HLAGF - Hapag-Lloyd: Sill Cautious As We Navigate The Downcycle

2023-08-23 13:58:08 ET

Summary

- Hapag’s operating profitability is deteriorating.

- H2 guidance now implies possible operating losses.

- With more cyclical headwinds ahead, Hapag stock looks vulnerable at its current premium.

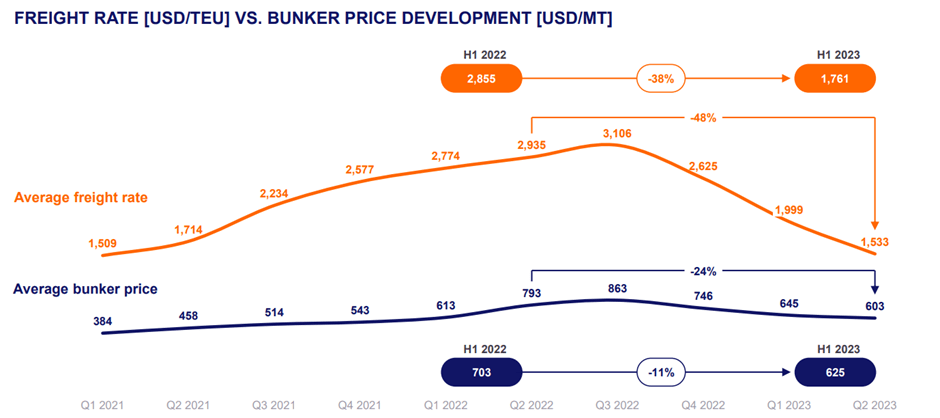

The massive supply shortage triggered by COVID has now reversed, and the containership industry is in a fight to stay profitable through a downcycle. As I cautioned before , Hapag-Lloyd ( HPGLY ) isn’t immune, with freight rates already normalizing to pre-COVID levels and driving significant YoY declines to the P&L. As seasonal tailwinds through the summer months and industry-wide ‘General Rate Increases’ fade as well, expect a soft Q3 and Q4, underpinning the extended destocking cycle warned by Maersk ( AMKAF ) and Hapag-Lloyd management.

Alongside the prospect of more supply headwinds through 2024 and heightened competitive pressures post-dissolution of the 2M alliance (Maersk and MSC ( MSM )), it’s hard to see a turnaround materializing anytime soon. Even in the optimistic scenario that this cycle isn’t as brutal as prior ones (in many cases, the cycle bottom only hits when major players go bankrupt), the company could still earn well below its cost of capital for a while. With Hapag-Lloyd stock also priced very richly at ~9x fwd EBITDA (vs. Maersk and ZIM Shipping ( ZIM ) in the low-single-digits EBITDA and Asian liners like COSCO Shipping ( CICOF ) closer to net cash ), I would remain on the sidelines here.

Puts and Takes from the H1 2023 Result

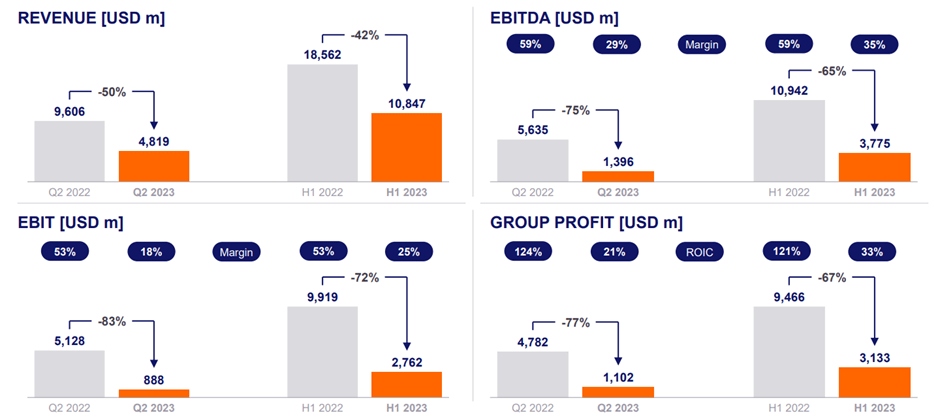

Hapag-Lloyd posted solid H1 2023 operating profits of EUR2.5bn, as its Q1 contribution was offset by a weaker Q2 2023 EBIT of EUR0.8bn (over 50% down sequentially). Relative to the other majors, Hapag-Lloyd is still holding its own, though, with its ~18% EBIT margin coming in above the low-teens percentage for Maersk and ~10% for Ocean Network. The only containership major running margins above Hapag-Lloyd is COSCO Shipping, though the delta is largely explained by their different route networks and shouldn’t detract from management’s outstanding cost discipline. Of note, Hapag delivered impressive low teens YoY unit cost declines through Q2 2023, helping to mitigate any difficulties passing through post-COVID cost inflation via contract rate increases.

