HALMY - Halma Stock: What Happened During The Great Recession

2023-05-01 17:00:12 ET

Summary

- Halma plc is a relatively unknown but very successful global company based in the United Kingdom.

- In this article, I take a look at Halma's performance in 2022 and examine whether the company's strategy is delivering healthy results even in such a difficult time.

- Given the rather bleak economic outlook in the U.K. and the potential for a global recession, I also look at the robustness of Halma's earnings and cash flow under stress.

- While a comparison with the Great Recession may seem overly pessimistic, a look at Halma's performance at that time provides surprising results.

- Nonetheless, I highlight why those investing in Halma today may be in for a (temporary) headache.

Introduction

There is no denying that conglomerate Halma plc ( HLMAF , HALMY ) is a formidable business. It is very profitable and highly diversified, and its management is conservative, forward-looking and shareholder-friendly. I first covered Halma stock back in February 2022 , when the bear market was just getting started. Considering the stock is 28% down from its all-time high in sterling terms, Halma could represent a solid value opportunity today. At the same time, investors should always remember the perils of recency bias. After all, the stock still trades at nearly 30 times 2022 adjusted earnings.

In this update, I'll take a look at how well the company did in 2022, especially against a backdrop of high inflation, ongoing supply chain issues, and a bleak economic outlook. In addition, I will analyze how Halma performed during the Great Recession, as this period provides a blueprint - perhaps too pessimistic - for the economic challenges ahead. I will draw a conclusion as to whether the stock is a good investment at its current, arguably premium valuation, or whether investors are merely demanding safety at any price.

Halma plc – Earnings Update

Halma's fiscal 2023 ended in March and results will be released in June. The company issued a trading update in March 2023 confirming pre-tax profit of around £360 million, up 14% year-over-year. I think this is an impeccable performance, as the company has already increased its profit at the same rate in fiscal 2022 (Figure 1). While the weaker pound is a bitter pill to swallow for U.S.-based investors (Halma's valuation and actual dividend payout decline as the U.S. dollar appreciates), it acts as a tailwind for corporate earnings. This is hardly surprising given that Halma generated more than 80% of its fiscal 2022 revenues outside the U.K., but reassuring given the rather bleak economic outlook for the U.K. economy.

{kind=link}

Figure 1: Halma plc’s [HLMAF, HALMY] historical adjusted earnings before taxes (own work, based on the company’s fiscal 2016 to fiscal 2022 earnings releases and the March 2023 trading update)

Those invested in or interested in Halma are used to the fact that management has a knack for making profitable acquisitions. In fiscal 2023, the company made six acquisitions and spent a record total of £264 million. Deep Trekker (Canada) is a market leader in underwater robots used for inspection, maintenance and other tasks. IZI Medical Products (U.S.) develops and manufactures medical consumables used by radiologists and surgeons. WEETECH Holding (Germany) develops and manufactures equipment for integrity testing of a variety of electrical systems. Thermocable (U.K.) is a manufacturer of linear heat detectors, which was acquired to support Halma's Apollo fire alarm segment. Zone Green (U.K.) was acquired as a bolt-on for the Sentric Interlock segment. Finally, the company acquired Ocean Insight from Rigaku (international), a company focused on light-based detection of aluminum scrap for recycling purposes.

I realize that these acquisitions sound like a lack of focus, but I refer those unfamiliar with Halma's organizational structure to my original article, as well as to Halma's business unit report (p. 44 et seq., fiscal 2022 annual report ). This detailed report does an excellent job of highlighting the many tailwinds Halma is experiencing in the current environment, focusing on renewable energy, the increasing importance of security, sensors, automation and healthcare. The company is the market leader in many of the segments it serves. Another point that should be appreciated is the fact that Halma's operations are spread across the globe, which dampens the impact from exchange rate movements. Given that management regularly makes acquisitions (and to some extent divestitures) and does not accumulate excessive cash on the balance sheet, I would not overstate the risk of foreign acquisitions becoming excessively expensive due to a weaker pound.

