HALMY - Halma: Unleashing Growth Potential

2023-08-29 04:50:18 ET

Summary

- Halma Plc is a global group of technology companies specializing in safety, healthcare, and environmental solutions.

- The company has achieved 20 straight years of record growth, driven by its impressive business model. Halma is a serial acquirer with deep expertise that allows for business development.

- The company has sticky demand, a wide moat, and non-cyclical earnings, making it incredibly attractive as a long-term hold.

- Margins are high, although the scope for improvement looks minimal.

- Relative to industrial businesses, Halma is a clear outperformer.

Investment thesis

Our current investment thesis is:

- Halma is a high-quality business, owing to its impressive M&A track record, diversified revenue, deep industry expertise, and exposure to attractive industries (high margins, stick revenue).

- The business looks positioned to continue its current growth trajectory, with M&A and organic growth propelling the business forward hand-in-hand.

- The business has been resilient to economic conditions and when compared to peers, is significantly outperforming.

- Halma looks slightly undervalued, with investors likely pricing in the impact of an increase in the cost of capital.

Company description

Halma Plc ( HLMAF ) is a global group of technology companies that specialize in safety, health, and environmental solutions. With a diverse portfolio of businesses, Halma focuses on developing innovative products and technologies to protect people and assets, prevent accidents, and improve operational efficiency. The company operates across various sectors, including healthcare, environmental, and industrial safety.

Halma was incorporated in 1894 and is listed in the UK.

Share price

Halma's share price has performed well in the last decade, slightly underperforming the wider S&P 500. This has been driven by a continuation of its successful growth strategy, as well as operational excellence.

Financial analysis

Halma financial analysis (Capital IQ)

{kind=link}

Presented above is Halma's financial performance for the last decade.

Revenue & Commercial Factors

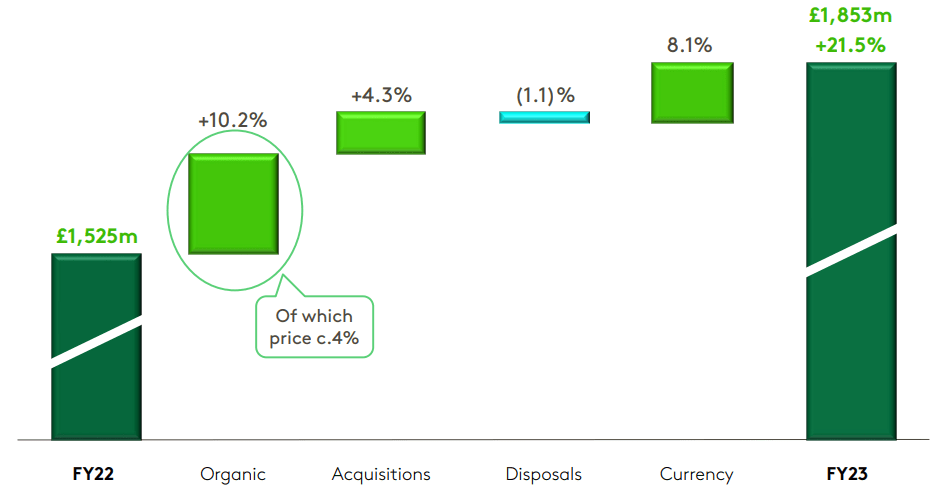

Halma's revenue has grown at a healthy 12% over the last 10 years, with no fiscal year post-FY16 with growth below 10% (excl. pandemic-impacted year). This reflects an impressive level of resilience in what is a mature market.

Business Model

Halma's business is split into three primary segments.

