PMOIF - Harbour Energy: Sector-Leading Cash Returns

2023-09-25 17:28:17 ET

Summary

- Harbour Energy plc is a UK-based oil and gas company focused on mature North Sea assets with a strong cash generation profile.

- The company has stable production and increasing exposure to spot prices as hedges expire, allowing for higher realized prices.

- Harbour Energy has significant option value in carbon capture and storage projects, which could create long-term value.

- Harbour's cash returns as a percentage of market capitalization (low twenties) stand out among E&P peers.

We present our note on Harbour Energy plc (HBRIY), an independent UK-based oil and gas company with a global portfolio. We are drawn by the firm’s capital returns, supported by stable production in the mid-term and increasing exposure to spot prices as hedges expire. Harbour’s free cash flow ("FCF") generation stands out among E&P peers, while valuation multiples are on the lower end. We will provide an overview of the company, analyze the key drivers of our thesis, and value the company’s shares.

Introduction to Harbour Energy

Harbour Energy is the largest upstream UK-listed oil and gas company with a leading position in the UK and a diversified global portfolio which includes interests in Norway, Vietnam, Indonesia, and Mexico. The company has a global production of more than 208 kboepd, out of which 90% comes from the UK. Harbour Energy was founded in 2014 by EIG Global Energy Partners, an American investment firm focused on the energy sector, aiming to acquire productive and cash-generating assets outside North America. Harbour made its first acquisition in 2017 backing Chrysaor to acquire a set of UK North Sea assets by Shell, and later ConocoPhillips’ UK North Sea in 2019. In 2021, Chrysaor merged with Premier Oil in a reverse takeover, to create Harbour Energy. The company is a FTSE250 component and has a current market capitalization of nearly £2 billion.

