HAL - Halliburton Q4 Earnings Preview: Increased Commitment To Capital Returns

Summary

- Next week, when Halliburton's results come out, I believe we'll see an increased commitment to return capital to shareholders.

- I believe that Halliburton's dividend could double to a +2.2% yield.

- A discussion of Halliburton's ability to improve the terms of its products and services margins.

Investment Thesis

Halliburton ( HAL ) is one of the world's largest providers of services to the energy industry. As such, I contend that its well positioned for both high oil prices and the inevitable demand that will follow from this positive and promising environment.

What's more, in my prior article , I said,

[...] despite all the bears' proclamations that a global recession will lead to oil demand next year coming down, the anecdotal evidence doesn't tie up with the actions of oil-producing countries.

I continue to believe this thesis, but this time I'm turning my attention in this analysis to focus on what I believe will be discussed at next week's Q4 earnings call, namely an increase in HAL's capital allocation framework.

Halliburton, Raking It In!

{kind=link}

HAL Q3 presentation

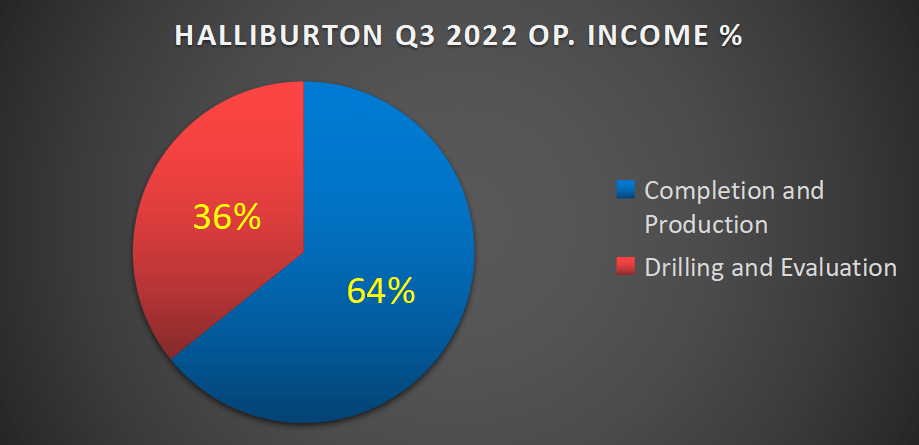

The graphic above demonstrates HAL's main segments. We can see its Drilling and Evaluation (shown above as exploration), as well as its Completion and Production.

And in the graphic that follows, we can see how Halliburton's profitability breaks down.

{kind=link}

As you can see above, approximately two-thirds of HAL's prospects are tied up to its Completion and Production segment.

On the surface, that could lead you to infer that HAL's Drilling and Evaluation segment isn't that interesting. After all, one would have thought that its true pricing power would come from its Completion and Production segment.

Recall, HAL's Completions and Production is involved in the production and recovery of oil and natural gas from wells by completing the well and preparing it for production.

This includes the addition of artificial lift systems or the cementing of the well wall itself to contain the oil in place, otherwise, the oil goes everywhere, and it's difficult and uneconomical to retrieve it.

Put simply, its Completion and Production service would have more fixed costs and a higher degree of operating leverage. But that's not what is actually happening. In fact, both Halliburton's segments are exhibiting a significant amount of operating leverage.

If I was to nitpick, I would contend that in fact, HAL's Drilling and Evaluation segment has the best operating leverage.

Nevertheless, this is my point of contention, that in the current environment, where oil prices are strong and relatively stable, oil exploration and production companies are very eager to pay up for oil service equipment and services .

And by extension, irrespective of the actual work that's being performed, HAL is reaching across the table and negotiating contracts on very favorable terms, irrespective of the service or product being provided.

I believe that in 2023, after multiple years of underinvestment by oil companies, it's unlikely to make much difference whether HAL is providing consulting services or equipment heavy lift systems. HAL is going to rake it in!

