HAL - Halliburton: Solid Company Growing With The Industry

2023-05-25 02:05:11 ET

Summary

- Halliburton had a fantastic start to 2023 as revenues rose 33% YoY as a result of a demanding market and eager companies to start producing oil and gas.

- The industry might be under pressure by the social sentiment, but there are still projects starting which create an opportunity for HAL to continue growing revenues.

- The current price might not be severely undervalued, but paying a fair price for a great company is something I can stand.

Investment Summary

Halliburton Company ( HAL ) is a prominent multinational corporation operating in the energy industry, offering a comprehensive range of services and solutions to clients globally. The company is recognized as a leading provider of products and services for oil and gas exploration, development, and production. As an influential oilfield services company, Halliburton delivers integrated solutions such as drilling services, evaluation services, completion tools and services, production enhancement techniques, and reservoir consulting to its clients.

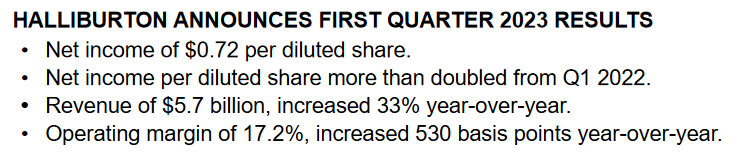

The strong position the company has in the market still leaves room for growth as shown in the last report by the company. To start off the first quarter of 2023, they managed to grow revenues 33% YoY to $5.7 billion. The company remains optimistic about the outlook for the year as they mention customers are eager to produce more oil and gas. The future estimates remain steady for the company and I think there is plenty of value here to be extracted by investors. Despite trading above the sector's average p/e, I find the company to still be a buy here given the dividend and the strong margins HAL has.

Oil And Gas Outlook

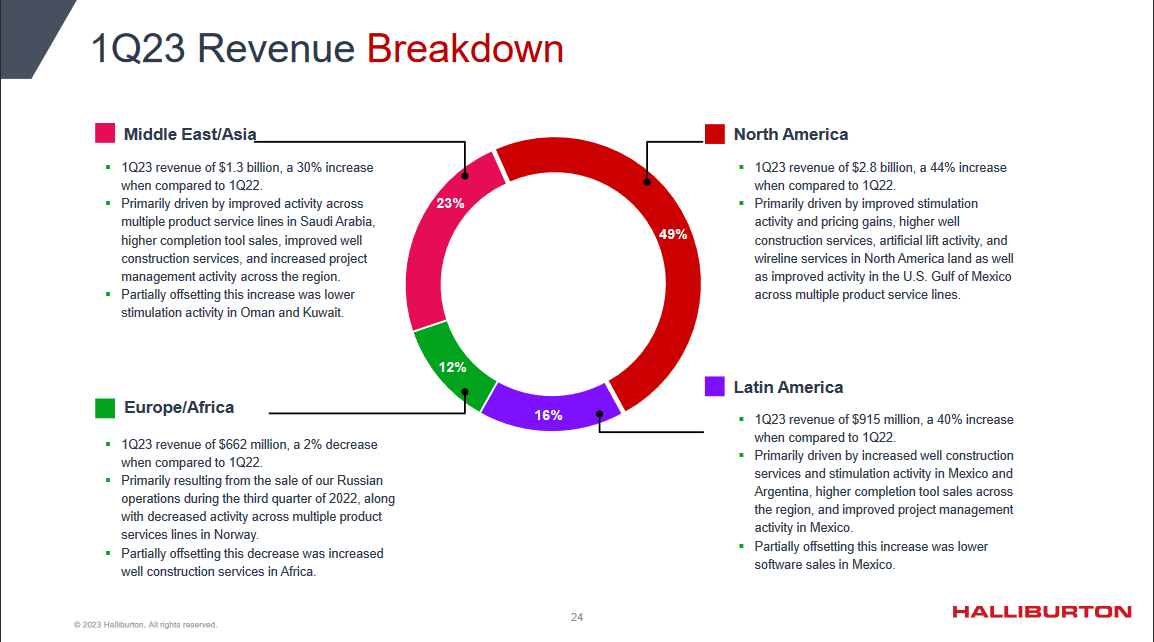

Looking at the momentum the company has been seeing it seems most of the markets they are present in remain demanding. The North American market made a big impact on the revenues as they increased 44% here YoY. Some of the reasons for the increase were improved stimulation and pricing gains and a general improvement in activities both in the US and also the Gulf Of Mexico.

