HPGLY - Hapag-Lloyd - Shipping In A Downcycle I Say 'HOLD' For Now

2023-11-13 15:33:26 ET

Summary

- The shipping industry has faced challenges and upsides in the past three years, leading to high stock prices for companies like Maersk and Hapag-Lloyd.

- Hapag-Lloyd is a German shipping company that has a strong balance sheet and cash position, but is facing a downturn in revenue growth.

- The company is adjusting its business to reflect the challenging market environment and expects a normalization in earnings, but the industry may face overcapacity in 2024.

Dear readers/followers,

I've been writing about the shipping industry and the challenges and upsides that it faces through my articles about Maersk, a Danish massive business in shipping worldwide. A reader contacted me and asked me to take a look at his bet on the industry, Hapag-Lloyd Aktiengesellschaft ( OTCPK:HPGLY ).

The entire shipping industry has, for the past 3 years, faced significant challenges and upsides. Due to supply chain challenges, the companies within this segment traded at multi-year and even all-time highs during 2022. Maersk was no exception to this, and neither was Hapag-Lloyd.

However, when it comes to shipping, a whole lot of the trend has to do with freight rates and prices for reefers/other pricing trends. This upturn in 2022 has left many of these companies - those in good positions - in extremely advantageous positions in terms of their balance sheet and cash. Most of these companies have been reinvesting this money in addition to paying out truly massive dividends.

I am long in Maersk - I'm not yet long in Hapag-Lloyd - but I'm looking at the company to see if we can invest here, basically in the face of a massive downturn in year-over-year revenue growth.

Let's look at what we have going for us here.

Hapag-Lloyd - Hamburg Shipping with a 50%+ dividend yield

While the name would suggest at least in part British origins for the company, that is not the case. Hapag-Lloyd is a purely German international shipping and container transporter - formed as early as 1970 when Hamburg American Line and Norddeutscher Lloyd merged. These companies in turn go back to the 1840s and 1850s. Over the course of its long history, Hapag-Lloyd has gone through multiple iterations, such as for some time being a part of TUI AG ( OTCPK:TUIFF ), which I also cover on Seeking Alpha. This was the case until the GFC and 2009 when TUI unloaded a majority stake to PI in Hamburg in both 2009 and 2012.

