HAL - Halliburton: Is This A Buy After The OPEC+ Production Cuts?

Summary

- Halliburton is writing some major tailwinds.

- OPEC+ production cuts will likely lift the stock further.

- The company may be going into a fantastic 2 to 3-year period following the recent debt retirement.

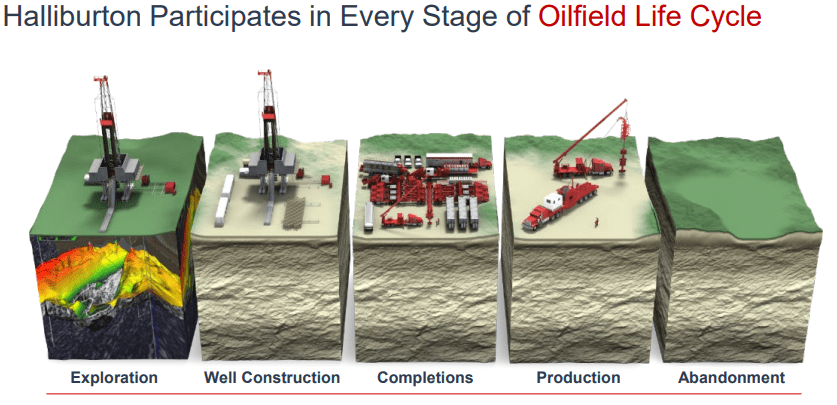

Halliburton Company ( HAL ) is an American oil infrastructure company that was established in 1919 in Duncan, Oklahoma. It is often mistaken for an oil-producing company, but Halliburton is a global leader in the oilfield services industry. Its services assist oil producers during every stage of the oilfield lifecycle, including exploration, well construction, completion & production, and abandonment.

{kind=link}

The stock has long been a major player in the American energy industry and has been a steady performer over the past year despite major volatility in both equities and oil. Much of this volatility has been brought about by tensions between Ukraine and Russia, prompting sanctions that have greatly limited supply to the European markets. This caused upward pressure on oil prices.

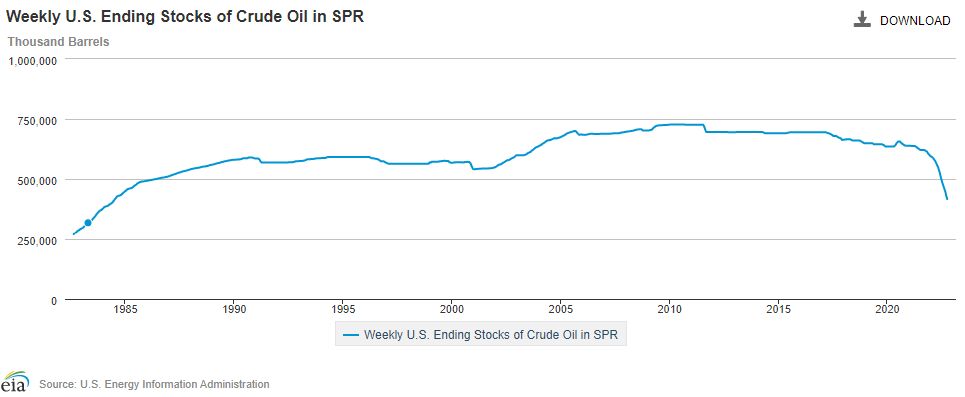

The strong appreciation of oil prices lifted Halliburton stock from the pandemic lows, but the recovery has since stalled due to a retreat in oil prices. This is largely due to the Biden administration's decision to utilize the Strategic Petroleum Reserve ("SPR") to soften energy prices to protect American households from soaring energy costs.

{kind=link}

Now, with the reserves at historic lows and the recent decision by OPEC+ to cut production ahead of winter, which usually sees oil at seasonal highs, the conditions are set for a strong performance from energy stocks over the next few months.

Company Outlook

We can think of Halliburton as a pick-and-shovel company for the global oil industry. What exactly does this mean? It means that the company provides essential services to oil producers through its Energy Services Group, or ESG. Halliburton focuses on assisting with drilling and evaluation, overall project management, completion, and production of oil. It is a leading software provider that is enhancing the company's digital presence in a new age of oil production. This software also provides the company with a nice source of recurring revenues and the requirement of further tech support for its customers.

The company also offers the innovative iCruise smart driller, which reduces the need for human capital as well as the influence of human error. Halliburton also produces the EarthStar deep drilling sensor, which provides a unique 3D view of oil wells up to 200 feet around. There is also its promising Halliburton Enterprise 4.0 software system that uses cloud solutions to process workflows and analyze data. It also includes a suite of smart tools to automate processes and improve the overall efficiency of any oil-producing operations. Recently, Halliburton produced the first ever all-electric oil fracking site, with the first true 5,000 hp pump.

For those who followed the company in the past, you will already be familiar with its transition from an oil field infrastructure builder to a services provider. It is a similar transition from hardware to software that many tech companies make. It has also established Halliburton's global presence in more than 70 different countries, and it is the leading services provider in the global oil market. The company has heavy revenue exposure to North America and the Middle East/Asia regions.

{kind=link}

One might call this risky, but when you consider the recent disruptions in energy markets and the fact that the world is moving past the Covid-19 pandemic, it's safe to say that there will be healthy demand for oil regardless of geopolitical tensions.

Earnings Download

In the recent Q2 earnings report , the company reported a net income of roughly $109 million, or $0.12 per share with an adjusted net income of roughly $0.49 per diluted share, excluding impairment charges. This is coming from a strong 18% sequential increase in revenue for the quarter. The main focus was the strong completion and production revenue which increase 24% and was largely attributable to strong performance in North America on international markets, which help offset a seasonal slowdown in software sales.

