SVNLF - Handelsbanken: Returning To One Of My Largest Bank Holdings

2023-03-22 13:11:30 ET

Summary

- Handelsbanken has been a part of my core portfolio for years. Until this year, I haven't applied "trim logic" to the holding, which is well over 3.5% of my portfolio.

- I own a significant stake of Handelsbanken which based on my cost basis is yielding over 9% here for this year. I will share with you when I will trim/BUY.

- For now, Handelsbanken stock is mostly a "HOLD" - though it could be an income play, if you want 7-8% from a Scandinavian bank.

Dear readers/followers,

My coverage on Handelsbanken ( SVNLF ) has been extensive over the years, though I haven't touched on this particular holding for some time. Today is the time to change that. In fact, the last article on the bank is also the last article I wrote on it - and I was neutral at the time. This proved to be the right decision, and my stance was clear - too little upside.

Seeking Alpha Handelsbanken (Seeking Alpha)

Handelsbanken remains, as I see it, one of the most quality banks in the Nordic regions. The latest few years haven't really done anything to change that assumption and stance. While I haven't added to my position in the bank for several years, and as a result of this, new additions of capital have diluted the relative position down below 4%, it's still a position that is firmly in the green, and very likely to remain so.

Let me show you what I have done and what the bank has done as of late.

Handelsbanken and its results and expectations for 2023

Handelsbanken reported its results back in February when it also decided on the dividend and a few other things that European businesses typically do when annual results are reported.

To put it simply, and although this is before all the troubles for the banking sector began, the company's 2022A results were excellent.

Why were they excellent?

Because Handelsbanken managed:

- Significant volume growth, 7% improvement in lending among other things

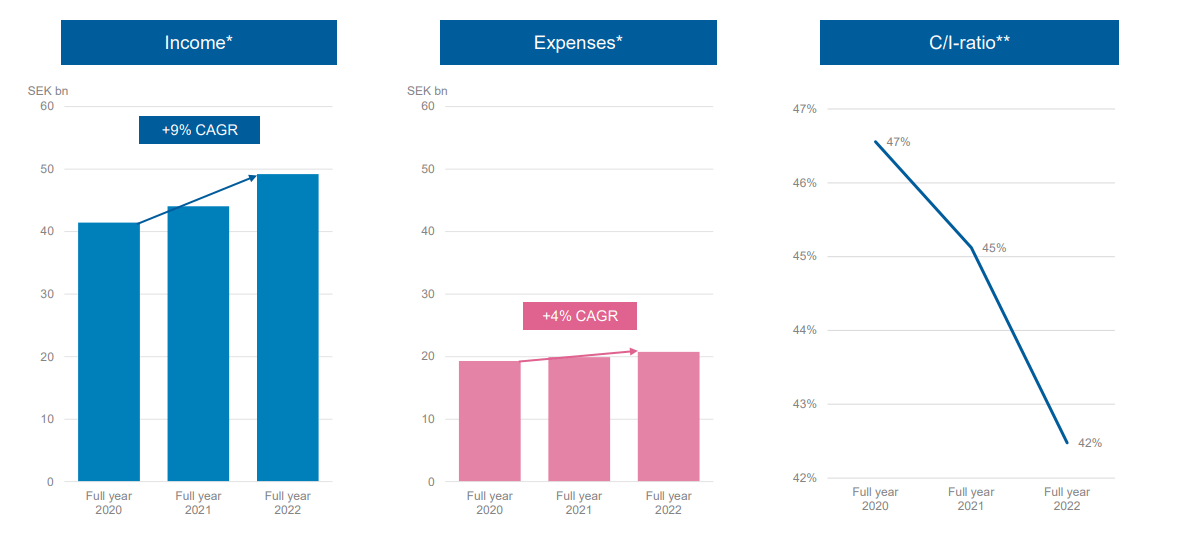

- 21% improvement in NII and 17% operating profit, pre-risk tax expenses.

- Cost/Income ratio down to 42%, from 47% back in 2020. To put it simply, despite inflation and interest rates, Handelsbanken has managed to significantly improve its expense efficiency over the past 2 years.

- Sales of Danish Operations , simplifying the bank's operating structure and segments

- Superb, and near-class leading capital position and safety.

- Increased investment in development for the bank.

- Growing share in a safety-seeking savings/deposit market

- A net credit loss ratio of 0.00% for 2022.

