HAL - Halliburton Q4: Mixed Earnings

Summary

- Halliburton Company's free cash flow was up 79% y/y in Q4 2022. That's the bulk of the good news coming out of its Q4 report.

- The bad news here is Halliburton's share repurchase framework appears to be slowing down.

- With Halliburton's revenue growth rates also slowing down sequentially and the stock priced at 26x free cash flow, I'm less bullish on this name.

Investment Thesis

Halliburton Company ( HAL ) was a stock that I had high hopes for. Indeed, it doesn't take much to recognize that the oil business is booming and that oil service providers ought to be generating a ton of free cash flow.

That should mean that HAL would be well-positioned to return large sums back to shareholders. Incidentally, this is what I said last week :

I don't believe that HAL will be too aggressive by returning more than 50% of its free cash flow, because it will want to leave behind some room for error and to shore up its balance sheet, in anticipation of inevitable difficult times ahead.

And as it turned out, I was right. Frustratingly, too right! Because HAL ended up reducing its capital returns to 41% of its free cash flow.

And what's more, its press statement didn't openly declare that increased buybacks were coming. So, it turns out that going forward, for now, Halliburton Company shareholders will have to content themselves with a 1.6% dividend yield on the stock.

In summary, I'm a little less bullish on this name than I was.

Expectations Were High

Over the previous three months, Halliburton and the oil field services sector as a whole have performed significantly better than the S&P 500 (SP500).

It's fair to say that there were great expectations for this report going into it. But after the results report was released, the price hardly changed premarket (up 1%).

Why Didn't Halliburton Live Up to Expectations?

{kind=link}

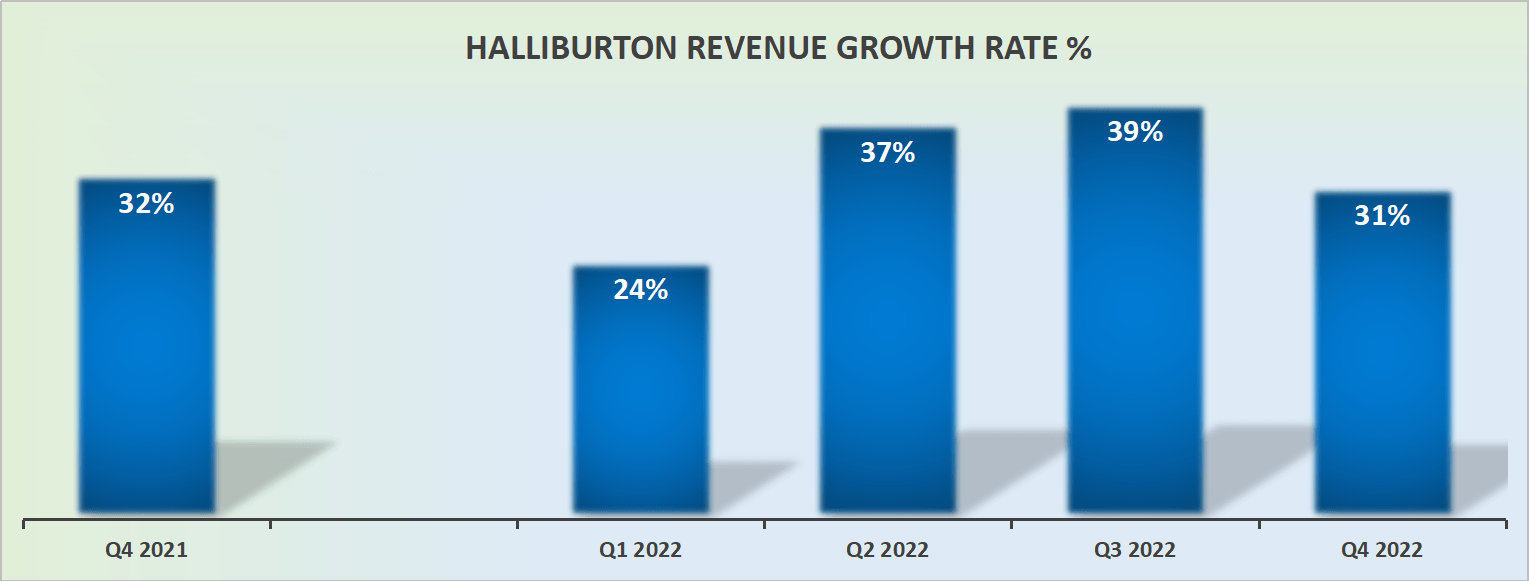

What's not to like, right? Halliburton just reported 31% y/y topline growth and even outperformed analysts' predictions. Well, not so fast.

The problem here is more nuanced than this.