{kind=link}

Hapag-Lloyd

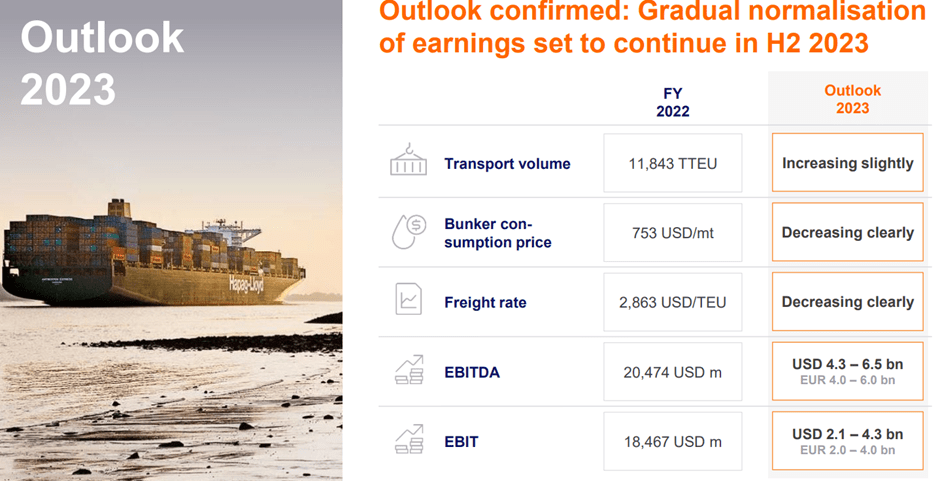

While the H1 result amounts to an implied ~85% of the EUR2-4bn full-year guidance, management has kept its guide unchanged. By comparison, Maersk’s H1 EBIT of $4.0bn is tracking at an even higher ~95% of its $3.5-$5.0bn guidance midpoint, so the industry consensus is clearly factoring in potential operating losses in H2 2023. Smaller scale players like ZIM have notably been more explicit in downgrading its H2 EBIT guidance, which now stands at a $100-$500m loss on the back of demand weakness weighing on the near-term freight rate path. This leaves management teams dependent on their cost levers to protect margins, though with Hapag citing a 25-30% higher unit cost base relative to pre-COVID levels, it’s not clear how much margin headroom is left. Plus, management is guiding to a rather optimistic volume rebound in its Asian trade routes through H2, which could be at risk given the ongoing China slowdown.

{kind=link}

Hapag-Lloyd

Material Mid to Long-Term Headwinds on the Horizon

With an extended destocking cycle quickly becoming the industry consensus view, a softer Q3 peak season for freight rates (vs. historical seasonal trends) looks likely to be followed by a downbeat Q4 as well. While bulls will argue for capacity discipline kicking in should rates decline below costs, history suggests this isn’t necessarily true. The downturn triggered by the ’08 financial crisis, for instance, saw major bankruptcies and consolidation before the downcycle was over. This time around, we haven’t yet seen anywhere near the competitive intensity, though the pending dissolution of the 2M mega alliance poses downside risk to the competitive landscape ahead of the 2025 target.

{kind=link}

Hapag-Lloyd

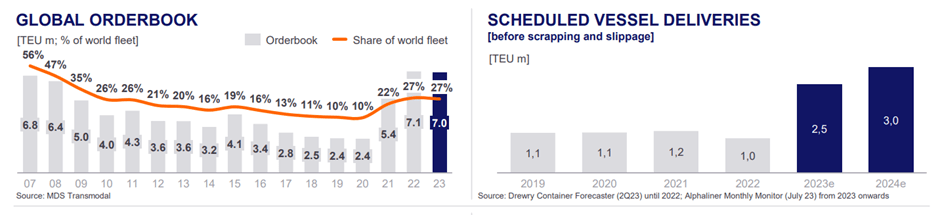

Beyond the demand side headwinds, the prospect of a major capacity influx also presents a key overhang over the coming years. For context, the industry is currently prepared for a massive 10% increase in capacity over 2023/2024 (Hapag is more optimistic at +8-9%), with another >150 in 2025. Even with mitigating factors like increased scrapping (i.e., the demolition of older vessels) and slow steaming (i.e., lower sailing speeds), an oversupply dynamic is the most likely scenario here. Beyond 2025, the industry will also need to mitigate structurally higher ESG-related costs that will weigh on free cash generation. The International Maritime Organization’s latest targets call for an accelerated net-zero emission target by 2050 (vs. the 50% reduction target prior), along with an ambitious transition towards sustainable (and more expensive) fuel alternatives. Hapag’s established track record of cost discipline places it ahead of the pack in navigating these changes, though the stock is also priced accordingly.

{kind=link}

Hapag-Lloyd

Sill Cautious as We Navigate the Downcycle

With the container shipping industry now headed for an excess capacity situation, freight rates have normalized well below the COVID peak, driving Hapag-Lloyd’s profitability lower YoY. While management's guidance embeds a seemingly pessimistic view, I remain concerned about more downside from here. Freight rates in recent months, for instance, benefited from seasonality and a series of ‘General Rate Increases’ which may not recur as the industry’s competitive intensity ramps up amid an extended destocking. And over the mid to long-run, capacity addition headwinds are key, along with the competitive impact for Hapag-Lloyd’s key routes post-dissolution of the 2M alliance. Admittedly, bankruptcy risk is off the table this time around (unlike the GFC-triggered downcycle), with the company’s healthy cash balance adding buffer; yet, the stock is also priced accordingly at a relative premium at ~9x fwd EBITDA. Pending signs of capacity discipline and an improved outlook for global trade, I remain cautious here.

For further details see:

Hapag-Lloyd: Sill Cautious As We Navigate The Downcycle