- A class/market-leading CET1 Capital safety ratio of 19.6%

I've said it before, and I will be clear here again. When looking at straight safety numbers and KPIs, Handelsbanken is one of the best-managed banks on earth. The way the company's numbers go is nothing short of staggeringly impressive.

Handelsbanken IR (Handelsbanken IR)

{kind=link}

And because of how the Swedish banking market looks, it's very unlikely that the next few years, or even a decade or two, will see any sort of significant change here. The same banks - Swedbank ( SWDBF ), Nordea ( NRDBY ), Handelsbanken, and SEB ( SVKEF ) remain the main banks in the market, with competition only managing to slice off small pieces of the pie. With the compressing market as we're seeing, and risk costs increasing, many of the smaller players are likely to see their customer base dwindling or disappearing entirely as customers move back to fundamentally more safe banking institutions.

Household lending continues to grow, 5% YoY, but not as much as corporate lending, which grew 11% YoY from 2021 to 2022. A lot and a majority of these loans include so-called green and sustainability-linked facilities and loans, with Handelsbanken now reporting that 20% of the financing volume consists of such.

NII improvements are coming in as a result of increased loan and business volume, but also 12% from significant margin improvement due to increased interest rates. The Bank generated close to 37B SEK in NII during 2022, and guarantor fees and costs only represent a very small margin of this. There was also a significant positive effect to the tune of over half a billion SEK, also driving NII up.

The fees and commissions that the bank introduced or increased to make up for lower NII during ZIRP also haven't been unwound. This has resulted in a two-pronged improvement both from interest rates, but also from continually growing fees and commissions for the bank, which come either as savings-related, payment-related or other. The bank managed over 11B SEK in fees and commissions during the year - somewhat lower than -21, but higher than -20.

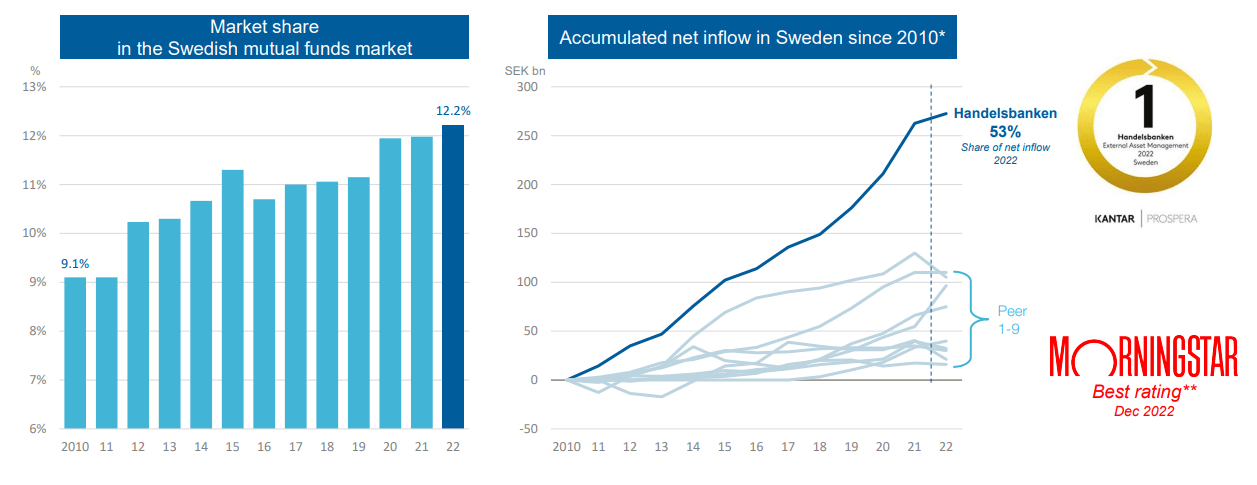

Handelsbanken has always had a massive share of the Swedish mutual funds market, where most people have their savings. And the bank has improved this leadership, together with its inflows.

Just how well Handelsbanken has managed this, I believe can be illustrated using the following.

Handelsbanken IR (Handelsbanken IR)

{kind=link}

It's the sort of trend that begs the question "Do you have any questions?", because the performance and the company's market position has been, and is so excellent.

