SVNLF - Handelsbanken: Plenty To Like Long Term Impressive Income Safety

2023-05-24 13:49:23 ET

Summary

- I've written about Handelsbanken a few times over the past 2 years, and I still maintain a solid position in the company at this time.

- I went ahead and sold long-dated covered calls about 6 months back, only to buy them back today at 93% profit.

- Handelsbanken is a solid, class-leading bank with an attractive yield - and I'm happy to keep owning it until it gives me reason to sell.

Dear readers/followers,

When I last wrote about Handelsbanken ( SVNLF ), I actually took a relatively somber stance and went " hold ". This proved to be the exact correct choice given where the bank has gone since. Without the dividend, we're down almost double digits, and even with the dividend, we're at negative 3.5%. That is far from beating the 6.25% RoR of the S&P500 in the same timeframe.

Handelsbanken RoR (Seeking Alpha)

The reason for this underperformance was that the bank reached a bit too high in the preceding months. That's also when I sold a number of very attractive covered calls, at annualized returns of almost 15% against my non-trivial position in the company, adding to my already-solid position by accepting the risk of selling my shares at a nice premium compared to the estimated fair value of the bank.

However, the bank stopped before it reached those levels, leaving me with my covered calls as things crashed down.

This wasn't a bad thing of course. This morning, I went ahead and tried buying those CCs back, and managed to do just that, locking in a 93% profit on my options and "Moving on".

Let's see what can be expected from Handelsbanken going forward.

