HAL - Halliburton: Not Enough Projected Growth To Offset Its Asset To Liability Relationship

2023-12-06 06:13:15 ET

Summary

- Shares for the Halliburton Company are currently overpriced and need to be reduced by approximately $4 before the share price warrants a buy rating.

- While Halliburton's valuation suggests an 8% upside when put through a discounted cash flow analysis, this still isn't enough upside when considering all the liabilities on Halliburton's balance sheet.

- There are other oil and gas companies that have a better relationship between their assets and liabilities and offer a better investment opportunity.

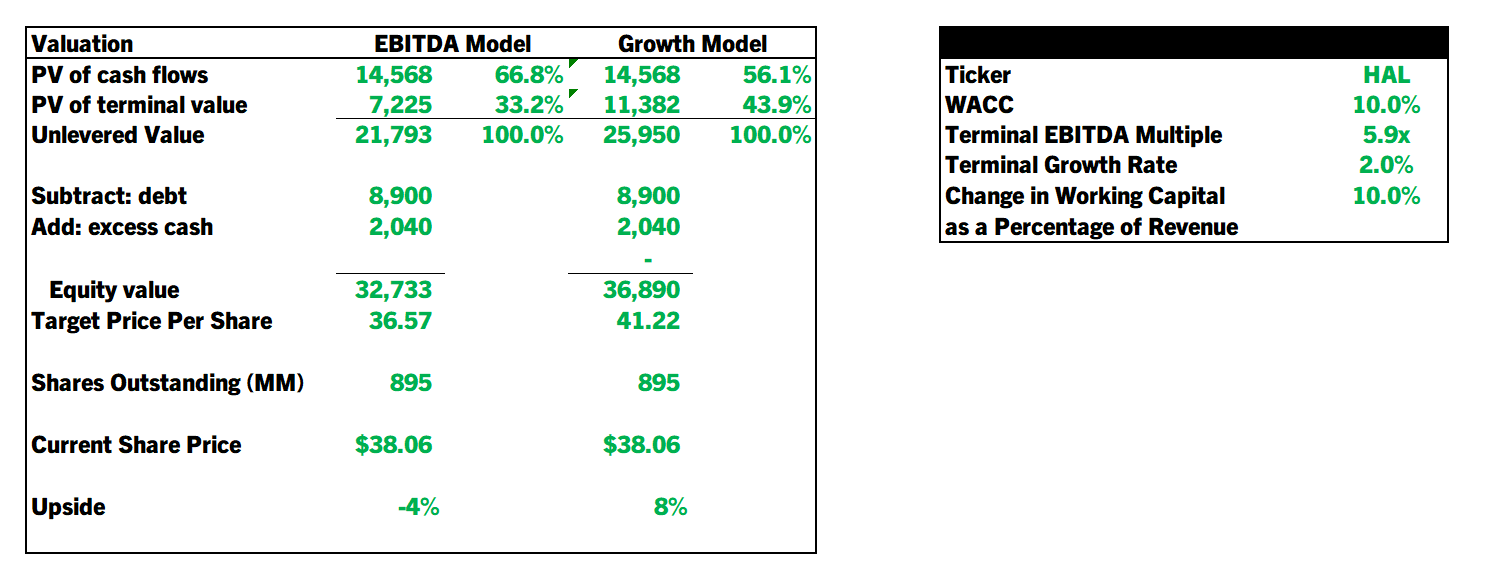

The Halliburton Company ( HAL ) has seen an impressive amount of growth from 2022 to 2023 and I believe that currently when taking into account the company's valuation from both a net asset value and a discounted cash flow perspective that the Halliburton Company should currently have a hold rating. The current price of $38.06 suggests an 8% upside when running it through a discounted cash flow analysis with a 3.1% growth rate through 2027 then a perpetual growth rate of 2%, with a 10% WACC, and a 24.4% tax rate. HAL's balance sheet valuation meanwhile, falls short of other oil and gas companies' balance sheets in debt to equity, Price to sales, long term debt, and price to book ratios. All of these data points leads me to believe that the Halliburton Company is currently a hold.

