HALO - Halozyme Therapeutics: Pharma With Growing Royalty Revenue And Product Income

2023-06-19 07:44:24 ET

Summary

- Halozyme Therapeutics' valuation has declined, providing a more attractive entry point for investors.

- The company has multiple royalty-producing products and two new ones awaiting approval in 2023.

- Halozyme has a strong pipeline of products in development and diverse revenue sources from various therapies.

This is my second article reviewing Halozyme Therapeutics ( HALO ). The first , 05/2022's "Halozyme Therapeutics: A Pharma Mutual Fund In A Single Company" ("Single Company") took a bullish perspective on the company.

At the time Halozyme's valuation held me back. It has since declined from >$40 to ~$35 on 06/18/2023 providing a more attractive entry point. In this article I provide a substantive review of the company. Key documents i will discuss include its Q1, 2023 earnings:

- Press release (the " Release ");

- Conference call (the " Call ");

- 10-Q (the " 10-Q ");

- Presentation (the " Presentation ");

Halozyme's business produces several revenue streams.

In the 10-Q, Halozyme provides a vague, unhelpful description of its business as:

...a biopharma technology platform company that provides innovative and disruptive solutions with the goal of improving the patient experience and potentially outcomes.

It goes on to describe its proprietary enzyme, rHuPH20. This enzyme facilitates the subcutaneous (“SC”) delivery of injectables. It works by breaking down a major component of the extracellular matrix of the SC space.

By temporarily reducing the barrier to bulk fluid flow it allows for superior SC delivery of high dose, high volume monoclonal antibodies and other large and small therapeutic molecules and fluids. ENHANZE is the trade name Halozyme uses to reference the application of rHuPH20 to facilitate the delivery of other drugs or fluids.

