HBRIY - Harbour Energy: Transformational Acquisition Resulting In A 7% Dividend Yield

2024-01-15 04:30:00 ET

Summary

- Harbour Energy signs an $11B acquisition agreement, a significant deal for a company with a $3B market capitalization.

- The acquisition includes significant oil production and reserves, positioning Harbour Energy as a major player in the industry with an output exceeding 500,000 boe/day.

- The deal diversifies Harbour Energy's exposure away from the UK and mitigates the impact of high UK taxes.

Introduction

More than five years ago, I discussed Premier Oil here on Seeking Alpha as I was hopeful the company starting up oil production in the North Sea would rapidly reduce its net debt . That has indeed happened and the company, now rebranded to Harbour Energy ( PMOIF ) ( HBRIY ), was in a position to sign a $11B acquisition agreement which is quite an impressive deal for a company with a market capitalization of just around $3B. In this article, I will discuss the details of the acquisition and the impact on Harbour’s future.

{kind=link}

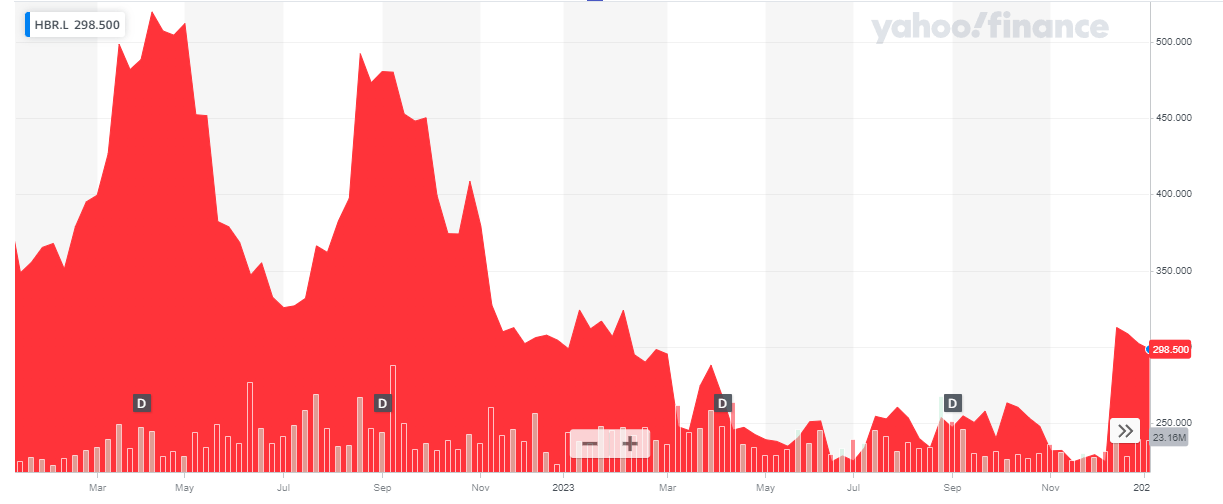

Harbour’s primary listing is on the London Stock Exchange where the company is trading with HBR as its ticker symbol. The average daily volume exceeds 3 million shares so the London listing for sure is the best listing to trade in the company’s stock.

The recent agreement to purchase Wintershall DEA

When companies announce an acquisition, their share price usually falls unless it is a really good acquisition. Their share prices fall even more when the market fears a company is biting off more than it can chew, but although that’s what you could generally expect when a $2.5B market cap company acquires $11.2B in assets, Harbour Energy actually gained on the news as the market realized this actually is an excellent deal for the oil producer.