Company Overview

Founded in 1919 and based out of Houston, Texas the Halliburton Company provides services for oil and natural gas businesses globally and splits its company up into two main segments. The completion and production segment helps HAL's customers finish drilling oil or gas wells, offers hydro fracturing services, as well as offering pipeline and processing services to transport product to pipelines or processing centers. The drilling and evaluation segment helps customers decide as accurately as possible the best place to drill new wells for maximum well production and efficiency as well as aiding in the drilling of new wells or being contracted out to physically drill the wells for their customers.

Business Operations

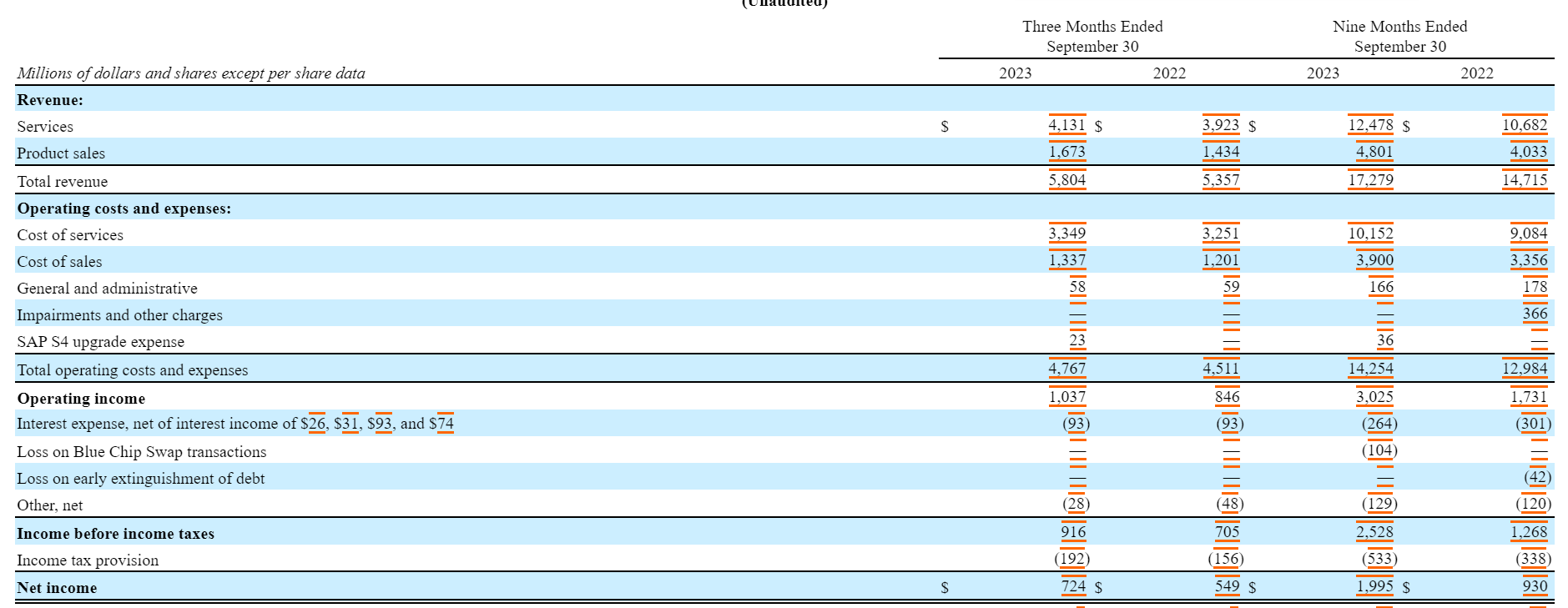

HAL has seen a stable increase in its revenue since 2020 and so far Halliburton has seen a 17% total increase in revenue when comparing the first nine months of 2022 to the first nine months of 2023 from $14.7 billion to $17.2 billion. This increase in its revenue figures has allowed HAL to grow its operating income by an impressive 76.5% from $1.7 billion in the first nine months of 2022 to $3.0 billion in the first nine months of 2023. This kind of revenue growth can be attributed largely to HAL's completion and production segment's ability to increase utilization and its pricing for its pumping services on top of higher global sales of tools used to complete wells. HAL saw its drilling and evaluation segment's revenue increase due primarily to its increase in its drill related services as well as higher wireline activity (Which essentially monitors well reservoir activity for data on how to proceed with getting the product out of the ground). All of this has led to a 114.5% increase in net income for Halliburton from $930 million in the first nine months of 2022 to $1.99 billion in the first nine months of 2023.