Handelsbanken - Upside for 2023

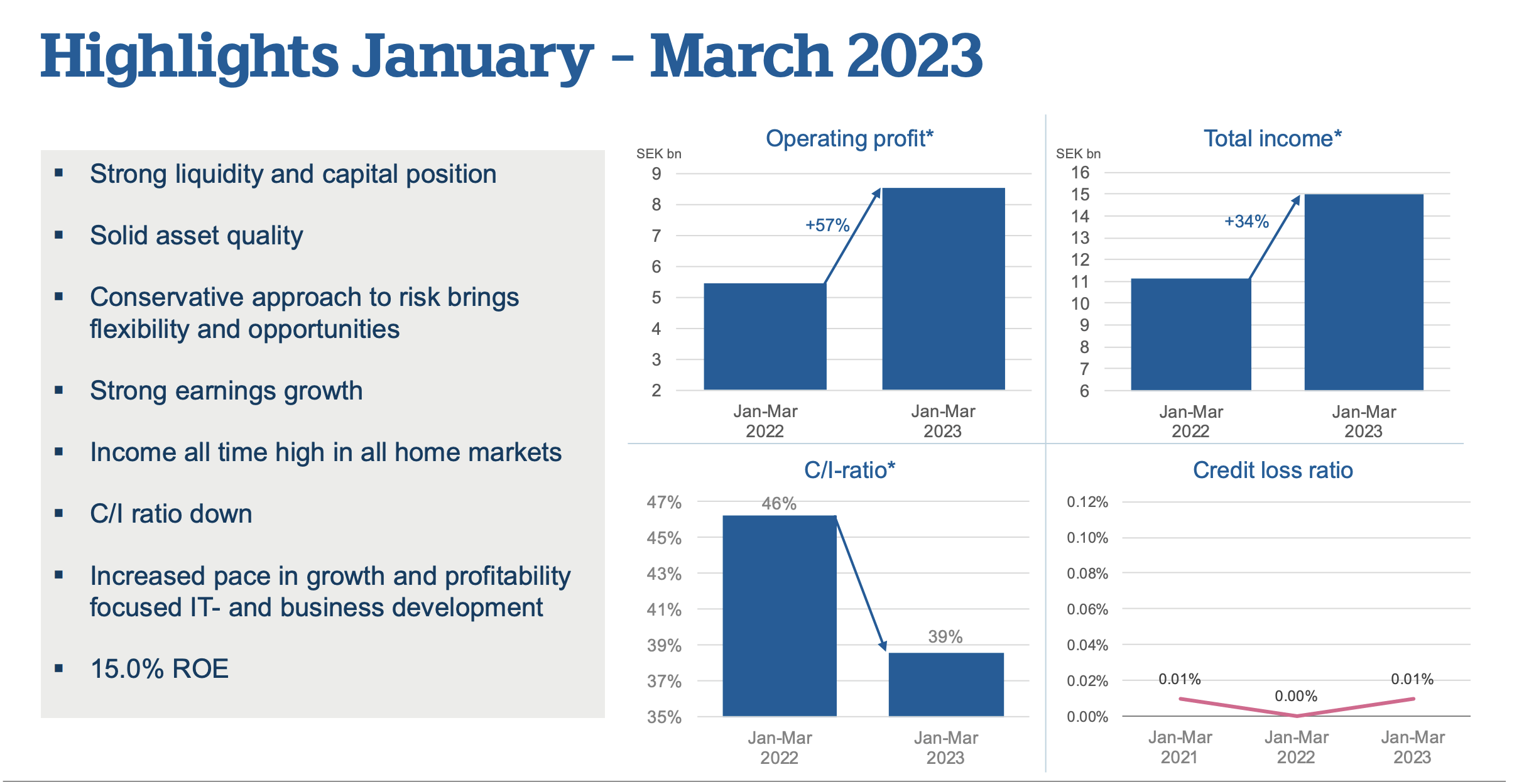

We have the 1Q23 period presented back at the end of April, and the results were predictably solid. In a rising interest rate environment, banks tend to outperform. Quality banks outperform more so. Looking at the banks in Scandinavia, you'd be excused for thinking there wasn't a banking crisis in the rest of the world because compared to some banks, these have held up like fortresses.

And this has been confirmed by the results, where operating profit went up over 55% YoY in 1Q, and total income went up by almost 35% YoY.

Handelsbanken continues to have a very strong liquidity and capital position, and unlike many of its international peers, does not have any sort of toxic or lower-quality assets to a degree that would or should be worrying here.

{kind=link}

Yes, credit loss ratios are up - to 0.01% from zero. Not exactly a red flag flapping in the wind. The company has shown good cost control, and ATH incomes in all home markets.

