HALMY - Halma: Smart M&A Policy But Still Not Cheap

Summary

- Halma is a UK-based holding company, owning and operating close to 50 companies.

- The share price is down by almost 30% since my previous article, but that doesn't make the company cheap.

- I like the M&A policy as Halma continues to acquire companies with a specific focus on the profitability of the acquirees.

- I expect the second half of the year to be better as pension payments and non-recurring acquisition expenses should be down.

- Halma will move to a pension surplus and that will likely result in reduced top-up payments into the pension fund.

Introduction

About 1.5 years ago, I thought Halma ( HLMAF ) ( HALMY ) was too expensive despite its resilient business model. Now, 1.5 years later and with a share price that's currently trading almost 30% lower than where it was at in July last year, I'm starting to warm up to Halma at its current valuation.

Halma is some sort of "holding company" as it owns 45 different companies which it has grouped into three sectors: Safety Technologies, Environmental & Analysis, and Medical Technologies. All divisions have one thing in common: The operating margin of all of them was approximately 25% in the past financial year. As I won't discuss every single company in detail, I'd like to refer you to the company's website, which provides a detailed breakdown of all 45 .

{kind=link}

Halma has its primary listing on the London Stock Exchange, where it's trading with HLMA as its ticker symbol . The average daily volume exceeds 1.2 million shares. As there are approximately 378 million shares outstanding, the current market capitalization is approximately 8.1B GBP.

A strong start of the current financial year

Halma's revenue increased pretty substantially in the first half of the current financial year (which ended on Sept. 30, Halma's financial year ends on March 31). The total revenue came in at 875.5M GBP resulting in an operating profit of 151.7M GBP after deducting about 6.2M in adjustments. According to the footnotes to the financial statements, the adjustments were mainly related to the amortization of acquired intangibles while the recently completed acquisitions also had a cost associated with them. As such, the entire 26.2M GBP in "adjustments" is either non-cash or non-recurring.

{kind=link}

This also means the reported 15.5M GBP in pre-tax income is a very conservative metric as the pre-tax income before these adjustments was approximately 172M GBP. The net income was 114.8M GBP on a reported basis, which included a 0.2M GBP loss attributable to minority interests. As you can see below, the net income attributable to Halma was 115M GBP for an EPS of 30.39 pence.

{kind=link}

The EPS excluding the aforementioned adjustments would have been 35.65 pence per share.

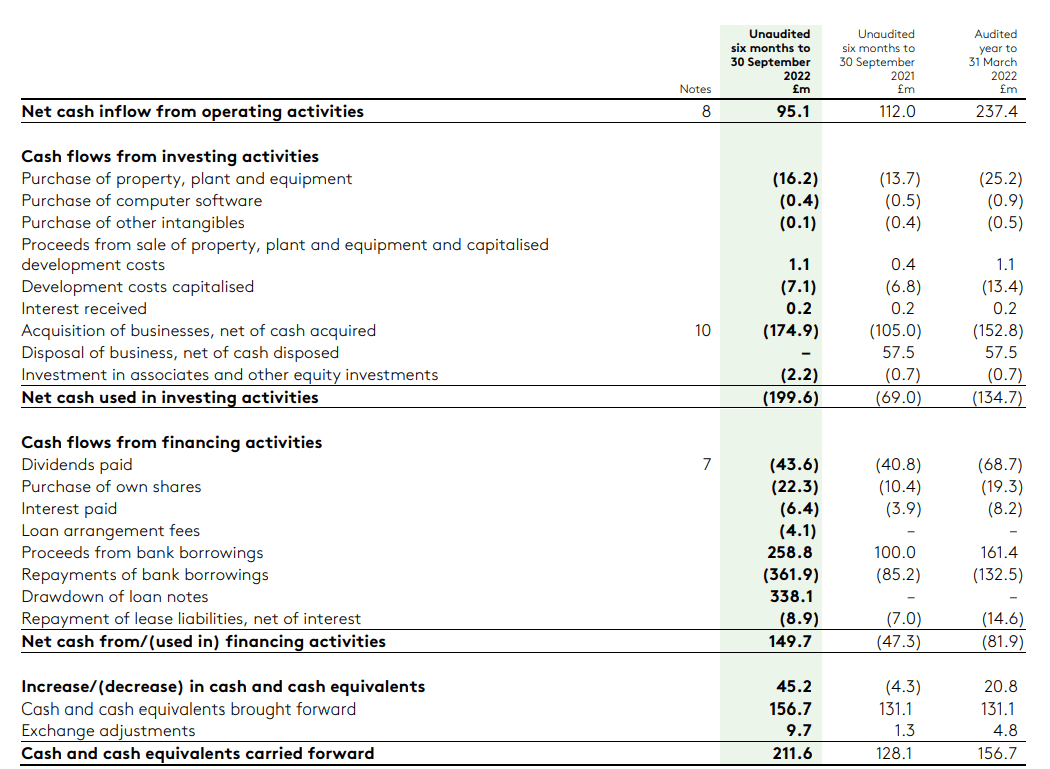

As there are quite a bit of non-cash items, I wanted to see how the cash flow statement worked out. The image below shows the starting point was the 95.1M GBP "net cash inflow from operating activities."

