HAL - Halliburton: Still Undervalued

Summary

- Halliburton is one of the three largest oilfield service firms in the world and is the dominating pressure pumping company in North America.

- The company is well-known for its exceptional record of implementing new technologies and consistently developing new ways to maximize value for its customers.

- Based on my valuation modeling, I believe HAL stock represents a compelling investment opportunity.

Editor's note: Seeking Alpha is proud to welcome Dair Sansyzbayev as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment thesis

Halliburton Company ( HAL ) is known for its exceptional record of introducing new technologies and is constantly developing new ways to maximize value for its customers. Given all the prospects and a favorable Discounted Cash Flow ((DCF)) valuation, I believe Halliburton stock is an attractive investment opportunity despite the +72% bull run in FY2022 and +1% YTD.

Company information

Founded in 1919, Halliburton is one of the world's largest energy services companies, with over 40,000 employees and operations in more than 70 countries. The company helps customers maximize value throughout the lifecycle of the reservoir - from locating hydrocarbons and managing geological data, to drilling and formation evaluation, well construction and completion, and the optimization of production.

The company operates within very diverse product service lines which include every stage in the oilfield life cycle: exploration, well construction, completion, production and abandonment.

The company reports its revenue disaggregated by the following segments:

- Completion and production (57% of total revenue per latest 10-Q)

- Drilling and evaluation (43% of total revenue)

Revenue is also disaggregated by geographic regions:

- North America (47% of total revenue)

- Middle East/Asia (25% of total revenue)

- Latin America (17% of total revenue)

- Europe/Africa/CIS (12% of total revenue)

Financials

Last quarter results

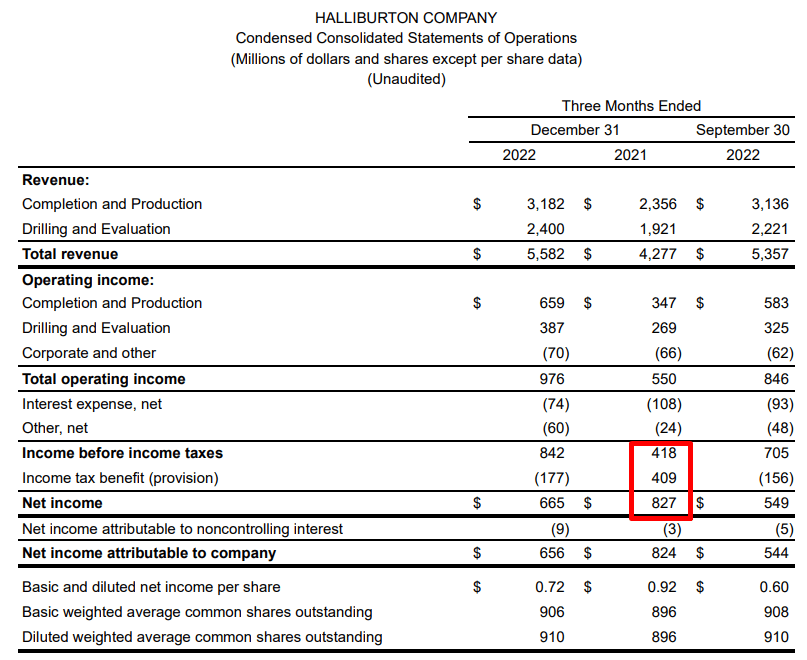

On 24 January 2023, Halliburton reported an adjusted 4Q22 net profit from continuing operations of $656 million or $0.72 per diluted share, up from $544 million or $0.60 per share in 3Q22. In terms of year-over-year (YoY) comparison, I think we should not be misled by the 4Q2021 bottom line coming in higher than the 4Q2022 figure, as the company utilized $409 million in tax benefits during the comparative period:

{kind=link}

To obtain a fair understanding of the YoY dynamics in terms of performance without that one-off tax benefit, I believe we should compare the operating margins which expanded significantly from 12.9% to 17.5%:

Author's calculations

Apart from increased operating margins, higher operating income reflected higher sales in both the Completion & Production (C&P) and Drilling & Evaluation (D&E) segments.