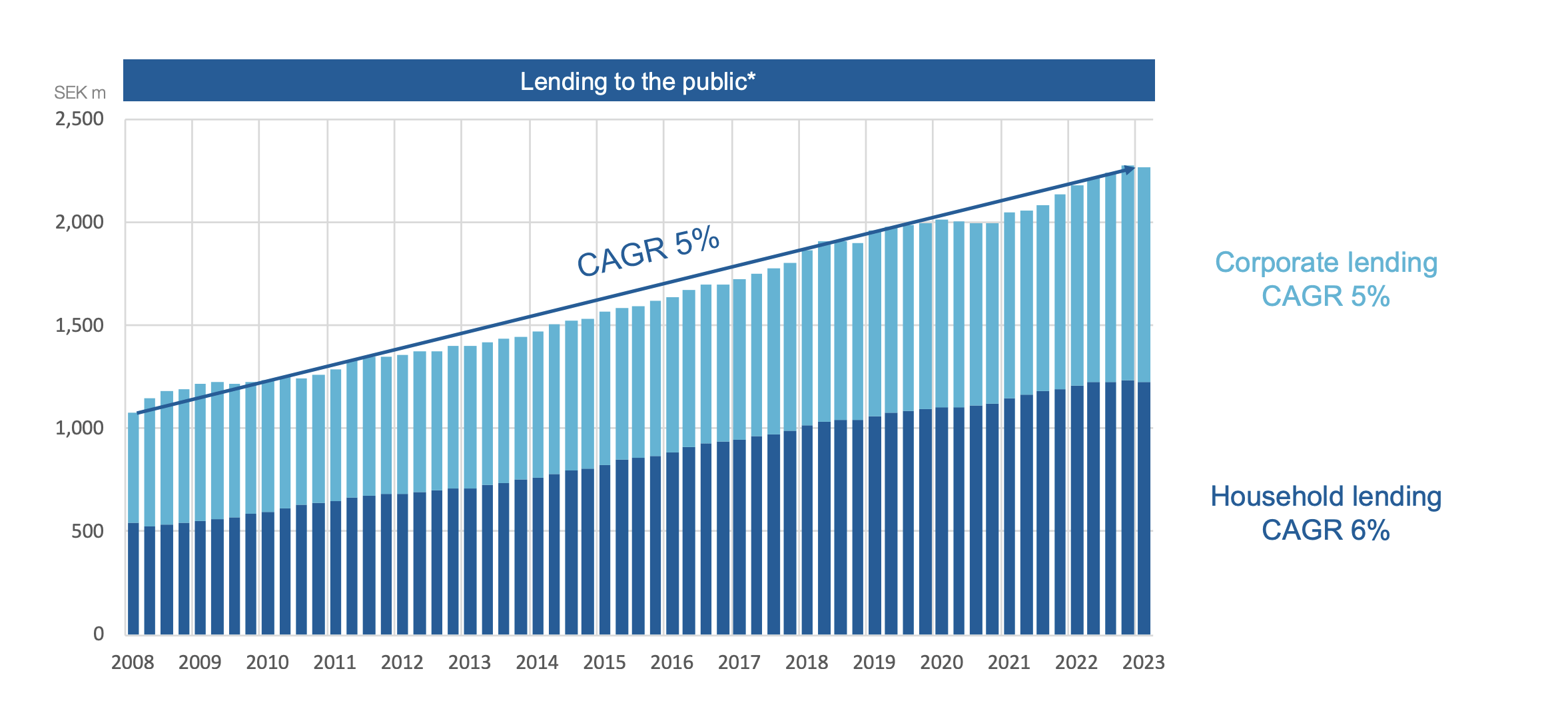

Handelsbanken has performed beautifully. And exactly like the high-quality bank I knew it to be when I invested in it many years ago. With a 19.4% CET-1 ratio, it's also one of the safer banks out there. I remind you that there are A-rated banks that carry no higher CET-1 than 13-14%. The company's lending is like a ramp - a ramp showing the right sort of trends.

{kind=link}

NII is up significantly due to positive margins, pressured only slightly by some volume, liquidity, and deposit fees/FX. Volume trends going down is actually something I like seeing here because it implies the bank is tightening credit standards and its demand on borrowers, which is what we want to see when working with Swedish geographies because Swedish borrowers tend to be leveraged at a very high rate compared to their actual payment ability.

