HVRRY - Hannover Rück: Great Fundamentals But Wait For A Pullback

2023-09-14 06:37:38 ET

Summary

- Hannover Re is a reinsurance company with strong fundamentals and a defensive business profile.

- The company has a global market share of around 10% in the Property & Casualty market and 8% in Life/Health.

- Hannover Re has a positive financial performance, with strong profitability and a strong balance sheet position.

Hannover Re ( HVRRY ) has great fundamentals within the reinsurance industry, but its quality profile seems to be currently reflected in its share price.

Business Overview

Hannover Re is a reinsurance company based in Germany, being the third largest reinsurer in the world. The company was founded in 1964 and is traded since 1994, while its current market value is about $27 billion and trades in the U.S. on the over-the-counter market. Its largest shareholder is Talanx ( TLLXY ) with a stake slightly above 50%, which is a German holding company with stakes in the financial and industrial sectors.

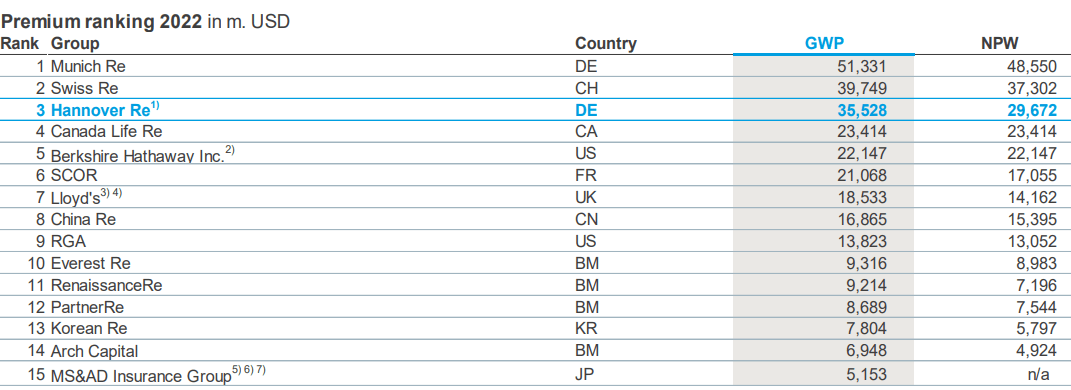

Historically, the company has grown mainly organically, even though it also performed some small bolt-on acquisitions, but its appetite for large M&A deals is rather low. This is not expected to change for the foreseeable future, as the reinsurance industry is somewhat concentrated with the largest five players accounting for nearly half of the market, and large companies in the industry are more likely to acquire smaller players than merge between them. In 2022, the largest reinsurance company measured by gross written premiums was Munich Re ( MURGY ), followed by Swiss Re ( SSREF ), while Hannover Re was not much behind has seen in the following table.

Reinsurance industry (Hannover RE)

{kind=link}

Like its peers, Hannover Re has a defensive business profile and a strong credit rating, being its business priority to maintain a sound financial position rather than seeking growth. This is also not expected to change much in the future, being a key characteristic of reinsurance companies, aiming to have a conservative and safe business profile over the long term.

Regarding its operating segments, Hannover Re operates both in the Property & Casualty (P&C) market and Life/Health segment. In the P&C market, it has a global market share of around 10%, while in Life/Health it holds a market share of about 8%. Over the past few years, both markets have increased in size, measured by gross written premiums, driven by insurance companies increasing demand for risk diversification, the pandemic, and higher prices across the industry. Despite that, the reinsurance industry only accounts for 8% of the whole global insurance industry, thus there is plenty of room to grow over the coming years.

Supported by industry growth and market share gains, Hannover Re’s growth history is quite good and above the sector’s average, given that over the past ten years, it has increased its annual premiums by 9.2% per year, which is a quite good achievement.

{kind=link}

Geographically, the company is well spread across the globe, with North America being its largest market (39% of total premiums), followed by Asia (16%), the U.K. (13%), and Germany (6%).

Despite its strong top-line growth and good business diversification, its bottom-line has been more volatile over the past decade, impacted by claim costs that can rise significantly due to specific events, such as hurricanes, or unexpected issues like the COVID-19 pandemic. This means its bottom-line can have significant swings on an annual basis, even though the company has been always profitable over the last decade.

Additionally, its profitability has also been above its own target over the past few years, measured by the return on equity ((ROE)) ratio, which was close to 12% on average over the past five years while its minimum target was above 9-9.4% during this period. Moreover, Hannover Re is one of the most profitable companies in the industry, given that its peers' average over the past five years was only 5.7%.