Author's calculations

In regards to disaggregation by geographic locations, three of them demonstrated strong growth except of Europe/Africa/CIS. The decline in one of the locations was primarily driven by the company's exit from Russia.

Author's calculations

Halliburton considers capital efficiency as its major priority which it strives to deliver by expanding digitalization and implementing new technologies. The company bets on its Halliburton 4.0 Digital Transformation program , especially its Well Construction 4.0 set of software which brings more value to customers by shortening drilling cycles via automation.

Thanks to strategic initiatives, HAL is being effective at using high crude oil price cycles by expanding its margins. We can see that operating margin grew even higher QoQ (December quarter) from 15.8% to 17.5%. Comparing to historical data on operating margin on the chart below, we can see that margins over the last two quarters are getting closer to levels which were demonstrated during previous high crude oil price cycles (2013-2014):

Full-year results

{kind=link}

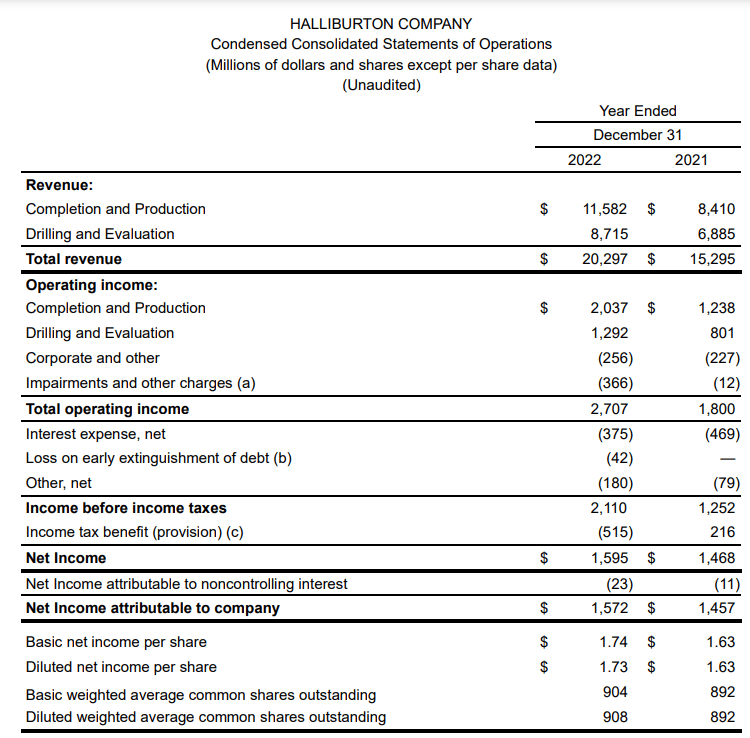

Full-year revenue was at $20.3 billion, which is 33% higher YoY. This increase comprised growth in both the C&P (up 38%) and D&E (up 27%) segments. Growth in revenue as well as improved efficiency enabled the company to significantly expand operating margins in both segments.

Author's calculations

The company's revenue in North America grew 51% in 2022 compared to 2021. International sales increased 20% for the full year. Strong revenue growth together with widening margins enabled Halliburton to increase dividends by 33% to 16 cents per share starting first quarter 2023.

Free cash flows

Halliburton demonstrated its ability to sustain various external shocks, like upstream companies' significant capital expenditure cuts as well as the COVID pandemic, mainly due to robust management. It is worth mentioning that HAL manufactures most of its equipment fleet which provides significant flexibility to increase or decrease capital expenditures based on market conditions.

The company is striving towards increasing capex efficiency, which enables it to strengthen its FCF profile. Historically, CAPEX as a percentage of revenue was in low double digits and the new reality for the company is 5-6% of revenue.

Halliburton

These measures at CAPEX optimization enabled the company to significantly improve its FCF margin from 4-5% in 2018 and 2019 to 10-11% in 2020-2021, and these years were not as good for oilfield companies as 2022 and beyond. Thus, during this favorable cycle for oilfield companies, we can reasonably expect FCF margin to increase to 15% in the worst case scenario.

