HRGLY - Hargreaves Lansdown: Changes Coming But Not Clearly Enough

Summary

- Changes may be coming after HL's co-founder and biggest shareholder called for change. Shares are down 64% since 2019.

- HL has good qualities like large recurring revenues and platform characteristics, but has had mixed results in recent years.

- Asset growth has been solid, but mix shift is negative. Revenue growth should continue over time, but costs are growing too fast.

- A new CEO will start in 2023, but it is unclear what he will change. Three long-time shareholders have 40% of the shares.

- At 879.12p, HL shares have a 17.5x P/E and a 4.5% Dividend Yield. We prefer to wait until clear evidence of self help. Avoid for now.

Introduction

We review Hargreaves Lansdown ( HRGLF ) (referred here as "HL"), the U.K.’s largest platform for retail investors, after co-founder and 20% shareholder Peter Hargreaves publicly criticised the company’s current strategy and called for “huge” cost cuts in an interview (subscription required) with the Financial Times over the weekend.

HL can be a potential turnaround. Its business has positive qualities, including high recurring revenues and platform characteristics, and shares have fallen 64% from their peak in May 2019, including 36% in the past year alone:

{kind=link}

Recent HL results have been mixed. Net New Business drove just 4% of AUA growth in FY22, down from around 8% in each of FY19-21. Overall Funds growth has been relatively solid, but the HL Funds business has continued to decline. There has been a negative mix shift towards Shares, which do not generate recurring revenues. Cash margin is expected to improve with rate rises. We think revenues can grow at mid-to-high single-digits over time in future.

Costs growth remains faster than revenue growth, and significant restructuring costs are expected in FY23-26. EBIT will likely fall to 30% below FY19 level in FY23. On balance we believe costs have grown too much due to poor management. A new CEO is starting in 2023, but he has been on the Board since 2019. An activist investor may help, but three long-time shareholders own 40%. HL shares are trading at 17.5x FY22 EPS and offer a 4.5% Dividend Yield.

Overall, we do not see an investment case now, and prefer to wait until clear evidence of self-help. Our rating on HL is now Hold, meaning the stock should be avoided.

Our Hargreaves Lansdown Rating History

We originally initiated a Buy rating on HL in June 2019, after the share price fell 16% following the suspension of redemptions by Woodford Investment Management, whose funds HL had heavily marketed to its clients. We last reiterated our Buy rating in August 2021, after which we had effectively ceased our active coverage.

Our Buy rating was wrong. Since our original initiation, HL shares have lost 44% (after dividends), though we made modest profits as short-term holders in both 2019 and 2020. Whereas we had expected earnings to grow at 10% annually, they did so for two years before collapsing back to FY19 levels in FY22; whereas we had expected stable valuation multiples, HL’s trailing P/E has more than halved from 36.2x at initiation to 17.5x at present:

| HL Comparison – Current vs. Initiation Source: HL company filings. |

Should there be a successful turnround that returns HL to earnings growth, the resulting P/E recovery alone could generate substantial gains of as much as 100% to shareholders.

We try to assess HL’ potential below. HL’s results have been mixed in recent years, and hard to interpret given the unusual environment since COVID-19.

Good Total Asset Growth Until FY22

HL has maintained good Assets Under Administration (“AUA”) growth until FY22, but with a worsening mix.

Net New Business (“NNB”), the amounts deposited or transferred by customers, contributed to 7.8% of AUA growth in FY20 and 8.4% in FY21, in line with the 8.0% in FY19, before halving to just 4.1% in FY22. “Market Growth & Other”, which includes the impact of volatile markets and the depreciation of the U.K. pound, averaged 6% across FY20-22:

which includes the impact of volatile markets and the depreciation of the U.K. pound, averaged 6% across FY20-22:

| HL AUA % Growth Y/Y by Source (FY16-22) Source: HL company filings. |

NNB was likely atypically strong in FY20-21, after COVID-19 restrictions boosted consumer savings and retail interest in markets, and atypically weak in FY22, after inflation and macro uncertainty reduced investor appetite. Adjusted for this, NNB will likely continue to be a diminishing driver of AUA growth, simply because the existing AUA base is getting larger. (In pound terms, NNB reached an all-time record of £8.7bn in FY21, up from £7.3bn in FY19.)

For the long term, we believe NNB can generate a mid-to-high single-digit AUA growth annually. This is helped by HL’s tax-advantaged SIPP and ISA products, which encourage regular contributions and penalize withdrawals. The percentage of HL’s AUA in SIPP and ISA products has remained largely unchanged at 75% since FY19. Natural asset price appreciation will likely add a few points to AUA growth, taking total AUA growth to likely 8-11%.