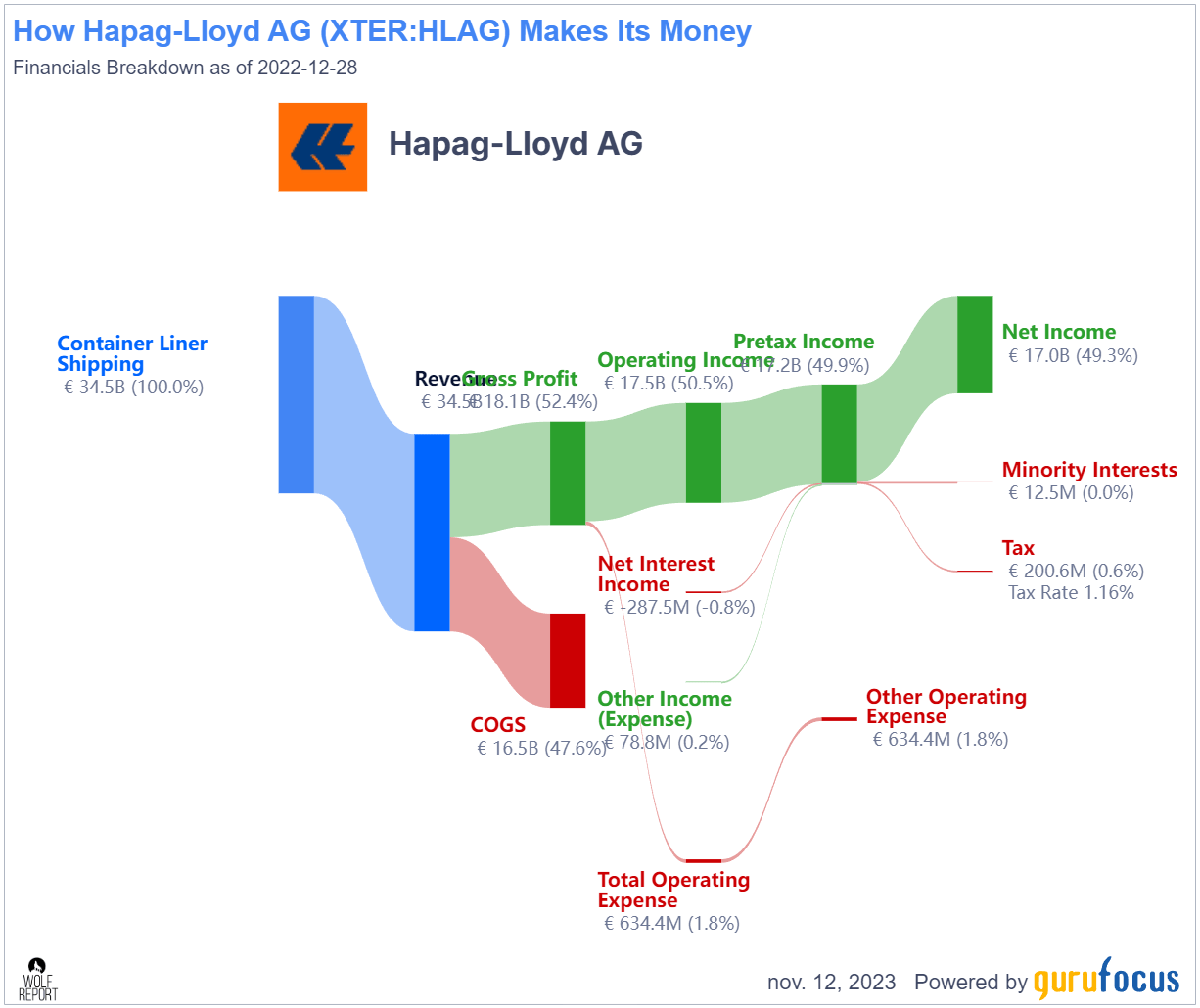

Hapag-Lloyd has also absorbed CSAV, CP ships, and the United Arab Shipping Company. Some basic data. The company manages revenues of over €25B per year, and on paper, has one of the most impressive business models that I have ever covered.

Hapag-Lloyd Business Model (GuruFocus)

{kind=link}

Of course, as you can see above, that's the 2022A results - which as mentioned, were somewhat outsized and unlikely to be repeated - otherwise, I'd probably consider allocating 20-30% of my entire portfolio to this company if this was in any way sustainable. We can look back historically to see just how this company typically performs, which is of course very different.

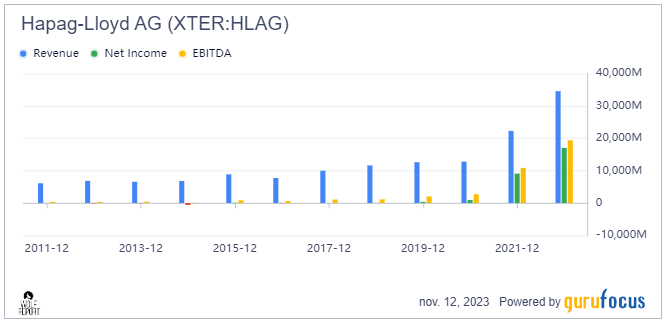

Hapag-Lloyd revenue/net (GuruFocus)

{kind=link}

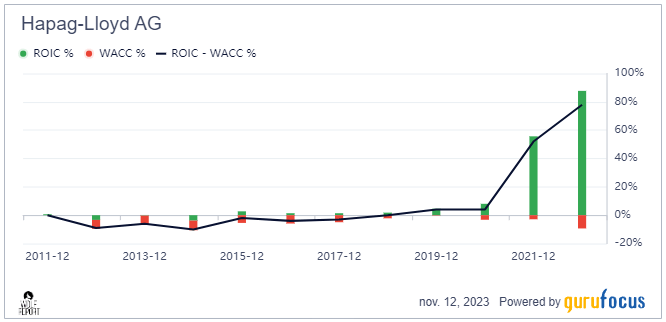

The company, as of the result of 2021-2022 is also extremely cash-heavy. At the YE 2022, the company recorded over $16B of cash/equivalent on its balance sheet, leading to the company being a net cash company as opposed to having debt. Another way to illustrate the non-sustainability of these latest results is to look at ROIC.