Halliburton Valuation

Based on rather, in my opinion, conservative valuation assumptions I prepared a DCF model of HAL. Revenue growth is expected to be sustainable in the next years due to the crude oil supply/demand imbalance caused by the underinvestment by upstream companies (capital expenditures) that started from 2014. Thus, I firmly believe that oil and gas supply will remain tight, requiring multiple years of investment in CAPEX.

The level of my conviction is high and can be supported by several sources which are discussed and cited below.

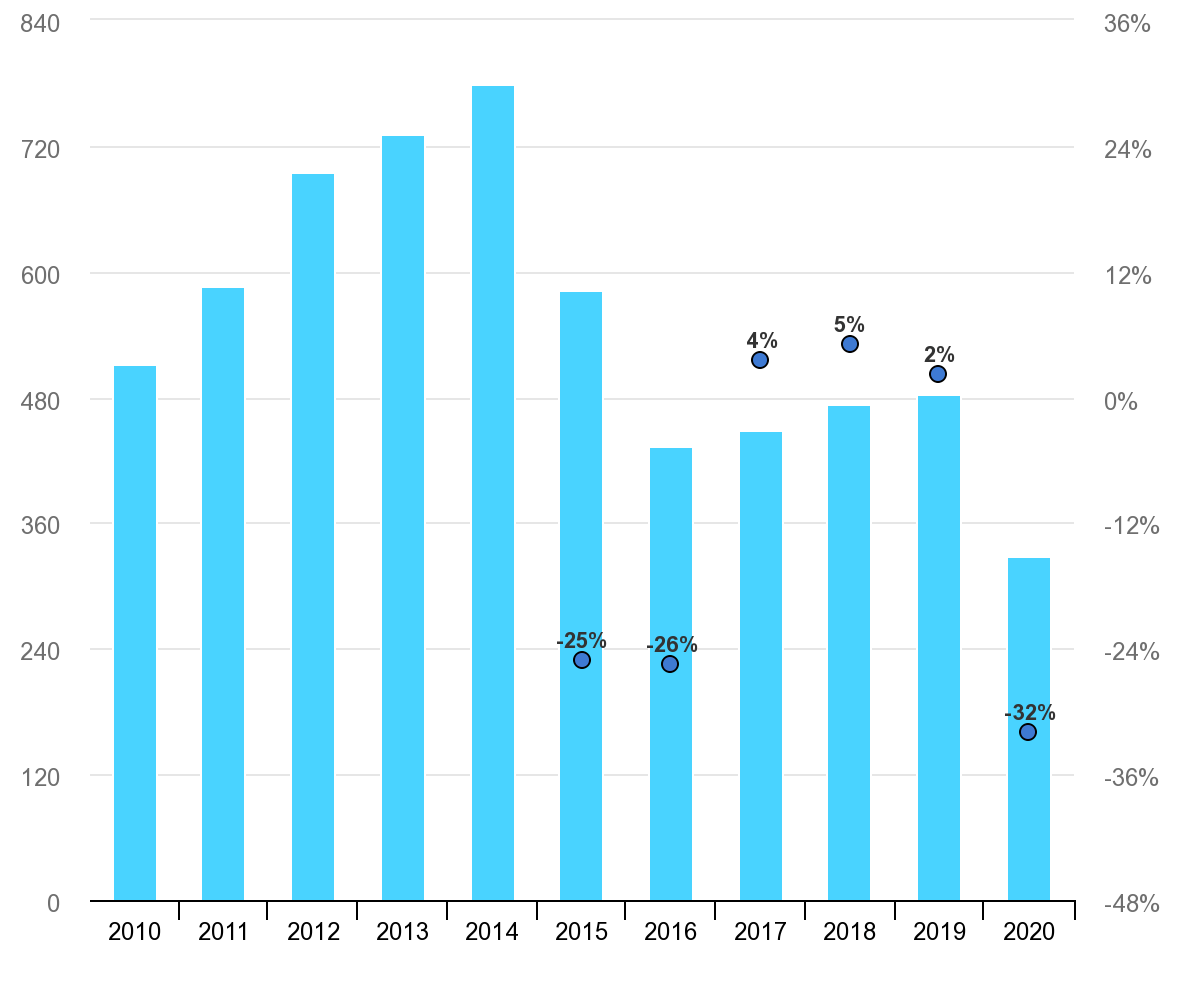

On the next graph you can see global investments in oil and gas upstream in nominal terms and percentage change from previous year between 2010 and 2020, amounts are in USD billions.