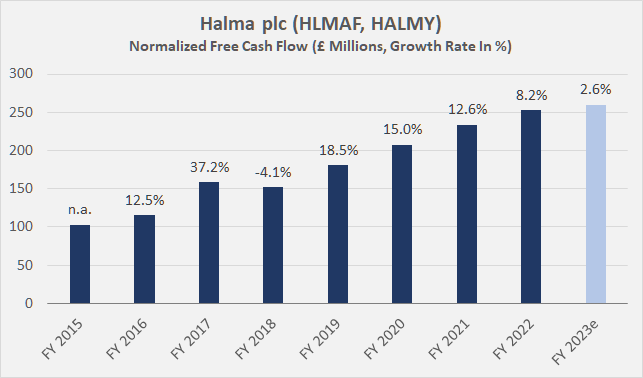

Of course, successful growth through acquisitions is difficult, especially for a conglomerate operating in a large number of business areas. However, Halma continues to deliver, best demonstrated by its very reliable return on invested capital, notably including goodwill (ROIC, Figure 2). Granted, earnings are relatively easy to manage, so the reliable ROIC, same as solid earnings CAGR of over 11% since fiscal 2015 should be taken with a grain of salt. However, when free cash flow ((FCF)) is taken into account and normalized for working capital movements and stock-based compensation, Halma shines equally. The CAGR of the company's normalized FCF actually outpaced its earnings CAGR at over 12% since fiscal 2015. Note that the deceleration in growth I expect in fiscal 2023 is due to the normalization of modest working capital-related impacts.

Halma should not be compared to the many companies that continue to struggle with supply chain issues and have seen their operating cash flow drop dramatically in 2021 and sometimes even in 2022. To be fair, however, it should be added that Halma's free cash flow was quite lackluster in the first half of fiscal 2023 due to working capital effects, but management has already indicated that cash generation was very strong in the second half (p. 2, March 2023 trading update).

At the same time, the stable gross margin of just over 50% confirms the company's pricing power and the moat that results from high switching costs and Halma's market-leading position in many segments. As I pointed out in my original article, the company supplies a large number of products needed to meet certain regulatory requirements. This leads to high customer loyalty, but also to short replacement cycles.

{kind=link}

Figure 2: Halma plc’s [HLMAF, HALMY] historical return on invested capital (own work, based on the company’s fiscal 2016 to fiscal 2022 earnings releases, annual reports, fiscal 2023 half-year report, March 2023 trading update and own estimates)

{kind=link}

Figure 3: Halma plc’s [HLMAF, HALMY] historical normalized free cash flow (own work, based on the company’s fiscal 2014 to fiscal 2022 annual reports, fiscal 2023 half-year report, March 2023 trading update and own estimates)

More or less irrespective of the determined cost of capital (anything above 9% seems excessive to me for such a high-quality company), Halma routinely continues to generate solid shareholder value. While a weighted-average cost of capital ((WACC)) of 9% sounds high at first, it should be remembered that Halma is largely equity financed. Using fiscal 2023 half year results, the equity portion of the WACC calculation accounts for more than 92%. At the end of September, Halma had gross debt of only £713 million, while its current market capitalization is about £8.7 billion.

Speaking of which, Halma's balance sheet is always a pleasure to look at. Granted, goodwill is the largest asset on the balance sheet, which is to be expected for a company that focuses on growth through acquisitions. Tangible equity is effectively zero, but I think it would be overly conservative to "write off" goodwill and other intangible assets. Halma's management has demonstrated a knack for profitable and disciplined acquisitions over several decades while maintaining a very conservative balance sheet.

The company's debt is unrated because it consists mostly of unsecured bank loans (p. 243, fiscal 2022 annual report ). The weighted-average interest rate on Halma's gross debt was 1.90% in 2022, a decrease of 42 basis points from the previous year. This translates to an interest coverage ratio of about 30 times normalized FCF before interest - it doesn't get much better than that. While the company's interest expense will certainly increase as a result of rising interest rates, I would not over-interpret this aspect due to the low level of absolute debt. As mentioned earlier, Halma's gross debt at the end of September 2022 was £713 million, including lease liabilities. Net of cash and cash equivalents, the remaining £500 million translates to about two times normalized free cash flow. This means that the company could hypothetically repay all of its interest-bearing debt within two years if it suspended the dividend.