With this premise in mind, let's now turn to what I believe will be the focus of discussion next week, at HAL's Q4 earnings call.

Next Catalyst for the Stock, Capital Allocation Framework

HAL has approximately $6 billion in net debt. But the bulk of its debt isn't due until after 2030.

Put another way, I believe that next week HAL will discuss its capital allocation framework for 2023, investors will probably see as much as 50% of its free cash flow returning to shareholders.

I also believe that in 2023, HAL could end up returning as much as $1 billion of its free cash flow back to shareholders.

Accordingly, in practice, this will most likely mean that HAL's 1.1% dividend yield could more than double to +2.2%.

That being said, I don't believe that HAL will be too aggressive by returning more than 50% of its free cash flow, because it will want to leave behind some room for error and to shore up its balance sheet, in anticipation of inevitable difficult times ahead.

That being said, consider this.

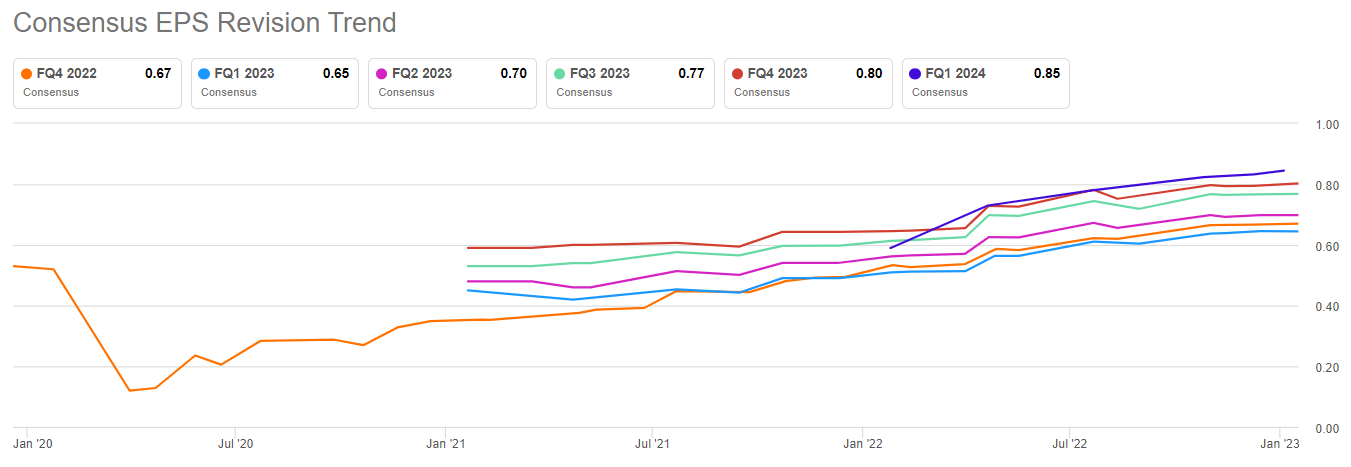

{kind=link}

HAL EPS estimates

What you see here is that analysts are steadily upwardly revising their EPS models for HAL.

It doesn't really matter all that much the exact figures that analysts have for HAL's EPS. What matters here is the ''directionality'' of the EPS.

There's a steady and rising conviction that HAL's near-term will be prosperous.

The Bottom Line

Here's the one-line summary, Halliburton has a strong balance sheet and will likely be announcing an increased commitment to return capital to shareholders.

The expanded summary notes that HAL, as an oil service company, will see strong demand for all its services and products in the coming year. This will mean rather than being a price taker as it has been in the recent past, it will be in a much stronger negotiating position.

This will translate into strong free cash flows and capital returns to shareholders.

Finally, I declare that the best investment situation one wants to be in, is in a stock where analysts are at your back and steadily raising their EPS estimates for the year ahead.

For further details see:

Halliburton Q4 Earnings Preview: Increased Commitment To Capital Returns