Hapag-Lloyd ROIC/WACC (GuruFocus)

{kind=link}

Ever since then, analysts, including myself, have been trying to estimate when we hit a shipping trough and when the price for the company is "cheap enough" to start investing in.

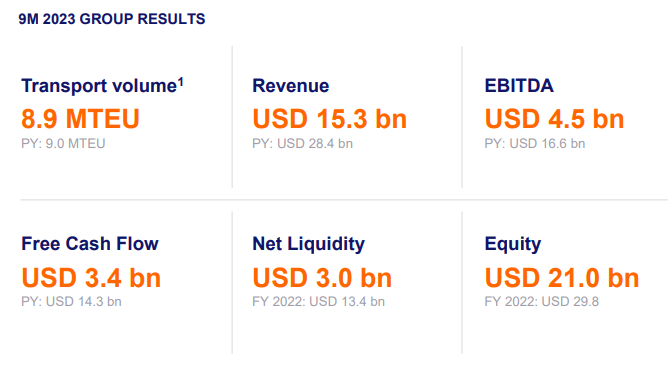

We have, as of writing this article, 9M23 results. Take a look at the container volumes. Despite growing container volumes as supply chain challenges are easing, the sheer decline in spot prices and contract prices are, no matter what these companies are doing , pressing revenues, margins, and other KPIs back to pre-pandemic or slightly above pre-pandemic levels. (Source: Hapag-Lloyd 3Q23 IR )

Hapag-Lloyd IR (Hapag-Lloyd IR)

The company even admits this very clearly, with the exact wording of "Freight rates remain under pressure leading to an increasingly challenging market environment".

Obviously, Hapag-Lloyd is adjusting its business to reflect this reality - or perhaps simply going back to "business as usual". We're seeing launches of new JVs, we're seeing a solid high order book (as reflected by container volumes), and we're seeing demand recovery - but the message is clear. Shipping supply will outstrip demand in both 2023 and 2024, making active cost management an inevitable necessity (Source: Hapag-Lloyd IR).

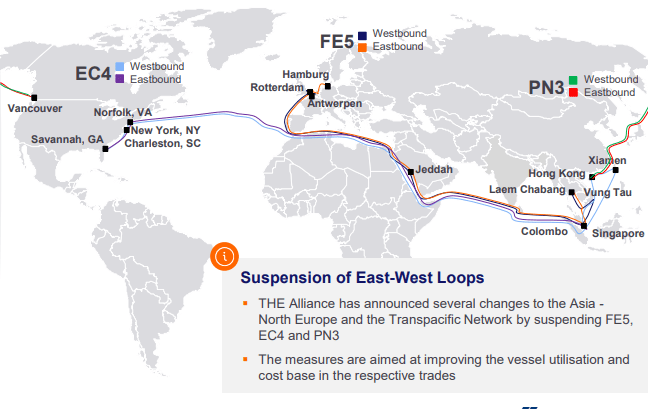

The company now sees the expected normalization in earnings - and has narrowed its 2023E outlook as a result of it. EBITDA is currently expected, for the full year, between $4.5B to $5.5B with EBIT up to $3.4B. Hapag-Lloyd is increasingly making its routes more and more efficient, by suspending several loops.

Hapag-Lloyd IR (Hapag-Lloyd IR)

{kind=link}

Much like with Maersk, Hapag-Lloyd is diversifying through a terminal and infrastructure business, where it tries to diversify its revenue streams and overall cash flows. To preserve capital and for other reasons, company expansions come in the form of JVs, such as the recent push into Brazil, the largest SAS economy with a constantly growing and in-demand transport sector. The company expects the first sailing to be initiated in January of 2024, with Norsul as a strong JV partner, where it will manage infrastructure on the "Norcoast", with weekly service offering for sabotage and feeder cargo, and integrated container transport and inland services. (Source: Hapag-Lloyd 3Q23 IR )

Much like Maersk, the top-and-bottom line results showcase exactly just how severe this normalization is.