HAL's Statement Of Operations (Halliburton's 2023 3rd Quarter 10-Q)

{kind=link}

At the beginning of 2023 Halliburton's board of directors approved a framework for returning at least 50% of its free cash flow to its shareholders through share repurchases and dividend payments. So far this year HAL has paid out $433 million in dividends and $546 million in stock repurchases.

Balance Sheet

Assets

{kind=link}

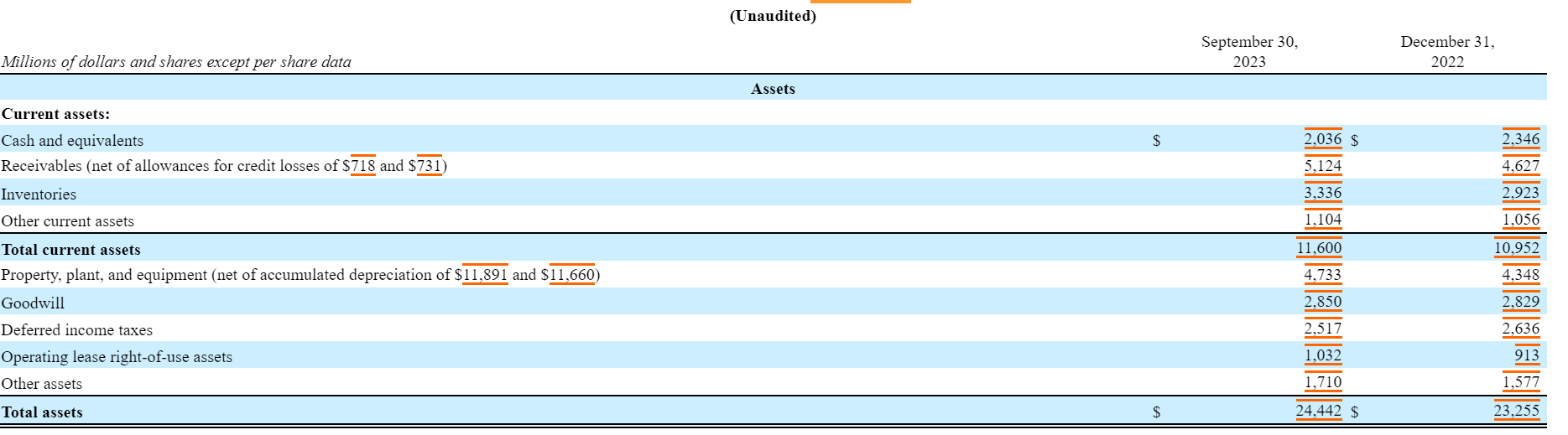

Halliburton saw a 5.9% increase in its total current assets in the first nine months of 2023 at $11.6 billion versus $11 billion in the first nine months of 2022. This increase comes from higher receivables and inventory levels and helped boost total assets for HAL by 5.1%. Unsurprisingly when higher inventories are needed for an increase in business demand this generally leads to higher capital expenditure costs and HAL's capital expenditures rose from $661 million in the first nine months of 2022 to $980 million in the first nine months of 2023. This added expense to business is still in line with HAL's commitment to keep its capital expenditures in the range of 5-6% of its total revenue. HAL has the flexibility to keep its capital expenditures in line mainly because it manufactures most of the equipment it provides to its customers.