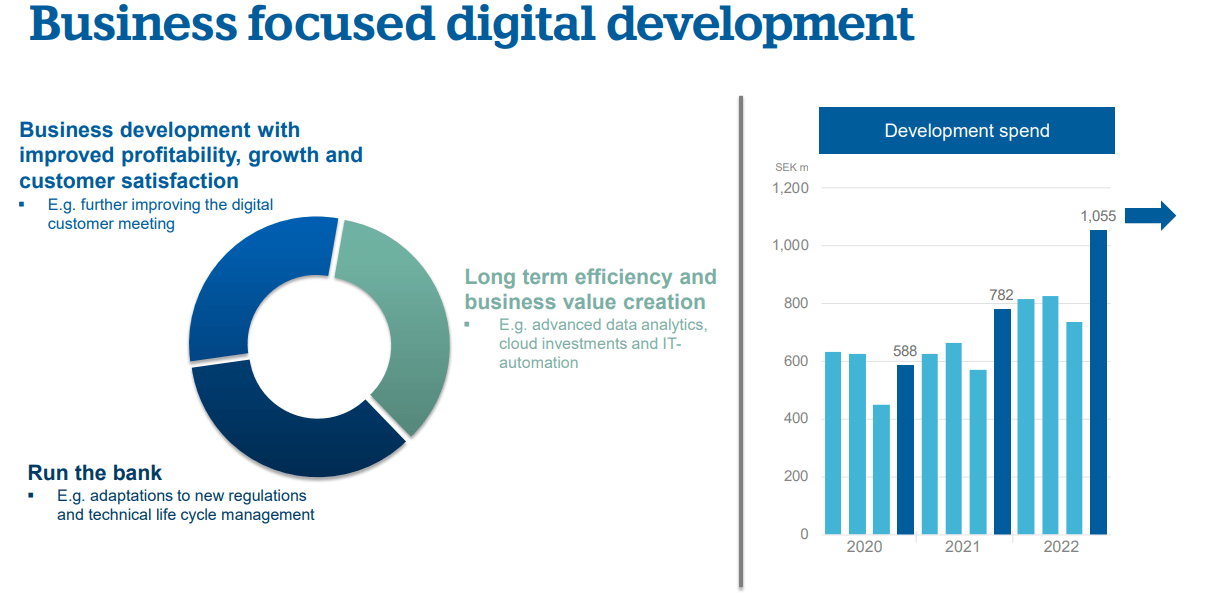

Now, expenses are up, despite the Cost/Income Ratio being down due to higher earnings. The increases in expenses come from development, the company's Oktogonen fund (read my early articles for an explanation of the Oktogonen ownership), and some negative FX. Expenses were up to around 21.2B SEK, which is up from around 20B, but is still up significantly less in relation to income.

Also, most of the increase came from development expenses for the bank, where Handelsbanken is improving its operations and really putting its money where its mouth is.

Handelsbanken IR (Handelsbanken IR)

{kind=link}

I've held this bank for almost as long as I've invested. In fact, it's one of my largest financial position, and returns, while not as great as some, are still quite impressive.

I would be a lot more confident if Handelsbanken was a bank with its main seat in any other nation except Sweden. You may not have followed this as closely, but Sweden is in a bad spot for the next decade or more. The combination of over 10-20 years of what amounts to allowing extensive sub-prime mortgaging and loaning for real estate has left the population indebted, with total mortgages well above 5T SEK. LTV for Swedish mortgage holders are, on average, at over 70% as of 2022 (Source: Finansinspektionen), with additional loans to finance the mortgages themselves at 55-60% of LTV. Most new mortgage holders go in at LTVs from 65-90%, which means that a downturn in the housing and mortgage market which we're seeing the beginning of, is going to put the screws to many homeowners - particularly in the urban areas.

The simple fact is, many people in Sweden with mortgages and homes do not have the income or the financial stability to handle interest rates in their mortgages of higher than 5-6% - and we're currently at an average of 4-5%. The problems have only started here, and given that we've had negative interest rates and are far more indebted than our neighbors or other parts of the EU, the Swedish FED needs to raise interest rates more and faster than its international counterparts to get a handle on what is already a higher, persistent rate of inflation compared to other EU members.

Sweden is in a far worse spot than Germany, France, the UK, or even Poland - and I see it getting a lot worse from here on, as the effects of interest rates that are unsustainable start trickling down the chain.

Being a well-capitalized bank like Handelsbanken is not an advantage in that environment - it's a fundamental requirement.

