sector, particularly overseas. As you can see below, since the start of 2020, HAL’s international revenue has risen by 20% while the international rig count is still 11% lower. HAL is generated about 33% more revenue per international rig in operation than it was just three years ago.

{kind=link}

This is particularly noteworthy as Halliburton’s business profile had always led it to be seen as a primarily North American company, in large part because it is the market leader in providing oil field services to fracking, which dominates US production. While HAL is heavily skewed to the US, international operations now account for the majority of its revenue (53%). North America is still the largest component, at 47%, and growth was a solid 11% from last year. Overseas, its geographic profile is rather diverse: 24% in the Middle East and Asia (revenue up 20% from last year, 17% in Latin America (up 31% from last year), and 12% in Europe and Africa (down 3% due to high software sales in Norway last year).

Consistent with Halliburton’s data, the Baker Hughes overseas rig count remains below pre-COVID levels, though it has been rising steadily. I would expect continued increases overseas. Even with the shift towards renewable energy and products like electric cars, the International Energy Agency expects oil demand to rise about 5.5% over the next five years, due to growth in the emerging world. The world needs more fossil fuels over the medium term to meet this demand. That will require getting drilling levels back to historic norms.

Baker Hughes

There are plans in place for this to happen. Brazil is proposing a $200 billion infrastructure program with increased exploration from Petrobras (PBR), a cornerstone of the plan. Saudi Arabia is proposing a 60% increase in capital spending over the next three years. Countries like Guyana have also become a key area of oil & gas investment, with Exxon Mobil (XOM) recently announcing plans to boost its spending there by $12 billion . Additionally, Saudi Arabia and Russia are capping production and will continue to do so through year-end, in a bid to keep prices elevated. The strong cash flow from higher oil prices will enable E&P firms to continue to grow cap-ex budgets.

While overseas growth is a critical tailwind for Halliburton, the US is its leading market. It is impressive to see the company’s double-digit revenue growth, given the decline in the rig count year to date. HAL is generating more revenue per operating rig, pointing to both its growing market share and strong pricing power. Importantly, we are now seeing the rig count stabilize, given higher commodity prices than a few months ago, meaning this headwind (which HAL was overcoming quite well) should fade.

Baker Hughes

This backdrop points to continued revenue growth for HAL over the next 18-24 months, at least. I would also note that Halliburton generates income across a well’s life cycle. Drilling and evaluation drive operating income of $376 million, up 31% from last year. More importantly, completion and production earned operating income of $707 million, up nearly 42%. The rising drilling activity we are seeing now will lead to wells that need completion and begin production in the coming months, which is where HAL generates nearly twice as much profits. This flywheel will help support ongoing profit growth.

This strong backdrop has resulted in impressive free cash flow, including $800 million of free cash flow last quarter. Over the past year, it has totaled $2.1 billion. Halliburton has committed to return at least 50% of free cash flow, and last quarter management said it has “confidence in our ability to return more cash to shareholders” in the earnings press release.

That is beginning to become apparent with $248 million of stock repurchased in Q2. HAL has a $4.5 billion buyback authorization. Halliburton also raised its dividend by 33% to $0.16 in Q1 , though it is still below the pre-COVID $0.18 level. The dividend was cut during COVID due to the uncertainty of the times, which may turn off some investors.

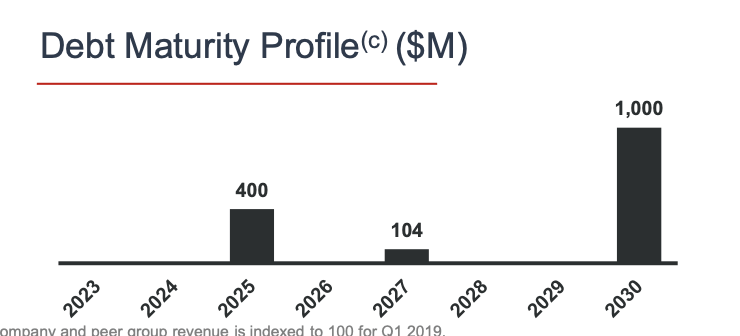

It is important to emphasize though that Halliburton has taken the past few years to aggressively improve its balance sheet, meaning the dividend should be more secure in future downturns (though hopefully nothing like COVID occurs again in the future). Its long-term debt is down by $2.4 billion since the end of 2019 to $7.9 billion. HAL only has one $400 million maturity over the next three years, which it can easily pay with its $2+ billion in cash on hand. About 80% of its debt does not mature for 7+ years. This also helps to insulate cash flows from higher rates.

{kind=link}

Haliburton is performing strongly, with the business generating meaningful growth as it grows its international business while maintaining a leading position in North America. This revenue growth is dropping down nicely to the bottom line as margins expand. With international drilling still muted and a host of projects needed to meet rising demand, I expect further revenue growth and margin expansion. At the same time, with its stronger balance sheet, it can return more cash flow to shareholders and sustain its dividend, even during a downturn.

In an $80 oil world where we see drilling activity rising by about 5% overseas and staying flat in North America, Halliburton can generate about $3.25 in earnings, giving shares a 12x multiple. At that level of earnings, it can pay its dividend and buy back about $1-1.5 billion in stock, enabling about 3% share count reduction. Lower oil prices and/or a recession are a risk, but at this multiple, given the need for a prolonged upcycle in global drilling, investors are being well compensated for it. I can see shares moving to about $45-48 or about 14-15x earnings as investors increasingly appreciate HAL’s gains overseas, and the ability of the company to accelerate shareholder returns now that its balance sheet is strong.

For further details see:

Halliburton: Getting A Bigger Piece Of A Growing Market