HAL's Capital Expenditures (Halliburton's 2023 3rd Quarter 10-Q)

{kind=link}

Liabilities

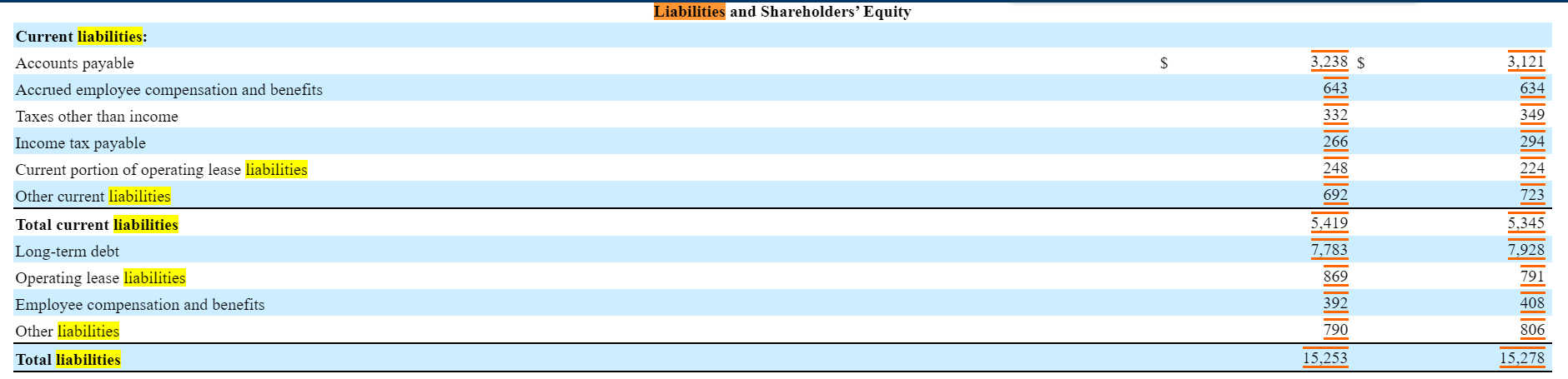

Despite the increase in assets the Halliburton Company only increased their total current liabilities by 1.4% from $5.3 billion in the first nine months of 2022 to $5.4 billion in 2023 and slightly decreased their total liabilities by 0.3% from $15.28 billion to $15.25 billion. $150 million of HAL's various bonds due between 2024 and 2096 had been repurchased by the company in August of 2023 being one of the reasons they were able to reduce their overall liabilities. This helped drop the fair value of HAL's total debt in the first 9 months of 2023 down to $7.1 billion down from $7.9 billion in the first 9 months of 2022.

{kind=link}

These debt repurchases have been offset by HAL's unfortunate necessity to sell off its remaining operations in Russia and Ukraine which amounted to a $366 million pre-tax write down charge for its Russian operations and a pre-tax charge of $22 million for HAL's Ukrainian operations.

Halliburton has also began its migration to a new business software called SAP S4. The software transition period is supposed to last until the end of 2025 and cost $250 million. So far HAL has only spent $36 million on the SAP S4 migration so investors should be looking for another $214 million in expenses over the course of the next two years.

Peer Comparison

When compared to the Baker Hughes Company ( BKR ), TechnipFMC plc ( FTI ), NOV Inc. ( NOV ), Weatherford International plc ( WFRD ), and Transocean Ltd. ( RIG ), HAL's total debt to equity stands at 96.85% compared to RIG and FTI who have debt to equity in the 70% range and BKR and NOV who have a debt to equity relationship in the 40% range. HAL also has the highest total amount of long term debt at $7.78 million.

{kind=link}

{kind=link}

HAL's price to book ratio also comes in significantly higher than most of its comparisons at 3.67 versus NOV's 1.35, BKR's 2.23, FTI's 2.94 and RIG's 0.48 leaving only WFRD with less assets to back up the value of its stock. Price to sales is again another figure where Halliburton's ratio of 1.48 is less desirable than NOV's 0.89, FTI's 1.23, WFRD's 1.33, and BKR's ratio of 1.39. Only RIG has a higher price to sales ratio at 1.75.

