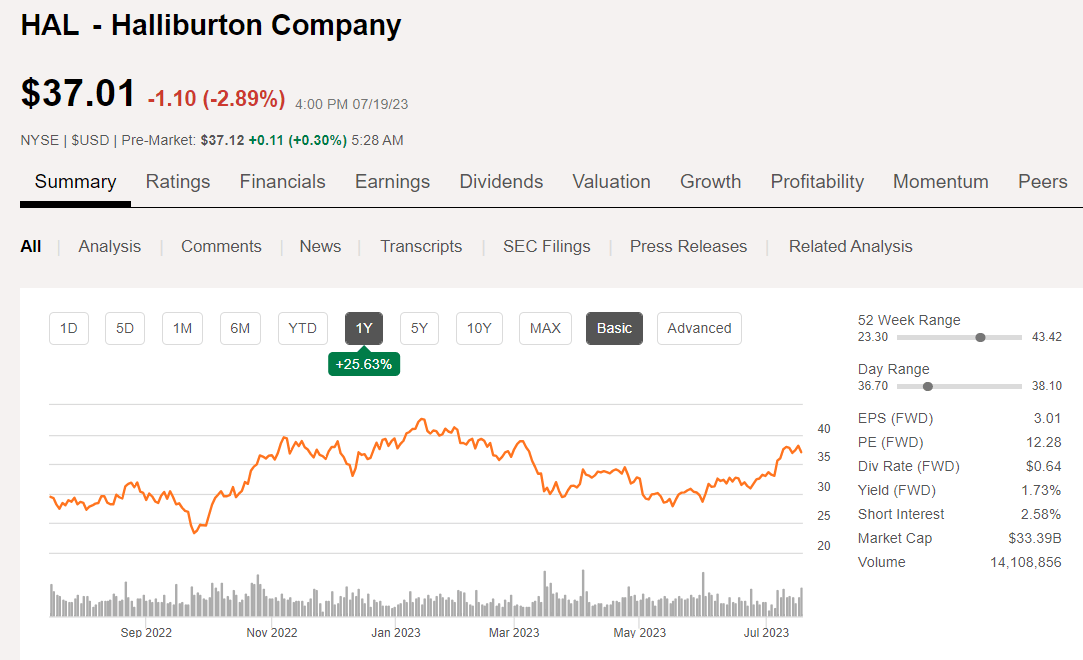

HAL - Halliburton Q2 Earnings: Technology Is The Key To Higher Margins

2023-07-22 08:00:00 ET

Summary

- Halliburton Company is growing margins sequentially through technology-driven sales.

- We think the company remains undervalued at current prices.

- Investors looking for growth and increasing shareholder returns may want to consider Halliburton Company shares for their portfolio.

Introduction

Halliburton Company (HAL), or "Hally" as I like to call it, has been steadily beating analyst estimates for a couple of years now. In Q1 2023 , they beat the estimate of $0.67 EPS by $0.05. Analysts moved expectations higher for Q2 by $0.03, which the company then beat again by $0.02, coming in at $0.77 per share as adjusted EPS.

{kind=link}

Revenues were off about $60 mm sequentially (hopefully to no one's great surprise), and the market spanked Hally with a 3% hit to shares.

Generally, the news from the call was strongly positive as regards international and Gulf of Mexico, but Hally validated our suspicions about Q-2 in North America, and the rest of the year. Eric Carre, CFO commented :

I know there's a lot of question on North America, so maybe I'll repeat what we indicated, which is H2 is going to be a little lower than H1 for North America. Q3 is a bit down compared to Q2 and we're expecting Q4 to be flat relative to Q3.

What the market is missing in those comments are the facts that Hally's margins are increasing, and cash flow is rising. Oilfield services have gotten more technology intensive, which more than makes up for a decline in activity. Jeff Miller CEO commented in this regard-

I think that this is my point around service intensity, meaning it takes more work to produce the same over time unless there are step changes in terms of either efficiency or insight. And so, we talk about our smart fleet offering quite often, but the reality is that's part of our technology portfolio to help customers better understand productivity of rock and where the frac is going and how to design fracs that can be more productive over time, so I think that's an important step.