Hapag-Lloyd IR (Hapag-Lloyd IR)

{kind=link}

Normalization trends are more than 50% on the top line, 85% on the EBITDA basis, 96% on EBIT, and 77-94% on group profit. Much like Maersk, Hapag-Lloyd was never "supposed" to be trading as high as that - much like during Tech mania, things were trading at 200-300x forward P/E and had some investors convinced that, yes, these are "fair" type valuations.

They weren't - and now we're going back down.

The best thing to hope for is that Hapag-Lloyd has used its cash influx well to reduce risk, reduce leverage, and really invest in things that are going to improve operations.

Hapag-Lloyd going forward, is going to be among the leaders in Liner Shipping and with a small appeal in Terminals and infrastructure. The latter portion is still at an almost laughably low level - we're talking sub-$100M in revenues compared to $28B+ in revenues for the liner shipping segment. But it's now in operation, and expected to grow.

The current decline of freight rates in terms of USD/TEU is down from a high of $3,100+ in 3Q22, to $1,300 in 3Q23 - but unit cost economics are at least somewhat improved due to better cost management and improved (or lack of) port congestion. The company made a massive, truly massive dividend payout that drained the company of $12B+ worth of cash, leaving the business at a cash flow of $6.7B compared to $16.2B cash and equivalents in December of 2022. (Source: Hapag-Lloyd 3Q23 IR )

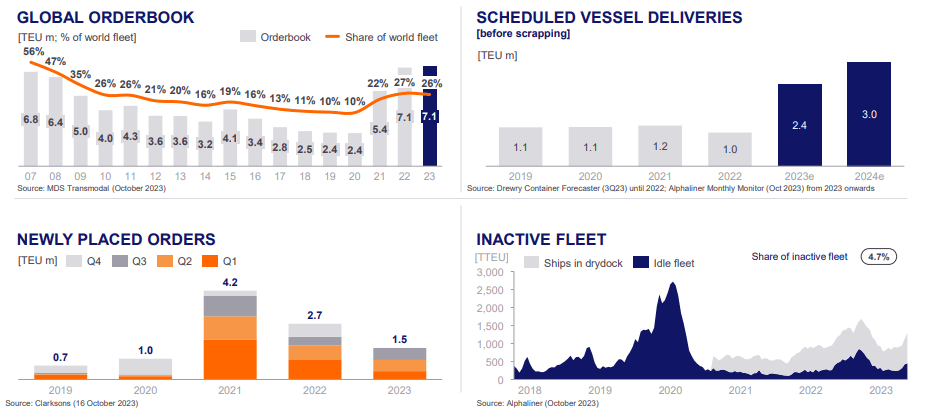

The company is still a net cash company, with over $3B worth of liquidity. This means Hapag-Lloyd has a leverage of 0x, financial debt of $5.7B. However, the global order trends and order book are very solid - and the company has several vessels incoming which will improve fleet economics in expectation for an eventual demand peak once again.

Hapag-Lloyd IR (Hapag-Lloyd IR)

{kind=link}

There's a very strong inflow of new capacity ships in the next few years, only somewhat offset by scrapping and slippage.

For the industry as a whole, and for Hapag-Lloyd specifically, I want to give you the following quote to consider if you're interested in investing in the company here.

While freight rates are likely to stabilize above the cost level in the medium term, rising overcapacity could have a significant negative impact on industry profitability in 2024.

(Source: Hapag-Lloyd IR).

The pain in shipping is far from over - and any investment here needs to be done as a long-term sort of consideration.

Let's look at the company's valuation.