HAL does have a lot of positive figures in its corner when compared to these other oil and gas companies, for instance HAL has the second lowest price to cash flow ratio at 10.46 vs an 11.24 for BKR, 16.17 for FTI, and a 20.89 for RIG. HAL also has the second highest return on assets and return on total capital at 13.36% and 14.17% which is at least double the figures for the return on assets and return on total capital figures for every company in our comparison group except WFRD.

{kind=link}

My biggest reason for my hold call on HAL is its debt and liabilities not being offset by a large enough margin from its assets. With this being said it is promising to read Halliburton's 10-k and 10-Qs where they have been working to pay down their long term bond debt and hope this kind of prudency from management continues however, HAL still has a ways to go before its liabilities to assets ratios comes more into line with other businesses in the oil and gas industry. With a much more limited ability to sell off assets should oil and gas prices see a prolonged decline, HAL could have a tough time selling off non-core assets to meet its debt obligations while not having to cut into the core of its business model. Once HAL can get these metrics to line up better I would then continue to accumulate stock.

Discounted Cash Flow

The day I was writing this article HAL's price per share stood at $38.06. When running a growth model discounted cash flow analysis for Halliburton with a 10% WACC assuming a 3.1% annual revenue growth rate through 2027 and a 2% annual revenue growth rate every year after that, a 10% increase in working capital as a percentage of revenue, a 24.4% tax rate, and an average EBIT margin of 10.8% I got an 8% upside to that stock price. The 3.1% revenue growth rate was my average revenue growth rate between the years 2019 to 2023 (using a TTM average figure for my 2023 revenue figure). I again used the average EBIT margins between the years 2019 and 2023 to come up with my EBIT margin percentage and I used HAL's recent tax figures to set up an estimated effective tax rate.

After getting my EBIT margins I subtract taxes from that year to get an unlevered free cash flow before further subtracting capital expenditures, adding back in depreciation and amortization charges, and adding or subtracting changes in working capital to come up with my unlevered free cash flow.

{kind=link}

When I Would Change My Call From Hold To Buy

My main argument for putting a hold call on Halliburton is that it doesn't currently have an adequate relationship between its assets and liabilities to justify taking additional risk in further ownership of the company. The 8% upside from the $38.06 share price my DCF model shows doesn't convince me that HAL is undervalued enough to take a risk on HAL's liabilities however, if the share price dropped down to $34.00 a share you begin to see a 20% upside from that stock price. A 20% upside in the stock price would, I believe, adequately reward a prudent investor and help guard them from a potential drop in the demand for oil and gas drilling services that is possible should this oil production boom in the United States continue to slump the price of oil for a sustained amount of time.

When I Would Change My Call From Hold To Sell

A substantial increase in oil production from OPEC and OPEC+ converging with record U.S. oil production would give me a reason to worry about a prolonged collapse in oil prices. The combination of these two events would warrant me to consider selling my Halliburton stock. This seems unlikely to happen currently because U.S. oil output has put pressure on OPEC and OPEC+ to further lower their output to keep prices up.

Aside from a collapse in oil prices caused by too much supply, a global economic slowdown led by China or the Unites States could collapse oil and gas prices and reduce demand substantially hurting HAL's ability to produce free cash flow. Shutting down drilling projects would also incur further expenses on HAL that could force them to take on additional debt. This additional debt would further offset HAL's liability to asset balancing. Combining additional liabilities with an inability to generate levered free cash flow in the future could have investors finding themselves holding onto a stock headed toward a free fall.

Conclusion

To sum things up... I believe that the Halliburton Company stock is a hold because their projected discounted cash flow, while currently having upside, does not look like it has enough potential upside to make up for the fact that its assets in proportion to its liabilities are off-kilter and I would need to see an upside potential in the stock price of at least 20% for me to justify buying anymore more stock from HAL. When taking into account Halliburton's current balance sheet and my discounted cash flow parameters the stock price would have to hit about $34.00 a share to change my rating from a hold to a buy.

For further details see:

Halliburton: Not Enough Projected Growth To Offset Its Asset To Liability Relationship