That makes Hally a buy below $40.00.

The technology thesis for Hally

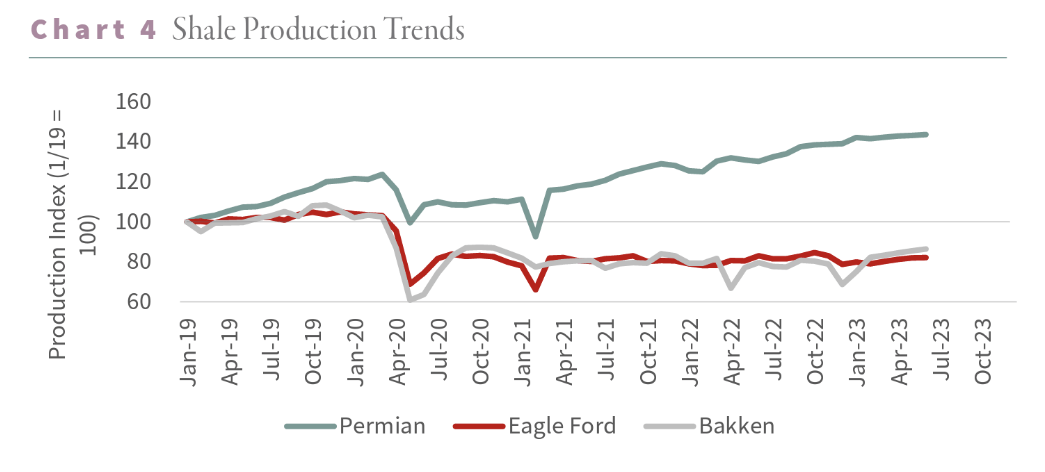

We are at a rough balance point in shale output, as reported by EIA DPR, WPSR, and 914 reports. Most shale plays are at best maintaining production levels thanks to sufficient levels of activity. Only one, the Permian, is still growing - barely. Opinions vary as to the exact cause for this plateauing of output.

There are two primary schools of thought. Certainly reduced activity measured against prior years is playing a role, (that's not the whole story as we will discuss), and poorer inventory now being drilled-a point I've made repeatedly, and one that analyst firm, Goerhring & Rosencwajg (G&R) makes in a recent blog report. The graph below shows relatively flat production from the Eagle Ford and Bakken since 2020. The Permian still is gaining, but at a much flatter slope since 2023.