{kind=link}

Needless to say, this isn't sufficient information but, fortunately, the referral to footnote 8 included a detailed breakdown of how that 95.1M GBP result was reached.

{kind=link}

We see the operating cash flow before taxes and before changes in the working capital was 198.6M GBP. We also see the company paid 31.2M GBP in taxes, so the adjusted operating cash flow before working capital changes was 167.5M GBP.

We should still deduct the interest payments (6.4M GBP) and the 8.9M GBP in lease payments. I'm ignoring the 4.1M GBP loan arrangement fee as that clearly is a non-recurring item, and I'm more interested in the "normalized" cash flow. The operating cash flow was 152.2M GBP on an adjusted basis and after deducting the just under 24M GBP in total capex (including capitalized development costs), the underlying free cash flow result was just over 128M GBP for an FCF per share of just under 34 pence. Keep in mind the total capex + lease payments exceeded the total depreciation, so Halma is investing at a slightly higher pace than it's depreciating its assets. The full-year capex guidance is 34M GBP, while Halma continues to pay 14.6M GBP into the pension fund this year (of which 8.7M GBP was recorded in the first half of this year). I think this cash outflow will fall away soon as the pension fund now has a small surplus and no top-up payments will be required. I expect Halma to talk to the trustee again to reduce and/or cancel future payments. Additionally, the annual report clearly states that Halma is entitled to the surplus when it winds up the defined benefit schemes.

Additionally, two recent acquisitions which were completed during the first half of the year will start to contribute as well.

{kind=link}

The net debt increased due to an acquisition

Halma indeed uses the majority of its free cash flow to pursue M&A and that still is the main growth engine for the company. The company closed two acquisitions during the first half of the year.

The first acquisition was the 39M GBP Deep Trekker acquisition, a manufacturer of remotely operated underwater robots used for inspection, surveying and maintenance. The pre-tax income on the approximately 12M GBP revenue exceeds Halma's 18-22% threshold , and according to a footnote in the financial statements, Deep Trekker contributed 0.6M GBP in after-tax profit during the first half of the year. This would have been approximately 0.1M GBP higher if Deep Trekker had started contributing from day 1.

The second acquisition was the largest acquisition as Halma forked over 138M GBP in cash to acquire IZI Medical Products, a designer, manufacturer and distributor of medical devices. As this acquisition only closed on Sept. 30, this purchase didn't contribute a single British Pound to the H1 results. Halma estimates the normalized net income would have been boosted by 3M GBP of it would have been included, so we can definitely expect an uptick in the second half of this year. Halma also mentioned the "return on sales" (the pre-tax profit margin) is "substantially higher" than the 18-22% it targets.

{kind=link}

And subsequent to the end of the semester, Halma acquired WEETECH Holding, a designer and manufacturer of safety-critical electrical testing technology used in avionics, rail, aerospace, and the automotive sector. Halma paid 50M GBP for this acquisition and based on the known revenue (18M GBP) and the return on sales of just over 22%, Halma appears to have purchased this company for 12-13 times the pre-tax income.

Investment thesis

Halma appears expensive from pretty much every single angle you look at. The free cash flow yield is still less than 4%, the company is trading at about 30 times earnings and the EV/EBITDA ratio is firmly above 15, given the enterprise value of in excess of 8.5B GBP and an EBITDA just north of 400M GBP.

That being said, Halma also has a few elements working in its favor: The pension payments should stop, the two most recent acquisitions will start contributing from this semester on, and I like the M&A strategy with a strong focus on profitability of the bolt-on additions to its empire.

Taking all these things into consideration, I'm still not a buyer of Halma at the current share price. I like the company's approach, and perhaps it will never get really cheap. But although the share price has lost about 30%, it still isn't in bargain territory. I will continue to keep an eye on its developments, but I remain on the sidelines for now.

For further details see:

Halma: Smart M&A Policy But Still Not Cheap