HLAGF - Hapag-Lloyd: Headed For Near-Term Losses

2023-11-28 12:52:42 ET

Summary

- Hapag-Lloyd isn’t being spared from a vicious cyclical downturn in the shipping industry.

- More capacity is still coming onstream with little demand respite, so it could be a while before the supply/demand balance returns.

- The stock may have de-rated but isn't cheap enough to warrant a position.

I’ve been cautious about shipping company Hapag-Lloyd ( OTCPK:HLAGF ) for a while now (see prior coverage here ), largely on account of a sector-wide downturn. If the latest quarterly miss and guidance downgrade (implying deeper Q4 EBIT losses) were anything to go by, these concerns still stand.

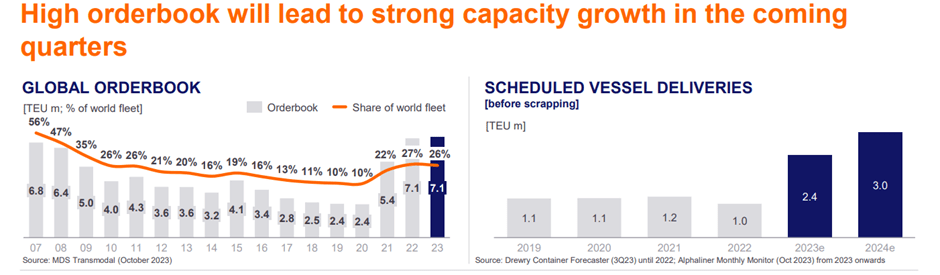

In sum, the company, like many of its peers, is getting hit on both sides of the P&L - lower freight rates and higher operating costs. This likely won’t change for the industry heading into 2024, mainly due to a capacity 'tidal wave' coming onstream, the result of industry players previously extrapolating pandemic-driven demand levels too far into the future. Demand-side factors aren’t favorable either - US/EU rate hikes are likely done, but global trade could remain cyclically weak (perhaps even structurally for China) as the lagged impact of monetary tightening works through the system.

The one positive here is that global liners like Hapag-Lloyd and key peer A.P.Møller–Mærsk ( OTCPK:AMKAF ) are proactively deploying their excess cash balances into reducing their cyclical business profile. While more predictability tends to drive a higher multiple over time, these are long-term projects and won’t override the inherent volatility of their core income streams. So, pending clarity into supply discipline and firmer demand trends, I would be very hesitant about underwriting a cyclical earnings recovery for Hapag-Lloyd, particularly with the stock still priced at a ~10% premium to book.

Feeling the Squeeze on Both Sides of the P&L

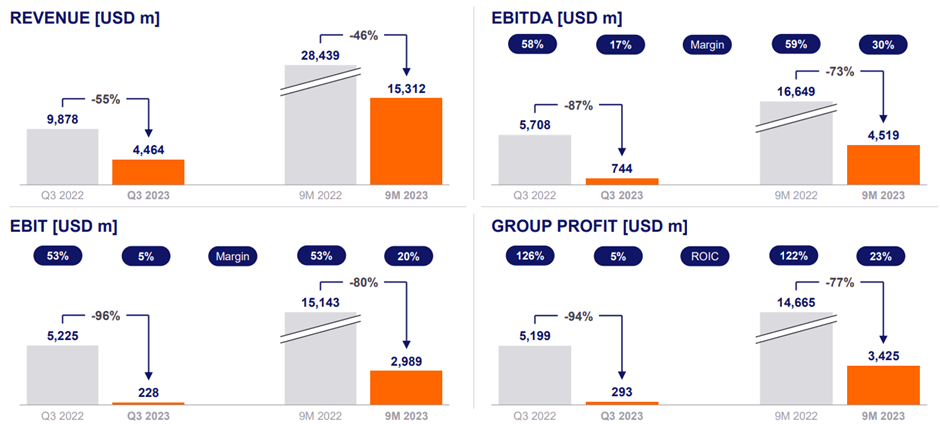

Hapag-Lloyd’s Q3 results disappointed across the board, with adjusted EBITDA and EBIT falling well below consensus expectations at $744m and $228m, respectively. The key culprit was sharply lower freight rates (down 58% YoY), which more than offset any volume growth (+5% YoY). By segment, the core liner EBIT margin stood at 5% (vs. high-teens YTD), below best-in-class Asian peer COSCO SHIPPING ( OTCPK:CICOF ) (~7% margin) but well ahead of Maersk’s negative shipping segment margin. Interestingly, HL also broke out its terminal and infrastructure business this quarter (mainly acquired stakes in terminals), signaling its diversification efforts into higher-margin, less cyclical revenue streams.

{kind=link}

Hapag-Lloyd

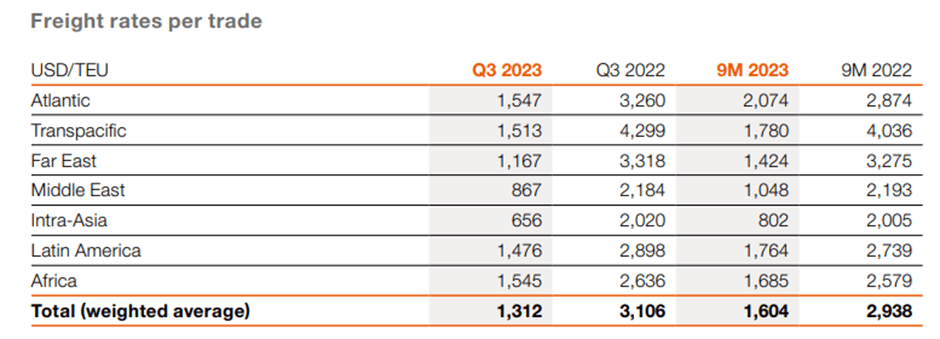

Digging deeper into the Q3 report, it’s hard to look past the worrying decline in dollar-denominated freight rates. The -58% YoY rate decline is not only faster than shipping peers but also stands in stark contrast with key freight forwarder Kuehne + Nagel ( OTCPK:KHNGF ), where management has rebalanced volumes towards higher-value cargo to protect margins. Hapag-Lloyd’s mitigation strategy, by comparison, remains limited to locking in multi-year contracts and maintaining a diversified geographic exposure. Given the viciousness of this shipping downcycle (freight rates are below cost in many of Hapag-Lloyd’s trade lanes), this likely won't be enough to protect Hapag-Lloyd’s P&L from a rapidly deteriorating spot market.