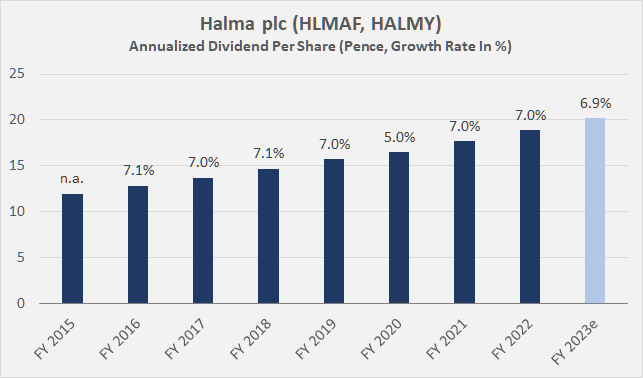

That said, the dividend cost of £70 million annually (current payout ratio <30%) leaves ample room for growth, even in the event of a prolonged recession (see next section). Finally, the forward-looking and conservative nature of Halma's management is also evident in the company's dividend growth track record. Annual dividend increases of 7% are the norm (Figure 4), and based on the interim dividend for fiscal 2023 (Halma pays dividends in 40/60 installments), yet another 7% increase can be expected for the final dividend. Even in fiscal 2020, at the height of the pandemic, management was true to its word and proposed a healthy 5% dividend increase. As a result, the increase in fiscal 2023 marks the 44 th consecutive year of dividend growth of at least 5% for Halma (p. 15, fiscal 2022 annual report).

Of course, it is important to remember that Halma's dividend is only a small part of its total return, given its current yield of 0.9%. As a result, I view Halma stock as a multi-generational dividend growth stock, with most of the current return coming from capital gains. Although I am a dividend-oriented investor, I find the fairly low dividend completely acceptable due to management's excellent capital allocation skills.

{kind=link}

Figure 4: Halma plc’s [HLMAF, HALMY] historical dividend payout on a per-share basis (own work, based on the company’s website: www.halma.com/investors/shareholder-information/dividend-history)

Performance Of Halma plc Stock During The Great Recession

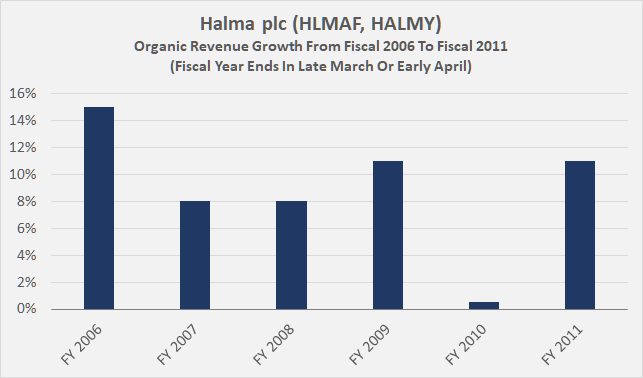

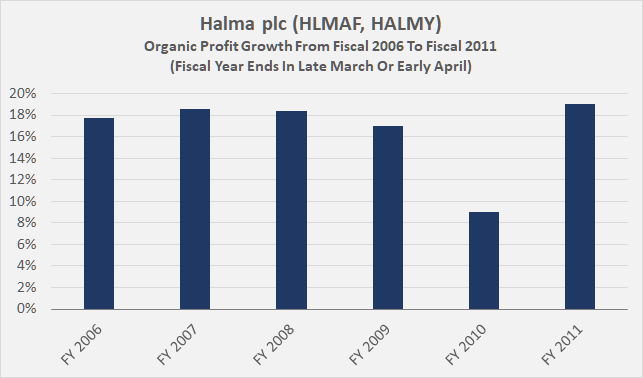

According to the company's fiscal 2007 financial statements , Halma generates revenues of £354 million in fiscal 2007, representing 14% year-over-year growth - a similar rate to today. However, it is important to consider Halma's growth through acquisitions strategy when evaluating its performance during the Great Recession. Adjusted for acquisitions, sales growth in fiscal 2007 was approximately 8%. The company maintained or exceeded 8% organic revenue growth in subsequent years, but in fiscal 2010 (which ended April 3), growth fell to 0.5% (Figure 5). Considering Halma's industrial exposure, I believe this is a phenomenal result and underscores the unwavering demand for the company's products. In addition, the company managed to deliver organic earnings growth of 9% this year - very strong indeed, but less than half of the growth Halma investors were used to in previous years (Figure 6). The recovery in fiscal 2011 was solid - with organic revenue and profit growth of 11% and 19%, respectively.

