THG - Hanover Insurance: Lower Combined Ratio Encouraging But Further Net Income Growth Needed

2023-11-14 11:27:23 ET

Summary

- Hanover Insurance Group has seen a decrease in the combined ratio (excluding catastrophic losses), which is encouraging.

- However, return on equity remains negative.

- I take the view that Hanover Insurance Group needs to see significant net income growth to justify further upside.

Investment Thesis: I take the view that the stock needs to see further net income growth for a bullish view to be justified.

In a previous article back in August, I made the argument that Hanover Insurance Group (THG) needs to see a substantial rebound in earnings and recovery in the Personal Lines segment to justify upside in the stock.

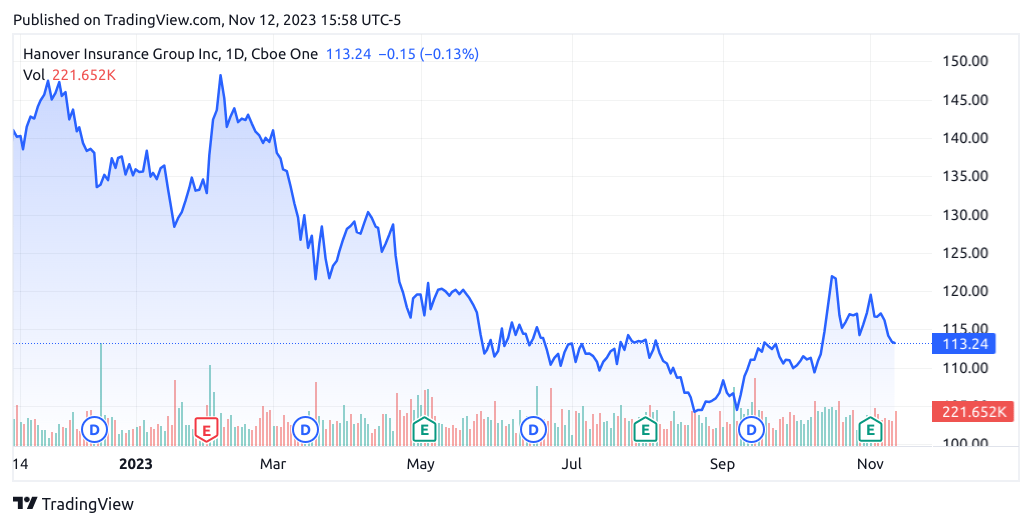

Since then, the stock has ascended slightly to a price of $113.24 at the time of writing:

{kind=link}

The purpose of this article is to assess whether Hanover Insurance Group has the ability to see continued growth from here taking recent performance into consideration.

Performance

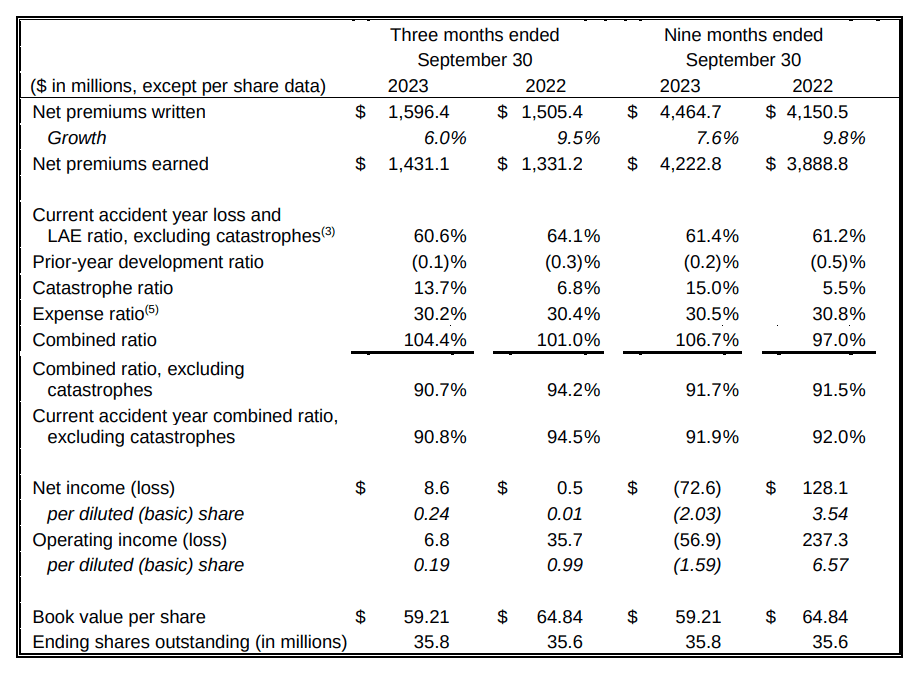

When looking at Q3 2023 earnings results for Hanover Insurance Group (as released on November 1), we can see that growth in net premiums written slowed to 6% from that of 9.5% YoY.

{kind=link}

Additionally, we also see that the combined ratio (or the ratio of incurred losses and expenses over the premium earned) has increased to 104.4% in Q3 2023 as compared to 101% for the same quarter last year.