{kind=link}

In order to support growing crude oil demand, especially considering China's reopening of borders to travel, upstream capex should grow substantially. As JP Morgan's head of oil and gas research Christyan Malek said the bank had identified a $600 billion shortfall of upstream investment needed between 2021 and 2030 to meet what he called a "muted" view of global oil demand. He also said:

We've had upstream businesses' capex slashed to extreme levels in favor of low carbon. I like to call it the straightjacket, where you've got debt reduction, dividends and decarbonization essentially starving the industry of the capital we need

This factor, the underinvestment in oil and gas upstream was also discussed during the latest Abu Dhabi International Petroleum Exhibition & Conference (ADIPEC) which took place in late autumn last year.

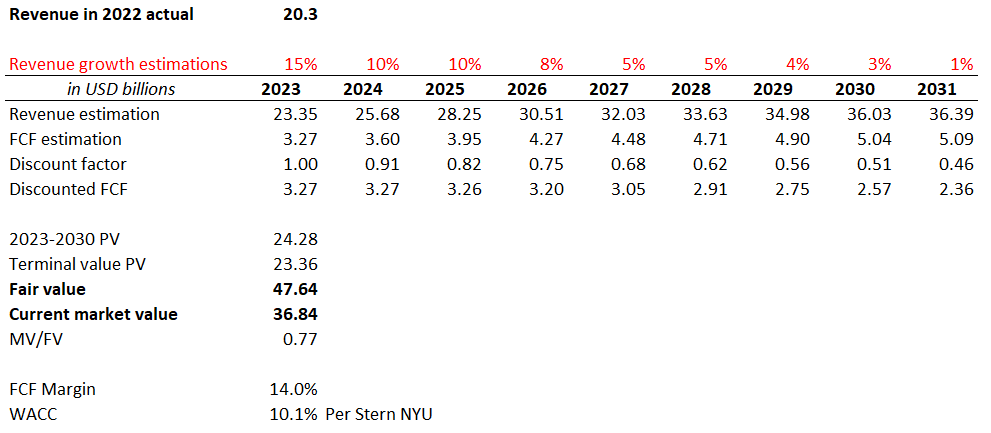

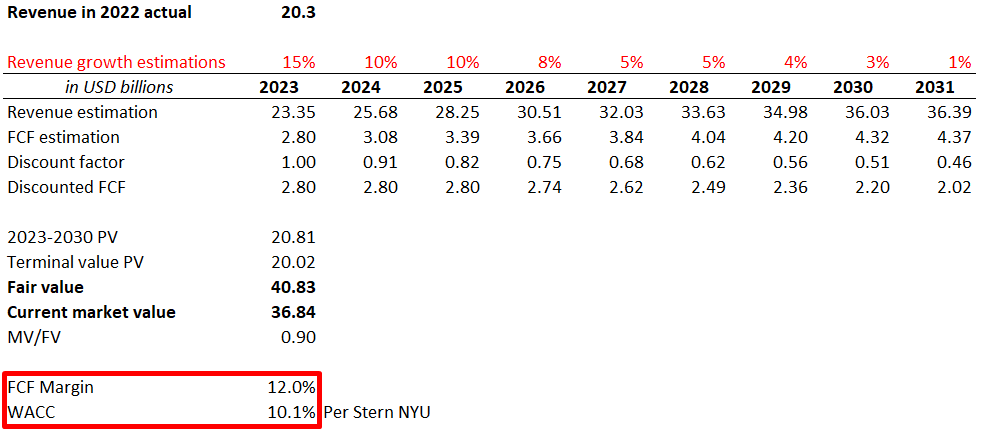

The DCF model assumes rather conservative 14% FCF margin (based on 2020-2022 historical averages adjusted for company's CAPEX optimization plans) and WACC at 10.1%. Revenue growth for the year 2023 is in line with Halliburton's expectations which were highlighted by Jeff Miller, the CEO, during last earnings call .

