HLMAF - Halma: Great Company But Continues To Look Overvalued

2023-11-20 22:09:44 ET

Summary

- Halma has a strong track record of dividend growth and operates in a defensive business area.

- The company expects good organic revenue growth despite negative market conditions in Asia Pacific.

- Halma's annual dividend has increased by at least 5% for 44 consecutive years, but its high valuation and growing net debt are concerns.

British-based alarm specialist Halma ( HLMAF ) has a long track record of dividend growth thanks to an attractive business niche and growth both organically and through acquisition.

I last covered Halma in my July 2022 “sell” piece Halma: Still Great But Still Pricey , since when the shares have declined 13%.

Business Continues to Do Well

The business model here, described in previous Halma pieces on SA including my own, remains attractive. I do expect a softer economy to mean some customers squeeze spending, but in broad terms safety equipment like Halma sells is a highly defensive business area in which to operate.

In its most recent trading statement , in September, the business pointed to “varied market conditions”. It said performance in Asia Pacific has been negative, for example, driven by declines in China. However, it said for the first half it expects “good organic constant currency revenue growth.” One risk is the appreciation of sterling, which as the company has an international business reporting in sterling could hurt its results.

Three acquisitions were made in the first half of the year, for a maximum consideration of £80m, meaning the company’s acquisitive strategy continues. Essentially, it is more of the same at Halma as it continues to plough a furrow that has proven so successful for it over the long term.

Last week the company issued its interim results , which it said showed record revenues and profits. Revenues grew in all markets and all regions except Asia-Pacific.

{kind=link}

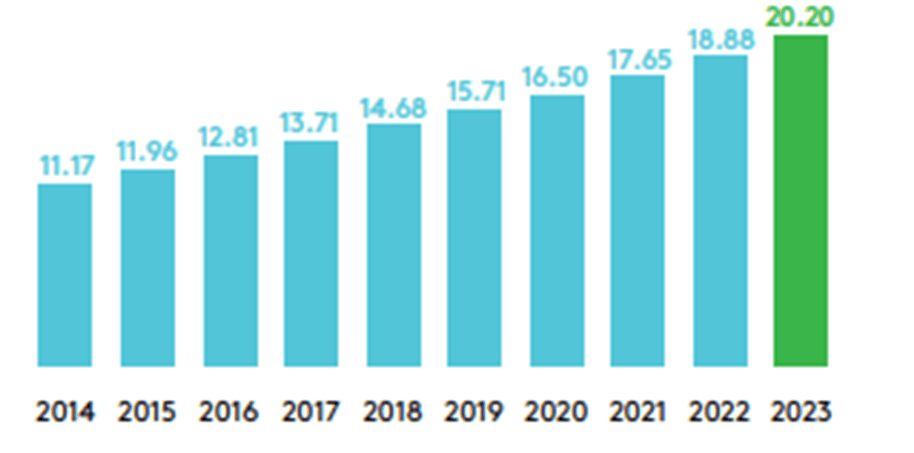

Dividend is set to Keep Growing

One of the best-known features of the Halma investment case is its long history of annual dividend increases. It has been hiked annually by at least 5% for 44 years on the trot. Last year saw the dividend grow by 7%. At the interim stage last week, the interim dividend was also boosted 7%.

Chart: Annual dividend per share (pence)

{kind=link}

If I was running a company with 44 years of 5%+ annual dividend increases, I would work hell for leather to keep up the track record. So I think it is fair to expect ongoing annual dividend increases of at least 5%.

Last year, free cash flow was £10.1m after spending £73.3m on dividends. But while operating cash flow came in nicely at £258.0m, investing cash outflows totalled £368.9m. That makes sense for an acquisitive company - £320.1m was spent on acquiring companies (net of cash acquired). But the financing cashflows also show the company’s sizeable borrowing (largely offset by repaying borrowings).

{kind=link}

Debt rose sharply last year. Net debt of continuing operations rose to £596.7m from £274.8m the year before. By the end of this year's first half, it was up to £618.8m.

If the company is to keep growing dividends at the current rate while borrowing substantially (albeit for growth), I expect that to mean net debt will likely grow over time. Let’s have a look at the past five years.

| All figures in £m |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| 2023 |

| Net cash inflow from operating activities |

| 219 |

| 255.5 |

| 277.6 |

| 237.4 |

| 258.0 |

| Net cash from/(used in) investing activities |

| -104 |

| -276.4 |

| -64.2 |

| -134.7 |

| -368.9 |

| Net cash from/(used in) financing activities |

| -113.6 |

| 53.7 |

| -183.5 |

| -81.9 |

| 121 |

| Net free cashflow |

| 1.4 |

| 32.8 |

| 29.9 |

| 20.8 |

| 10.1 |

| Net debt |

| 181.7 |

| 375.3 |

| 256.2 |

| 274.8 |

| 596.7 |

Chart compiled by author using data from company annual reports

There is consistently free cash flow left over even after paying the growing dividend. But net debt has grown sharply during the past five-year period. If the company keeps borrowing to fund acquisitions, the dividend could keep growing but so too could net debt. That is what I see as most likely.

But, looking at the juggling of borrowing in the financing cashflows, I would say that ongoing annual dividend increases at the company look likely to continue because they are key to the investment case and it is in management’s interest to find a way to make them happen, rather than because Halma is a free cash flow gusher even after financing and investing costs that has so much cash it could comfortably keep on growing the dividends even if operating cash flows do not grow at the same rate.

It’s worth adding that, due to the share price, the yield is only 1% despite those decades of dividend hikes.

Valuation continues to look high

Despite declining since my last piece, I continue to see the Halma share price as too high.

Yes, it’s a solid company with a large moat, consistent profitability, and an attractive policy of annual dividend increases. The choice to focus on alarms means customers have a clear and often essential need, quality matters and they are willing to pay a premium price. That gives Halma a competitive advantage that helps give it pricing power.

But it trades on a price-to-earnings ratio of 32. That looks unreasonably high to me. It does not have very similar competitors that might allow a direct comparison, but the Halma P/E ratio is slightly over double the average for a FTSE 100 company at the moment.

I think a fairer P/E ratio for a company of this quality would be 15 to 20 max. Even then, I’d like to see more consistency in financial growth beyond just dividends. Accordingly, I maintain my “sell” rating. That is all about the valuation not the undoubted strength of the underlying business. If the price falls considerably, or earnings move up very sharply, I would consider changing my rating.

For further details see:

Halma: Great Company But Continues To Look Overvalued