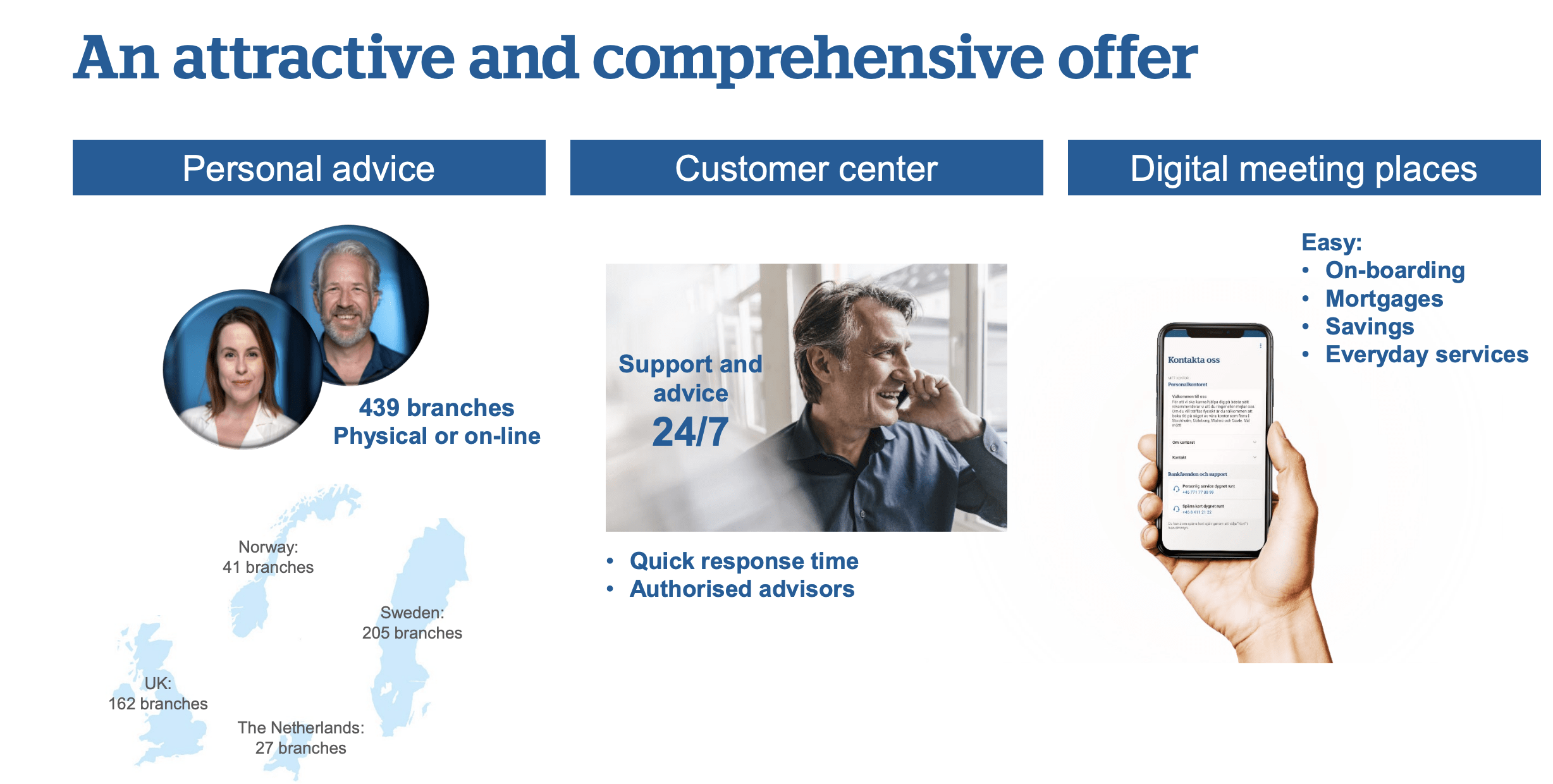

I've previously described Handelsbanken as being a bit of the odd man out because it still relies on personal advice and advisors - the touch many other banks have lost to the digital age. Handelsbanken has become more digitized over the last few years, but it does still retain that personal touch. I know that personally, because I'm the treasurer in our condominium association, and we use the bank - personal connection with our banking contact has always been number one for us, and we maintain this. Whenever we need to leverage up or fund something, it's always a personal talk with the person responsible for us.