Management was incredibly bullish about the state of the energy market, which is understandable. The market is in a fantastic place right now, resulting in some really strong revenue performances. Despite this fact, investors shouldn't get carried away with cash flow expectations. We often want to see dividend hikes in situations like this, but it is important to remember that Halliburton is in the middle of redeeming senior notes , which should reduce the company's cash interest expense over the long term and strengthen the balance sheet provided demand remains elevated.

{kind=link}

Nevertheless, Halliburton is still a cash flow machine. We can see clear room for long-term improvements holding commodity prices constant due to the tactical decisions the leadership team is making today.

Halliburton

The company reports earnings next on October 25. I am looking forward to some strong performances in North America. I'm interested in hearing about the company's efforts to diversify sources as energy security becomes a major talking point for most governments. The main thing is the outlook on energy prices going into what could be a very cold winter. Leadership has already mentioned that there have been strong sales in mind in most segments, so I would not expect any major updates there.

Halliburton also recently sold its Russia oil operations, and it will be interesting to see what effect, if any, that has had on performance and whole the leadership sees its relationship with Russia and Ukraine going forward. All in all, this should be a fairly straightforward report apart from the Russia issue.

HAL Valuation and Forward-Looking Commentary

As we discussed earlier, energy stocks have been on quite a run lately. Halliburton trades at comparable ranges to its peers with respect to P/S ratios and is about the middle of the pack when considering P/E multiples.

The interesting thing about energy stocks is that the underlying pricing dynamics of the commodity greatly influence valuations across the board. That said, there is a seasonal component to price action in oil, and they are also tailwinds associated with the recent OPEC+ production cuts and tensions in Ukraine. This is setting up for an oil run during the winter months, which will likely lift the stock further. Depending on the actions of Russia and OPEC+, we may see elevated prices for some time beyond the winter months. Still, the OPEC+ nations tend to have differing opinions on production levels, and it is not rare to see some producers break ranks and hike production to help fund their economies. Iraq has already mentioned that they cannot afford the production cuts, and we may see other low-cost producers follow suit in a bid to capitalize on the elevated prices even as higher-cost producers attempt to lift prices further. It's definitely a sensitive situation that will continue to evolve over time, but I think investors can feel pretty confident about the stability of oil prices going into H1 2022.

Halliburton also pays investors to wait. With a decent 1.95% dividend yield, an impressive 20.75% payout ratio, and a strong history of returning cash to shareholders, the more conservative dividend aristocrats have some cash flow to look forward to. We can see below that Halliburton has more generous competition in the space, but it is certainly a viable option.

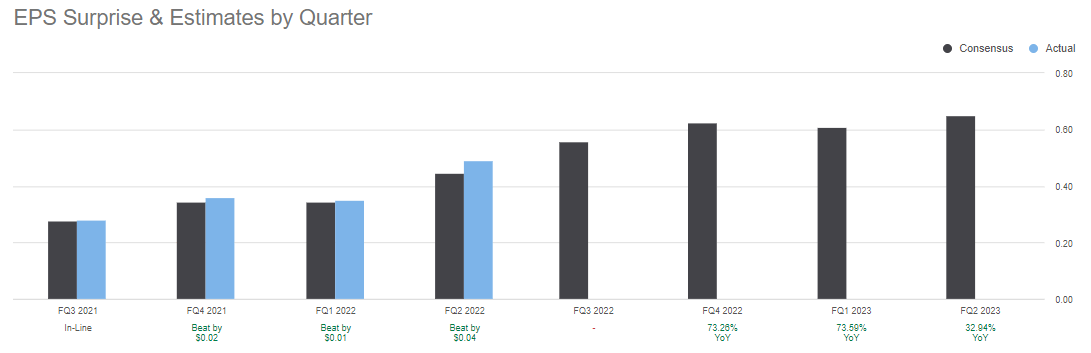

We can also see that the management team does a good job delivering to EPS estimates. The company has beaten or matched in each of the last four reports. It is also important to note that EPS trends are expected to be favorable over the coming quarters, which is consistent with the seasonal theme and underlying tailwinds discussed earlier.

{kind=link}

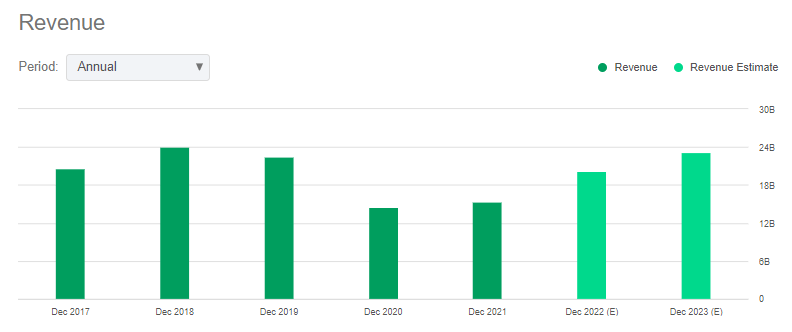

Revenue trends also look favorable, as one might expect. We should be heading into a good 2 to 3-year cycle for energy opportunities like Halliburton.

{kind=link}

The Takeaway

We can see clear tailwinds for energy. Some secular trends suggest the adoption of renewables is well underway, but for the foreseeable future the world will likely be relying on oil, and Halliburton is simply one of the biggest players in the game. With its transition from infrastructure construction to oil field services and software solutions, Halliburton has likely extended its dominance in the global oil industry. It is a high cash-flow business model with global operations and a long history of rewarding shareholders. We will likely call current levels a bargain in the next 6 to 12 months. I rate Halliburton as a buy.

For further details see:

Halliburton: Is This A Buy After The OPEC+ Production Cuts?