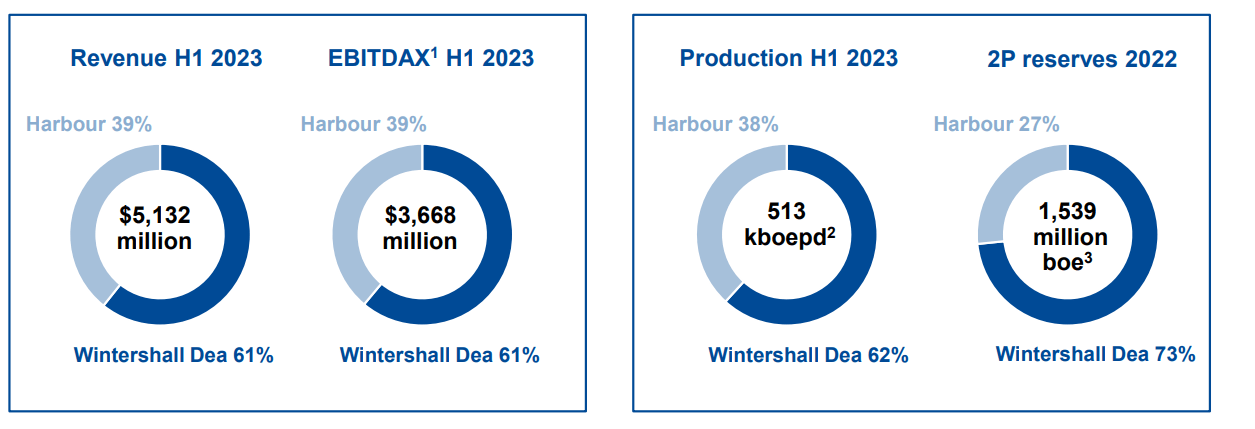

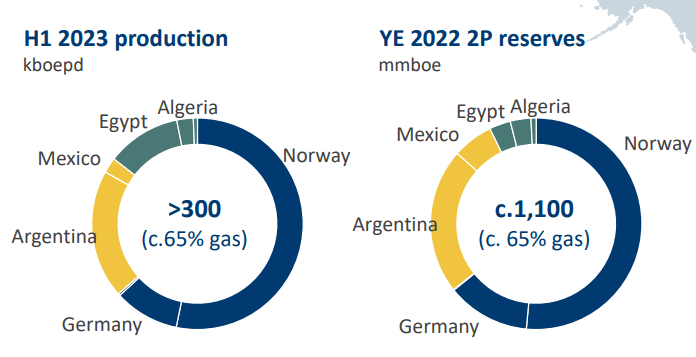

Let’s first see what Harbour Energy is acquiring and paying for it. Harbour is acquiring virtually all (non-Russian) assets of Wintershall DEA which is currently producing 300,000 barrels of oil equivalent per day. Indeed, this is a massive acquisition, not in the least because the production scenario is backed by 1.1 billion barrels of oil equivalent. So with this move, Harbour is buying production and the reserves to back the production results.

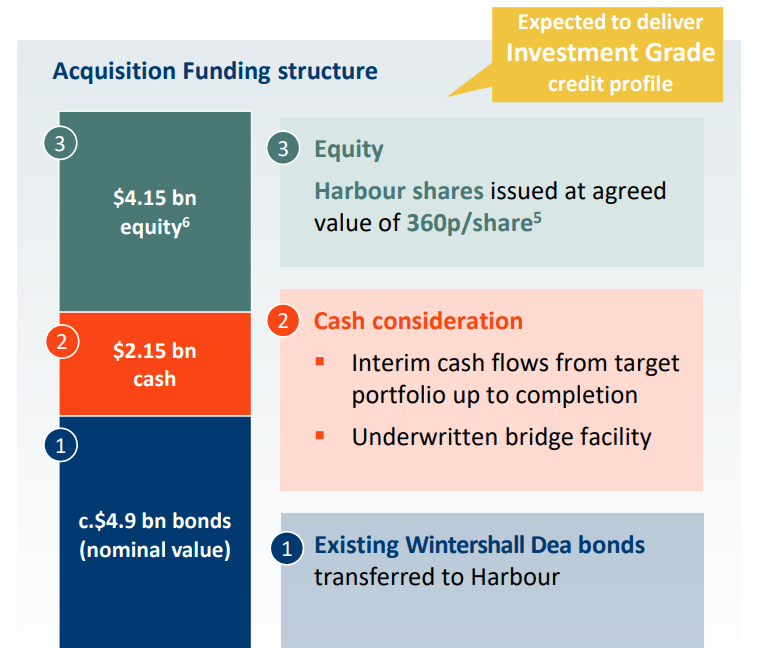

Of course, a big deal comes at a hefty price. $11.2B to be exact. This does not mean Harbour Energy will have to fork over $11.2B in cash, as the deal is actually very well-structured. The purchase price will be funded through three avenues.

First of all, Harbour Energy will be assuming $4.9B in existing debt on the Wintershall level. That debt has an average interest rate of just 1.8% so it definitely works in Harbour’s favor.

{kind=link}

Secondly, a cash payment of $2.15B will be due as well. Harbour will generate a few hundred million dollars in free cash flow before the transaction closes and has signed a bridge loan facility agreement. Also important to note: the agreement will have an effective date of 30 June 2023 which means that all cash flows generated on the Wintershall level between June 2023 and the effective closing date will be deducted from the $2.15B cash portion. As the closing date is anticipated to be in the fourth quarter of this year, about 5-6 quarters of Wintershall free cash flow will be deducted from the $2.15B cash payment. Wintershall generated $2.2B in EBITDAX in H1 2023 and will likely generate around $4-5B in EBITDAX between Q3 2023 and the end of Q3 2024 even at lower oil and gas prices. I think the final cash payment may actually be less than $1B.