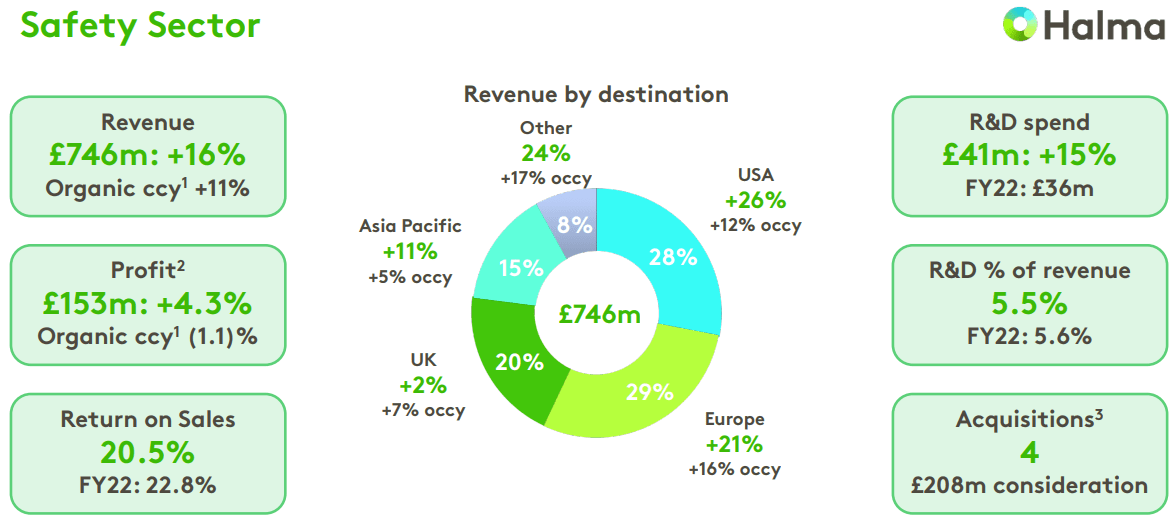

Safety

In this segment, the company offers a range of solutions related to fire safety, including fire detection and suppression systems. Additionally, it provides solutions for ensuring safe movement in public, commercial, and industrial spaces, as well as elevator safety measures.

Given the breadth of services, these solutions are utilized by a variety of industries, such as shops, healthcare facilities, offices, stadiums, industrial and logistics assets.

This segment generates high-quality revenue as a large portion of this is recurring in nature. The reason for this is maintenance and compliance, which means ongoing services are required (both by law and by operational necessity).

Growth remains strong in this segment, with 16% in FY23. This was partially supported by the 4 acquisitions conducted in the year but organic growth was an impressive 11%. With strong R&D spending and the benefits of full-year acquisitions, FY24 is expected to be another strong year.

{kind=link}

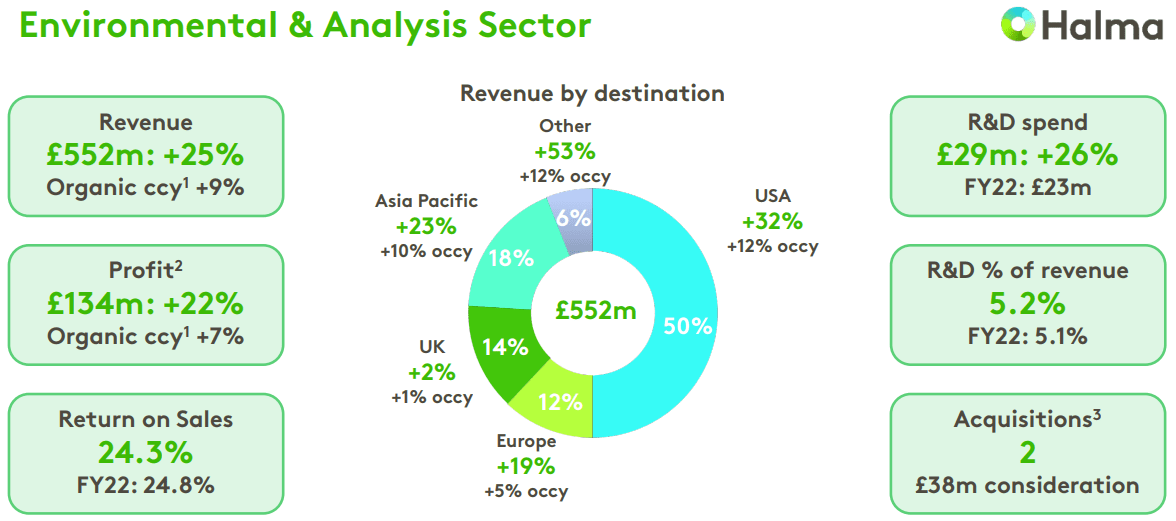

Environmental & Analysis

This segment of the company specializes in optical, optoelectronic, and spectral imaging systems. It offers solutions for environmental monitoring, water and wastewater analysis and treatment, gas analysis and detection, and optical analysis.