{kind=link}

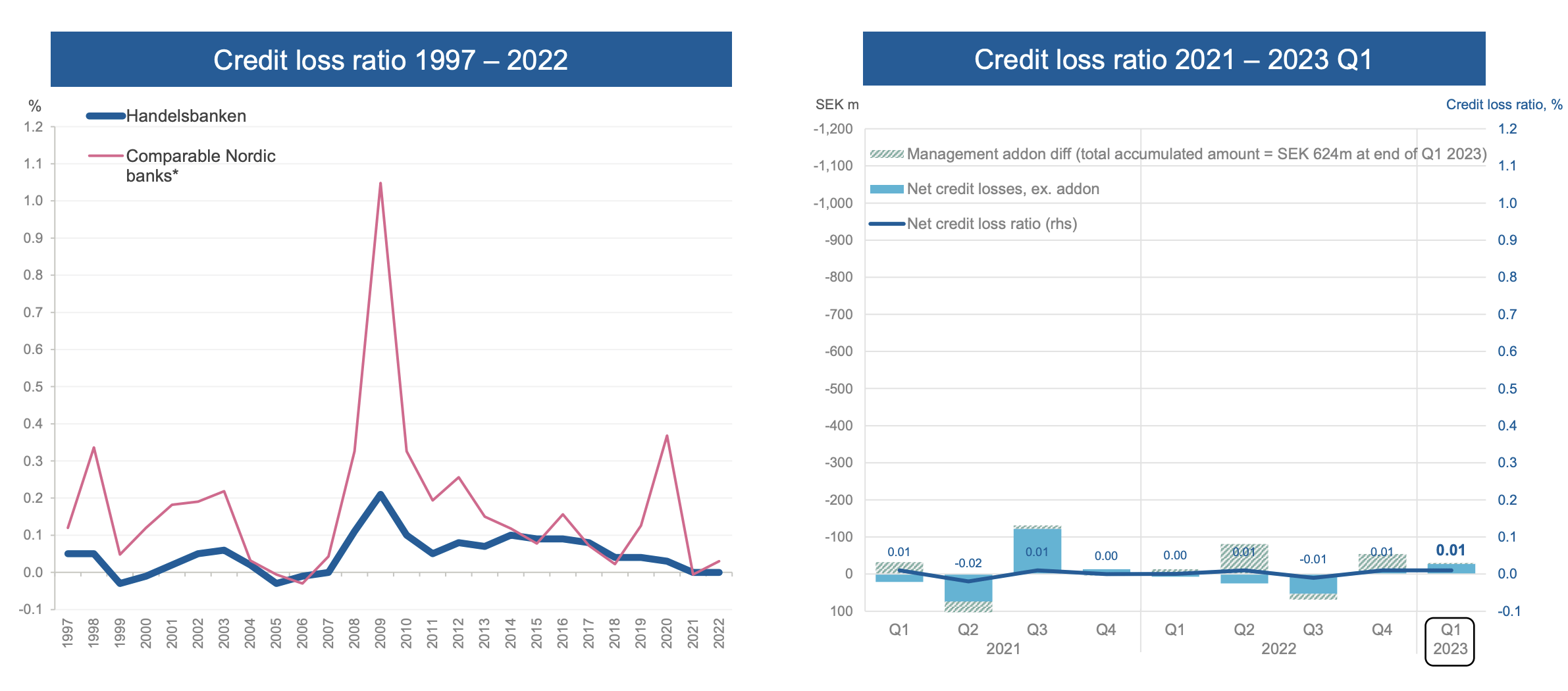

I want to remind you at this point what happens to Handelsbanken in a recession in terms of credit loss ratios and the like, thanks to its absolutely excellent loan standards. We can go back to 1997 and see that Handelsbanken has almost always outperformed its peers on this basis.

{kind=link}

While the bank, like many others, is sitting on some unrealized losses from longer-term bond placements, there's no reason to think that it cannot sit these losses out. Short-term liabilities are backed in turn by 1.7x the number of short-term assets, and asset/liability matching on the longer term is solid as well. Handelsbanken has unutilized room for liquidity-enhancing measures of around $70B if need be, by using covered bonds.

Therefore, the amount of realistic risk inherent to this investment is very, very low, when looking at bankruptcy potential or realistic fundamental impairment. With a 0.01% net credit loss ratio and a sub-39% C/I ratio, this is one of the best banks on the planet. This is a stance I have held for many years, and I continue to hold at this particular time.

Still, some high-level warnings for the general Scandinavian geography. If you invest in any Swedish company, especially Swedish finance, you should be aware of this - we're in for potentially years of pain. The Swedish currency is likely to see continued weakness in the near term. Handelsbanken isn't going anywhere - but it's also in for, as many finance stocks are, certain pressures.

Handelsbanken is one of the best banks around, even if you look at the sector margins. In terms of its net margin, which is currently 42.7%, which puts the company in the 88th percentile in terms of banks. Its profitability is better than 99.9% of all banks in terms of years of profitability over the 10 past years.