{kind=link}

Figure 5: Halma plc’s [HLMAF, HALMY] historical organic revenue growth (own work, based on the company’s fiscal 2006 to fiscal 2011 annual reports)

{kind=link}

Figure 6: Halma plc’s [HLMAF, HALMY] historical organic profit growth (own work, based on the company’s fiscal 2006 to fiscal 2011 financial data)

The company also performed remarkably well in terms of free cash flow. Since working capital data for the years prior to fiscal 2007 are no longer available online, I am unable to assess the company's performance well before the Great Recession. However, considering that fiscal 2007 ended March 31, the data should provide a good enough view of pre-recession conditions. In fiscal 2008, normalized free cash flow growth was about 2% year-over-year. This is likely due in part to working capital-related effects, as Halma's unadjusted free cash flow margin was 10.9% in fiscal 2008, down 77 basis points from the prior year. During the recession, free cash flow growth was surprisingly solid at 14% and 56% in fiscal 2009 and 2010, respectively. In 2011, growth decelerated to 9%. Of course, Halma's strong free cash flow growth during the Great Recession should not be over-interpreted due to contributions from acquisitions, but the numbers nonetheless confirm the company's extremely strong position. And rest assured, Halma's balance sheet was in really good shape even after the Great Recession. At the end of fiscal 2010, the company had a net cash position of about £9 million, when cash and cash equivalents are netted against short- and long-term debt. Halma's dividend payout ratio was approximately 60% of normalized FCF prior to the Great Recession and declined to 40% by fiscal 2011. The further decline in the payout ratio to the current level of 30% - although the dividend continues to increase at a rate of at least 5% per year - underscores management's conservative but shareholder-friendly stance.