The company assists clients in accurately analyzing and understanding various environmental factors and contributes to the improvement of environmental management and resource utilization.

This segment, similar to Safety, has a strong integration in economic development. The legal requirements for environmental impact and water treatment are high and is a recurring process. We expect growth to be enhanced by the focus on environmental care and the impact of climate change, especially as acquisitions bolster its exposure to this.

Growth has been strong in FY23, with acquisition-led gains. This is expected to normalize in FY24 following only small acquisitions, but once again, organic growth is impressive.

Environmental analysis (Halma)

{kind=link}

Medical

The company's Medical segment provides critical fluidic components that are essential for medical diagnostics and original equipment manufacturers in the healthcare industry. It also offers components, devices, and systems that provide information and analytics to aid in understanding patient health and decision-making for healthcare providers across the continuum of care.

Through the wide range of services provided within this segment, the business enables medical diagnostics, treatment across clinical specialties, and advancements in life sciences.

This segment also falls under the "critical" services criteria Halma operates with, providing a deeply integrated service with sticky revenue. Growth is in line with the other segments, with strong organic growth and an M&A-led top line.

{kind=link}

As the segment analysis shows, Halma's revenue profile is highly attractive. The business targets non-cyclical industries that require deep expertise, scale, and scope for recurring revenue through client relationships. These factors smooth the revenue curve on an upward trajectory while providing the business with a wide moat.

Further compounding this quality is its geographical spread, with no country representing more than 42% of revenue. Although the business isn't cyclical, this still supports the reduction of concentration risk.

{kind=link}

These factors have led to the company's 20th year of record profitability, driven by a fundamentally strong organic growth profile. Capex investment has consistently remained at 2-3% of revenue, supporting business improvement, and allowing Halma's brands to remain market leaders.

Snapshot (Halma)

One factor that underpins this is Halma's approach to business. Halma is centered around acquiring and nurturing a portfolio of companies that have scope for high growth. The company provides strategic guidance and support to its subsidiary companies while encouraging them to maintain entrepreneurial independence. Halma's decentralized model allows each business to focus on its specific market and customer needs.

We are a big fan of an M&A strategy, especially when Management is savvy enough to understand how to execute it successfully. Halma's approach has been fantastic, with quality due diligence around realizable synergies, market potential (scope for widening or deepening), customer relationships, and cross-selling opportunities with existing businesses.

The industries it operates within are highly fragmented, especially in the safety market, allowing the business to have an impressive runway for acquiring and improving businesses that lack scale and operational capabilities.

In FY23, the company acquired 7 businesses for £397m. We expect a successful continuation of this strategy, and given the size of its deeps, we are not overly concerned by the odd poor purchase.

Now that readers understand the wider profile of Halma, it is worth illustrating how revenue growth is built up. The business does not rely on M&A to drive growth, although it does materially contribute. The business has been incredibly successful with a two-pronged approach. The business is very good at buying and very good and building.

{kind=link}

Looking ahead, we believe revenue growth will be supported by expansion into new geographies. As regulatory requirements and infrastructure spending developments in emerging markets, the demand for Halma's services across its various businesses will increase. Given its strong presence in the West and clear market-leading expertise, we believe its companies will be well-positioned to win new mandates. Further, M&A will support this, as its clear skills in identifying good Management teams will allow the business to find local targets to support entry into larger markets where organic growth is more difficult.

Competitive Positioning

Halma's competitive position revolves around the following key factors.

- Halma operates through a wide range of companies, enabling the company to address multiple industries and benefit from cross-selling opportunities. Further, through operating multiple businesses in an industry, the company is able to capture a wider portion of the market.

- Halma's businesses leverage advanced technologies and deep expertise to continually innovate, ensuring the focus is on achieving a healthy mix of both optimized returns and growth.

- Operational expertise, both for maximizing returns and in the identification of M&A targets.