There is some protection. Due to a massive lack of housing, the market can't fall indefinitely. We're not going to be seeing the banks repossessing property that then will be torn down. What will happen though, is that people likely will be forced to sell and incur losses on property sales, which could really send a lot of people's FICO-equivalent scores which are already bad, even worse. The royal collections agency are already seeing indications of mounting debt and woes, and things are likely to get worse.

I personally have an LTV of 45%, for my primary residence and I'm in a position to immediately ratchet this to 0% if need be, but this is an absolute minority.

If you invest in any Swedish company, especially Swedish finance, you should be aware of this - we're in for years of pain. And the Swedish currency is likely to see continued weakness in the near term - and this needs to be taken into consideration when valuing the bank.

Handelsbanken isn't going anywhere - but it's also in for, as many finance stocks are, certain pressures.

This creates the following situation in terms of valuation.

Handelsbanken Valuation - Attractive, but not as attractive as it might seem

Handelsbanken recently announced a very attractive dividend, including an extra dividend of 2.5 SEK/Share, coming to 8/share for the year, which turns the yield over 8% as the company is currently trading below 100 SEK/share. This corresponds to a payout ratio of no higher than 51% for the ordinary, and 74% in total, with a 10% DGR since the last year. The dividend is paid out in one week, with an Ex-date in 2 days from submitting this article.

Handelsbanken is followed by 20 analysts from S&P Global. The analysts give the company a target starting at 91 SEK and going to 145 SEK. Both are extreme. I consider Handelsbanken a "BUY" at anything below 90-95 SEK, and a "HOLD" at anything above 105 SEK.

I also have conservatively-priced call options covering the entirety of my current position sold at various expiration dates between 2023-2024, covering strikes of 126-139 SEK, which enhance my yield for the stock to about 9-13%, provided the calls don't get assigned. I usually write puts for the bank at ranges of 80-88 SEK for strikes when the yields allow me to make good money off such calls.

Out of 20 analysts, 8 consider the bank a "BUY" here, with 11 "HOLDS". Not one analyst has a "SELL" rating on the bank, and the conservative PT is around 118 SEK. That's far too high for me.

I would say the bank, given the dynamics I described above, becomes a "BUY" at around double digits - and the more double digits it goes, the more a "BUY" it becomes.

That means that you can technically "BUY" Handelsbanken today. I forecast that Handelsbanken will be able to maintain a single-digit growth rate in terms of EPS at least, though I forecast that the earnings will plateau sometime in the next few years, resulting in flat development both in earnings and margins. The dividend yield for the investment is likely to stay at least 5-6%, which means that I view this as an attractive, long-term income investment because it isn't going anywhere.