{kind=link}

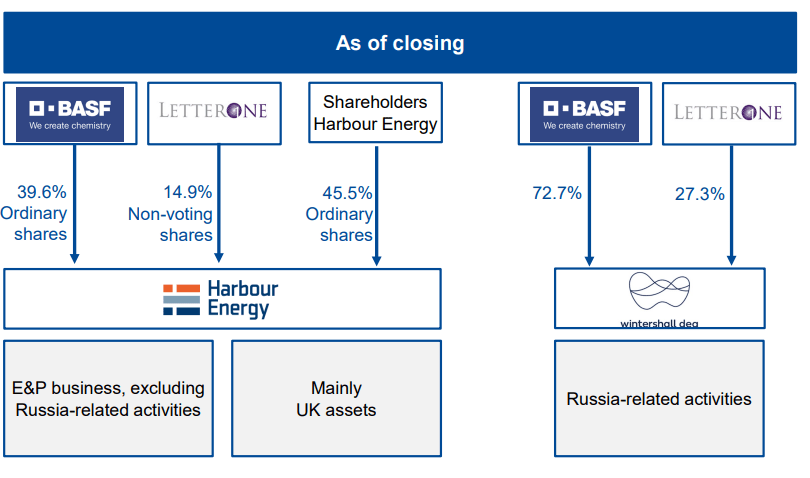

And finally, Harbour will issue $4.15B worth of stock to the shareholders of Wintershall at a substantial premium to the share price. Although the share price was trading at a 30-day VWAP of 227 pence when the deal was announced and although it is trading at 295 pence now, the shares to be issued to Wintershall shareholders are priced at 360 pence. The main shareholder of Wintershall, the German conglomerate BASF ( BASFY ) ( BFFAF ), will own 46.5% of Harbour Energy’s share count after completing the deal.

The share issuance to the shareholders of Wintershall does have one complicating factor. LetterOne, a 27.3% shareholder in Wintershall, is subject to EU sanctions because of its close ties to the Kremlin . Harbour Energy has found an elegant solution to comply with all rules, regulations, and sanctions, and the 251.5 million shares issued to LetterOne as part of the transaction will be non-voting and non-listed. They exist, but LetterOne cannot weigh on Harbour’s corporate policy.

{kind=link}

Should the sanctions get lifted, the non-voting shares can be converted into normal common shares. If that happens, BASF would become a 39.6% shareholder while LetterOne would become a 14.9% shareholder of Harbour Energy.

This will catapult Harbour Energy into the league of serious players

Although the price tag of $11.2B sounds like Harbour Energy is getting ahead of itself, the net cash outlay will likely be less than $1B when all the dust settles. Of course, the $4.9B in assumed debt will have to be repaid (the weighted maturity is 4.5 years) but given the low interest rate and strong cash flow generation of the portfolio, this shouldn’t be an issue. After all, Wintershall DEA was able to secure that debt based on its own production and cash flow profile.

I mainly like the deal because it 1) increases Harbour Energy’s exposure to Natural Gas and 2) diversifies the company away from the UK.

{kind=link}

About the natural gas. As you can see above, 65% of the acquired portfolio consists of natural gas, with the majority either in Europe or at least destined for Europe (where the natural gas price is still trading at a premium). The TTF natural gas price is approximately 32 EUR per MWh which roughly translates into US$10 per Mcf (depending on the specific energetic value, of course, the US$10/Mcf is just to give you a rough idea). With an average production cost of just $9 per boe, the margins will be healthy. Additionally, on a consolidated basis, it will reduce Harbour Energy’s operating costs from $15/boe to $11/boe. The consolidated pro forma EBITDAX of the combined entity will come in at around $7B using the current oil and gas prices.

I am also very happy the company is diversifying its exposure away from the UK. The sole reason why I currently have no position in Harbour Energy is the very punitive UK tax regime. The newly introduced Energy Profits Levy is hurting the company (and other UK-based producers) as the headline tax rate on UK oil and gas profits has increased from 40% to 75%. An unworkable tax rate has a profound negative impact on the after-tax net income and net free cash flow. Acquiring a non-UK portfolio will help to mitigate the impact of the sky-high UK taxes.

Investment thesis

Harbour Energy is a well-managed company but the 75% tax rate on UK oil and gas profits hurts the investment case and that’s why I had no position in the company anymore. The acquisition of Wintershall DEA changes everything as the average tax pressure will decrease while the company acquires the new assets at a price of just $30,000 per flowing barrel. The consolidated entity will have a net debt position of approximately $5-6B by the end of this year while the total share count of approximately 1.7B shares will result in a market cap of approximately $6.5B for a total enterprise value of $11.5-12.5B. Which is barely more than what Harbour is paying for the acquisition (the explanation is very simple: Harbour is issuing shares at a premium while the cash flow since June 30 th will accrue and reduce the net payable price upon closing the acquisition).

Once the transaction has been completed, Harbour Energy will hike its dividend and has earmarked $455M per year for dividends. Divided over approximately 1.7B shares, this results in a dividend of $0.267 per share or roughly 20-21 pence for a yield of 7% (but investors will have to wait until 2025 as that will be the first year after the deal closes).

I will likely initiate a long position in Harbour Energy in the next few weeks as I like this transaction and the $5-6B net debt can easily be dealt with.

For further details see:

Harbour Energy: Transformational Acquisition Resulting In A 7% Dividend Yield