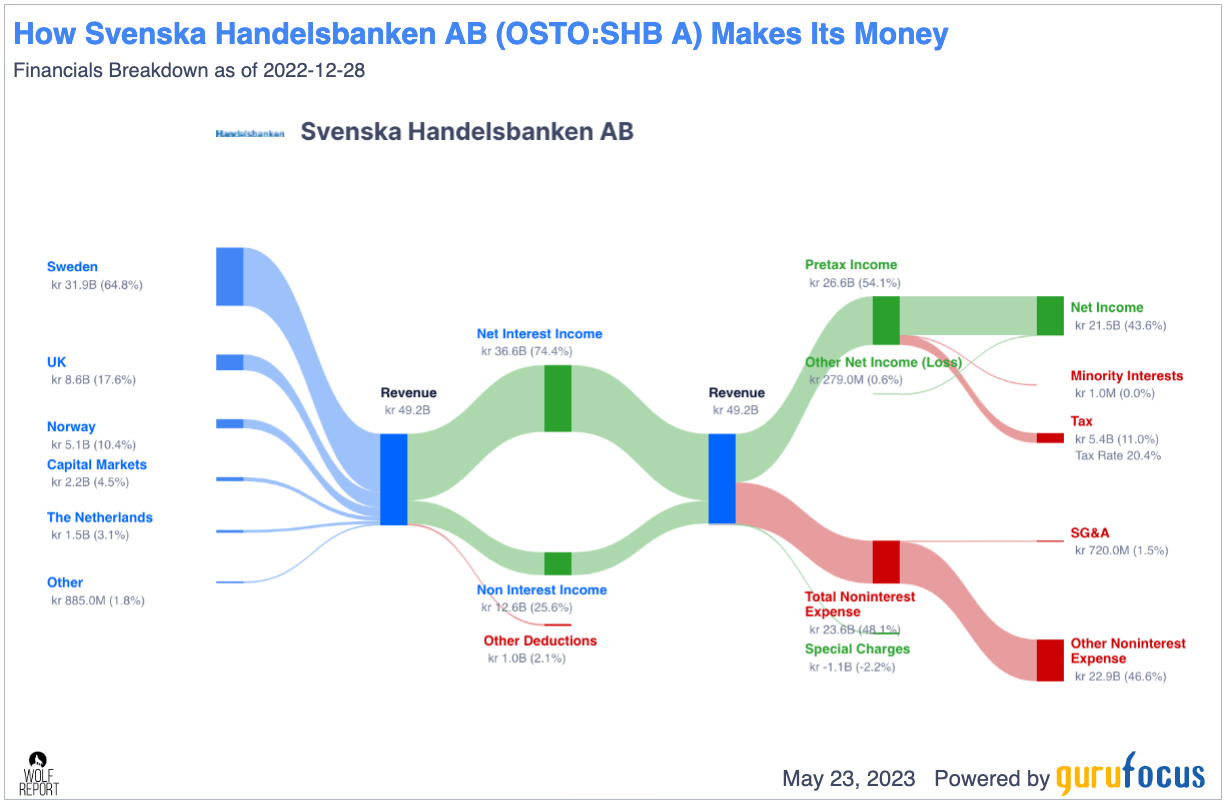

A bank in terms of its income statement looks something like this - and is valuable to look at to get a picture of how the company is exposed, and what amount of NII/Non-NII we have.

Handelsbanken revenue/net (GuruFocus)

{kind=link}

Handelsbanken also sees frequent institutional interest in the form of buying. The recent push against the company which has driven the share price down is, as I see it, a bit of an opportunity to perhaps load up more of the stock.

Let me show you, in simple terms, why I believe now is actually a super time to add to either an existing position or to even start a new one in the space.

Handelsbanken - Plenty to like about the valuation

Investing in Finance companies today is always a bit risky - but I argue that Handelsbanken does remove a lot of that risk.

Why is that, you might ask?