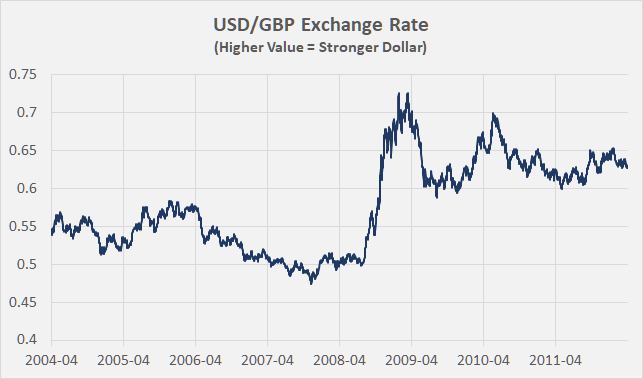

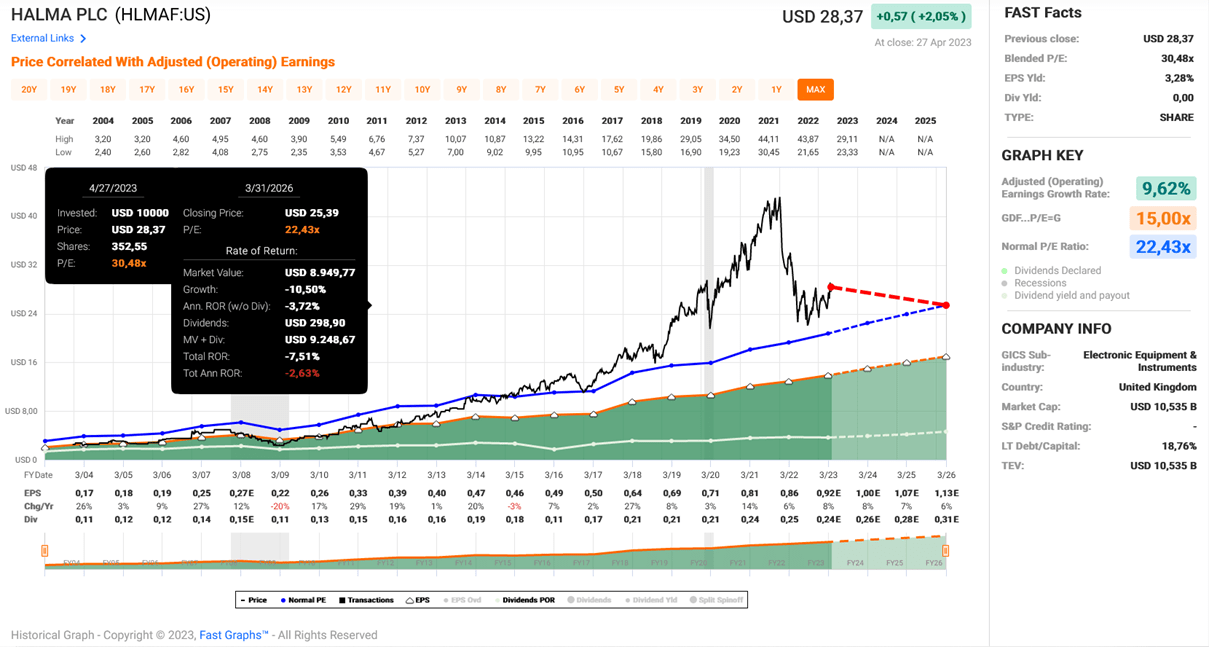

Against this backdrop, it is difficult to understand the drastic decline in the share price (Figure 7). It should be noted, however, that the FAST Graphs chart is expressed in U.S. dollars. The implied decline in earnings per share ((EPS)) in fiscal 2009 was due to a significant appreciation in the USD/GBP exchange rate during the Great Recession (Figure 8). In sterling terms, Halma actually reported adjusted EPS growth of 10% year-over-year, to be precise.

{kind=link}

Figure 7: 2004 – 2012 FAST Graphs chart for Halma plc’s OTC-traded shares [HLMAF], based on adjusted operating earnings per share (obtained with permission from www.fastgraphs.com)

{kind=link}

Figure 8: USD/GBP exchange rate between April 2004 and April 2012 (own work, based on data from Yahoo Finance)

Like the apparent EPS decline, the sharp decline in the share price since mid-2007 (>50% from peak to trough) should not be overinterpreted, as it is also influenced by the exchange rate. In pound sterling terms, Halma shares declined by about 40% from peak to trough. Overall, the decline was certainly still significant, but in hindsight it is difficult to understand given the company's excellent performance. Given that Halma's smart acquisition strategy has not changed, its balance sheet remains very solid, and management shows an unwavering commitment to sustainable growth, I believe the past is indeed a reasonable blueprint for the future.

Concluding Remarks

Halma, the extremely well-managed but little-noticed U.K.-based conglomerate, surprised investors positively even during a period characterized by supply chain disruptions, high inflation and a poor economic outlook. The company remains committed to sustainable growth through disciplined acquisitions and delivered 14% adjusted earnings growth for fiscal 2022, and is expected to report similarly strong results in June. Unlike many other companies, Halma has had very little issues with working capital management and continues to generate very strong free cash flow. Return on invested capital, from both an earnings and cash flow perspective, continues to be well above the company's estimated cost of capital.

In addition to the continued strong performance, a look at the past provides insight into why Halma likely continues to trade at a premium valuation (28.7 P/E based on 2022 adjusted EPS). The company weathered the Great Recession very well, even posting 10% adjusted EPS growth in both fiscal 2010 and fiscal 2009. Even then, Halma was characterized by a smart acquisition strategy, an unwavering commitment to sustainable growth, and a very solid balance sheet.

Of course, Halma's stock price fell significantly in 2022, but I would argue that the strong performance after the dip in March 2020 is largely attributable to yet another irrational exuberance by Mr. Market – ESG-based investing and companies that benefit from this trend. It should not be forgotten, however, that the depreciation of the British pound against the U.S. dollar since mid-2021 has also contributed to Halma's poor performance in the USD-based FAST Graphs chart in Figure 9.

{kind=link}

Figure 9: 2003 – 2023 FAST Graphs chart for Halma plc’s OTC-traded shares [HLMAF], based on adjusted operating earnings per share (obtained with permission from www.fastgraphs.com)

The current P/E ratio of 29 (based on fiscal 2022 earnings) is definitely high, but can be considered acceptable given the continued strong growth. I also concede that the stock looks compelling given the sharp decline since late 2021. However, recency bias is a dangerous psychological phenomenon that we should always remind ourselves of.

At the current P/E ratio, a price-to-earnings-growth ratio of over 2.0, and a free cash flow yield of less than 3%, I don't think Mr. Market is offering us a Halma stock with a reasonable margin of safety. Add to that the fact that investors are likely to sell Halma stock in anticipation of poor earnings when the next recession hits the news, I would be wary of buying Halma stock at this level. Even though the company's earnings can be expected to hold up in a recession, same as in 2008/09, I think investing in the stock today could provide a false sense of security. That being said, it is always difficult to buy great companies as they never seem to be cheap. I'm keeping Halma on my watch list and would feel comfortable building a position if the P/E ratio drops to the low 20s.

As always, please consider this article only as a first step in your own due diligence. Thank you for taking the time to read my latest article. Whether you agree or disagree with my conclusions, I always welcome your opinion and feedback in the comments below. And if there is anything I should improve or expand on in future articles, drop me a line as well.

For further details see:

Halma Stock: What Happened During The Great Recession