{kind=link}

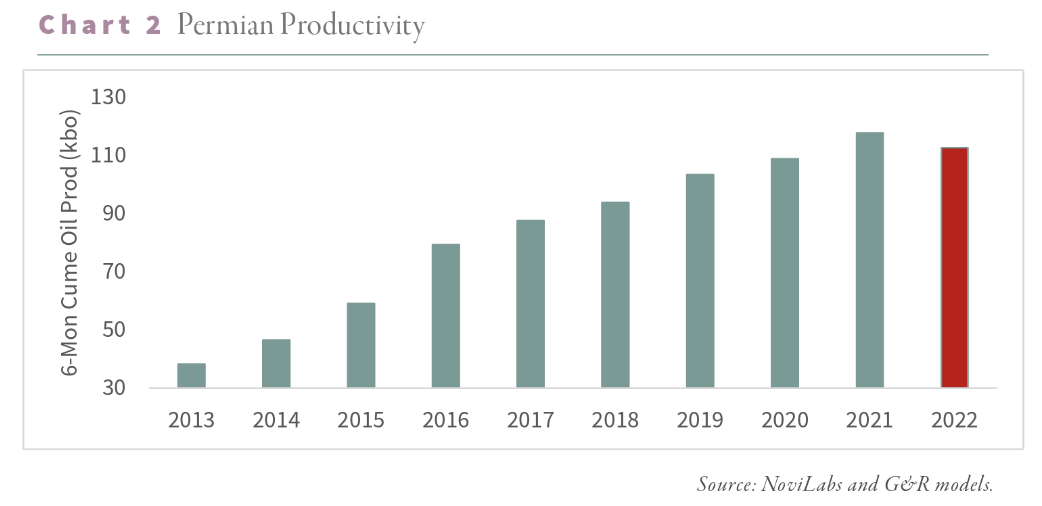

In a recent ( DDR internal ) article, I pointed out that a technological transformation had taken place since 2018 that enabled production to grow with far fewer resources than in the past. Longer horizontal sections, higher intensity treatments, better analysis (machine learning, AI) have enabled this growth. What we are now faced with is the reality of operators pulling forward their best-Tier I acreage in the 2018-2021 era, driven by prices, is beginning to exert itself, as this next G&R graphic shows.

Total oil produced over a 6-month period is falling, and not by an insignificant amount in 2022. What's changing is the productivity of the wells which was growing for the reasons listed above in 2021-22, the productivity per foot began to peaked in 2021. In 2022 the was no growth, and the law of large numbers began to take hold, and output per foot of interval began to fall.

{kind=link}

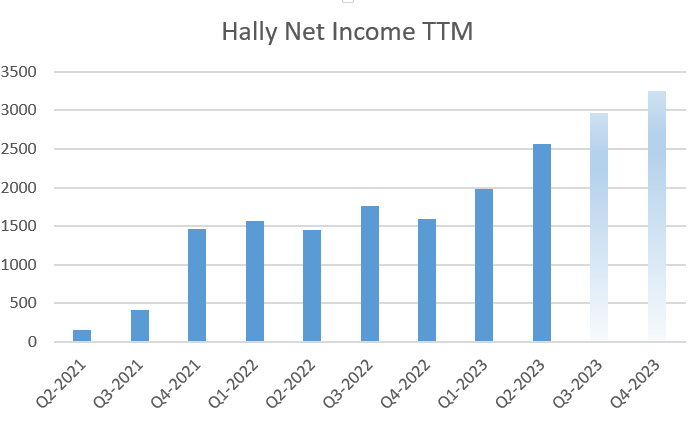

What is means for Halliburton is that, even though the raw numbers may flatline or fall, the technology required to maintain output, or at least slow the decline, will improve margins and add cash to Hally's bottom line. The chart below shows the progression in the company's net income over the last couple of years, and projects (based on analyst estimates) where it may go through the end of the year.

{kind=link}

Hally Q2 2023 and guidance

Total company revenue for the quarter was $5.8 billion, a 2% sequential increase, while operating income was $1 billion, a sequential increase of 4%. Operating margin for the company was 17.4% in the second quarter, a 329 basis points increase over second quarter of 2022 adjusted operating margin. These results were primarily driven by strong international activity across both divisions, along with improved pricing.

Completion and production segment

Revenue in the second quarter was $3.5 billion, a 2% sequential increase, while operating income was $707 million, an increase of 6% sequentially. C&P delivered an operating income margin of 20%. These results were due to increased activity from multiple product lines in international markets and higher artificial lift activity in North America.

Drilling and Evaluation division

Revenue in the second quarter was $2.3 billion, a sequential increase of 2%, while operating income was $376 million, a sequential increase of 2%. D&E delivered an operating income margin of 16%. These results were driven by higher drilling activity and increased fluid services in key regions, including Middle East and Latin America, partially offset by seasonal roll-off of software sales across multiple regions.

Geographic results

Second quarter international revenue increased 7% sequentially due to solid product sales, activity increases and pricing gains across multiple product lines. These results were impacted by lower software sales in the eastern hemisphere.