ROE (Hannover RE)

This higher profitability level is explained largely by a very efficient operation, given that Hannover Re has an administrative expense ratio of 1.9%, while its peers' average is close to 5%, while its total expense ratio was 28.9%, on average, over the past five years (vs. more than 30% for its peers during the same period). This shows that Hannover Re also has strong underwriting criteria, which is critical to maintain a strong operating profitability over the long term.

Going forward, the company’s strategy is not expected to change much, remaining focused on organic growth and maintaining its lean operating model, returning excess capital to shareholders and potentially performing some small bolt-on acquisitions if the opportunity arises.

Financial Overview

Regarding its financial performance, Hannover Re has a positive track record, being able to have much less earnings volatility than its closest peers and an above-average profitability level. This is justified by the company’s operating model, having an efficient business and strong and centralized underwriting criteria, which is key to have consistent results over the long term.

In 2022 , Hannover Re has maintained a positive operating momentum supported by higher premiums in both P&C and Life segment, plus higher investment income. Reinsurance renewals have been positive across the industry for established players, as higher cost of capital has led alternative players to be less competitive, being an important support for higher prices especially in the P&C segment.

Taking into account this backdrop, Hannover Re’s gross written premiums amounted to €33.2 billion in 2022, an increase of nearly 20% YoY, boosted by higher pricing and forex tailwinds. Adjusted for currency moves, gross written premiums increased by 13% YoY, still a very good outcome. Due to good cost control despite the inflationary environment, its earnings before interest increased by 20.3% YoY to more than €2 billion in the past year, while its net income was €1.4 billion (+14.2% YoY).

On the other hand, like most of its peers, Hannover Re’s investment portfolio is heavily exposed to bonds (both government and corporate bonds), accounting for some 83% of its asset allocation, which were naturally negatively impacted by rising interest rates over the past year. This is reflected negatively in the company’s Other Comprehensive Income and in its net book value, which decreased by 32% YoY to €67 per share at the end of 2022.

Its ROE, a key measure of profitability in the insurance sector, was above 14% in 2022, much higher than its target of at least 9.4%, showing that Hannover Re’s profitability is quite good and higher than compared to its peers over the cycle, as shown in the next graph.

ROE vs. peers (Hannover RE)

During the first six months of 2023 , Hannover Re’s operating momentum remained strong, even though its growth was more moderate than compared to 2022. Pricing remained strong in the P&C segment (revenues up by 6.6% YoY), but there was some softness in the Life/Health segment (revenues -1.5% YoY), leading to overall revenues of €12.3 billion in H1 2023, up by 3.9% YoY.

Its net income was €960 million in H1 2023, up by 17.8% YoY, and its ROE was 21% which is much higher than its target of at least 10.8%. This very good results is justified by lower large losses from catastrophe events than budgeted, allowing the company to release reserves in the period, which is a boost to earnings.

For the rest of the year, the company expects positive price and volumes developments in the P&C segment to continue, which should be the major support for overall reinsurance revenue up by more than 5% in the year. Its investment income is also expected to grow compared to the previous year, which should lead to a net income above €1.7 billion, representing annual growth of about 21% YoY.

Regarding its capitalization, Hannover Re has a strong balance sheet position, like most of its closest peers, given that its Solvency II ratio was 270% at the end of last June. This is an increase of 18 percentage points compared to its level at the end of 2022, and much higher than its internal target of at least 200%.

This means that Hannover Re has an excess capital position and can return capital to shareholders, being a strong support for its dividend. As can be seen in the next graph, the company had a positive dividend history based on ordinary dividends, while its strategy is to distribute special dividends related to its financial performance.

{kind=link}

Its last annual dividend, related to 2022 earnings, was €6 per share, representing an annual increase of 4.3%. This represented a dividend payout ratio of less than 50%, which is a relatively low payout ratio within the European insurance sector, showing that the company is somewhat conservative in its dividend growth, preferring to deliver a growing dividend over the long term rather than making big changes on an annual basis.

At its current share price, Hannover Re offers a dividend yield of less than 3%, and it only pays one dividend per year, reducing its income appeal compared to other alternatives. Going forward, according to analysts’ estimates, its dividend is expected to grow gradually over the next few years to more than €8 per share by 2026, thus Hannover Re is not expected to become a high-dividend yielder over the coming years.

Conclusion

Hannover Re is a company with strong fundamentals within the reinsurance industry and its growth prospects are positive over the near future, but this seems to be priced-in given that its shares are currently trading near its all-time highs. Moreover, its quality profile is also reflected in its valuation, taking into account that it’s currently trading at 2.7x book value, at a premium to its historical average of about 1.9x book value, and also a multiple that is above its peer’s average. Therefore, even though Hannover Re is a great company in the insurance sector, investors should wait for a better price to enter into its stock.

For further details see:

Hannover Rück: Great Fundamentals But Wait For A Pullback