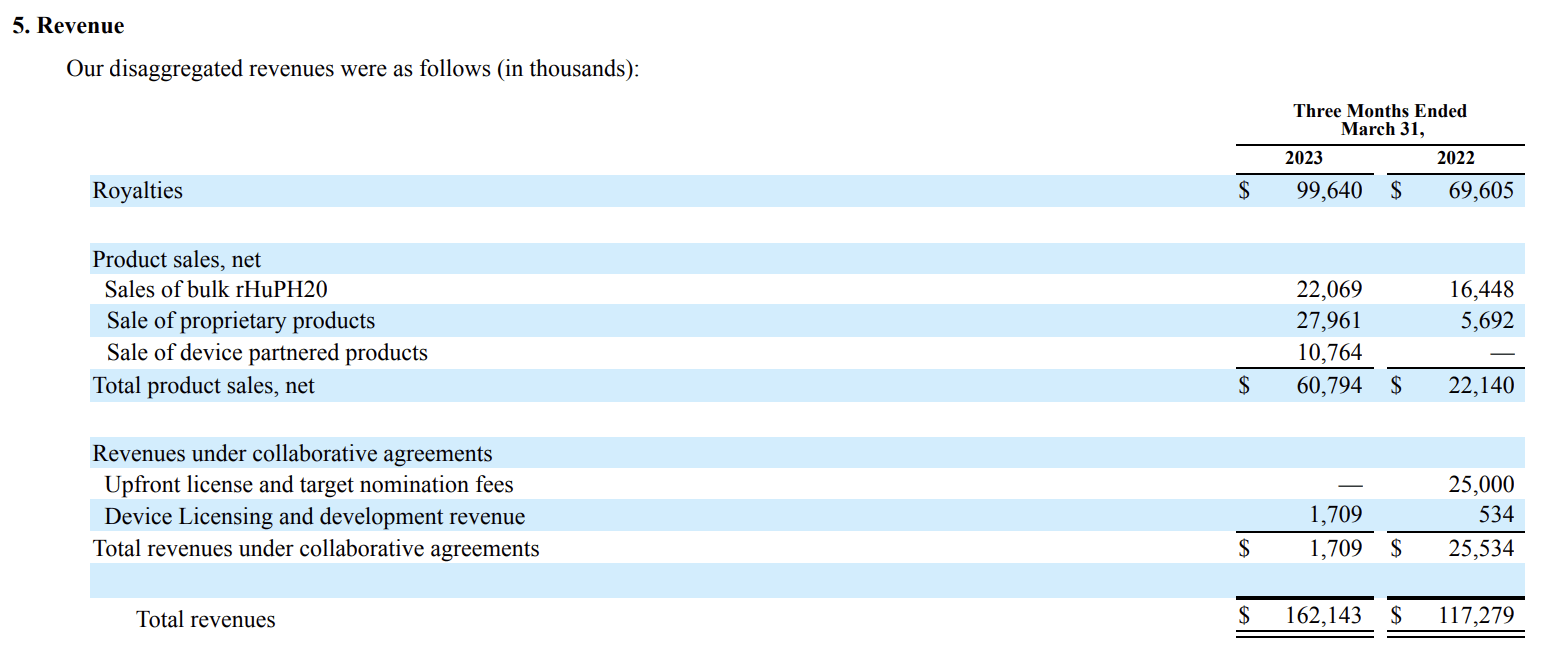

The 10-Q lists the following disaggregated revenue report:

{kind=link}

seekingalpha.com

Four discrete entries make up the bulk of its revenues:

- royalties;

- bulk rHuPH20;

- proprietary products; and

- device partnered products.