{kind=link}

Stable production and exposure to spot prices

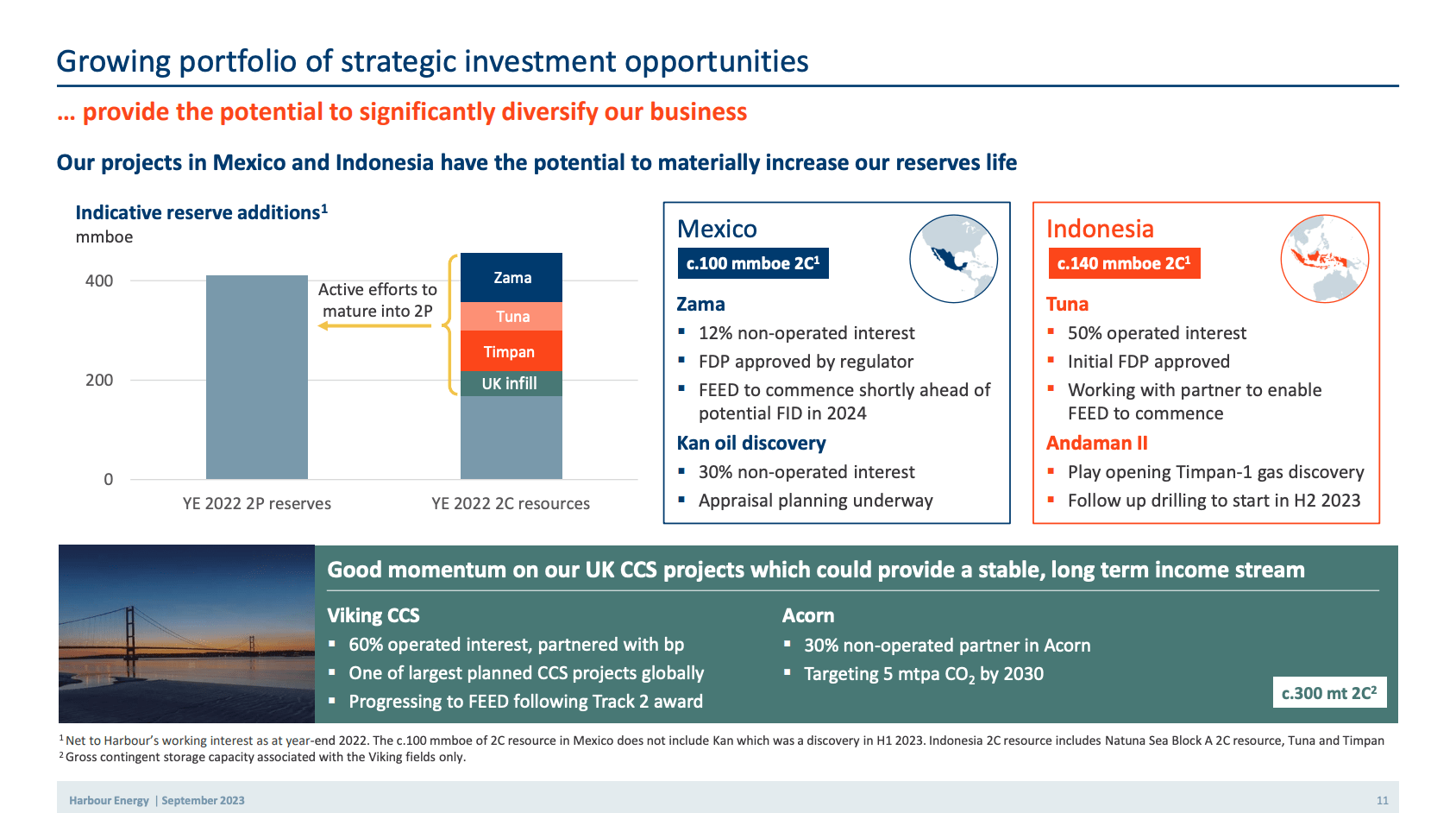

The backdrop for UK North Sea producers has been challenging, given the adverse fiscal changes and declining production. The windfall tax has resulted in increased uncertainty and various project deferrals, leading to lower capex and lower expected production. However, the growth coming from new assets including 2 UK projects (Talbot and Leverett) and international opportunities, i.e., Mexico and Indonesia supports a stable production profile, i.e., around 200kboepd over the mid-term.