With a combined ratio of over 100%, this indicates that Hanover Insurance Group is now incurring more in losses and expenses associated with funding claims compared to the degree of premiums collected - the fact that the combined ratio is now even higher is a cause for concern.

On the other hand, we also observe that when excluding catastrophes - the combined ratio actually fell from 94.2% to 90.7%. Taking this into consideration, a higher combined ratio is not of as much concern - as this indicates that Hanover Insurance Group is in fact boosting the degree of premiums collected compared to that incurred in losses and expenses.

Additionally, catastrophe losses of $44.6 million in Q3 2023 were primarily driven by hail and wind damage in the Midwestern United States, as compared to losses of $32.7 million in the prior-year quarter. From this standpoint - I take the view that upon seeing catastrophe losses return to more typical levels in subsequent quarters - we should see the combined ratio decrease accordingly.

When looking at the combined ratio (excluding catastrophes), we can see that while the combined ratio was higher than the year prior for Q1 and Q2 - this has reduced substantially for Q3. A similar result in Q4 would be encouraging.

Figures sourced from previous Hanover Insurance Group Earnings Releases (Q1 2019 to Q3 2023). Heatmap generated by author using Python's seaborn visualisation library.

In my view, if we see a lower combined ratio in the upcoming quarter, then it would further indicate that Hanover Insurance Group has the capacity to continue growing premiums at a faster rate than that of losses and expenses. This, along with further growth in net income - could see the stock ascend further. We have already seen that net income has made a strong recovery to $0.24 per diluted share as compared to $0.01 in the prior-year quarter.

My Perspective

As regards my take on the above results and the implications for the growth trajectory of the stock going forward, I had previously pointed out that the Personal Lines segment had been placing pressure on earnings given the impact of both catastrophic losses and higher costs.

{kind=link}

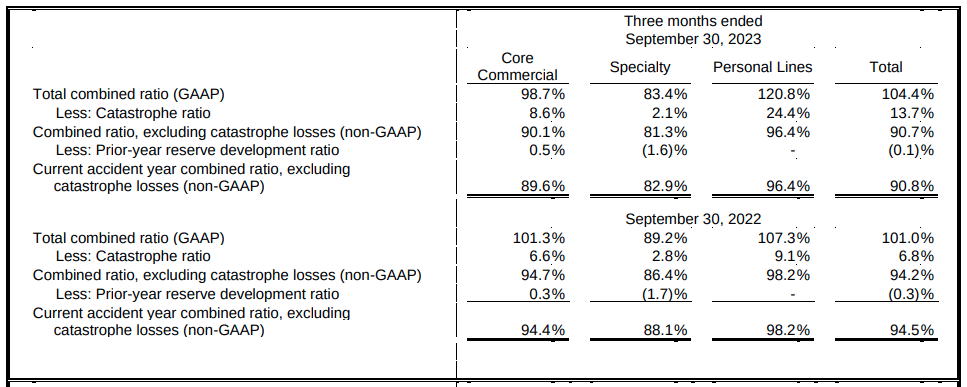

However, we can see that in spite of the segment having the highest catastrophe ratio - the current accident year combined ratio in the absence of catastrophe losses is 96.4%.

Moreover, renewal price increases for Personal Lines averaged 18% - in contrast with average rate increases of 10.7%. In this regard, despite the fact that this segment has seen a higher degree of catastrophic losses as compared to the Core Commercial and Specialty segment - I take the view that strong price growth has the capacity to significantly boost premium growth in turn and ultimately allow for further growth in net income.

From a valuation standpoint, we can see that the price to book ratio is trading near the upper end of the range that we have seen over the past five years - while return on equity has gone into negative territory for 2023.

Price to Book

ycharts.com

Return on Equity

ycharts.com

In this regard, my view on Hanover Insurance Group is that while the recovery in net income and the decrease in the combined ratio for this quarter has been encouraging - net income is still negative on a nine-month basis and this is reflected by a negative return on equity (net income/shareholder's equity).

In my view, Hanover Insurance Group needs to demonstrate a strong trajectory of recovery in net income over the next two to three quarters. A lower combined ratio will likely not be sufficient to induce significant upside in the stock from here.

Risks

In terms of the potential risks to Hanover Insurance Group at this time, I take the view that catastrophe losses and the impact of higher costs could continue to place pressure on the stock in the short to medium-term.

While premium growth has continued, we see that the rate of the same has slowed in the past year. Should we see elevated catastrophe losses in upcoming quarters, then this combined with the effect of higher costs could prevent further net income growth - which would likely have a negative effect on stock price growth.

Additionally, the Personal Lines segment is significantly dependent on performance across the personal auto segment - which 1) has been seeing potential car owners delay purchases given the strong price increase in newer models, and 2) with car insurance premiums having hit a record high - it is likely that Hanover Insurance Group could see upward pressure on churn as some customers attempt to switch providers.

Conclusion

To conclude, my overall view on Hanover Insurance Group is that while premium growth has continued and the drop in the combined ratio for this quarter is encouraging - the company still faces significant risks which could hinder growth in net income.

In this regard, I take the view that the stock needs to see further net income growth for a bullish view to be justified.

For further details see:

Hanover Insurance: Lower Combined Ratio Encouraging, But Further Net Income Growth Needed