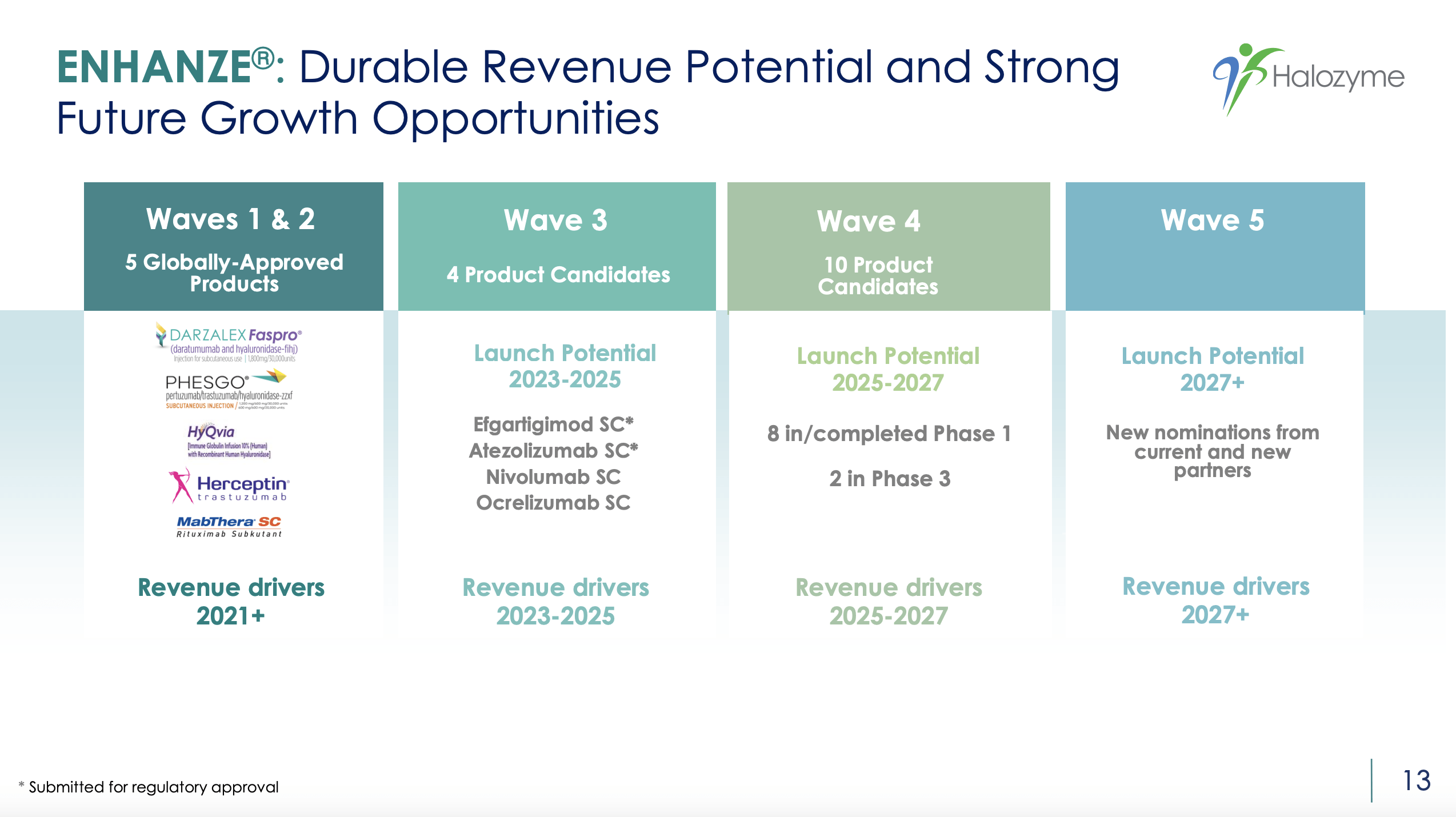

Entry 1 - royalties and entry 2 - rHuPH20 are very much tied at the hip in the sense that the bulk of Halozyme's royalties derive from ENHANZE technology which is enabled by HuPH20 . Presentation slide 13 shows the significant role that ENHANZE and by extension rHuPH20 play in the past, present and future of the Halozyme story:

{kind=link}

seekingalpha.com

Halozyme's guidance is encouraging.