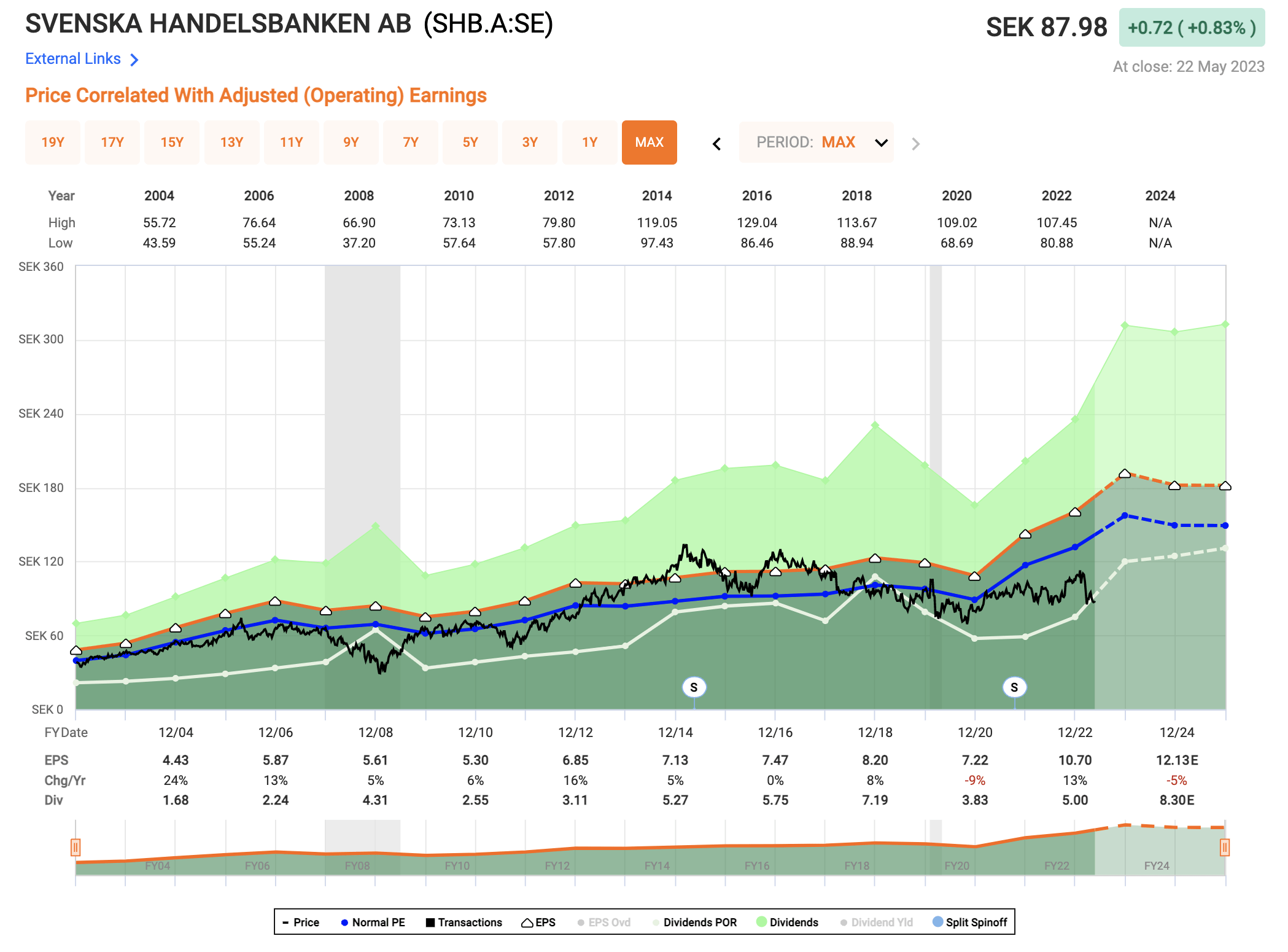

Handelsbanken Valuation (F.A.S.T. Graphs)

{kind=link}

Because Handelsbanken offers you an AA rating, first of all. It's one of the very few banks that achieves this. It has a TEV of over SEK1.3T, and a market cap of nearing $20B - small internationally, but huge here. It pays a well-covered yield at this time of 6.25%. There are finance companies that pay more, but none with the income safety that Handelsbanken could offer you if the forecasts hold. Also, Handelsbanken is currently significantly undervalued seen to its historicals, with a P/E at around 7.6x.