{kind=link}

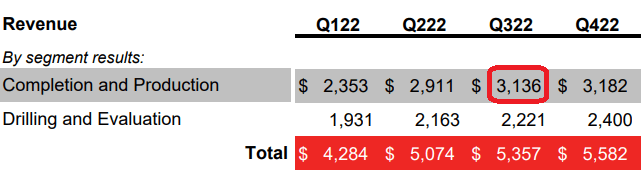

What you see here is that HAL's completion and Production segment appears to see slowing revenue growth rates with each passing quarter. More specifically, Q3 2022 saw $3.1 billion in revenues within its Completion and Production segment, while Q4 2022 was only up about 1% sequentially.

Immediately, investors are thinking to themselves, this means that Halliburton is going to have one more ''easy'' comparable quarter in Q1 2023, before the remainder of 2023 when Halliburton will have tough comparables to go up against.

This is fundamentally the investment thesis of Halliburton, a company that has recently finished a fantastic year with revenues increasing more than 30% y/y. Investors' stories were reinforced by the media, who picked up on the notion that the oil services industry was the place to be.

However, the problem here is that as we look ahead to 2023, investors are unsure of where HAL's revenue growth rates will stabilize at.

Should we expect to see +25% or +20% CAGR? Or perhaps +15% CAGR is where HAL's prospects will end up?

And getting a firm level of conviction over what sort of growth rate an investor is going to get from Halliburton in 2023 is crucial, particularly given that the stock has already rallied significantly more than the S&P 500 in the trailing 3 months.

But before anyone thinks that Halliburton Company stock is done and dusted, consider the following.

Bull Case, Free Cash Flow Jumps 79% Y/Y in Q4 2022

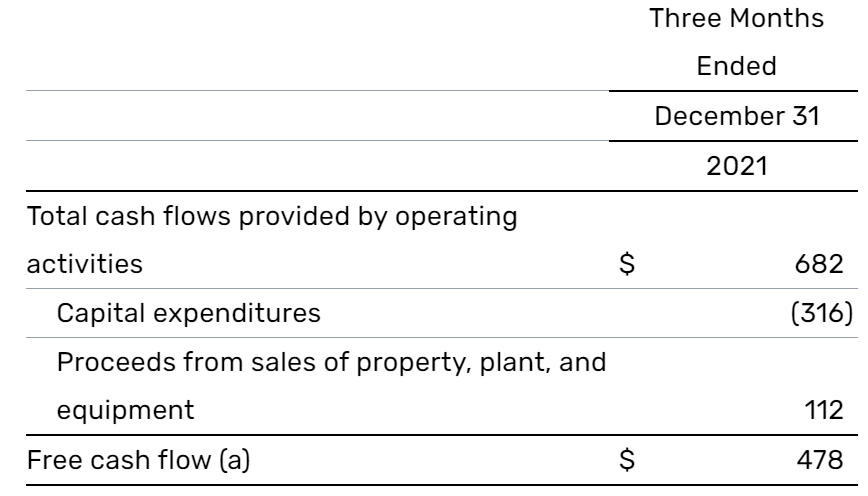

For perspective, consider HAL's free cash flow in the prior year Q4.

{kind=link}

What you see here is that Q4 2021 saw HAL's free cash flow at less than $480 million.

Then, fast forward to its most recently reported results, Q4 2022, and HAL's free cash flow was up 79% y/y to $856 million.

Clearly, Halliburton Company is making the right moves. And despite revenues not quite living up to investors' hopes, HAL's free cash flow line delivered a strong performance and then some.

So, what's the problem with the stock?

Capital Allocation Framework?

A few days ago, as we headed into HAL's Q4 earnings, I said:

I believe that next week HAL will discuss its capital allocation framework for 2023, investors will probably see as much as 50% of its free cash flow returning to shareholders.

As it turns out, this was wrong. Not only did HAL's return of capital end up at 41% of its free cash flow rather than my estimated 50% of free cash flow. But what truly surprised me is that HAL made no further mention of continuing to return capital to shareholders via share repurchases.

And this curious change in capital allocation would have left many investors unsure.

The Bottom Line

The best aspect of this Q4 quarterly result was that Halliburton Company's free cash flow line jumped by 79% y/y to $856 million. And this meant that, on a trailing basis, HAL stock is now priced at 26x trailing free cash flows.

However, when everyone in the oil sector is actively discussing ways to increase their capital return policy to shareholders, I believe that getting a 1.6% dividend yield on Halliburton Company stock doesn't live up to my expectations.

Author's rating on HAL

Thus, I'll bank my +12% gain on Halliburton Company while the S&P500 went nowhere fast since November and call it a day.

For further details see:

Halliburton Q4: Mixed Earnings