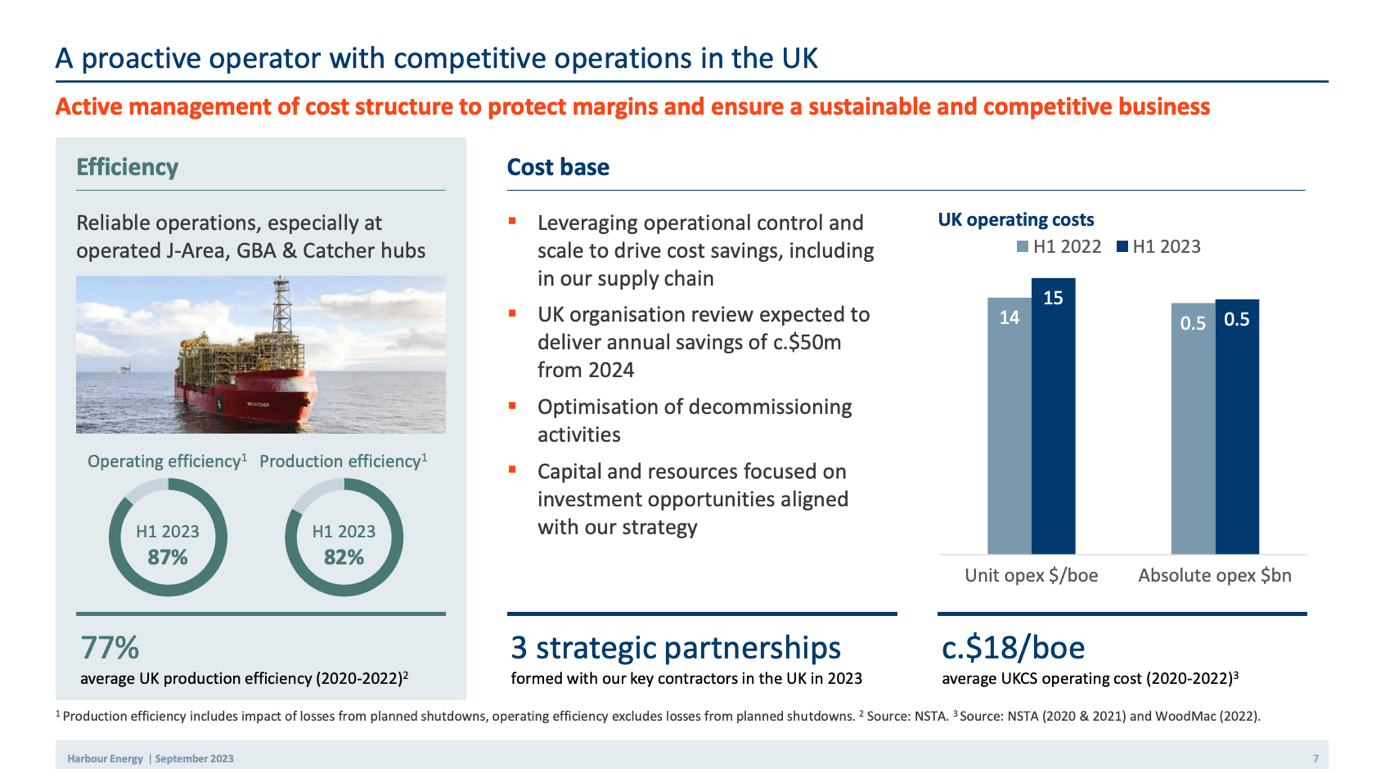

In addition, we would like to note that Harbour largely missed out on the commodity boom (also reflected in the equity’s performance) due to high hedged volumes. The company should increasingly benefit from higher oil and gas spot prices as hedged volumes decrease (i.e., hedges roll off), and new hedging contracts are signed at higher prices or production is sold at spot. More than 60% of volumes are hedged in FY2023, and the number drops substantially by ca. 1/3 rd in the next year and more thereafter, allowing Harbour to capture higher realized prices.

{kind=link}

Carbon capture and storage

We believe CCS represent an attractive opportunity and significant option value for Harbour. UK CCS projects Viking (60% working interest) and Acorn (30% working interest) have been awarded Track 2 status, with the investment decision being made in 2024. The project leverages Harbour’s and BP’s experience and infrastructure. Viking is one of the largest CCS projects in the world and could be crucial to the UK’s 2030 carbon capture targets.

Harbour has around £4 billion (a part of which is offset by tax assets/loss carry forwards) of decommissioning liabilities, or a few hundred million per North Sea field. After significant capex and infrastructure improvements, depleted reservoirs can store carbon using existing pipelines. Companies providing CCS can be remunerated through a regulated asset base framework that determines a given return on assets, potentially creating attractive long-term value.

We acknowledge only a small part of Harbour’s assets can be utilized for these purposes, but this can have a material impact as decommissioning cash outflows are pushed further into the future and discounted at higher rates. We do not consider any upside from CCS in our investment case, but we see it as option value.

UK windfall tax

The UK government introduced a 25% earnings levy in 2022, which was followed by an increase to 35% commencing in January 2023 until March 2028. We view the impact of the windfall tax as fully priced in and do not expect any further downside related to fiscal regime changes.

Investment thesis and valuation

We see high levels of cash generation and low leverage driving substantial capital returns over the mid-term which stand out among E&P peers. We value Harbour Energy using P/E multiples and free cash flow ("FCF") yields. Taking into account the hedged volumes and assuming an average spot price of $80/bbl. We forecast $4.7 billion of revenue in FY2024e, an EBIT of $2.1 billion, and net profit of ca. $380 million, and an FCF of $760 million. This implies a forward P/E ratio of 6.2x and an FCF yield of 32%. The company will effectively generate its entire market capitalization in FCF over the next 3–4 years. We assume around $500 million will be distributed as dividends and buybacks in 2024, implying a 22% cash return yield. A NAV approach would result in a valuation of around 300p per share, implying 20% upside. This valuation discount combined with sector-leading cash returns makes Harbour an attractive investment.

Risks

Downside risks include but are not limited to softer macroeconomic conditions, a decline in oil and gas prices, lower recovery rates in mature assets, higher than expected abandonment costs leading to higher capex, failure to execute on carbon capture and storage projects, slower than expected project execution and later commissioning resulting in lower production volumes, worse than expected exploration success, operational problems, suboptimal capital allocation, lower than expected capital returns: change in dividend and buyback guidance, adverse regulatory changes, additional windfall taxes, energy transition and climate change risks, geopolitical risk given the geographic mix, natural disasters, accidents, etc.

Conclusion

We recommend buying Harbour Energy plc shares on the back of an attractive valuation and high capital returns that will allow to crystallize value.

For further details see:

Harbour Energy: Sector-Leading Cash Returns