{kind=link}

We can see, based on the DCF model, that the company is trading at a 23% discount given rather conservative assumptions.

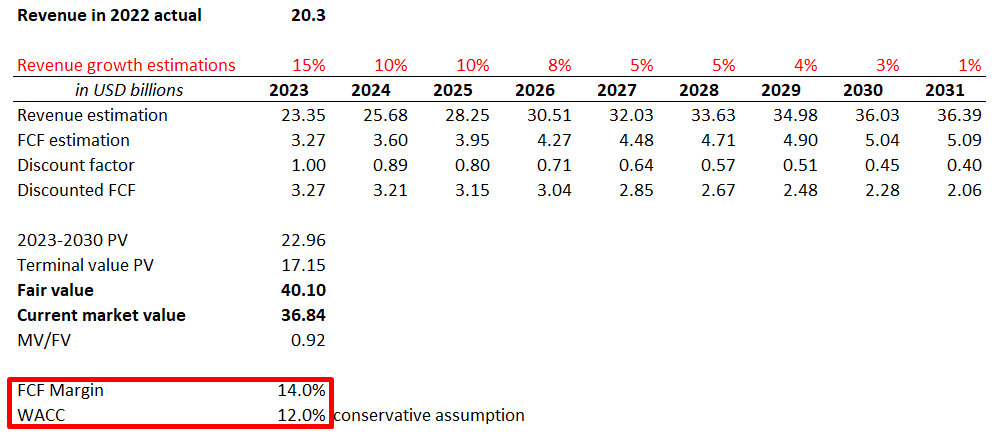

I have also made sensitivity check for the DCF in order to figure out how change in assumptions will affect the model. First, I implemented even more conservative FCF margin at 12% of revenue - DCF still demonstrates undervaluation of 10%:

{kind=link}

Second, I applied a higher WACC to the DCF of 12% which still demonstrates an undervaluation of 8%:

{kind=link}

In order to cross-check reasonableness of the fair value figured out in my DCF, we can also compare Halliburton's current Price/FCF ratio to the latest oil and gas cycle peaks.

From the above chart we can see that during previous oil and gas cycles HAL has been trading at more generous multiples than it is experiencing now.

Potential risks

Halliburton is subject to the cyclicality which is inherent to oil and gas markets, which makes company's revenue sources volatile. Moreover, the firm is dependent on well operator's capital investment decision making and their budgets. Halliburton is also heavily exposed to North American shale market, which also puts additional risks to revenue growth perspectives.

Obviously, as an oilfield service company, Halliburton is exposed to a range of environmental, social, and governance risk. The company is exposed to liabilities associated with wellsite emissions, incidents, ecological risks etc. Emergency during production processes could result in serious employee injury-even death-as well as environmental damage, all of which could subject Halliburton to lawsuits, penalties and regulatory charges. Such incidents also disrupt operations, which will result in idle time and potentially lost hundreds of thousands of dollars per day. This also might result in reputational damage for Halliburton and a given incident could make it difficult for Halliburton to win contracts later.

Surely, for all above risks, the degree of liability depends on numerous factors, such as contract terms, and service firms risks are usually limited by contracts terms and conditions, but the risk remains.

Bottom line

To conclude, Halliburton possesses strong positions to benefit from current high crude oil prices cycle which is expected to last next several years due to underinvestment in oil and gas upstream CAPEX in recent years. The company was one of the top-performing oilfield service firms in 2022 which share price appreciated more than 70% during the calendar year. In spite of the massive last year rally, the DCF model and different sensitivity tests suggest that the company is still a buy given an upside potential with dividends secured and growing.

For further details see:

Halliburton: Still Undervalued