{kind=link}

As Halliburton operates as sort of a service company to major drilling companies in the world, the demand for their products translates into a demand for the services that HAL provides. Looking at the US market prices of oil are steadily climbing as a result of continued demand whilst outputs remain lower. The sentiment around oil or nonrenewable energy sources has for a while now been very negative, and companies are uncertain about their prospects of being able to continue starting projects and drilling for oil. But it seems the tide is turning in the favor of big oil companies as it's easing into beginning more and more projects, in Alaska especially but other areas across the US.

{kind=link}

All in all, I think the outlook remains strong for HAL as they can ride the wave of continued demand for oil and natural gas across the globe, especially given their international presence and wide range of services. Oil prices are lower than a year ago, but expectations are high and some analysts estimate the prices to see a surge in 2023 or 2024. Keeping an eye on the growth of HAL could be a decent indicator of the sentiment in the industry and whether or not it's optimistic or not.

Quarterly Result

HAL had a fantastic start to 2023 with strong revenues increasing 33% YoY, and EPS coming in at $0.72 per share. The company had a difficult 2020 with negative net margins , but they seem to be on the track upward right now at least. Looking at the coming quarters keeping an eye on the margins will be a major priority for me as oil prices are stabilizing a major catalyst for HAL could be a continued improvement on the margins, without oil prices growing rapidly.

{kind=link}

The CEO Jeff Miller remained positive about the remaining 2023 and said that demand is strong among other things

"My Halliburton outlook -- for both the current year and the long-term -- is strong. We hear it from our customers, and we see it in our first quarter results. Our customers are clearly motivated to produce more oil and gas and service capacity is tight."

I think the easing of starting new projects is a major tailwind for the company. As new projects being they need the infrastructure and services that HAL provides in order to run it efficiently and profitably.

As highlighted before, some of the regions where strong growth was had were in the US. But I think that a region like Brazil could be an exciting new market to enter for the company. The expectations are high here and if HAL can get a foothold the current valuation might look like a steal in hindsight. Nonetheless, the coming quarters for the year will tell the story and lay the foundation for the value that investors can get here. If HAL continues to generate strong cash flows the dividend is likely to be kept up and possibly raised too as they have done before .

