HLAGF - Hapag-Lloyd: A Quality Holding In A Challenging Environment

2023-03-08 04:39:34 ET

Summary

- Hapag-Lloyd reported record earnings and a huge dividend. Both are not sustainable in the short run.

- Apart from softening rates, the company is also facing increased operational costs fueled by strong inflationary pressures.

- They do have a huge liquidity reserve and a well-laddered liability schedule.

- I believe that the current valuation reflects the upcoming dividend and that after the ex-date, the share price will not return to the current levels.

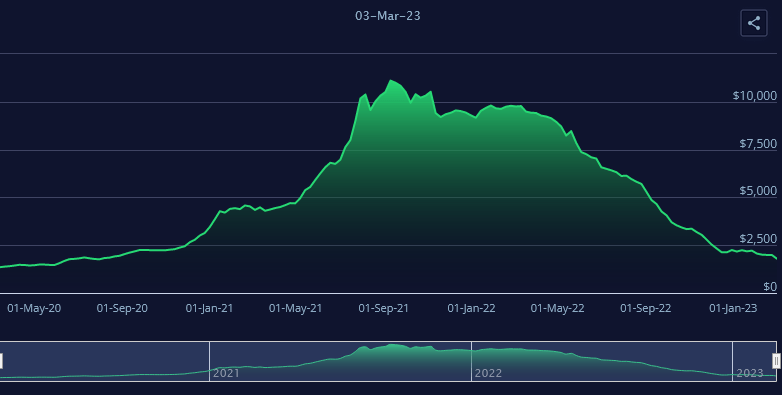

Container liners like Hapag-Lloyd (HLAGF) and ZIM ( ZIM ) have been excessively under the spotlight during the recent months, as container freight rates have eased substantially from record levels observed in 2021, as it is shown in the graph listed below. Caught in a challenging situation, companies like those mentioned earlier have seen their share prices decline rapidly.

Freightos Baltic Index, data from March 3rd, 2023 (Freightos.com)

{kind=link}

A few days ago, Hapag-Lloyd reported total revenues of 34.6 billion euros, earnings per share of 98.89 euros and an EBITDA of EUR 20 billion. There's no doubt that these are exceptional figures, supported by the high freight rates recorded in 2022. However, there is a catch: Guidance for 2023 was quite softer than the previous year. In fact, for 2023, Hapag-Lloyd expects an EBITDA figure in the range of EUR 4 to EUR 6 billion, which signifies a YoY EBITDA decrease in the ballpark of 70%.

But is this new guidance actually something to be concerned about, from a viability standpoint? The following chart implies that it is not. As we can see, years 2021 and 2022 were record breakers in terms of freight rates, and, consequently, in terms of financial results.

Hapag-Lloyd EBITDA in recent years (Hapag-Lloyd's FY 2022 Investor Presentation)

We can also see that the proposed FY 2023 earnings guidance is well above the EBITDA figures observed in the years 2018 to 2020. In the recent earnings call , it was stated that the company expects profitability of the current year to be "front - loaded", due to contracts from 2022 getting close to expiration.

What's the problem then?

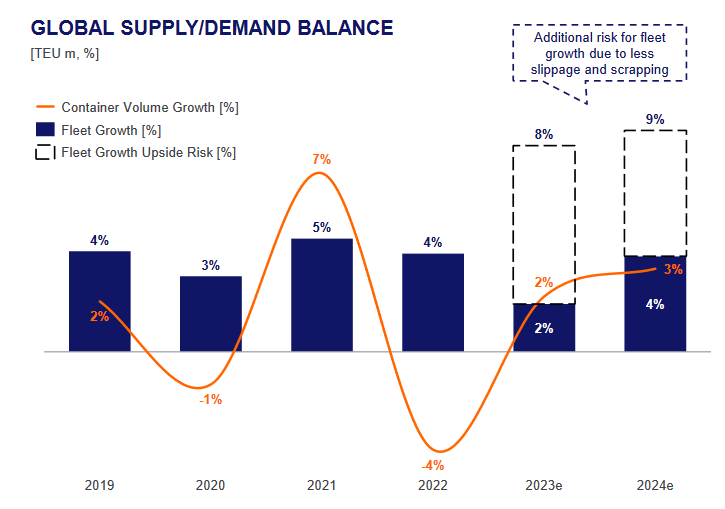

Container freight rates are expected to continue to remain away from the record levels we saw in the two previous years. There is an apparent supply versus demand growth issue here, with the former clearly outpacing the latter. As the following graph indicates, global container fleet growth could be even fourfold higher than container demand, which will compress rates even more.