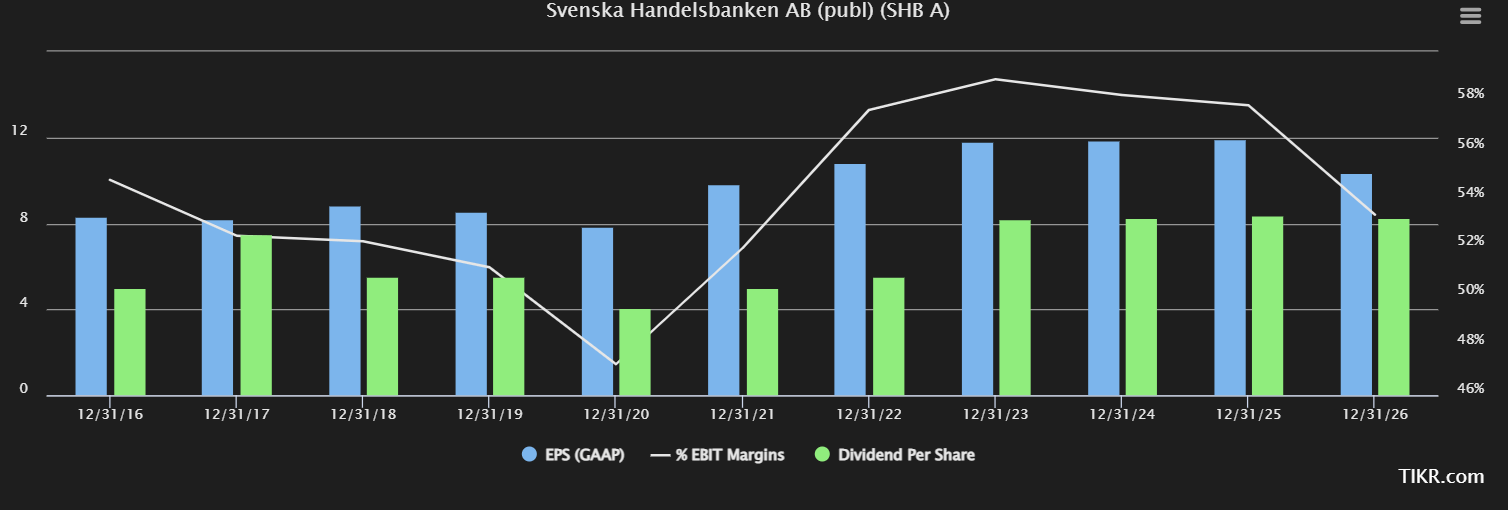

But you need to understand that the 2021-2022 development, I don't see a repetition of that easily over the next few years. Neither do many other analysts.

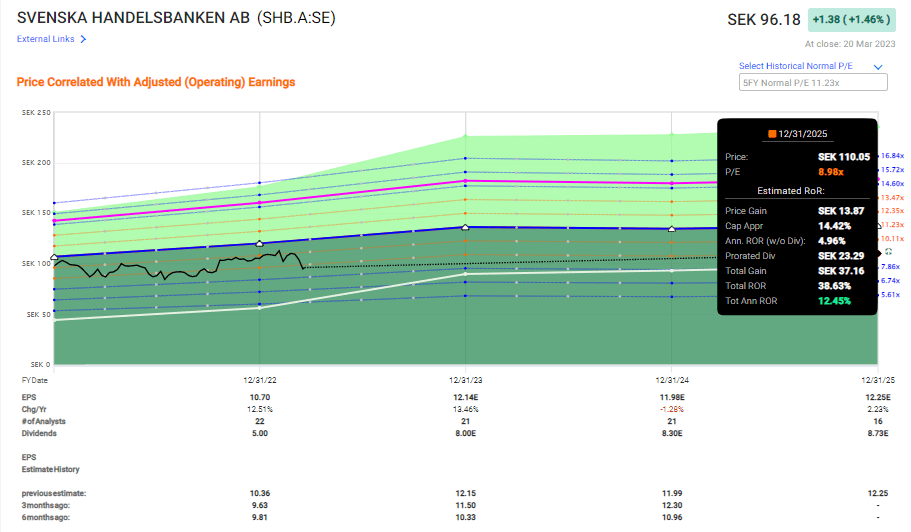

Handelsbanken Forecasts (TIKR.com)

{kind=link}

My main problem with the bank is the multiples the market is demanding for a share of the profits here. While analysts continue to have a major upside of double digits to a high price target of 118 SEK/share for the bank, I view this as too expensive. I can also show this to you by checking the estimates for the company from FactSet. Yes, there is an upside - but no, that upside isn't higher than 110-115 at most, or a 9-10x P/E range, not far above that.

This is despite the company's AA rating.

Handelsbanken Forecast (F.A.S.T graphs)

{kind=link}

I also believe FactSet analysts are underestimating the impact of earnings growth slowing down when some of these issues I mention start trickling down more seriously.

I estimate that to begin in 2Q or 3Q this year, once interest rates in Sweden start breaching 5-6%, and once people increasingly are forced to refinance 2-5 year loans that expire in 2023 and 2024. That's when the "real pain" will be starting - and Handelsbanken won't be immune at that point. These are the current interest rates the bank offers.

Handelsbanken mortgage rates (Handelsbanken)

Once the Swedish FED hikes again, which I would bet money on they will, things will get worse.

For that reason, here is my thesis for Handelsbanken at this time.

Thesis

- Handelsbanken is a theoretically attractive, and fundamentally appealing bank with a sound set of capital safeties, a 5%+ yield, and overall one of the more conservative banks in the entire Swedish banking market. It's also one of my largest financial holdings, and I frequently sell both puts and calls on the bank.

- At a double-digit price inching closer to 90 SEK, I believe this bank offers enough safety and conservative appeal to make it a "BUY" here. But given certain fundamental troubles brewing in EU/Swedish economy, I would be careful where I start "going in" to the bank as an investment.

- I give the bank a conservative PT of 95 SEK/share, which at this point means the bank is actually a "HOLD", but it's a close call.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company may have an upside, but it is not cheap, and given the troubles we're seeing here, I'm saying "No" at this particular price.

Thank you for reading.

For further details see:

Handelsbanken: Returning To One Of My Largest Bank Holdings