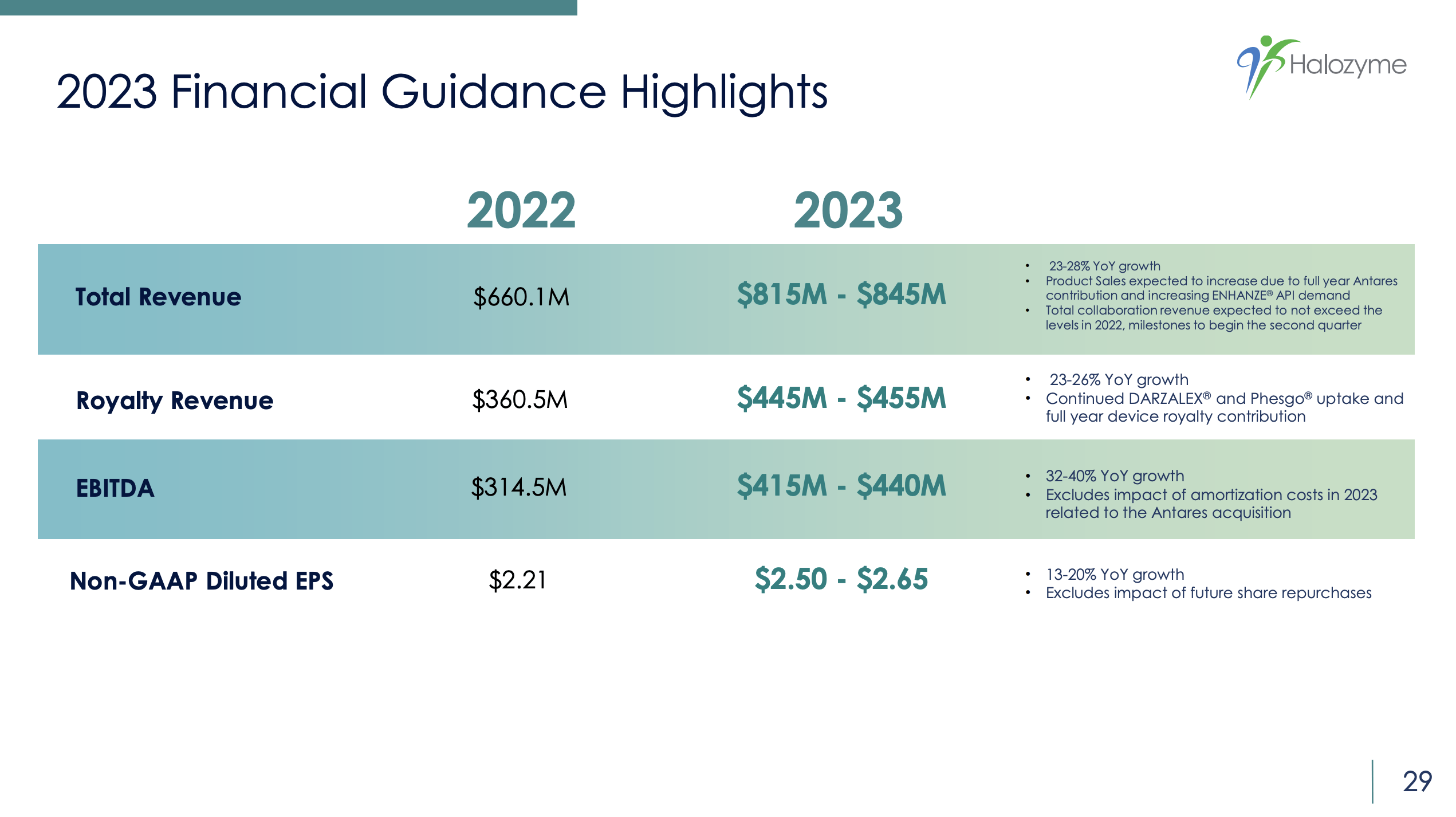

During the Call Halozyme issued confirmation of its previous 2023 guidance as shown on its Presentation slide 29:

{kind=link}

seekingalpha.com

It emphasized the following in regard to these highlights:

- ENHANZE wave 2 products, DARZALEX SC and Phesgol expected to be primary total revenue drivers;

- revenue includes full year of Antares product sales in auto injector royalty contribution;

- revenue from royalties to increase between 23% to 26% over revenue from royalties in 2022 to a range of $445 million to $455 million

- year 2023 guidance includes milestone payments for the approval of SC efgartigimod and atezolizumab for conservative royalty revenue contributions from these two products within this year;

- EBITDA of $415 million to $440 million representing growth of more than 30% over 2022 EBITDA, which excludes the impact of amortization costs related to the Antares acquisition.

During the Call several analysts inquired as to the expected impact of the Inflation Reduction Act [IRA] on its guidance. CEO Torley batted down any concerns on this score. Large volume injectables are in Part B, while to this point guidance issued for the IRA has focused on Part D.

If Part B gets the same treatment as Part D, Its expected impact would be minimal. Subcu, which is enabled by rHuPH20, would be treated as a separate single source agent than the IV drugs.

Halozyme's finances are strong including significant buybacks.

Presentation slide 29 sets out Halozyme's revenue guidance. It also shows its EBITDA for 2023 expected to grow in a range from $415-$440 million growing at a rate of 32-40% YoY. Excluding any impact of future share repurchases, non-GAAP diluted EPS are expected to grow 13-20% YoY to $2.50-$2.65.

CFO LaBrosse rounded out its financial picture by reporting on its liquidity and capital allocations as follows:

Our share buyback programs have resulted in the repurchase of 34.8 million shares since 2019 which contributed $0.09 to non-GAAP earnings per share in the first quarter. Our cash, cash equivalents and marketable securities were $275.6 million as of March 31st, 2023, compared to $362.8 million on December 31st of 2022 due to our Q1 share repurchases.

Our balance sheet remained strong with projected cash generation and EBITDA growth in 2023. Our net debt to EBITDA ratio is 3.2 as of March 31, 2023, which is expected to be less than three by the end of the year. While we have completed our share repurchases allocated for the year, we will continuously evaluate our future use of capital and monitor market conditions and other factors while also preserving capital to fund revenue growth and durability via M&A.

LaBrosse confirmed that Halozyme's decreasing leverage profile, cash flow generation and expected EBITDA growth preserved ample opportunity for future M&A. CEO Torley advised it was actively evaluating M&A opportunities. It was looking for companies with de-risked assets or platforms or technologies with significant, durable revenue growth potential.

Conclusion

Single Company included a "buy" rating for Halozyme. I closed the article:

I view it as a long-term play. Its D-[quant] valuation holds me back from investing more than a nominal sum in the near term. However, I do view this as a definite buy and I expect to acquire additional shares gradually on pullbacks.

As I write on 06/18/2023 Halozyme carries the following quant factor grades:

seekingalpha.com

The valuation grade is only marginally more favorable as is its growth factor grade increase from its former B to its current B+. Accordingly in recognition of its ongoing struggles to generate wider enthusiasm, I will restrain my own. I continue to rate it as a buy for its long term growth potential. I note in this regard CEO Torley's statement during the Call:

... we continue to be excited about the growth of our products and the royalties as we look forward to the potential for $1 billion in 2027 and project the potential to be higher than that in 2031.

For further details see:

Halozyme Therapeutics: Pharma With Growing Royalty Revenue And Product Income