Economic & External Consideration

Current economic conditions are depressing many businesses, as consumer spending declines due to high inflation and elevated rates. We believe the impact on Halma will be small, primarily due to the inelastic nature of demand, as it provides "necessities". This should allow the business to outperform the wider economy in the coming 12-24 months.

If anything, we believe this could represent a short-term opportunity, as small businesses are more likely to be sold at attractive valuations, with the cost of capital temporarily high. As a cash-generative business with scope for further debt or equity raising, Halma is positioned well.

Margins

Halma has strong margins, with an EBITDA-M of 22% and a NIM of 13%. Margins have generally remained flat over the historical period. Halma's strong margins are a reflection of its industry dynamics, with inelastic demand allowing the business to price aggressively.

The lack of margin improvement over the last 10 years is slightly disappointing but a reflection of its inability to achieve margins in excess of this at scale. With an employee-led business, the company will always be partially hamstrung by improving compensation.

Balance sheet & Cash Flows

Halma is conservatively financed, with a ND/EBITDA ratio of 1.4x, much of which is leases. This low level is a reflection of the company primarily utilizing cash for its acquisitions, reducing the risk of a poor acquisition negatively impacting the business over time.

Despite the capital allocation toward growth, the business is still in a position to distribute to shareholders. The absolute amount is underwhelming but given the positive price action, we consider this healthy.

Industry analysis

Industrial Conglomerates (Halma)

Presented above is a comparison of Halma's growth and profitability to the average of the Industrials industry, as defined by Seeking Alpha (8 companies).

Halma performs extremely well in our view. The business has achieved outside growth, in both revenue and profitability, across various timeframes. This illustrates the strong M&A execution but also its organic trajectory, which if taken alone would materially outperform the industry.

Further, Halma has superior margins to the market, owing to its focus on industries it can develop a wide moat within.

Valuation

{kind=link}

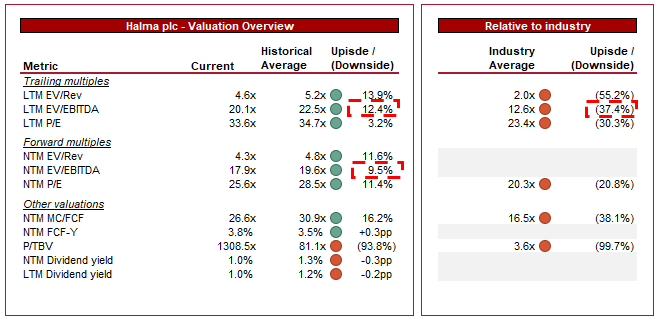

Halma is currently trading at 20x LTM EBITDA and 18x NTM EBITDA. This is a discount to its historical average.

Our view is that a premium to its historical average is justified. Halma is at a large scale, has a bigger portfolio of businesses, continues to develop its market presence, and has maintained its current margins. Looking ahead, we expect a softening of rates to support a resurgence in M&A activity (likely to begin in 6-12 months as there is a belief M&A may now begin to improve ), unleashing the company to continue its current trajectory.

Peer analysis is far more difficult to assess given the substantial growth delta and margin superiority. For this reason, we put far more weight on the historical view.

Key risks with our thesis

The risks to our current thesis are:

- FX. As a global business, the translation of earnings to Sterling represents a key threat. In FY23, this was beneficial for the business but it is uncertain how this will develop in the medium term.

- Deal origination. As an acquirer, the business must continue to identify high-quality acquisitions in order to move the business forward. This has been successful thus far and with fragmented industries, this should continue. This said, there is a risk that the quality of acquisitions decline.

Final thoughts

Halma is an incredibly well-run business. The company's focus on acquiring businesses with a quality commercial profile has allowed it to achieve respectable organic and inorganic growth. We very much like the revenue profile, sticky demand, and defensible position. Our expectation is for healthy growth to continue in the coming years.

The business is likely trading at a discount due to the rapid rise of the cost of capital, as well as general market weakness. Given the acquisitions already conducted, we believe FY24 will be strong. Post this, we see a softening of rates, which should allow cost-effective M&A to return.

For further details see:

Halma: Unleashing Growth Potential