ARGX - Halozyme: Inflection Point With argenx's Vyvgart SC Approval (Reiterating Buy)

2023-07-05 06:24:36 ET

Summary

- argenx's Vyvgart Hytrulo, a game-changer with its 1-minute SC formulation, opens a new revenue stream for Halozyme with sales expected to surpass $10Bn.

- Despite past headwinds, Vyvgart's SC approval and potential co-formulation patent disclosure could kick-start HALO's stock recovery.

- A plethora of 2023 catalysts including subcutaneous formulation data for Ocrevus and Opdivo, Tecentriq approval, and phase 3 efgartigimod CIDP readout may further elevate HALO's stock.

- Amid potential risks, HALO's attractive P/E ratio, strong cash position, and future royalty streams forecast a promising growth trajectory.

- We maintain a buy rating for Halozyme.

Update: Resurgence on the Horizon: Halozyme's Inflection Point with argenx's Vyvgart SC Approval

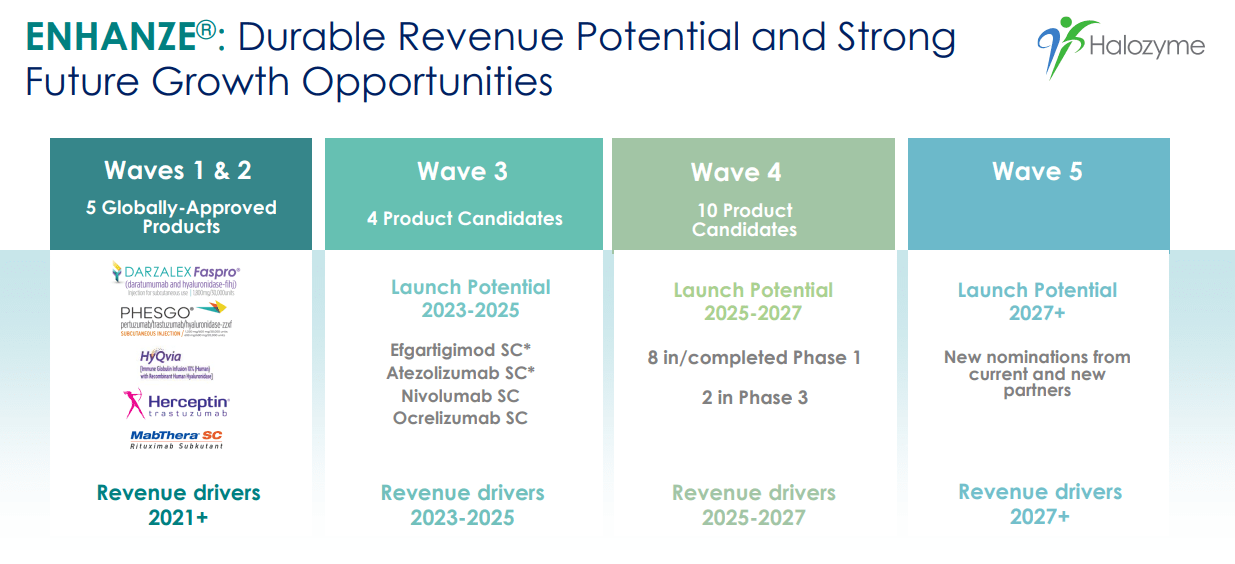

A pivotal event unfolded on June 20th , as argenx's ( ARGX ) subcutaneous formulation of Vyvgart was approved for myasthenia gravis ((MG)), a long-awaited step that brings a breath of fresh air into Halozyme's ( HALO ) product cycle. We believe the FDA's approval of the Biologics License Application ((BLA)) for Vyvgart Hytrulo (SC efgartigimod) opens the gate for an additional revenue stream for Halozyme and we believe SC formulation will be a game-changer and boost its sales trajectory considering the convenient nature of the administration (cuts the injection time from a 1 hour-long IV infusion to a roughly 1-minute subcutaneous injection), some analysts are projecting Vyvgart's peak sales to surpass $ 10Bn .

Potential inflection point for Halozyme

Since we initiated Halozyme back in April , Halozyme's stock has endured a turbulent year, burdened by a series of unfortunate events: a) the delay in Vyvgart's PDUFA approval, b) an intellectual property setback in the EU for Darzalex, and c) overhang around IRA (inflation reduction act). However, we believe Vyvgart's recent SC approval might be the first sign of a market rebound for HALO, given its potential to substantially increase patient reach (and prescribing volume) through its convenient dosing that can boost efgartigimod's sales (remember the current efgartigimod is just an IV formulation without using Halozyme's technology and efgar still generated ~$400m). Furthermore, we believe there is a possibility that the companies may disclose a co-formulation patent, which can add more confidence around its royalty cash flow beyond 10 years for efgartigimod (which may have not been fully priced into the current valuation).

{kind=link}

Potential future royalty opportunity (Company IR deck)

Lots of catalysts to be excited at

Furthermore, we believe 2023 isn't lacking catalysts for HALO, which might be the impetus needed to liberate the stock from its current slump. We believe the critical upcoming events include a) Ocrevus and Opdivo subcutaneous formulation data in the 2H 2023, b) the potential approval of Tecentriq, c) the high-volume autoinjector human study results (2H 2023), d) phase 3 efgartigimod CIDP readout (2H 2023), and c) efgartigimod ITP launch 2H 2023 or during 2024.

Risks

Our thesis hinges on the company's ability to deliver favorable clinical data readouts and robust royalties. Other potential risk factors that investors should consider are a) competitive pressure (from other competitive technologies), b) regulatory obstacles, and c) reimbursement issues and pricing concerns (potential tailwind from IRA).

Conclusion

Net-net, we believe that Halozyme is on the verge of a significant inflection point and reiterate our non-consensus Buy rating moving into 2H 2023. In terms of the valuation standpoint, the company's PE ratio is only 13.8, which is highly attractive for a high-growth biotech company and the current $275m cash in the balance sheet should give comfort to investors. The main reason for our non-consensus optimism around the stock is that we believe the stock's current value does not adequately reflect the potential upside from the post-wave 3 royalty streams, where we see royalty growth into 2030 where the market will re-rate the stock moving forward in a short period of time as better than expected royalty stream comes in from argenx's efgartigimod SC formulation, especially when argenx is pricing the SC formulation in line with the IV formulation. Furthermore, we believe there are potential positive catalysts in the mid-term future in Wave 4 activities around initial IP discussions (2027 in the US).

For further details see:

Halozyme: Inflection Point With argenx's Vyvgart SC Approval (Reiterating Buy)