Hapag-Lloyd - the company is cheaper than Maersk, COSCO and OOCL

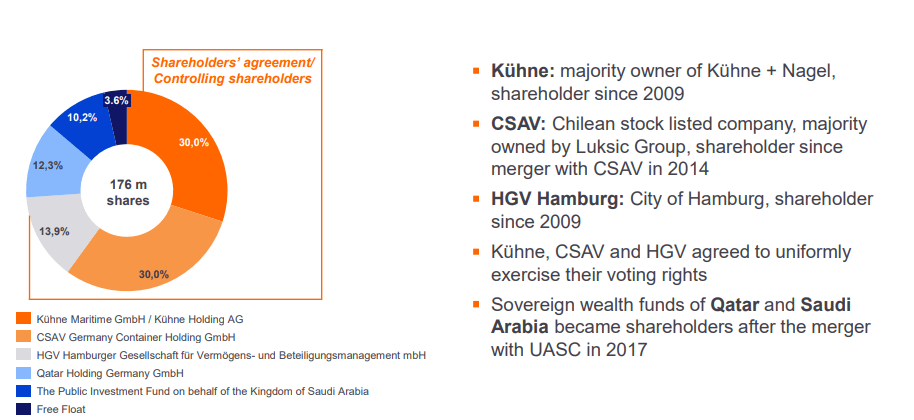

The company has a collection of controlling shareholders. Only a very small part of the shares are free float or available to the public. This is the epitome of a long-term through-cyclic investment. If you buy here, I would say you're taking a very long-term stance and you should probably never sell those shares - unless we see an undervaluation similar to what we saw during 2021-2022.

Hapag-Lloyd IR (Hapag-Lloyd IR)

{kind=link}

HLAG is the native ticker, trading at €122/share. The current street targets are not very forgiving to this, with 11 analysts going from a low of €79 to a high of €145 with an average of €125/share. Not a single analyst is at a "BUY" rating here. Instead, we have 5 "SELL" and 2 "underperform" ratings, that seem to be sticking to the PT trend which has seen the company drop from an average of €230 to €125 as it currently stands (Source: S&P Global/TIKR).

With a far heavier container-focused mix than Maersk, I view Hapag-Lloyd as not being a company to "BUY" until the downcycle really becomes much clearer than it currently is. I expect to see more clarity going into 2024, maybe 1H24, at which point we can more confidently assess where things may end up.

To express the extreme up and down we're likely to see, the company's 2022A adjusted EPS for the native ticker was €96.89 per share. The result this year is expected to be €16.77. Next year, the current forecast is €1.77/share (Source: FactSet).

So do I think the company can go lower? yes, based on this expectation, I do forecast that we'll see a lower share price than the current €122/share.

When it comes to Hapag-Lloyd, I go into the company here forecasting the company at tangible book value, coming to €90/share. I believe tangible book value represents the absolutely highest you want to go for a shipping business here, especially one with HLAG's overall income mix. As I mentioned, Maersk has a better overall mix and tends to trade closer at a mean of 1x, at times dipping to 0.6x. If you're paying that for a larger business with better and more diverse segments, you certainly don't want to pay 1.3-1.4x P/B, which is what the current share price implies. I view other methods of evaluating the company as risky - any sort of projected averages like FCF takes into account the massively successful few years - implied by the Peter Lynch Value, which currently comes to almost €1,600/share. I don't view the company as being worth this - do you?

Going forward, I expect slow normalization for the company. Given the pressure on freight prices, I expect it will be until about 2024-2025E until we see a trough for the earnings, which I expect will be between €1.5-€1.7/share, with current analysts forecasting €1.77/share (Source: FactSet).

However, you're investing in slow normalization in a company that's going down. I expect an 85%+ EPS drop this year, and I'm not the only one (Source: FactSet), followed by yet another 70%+ EPS drop, as things normalize further in 2024E.

This makes the company a "BUY" only in the most limited and niche of situations.

This is my thesis for the company as of November 2023.

Thesis

- Hapag-Lloyd is among the world leaders in container shipping/line freight. The company has a very strong net cash balance sheet. I view the fundamental risk to the company's survival as essentially zero, and eventual reversal will likely come beyond the current normalization trends.

- However, the lack of visibility in the entire shipping sector makes any investment here a tricky venture. There are so many great opportunities on the market today, that a declining shipping company facing challenges into 2024 doesn't necessarily come off as one of the greatest investments here.

- I give the company a conservative PT of €90/share for the German native ticker, making it a "HOLD" here.

- I think the right way to go about this business is to wait until we can clearly navigate the downcycle.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansions/reversions.

This is a somewhat interesting situation because Hapag-Lloyd does fulfill some of my criteria, but we have to be careful due to the current macro. I say "HOLD" here.

For further details see:

Hapag-Lloyd - Shipping In A Downcycle, I Say 'HOLD' For Now