Global Supply and Demand Balance (Hapag-Lloyd FY 2022 Investor Presentation)

{kind=link}

In fact, while slow steaming, slippage and scrapping will artificially smooth out this imbalance partially, a decrease in total TEU capacity is practically inevitable. Already, 6.2% of the global container capacity has become idle , which is a trend that is expected to continue at a harder pace. In addition, projections regarding 2024 are based on specific assumptions of slippage and scrapping. When asked about that subject in the earnings call, Hapag-Lloyd's CEO, Rolf Jansen said that there's no way a sensible projection will be made regarding 2024 freight rates. This statement clearly implies uncertainty in all those assumptions that define freight rates.

An additional problem that container liners face is the increase in their operating costs, due to the inflationary pressures worldwide. While in 2022 costs like bunker, storage and handling were a pain in the neck, the company expects the latter two to normalize relatively quickly during 2023. However, bunker prices and time charter costs are expected to remain elevated for a longer period.

The sum of all good things

Hapag-Lloyd is a container shipping giant and, as such, they know how to get prepared for shipping market cycles. The company took advantage of the two strong previous years, and raised its liquidity to almost EUR 17 billion. The total market capitalization of the company is approximately EUR 52 billion. It is important to note that the company holds additional cash into time deposits, with duration of more than three months, which are not included in its total liquidity figure.

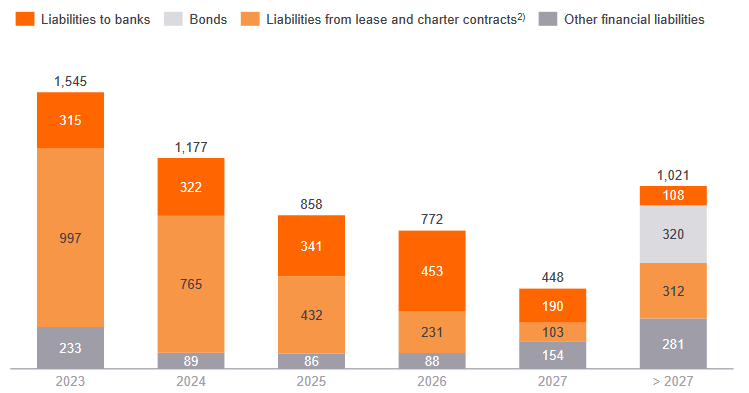

Hapag-Lloyd Debt Profile (Hapag-Lloyd FY 2022 Investor Presentation)

{kind=link}

As we can see in the chart listed above, the company has EUR 1.5 billion of debt and charter liabilities in 2023, which are exceptionally covered by their liquidity reserves, at the end of 2022.

For the full year 2022, the company distributed EUR 63 per share in dividends of their common share, representing a 65% payout ratio, based on the EPS figure of EUR 98.89. Given the FY 2023 EBITDA guidance of 4 to 6 billion euros, and assuming a lower payout ratio of 50%, we can estimate a FY 2023 dividend of EUR 14 per common share, using some back of the envelope calculations. This figure corresponds to a quite reasonable dividend yield in the ballpark of 5%.

Finally, dividend investors should also note the shareholder structure of the company. As we can see, the majority of the company's float is owned by institutional and long term investors, with free float being only 3.6%. Moreover, it is encouraging to see that entities other than speculative funds have significant stakes in the company. For instance, the City of Hamburg owns almost 14% of the company, while Qatari and Saudi Arabian sovereign funds also own double digit chunks of Hapag-Lloyd.

Hapag-Lloyd Shareholder Structure (Hapag-Lloyd FY 2022 Investor Presentation)

Bottom Line

While I like the management and business model of Hapag-Lloyd, this time I will remain on the sidelines. The container shipping market fundamentals create a challenging environment for the company, and the present valuation does not reflect that. I think that the company is artificially kept in its current valuation, due to the proposed dividend, and that after the ex date, its share price will not recover to its current level. So, I would hold my hypothetical stake or sell it, depending on factors such as investment time frame and dividend taxation.

For further details see:

Hapag-Lloyd: A Quality Holding In A Challenging Environment