The Shareholder Value

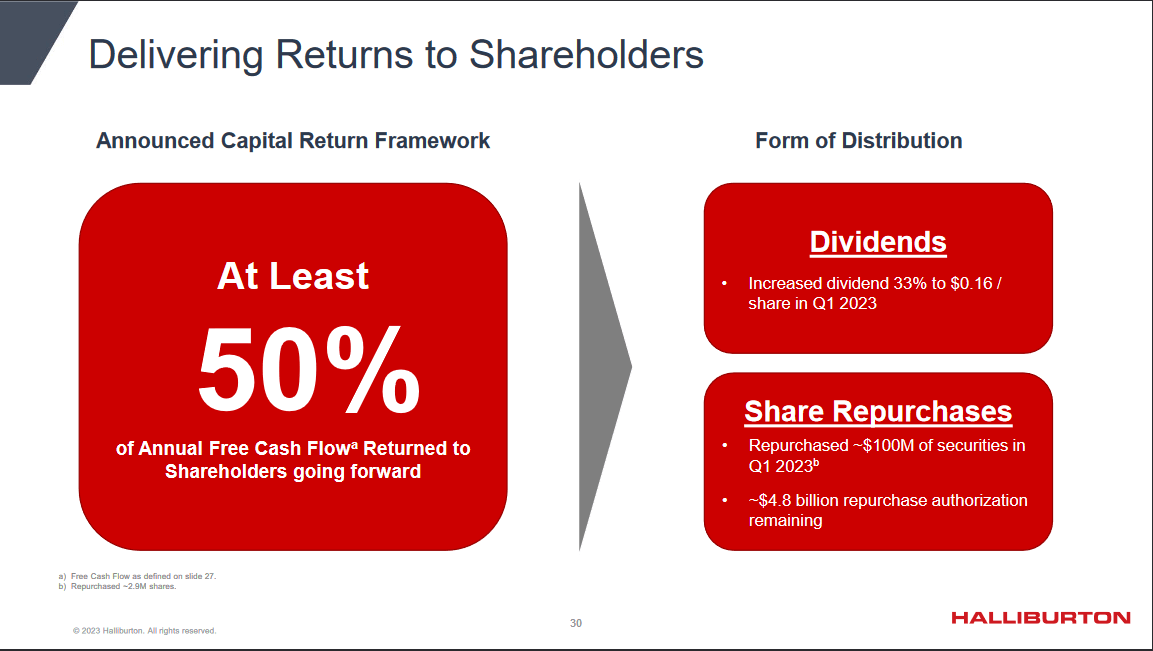

One of the key reasons for my buy rating with HAL is the value I think can be extracted by shareholders here. The company has announced an intriguing capital program going forward that will greatly benefit investors.

{kind=link}

With 50% of free cash flows returned to shareholders the coming several years could prove very profitable for investors. With already $4.8 billion authorized by the company for buybacks, they could theoretically reduce the outstanding shares by almost 20% right now. With an increased dividend too the company is looking more and more intriguing. With around $1 billion of FCF in 2022, a return of $500 million to shareholders annually would decrease the shares by around 1.8% yearly or result in a dividend of $1.81 per share, give or take. The one fear I have is the shares increasing over the last few years, and hopefully, the buybacks program the company has authorized will reverse this trend.

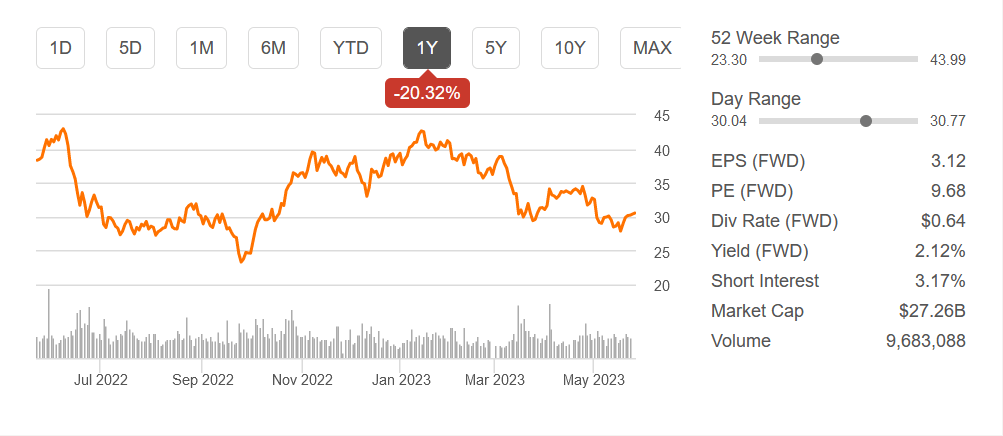

Valuation & Wrap Up

Right now HAL is trading a little above the rest of the sector, but I think the price right now is fair to pay and I don't think we are going to get a much better entry point. As the company has a massive buyback budget and strong dividend, buying at 9x forward earnings or 8x won't do much of a difference in 10 years' time anyway.

{kind=link}

What HAL offers is perhaps a different type of exposure to oil and gas, as they provide a service to the industry. But I think it's fair to say their revenues will very much also be driven by the cyclicality of the industry. Looking ahead though, oil prices seem to stabilize somewhat, and seeing whether or not HAL is able to grow margins will be interesting. I find the current price appealing and will be rating HAL a buy.

For further details see:

Halliburton: Solid Company Growing With The Industry