{kind=link}

Hapag-Lloyd

Management also seems to have limited options on the cost side, with inflation already driving key operating cost lines well above pre-COVID levels. Structural ESG-related cost pressures only add to the P&L woes. In essence, Hapag-Lloyd is being squeezed on both sides of the income statement and will probably, like Maersk , have to make some tough personnel decisions in the coming months.

Narrowed Guidance Indicates More Headwinds on the Horizon

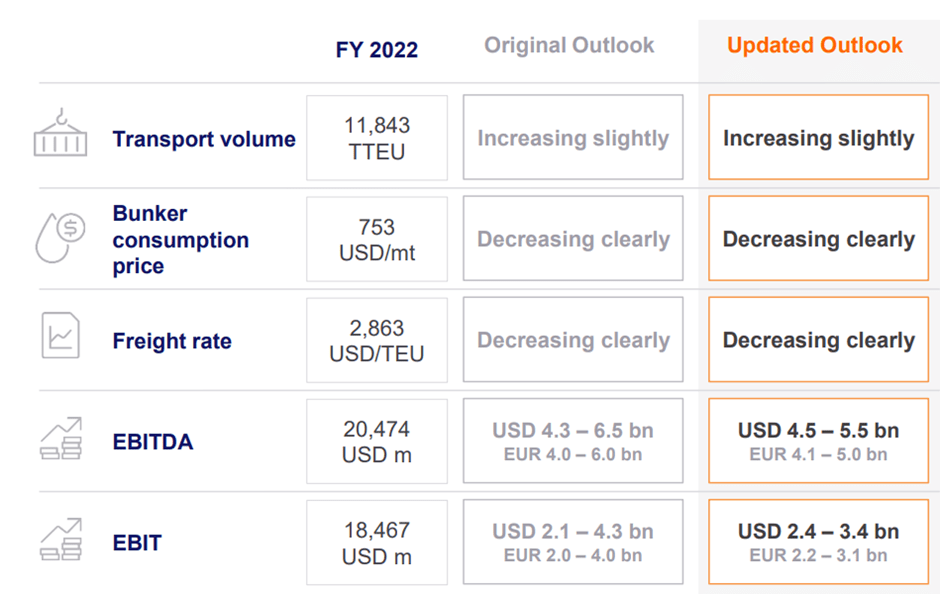

Management did a decent enough job of managing expectations on the post-earnings call, cautioning against a swift demand recovery anytime soon. In line with this view, Hapag-Lloyd has essentially rebased its EBITDA guidance lower to EUR4.1-5.0bn (vs EUR4.0-6.0bn previously), implying a 77% YoY decline at the midpoint. Similarly, the full-year EBIT guidance range has been narrowed to EUR2.2-3.1bn (down from EUR2-4bn previously), implying a Q4 >EUR100m EBIT loss amid more freight rate pressures. This seems prudent to me – across virtually all its key routes, freight rates are down over 50%, and in many cases, shipping lines are already below cost. This competitive intensity isn’t going to ease anytime soon, with management citing supply growth outpacing demand growth through 2024 as well.

{kind=link}

Hapag-Lloyd

Against a slowing demand backdrop, management hasn’t been able to contain an inflating operating cost base either. This needs to be significantly rightsized at some point (think massive job cuts a la Maersk) to mitigate deep losses in the coming quarters. Further complicating the near-term P&L trend are new European antitrust regulations blocking the Consortia Block Exemption Regulation (CBER) extension, which may lead to less cost-optimized route operations and by extension, higher costs. Plus, there’s the ever-present structural ‘green’ cost headwind, for instance, the usage of pricier low-sulfur bunker fuel (+15.4% YoY in Q3). Unless we see a demand recovery (unlikely given where global PMIs are currently tracking ), earnings won’t be recovering any time before late 2024 or 2025 once smaller players get shaken out and the industry regains its supply discipline.

{kind=link}

Hapag-Lloyd

Headed for Near-Term Losses

The shipping industry isn’t a great place to be right now, as illustrated by the recent selloff in industry leader Maersk (see prior coverage here ) and Hapag-Lloyd following disappointing quarterly reports. While we’ve also seen some big resets, with Q4 losses now the consensus expectation across the industry, I wouldn’t be too quick to call a bottom.

Freight rates are, after all, running below breakeven in key routes, implying little room to pass on operating cost pressures. The capacity ‘tidal wave’ isn’t slowing down either, so expect more of the same through next year until we see some demand-led support for freight rates. To be fair, Hapag-Lloyd's valuations have de-rated in recent months - though not nearly enough to compensate for the challenging outlook at the current ~1.1x book value. Without a wider margin of safety (e.g., Asian peer COSCO Shipping trades below net cash ), I don’t see a compelling reason to be long here.

For further details see:

Hapag-Lloyd: Headed For Near-Term Losses