In North America, revenue in the second quarter was $2.7 billion, a 2% decrease sequentially. This decline was primarily driven by decreased stimulation activity in U.S. land, partially offset by increased artificial lift activity in U.S. land and higher activity across multiple product service lines in the Gulf of Mexico.

Latin America revenue in the second quarter was $994 million, a 9% increase sequentially, resulting from higher completion tool sales in Brazil and improved activity across multiple product service lines in Mexico and Argentina. Partially offsetting this increase is reduced activity in the Caribbean across multiple product service lines.

Europe/Africa revenue in the second quarter was $698 million, a 5% increase sequentially. This improvement was primarily driven by increased fluid services across the region and higher completion tool sales in Angola and Norway.

Middle East/Asia revenue in the second quarter was $1.4 billion, a 6% increase sequentially, largely resulting from higher completion tool sales in Saudi Arabia and higher Wireline activity, drilling services, and stimulation activity in the region. This improvement was partially offset by decreased project management activity in Saudi Arabia.

Q-2 cash flow from operations was $1.1 billion and free cash flow was $798 million. The company expects to generate free cash flow for the full year 2023; that is 30% to 40% higher than last year. Hally repurchased $248 million of their common stock during the second quarter.

Guidance for full year

The third quarter will be fairly flat. Completion and Production division, sequential revenue is expected to be essentially flat with the second quarter and margins to remain approximately flat. In the Drilling and Evaluation division, revenue is anticipated to increase sequentially in the low single digits and margins to increase 25 to 75 basis points.

Source .

Key wins in the quarter

- In the Middle East, Halliburton achieved a world record for the longest well ever drilled, with a measured depth of over 51,000 feet, using Halliburton's iCruise, iStar and LOGIX Technologies.

- Completions Technology is unlocking production for customers. Hally recently set another world record with the successful installation of the first 12 ZONE intelligent completion for a Middle East offshore customer using Halliburton's SmartWell technology on their eCompletions Platform.

- Landmark software business closed on the acquisition of Resoptima, a leader in advanced ensemble modeling at the reservoir level. Resoptima's technology, will accelerate Landmark's roadmap for next-generation reservoir modeling technology.

- Halliburton and Vår Energi's announcement of a long-term strategic relationship for drilling services.

A near-term catalyst

Hally is going full steam at trading out their legacy Tier II frac equipment with Zeus efleets that are in high demand for cost and emissions reduction. Jeff Miller commented on the impact of the Zeus fleets in North America:

Executing on our strategy during the second quarter, we deployed additional Zeus fleets on multi-year contracts, while retiring additional diesel equipment.

Demand for our Zeus e-fleets is strong. In fact, during the second quarter we signed more multi-year Zeus contracts than in any prior quarter. The multi-year duration of these contracts provides both stability and secure economic returns, which furthers my confidence in the strength of our margins. I continue to be impressed by the performance of our Zeus e-fleets and the optimization and efficiencies that come with scale.

We don't have any firm data on how these Zeus fleets are charged, but they are significantly more than older equipment, and as Zeus fleets comprise larger portions of the total, they should impact margins and revenues positively.

Risks

The rally we have seen in Hally is the result of oil prices firming in the mid-$70's, with an expectation of being driven higher as demand outstrips production in the second half. If that doesn't occur, we could see Hally stock fall back into the low $30's, or lower.

Your takeaway

Hally is trading at 15X Net Income on run rate basis. If that rises as expected through the course of the year, shares should rerate higher. If we hit $2.9 bn in Q3, the stock should rally toward $40 to maintain the same ratio. $3.2 bn in Q4, would get us to $44 by the end of the year, holding on to that 15X. That's a pretty good rally from current levels and should set the stage for 2024.

24 of the 29 analysts that cover Hally rate it a Buy . Price targets range from $34-57.00, with median being $46.

I think Halliburton Company stock is in a buy zone and have added to my position incrementally today.

For further details see:

Halliburton Q2 Earnings: Technology Is The Key To Higher Margins