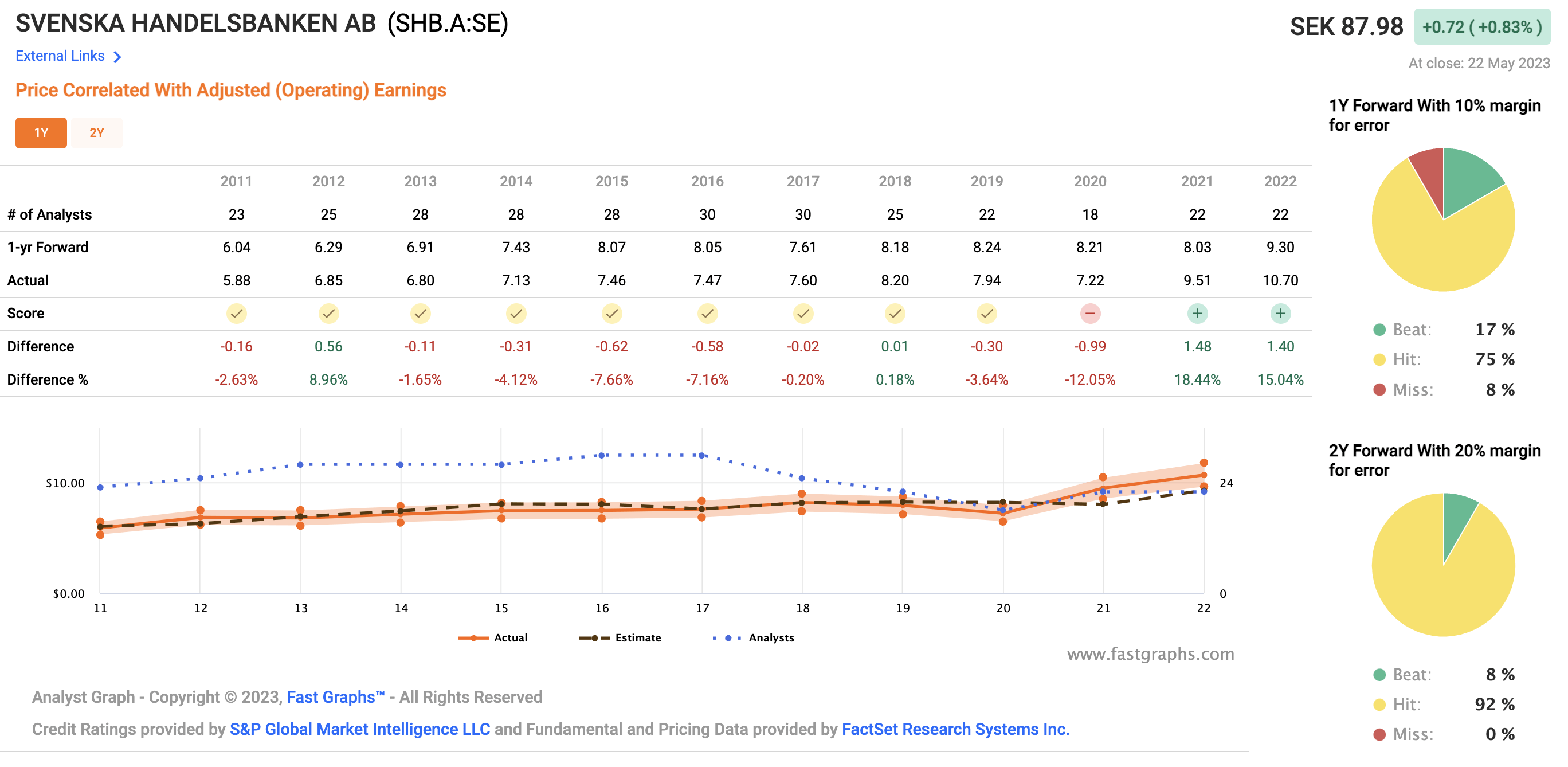

Analyst Accuracy (F.A.S.T. Graphs)

{kind=link}

Even completely ignoring 15x P/E as a mark, which we should because the company seems to lie closer to around 11-12x P/E, the upside based on estimated earnings growth with a 19.49% for this year, and a 4-5% average EPS growth for the next few years every year, is over 23.5%, or 74% RoR until 2025E. That's forecasted at an 11.23x P/E, with an analyst accuracy of nearly 100%.

So, you can argue with me that Handelsbanken isn't as safe as we might think - but you'll need to bring some real arguments to the table for me to even begin to take that sort of stance seriously in any way.

S&P Global averages for this bank come to around SEK115, compared to a SEK88 share price, with an upside of 30.7%. 20 of the analysts follow Handelsbaken, and out of those 6 are at buy. Not a massive amount given the undervaluation we're seeing - I believe they simply haven't caught up in their recommendations for this particular company.

Not so me - I'm taking this opportunity of sub-SEK90 to really push for Handelsbanken, and to clearly change my rating on the company to a " buy ". My previous PT for this particular company was SEK95/share. I'm keeping this PT, and I'm telling you that at this time, you could easily make this company a solid " buy ".

Any downside to this company or its prospects is, as I see it, momentary or not specific to the company itself but rather the entire finance sector. Due to the fact that most insurance companies in Sweden are not in any way publicly traded, I find my finance investments more in the banking sector here.

I now say Handelsbanken is a " buy ", and I'm adding it here.

Thesis

- Handelsbanken is a theoretically attractive and fundamentally appealing bank with a sound set of capital safeties, a 6%+ yield, and overall one of the more conservative banks in the entire Swedish banking market. It's also one of my largest financial holdings, and I frequently sell both puts and calls on the bank.

- At a double-digit price inching closer to SEK90, I believe this bank offers enough safety and conservative appeal to make it a " buy " here. But given certain fundamental troubles brewing in the EU/Swedish economy, I would be careful where I start "going in" to the bank as an investment - though at this price, it's favorable.

- I give the bank a conservative PT of SEK95/share, which at this point means the bank is actually a " buy " as of this article update for May of 2023.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Thank you for reading.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

For further details see:

Handelsbanken: Plenty To Like Long Term, Impressive Income Safety