Worsening Asset Mix, Perhaps Temporarily

The mix in HL’s AUA has worsened since FY19, though potentially temporarily due to one-off factors.

| HL A verage AUA By Asset Class (FY16-22) Source: HL company filings. |

Funds on HL’s platform, including both funds operated by third-party managers and by HL itself, grew with a relatively solid CAGR of 8.9%in FY19-22. However, whereas non-HL funds had a 10.9% CAGR, HL Funds declined by 1.5% annually on average, likely due to reputational damage related to the Woodford controversy. The decline in HL Funds is a negative because these pay both platform fees like any fund and management fees to HL as the fund manager.

Shares , stockbroking accounts operated by HL, grew AUA with a CAGR of 18.5% in FY19-22, by far the fastest-growing asset class in the group. This may be associated with heightened retail interest in market during the pandemic. It is a negative for HL because Shares only generate transaction-based commissions but no recurring platform fees.

Cash , including both cash in Funds and Shares accounts as well as dedicated “Active Savings” product, grew AUA with a solid CAGR of 10.1% in FY19-22, with Active Savings reaching a period-end balance of £4.6bn.

For the longer term, we expect the AUA mix to shift somewhat back to Funds from Shares as retail interest in stocks normalizes towards pre-COVID levels, but we do expect continuing weak demand for HL Funds.

Revenues Peaked in FY21, Down in FY22

HL revenues peaked in FY21 but fell 7.6% in FY22, giving an overall FY19-22 revenue CAGR of 6.7%:

| HL R evenues By Asset Class (FY16-22) Source: HL company filings. |

Funds revenues, i.e. platform fees, grew with a CAGR of 7.3%, below Funds AUA CAGR of 8.9%. Revenue margin on Funds tends to drift slightly down over time because, while the standard 45 bps fee rate remains unchanged, more investors are gaining discounts on reaching certain asset size thresholds.

HL Funds revenues, i.e. management fees to HL as the fund manager, has declined on average by 4.1% annually, worse than the decline in AUA because of a fee reduction in 2021 to appease investors for poor performance.

Share revenues, i.e. stockbroking commissions, had a CAGR of 31.3% in FY19-22 due to customers trading much more during the pandemic, but already down 24% year-on-year in FY22 as activity levels return to normal.

Cash revenues, mostly interest HL receives on unused customer cash balances, fell by 32% between FY19 and FY22 due to lower interest rates. These are now rising again with interest rate hikes, though the 90-110 bps guided for FY23 is higher than any year in FY15-22 (the range was 37-72 bps), likely a temporary benefit from HL not yet passing on the benefit of rate hikes to customers.

Revenue margins have been relatively stable in Funds in recent years, volatile in Cash due to interest rate movements, and they remained much higher than pre-COVID levels Shares in FY22. They are guided to recover to 44-47 bps in FY23 (compared to 40 bps in FY22), largely because of the jump in Cash revenue margin:

| HL Net Revenue Margin by Asset Class (FY16-23E) Source: HL company filings. |

Longer-term revenue margins are hard to predict, driven by changes in asset mix, interest rates, share trading frequency, etc. Ultimately, they depend on HL’s value-add as perceived by customers, not least because in each asset class there are (smaller) alternative providers that offer the same products at effectively lower prices. On balance, we think revenues can grow at mid-to-high single-digits in the future, from an 8-11% AUA growth and continuing margin shrinkage.

Costs Growing Too Fast – Buy Why?

HL’s costs have consistently grown faster than revenues, resulting in a continuing decline in its EBIT margin. Between FY16 and FY22, reported EBIT margin has fallen by more than 20 ppt from 66.9% to 46.3%:

| HL P&L Growth Rates vs. EBIT Margin (FY16-22) Source: HL company filings. NB. FY22 includes £28.3m (around 5% of revenues) of "strategic costs". |

Much of the cost growth can be attributed to headcount growth. Staff Costs represented 50% of all Operating Costs in FY22, and the number of employees has more than doubled during FY16-22, actually growing by a slightly larger percentage than the number of customers (108% vs. 105%).

HL’s performance cost and margin is the opposite of what we have seen in most financial services firms, which tend to have stable to improving cost margins thanks to economies of scale and increasing use of technology.

There are broadly three possible explanations for HL’s cost growth:

- Management has done a bad job on costs with profitable customers

- HL is “investing” in customers who are not profitable now but will be in the future

- HL customers are increasingly unprofitable to service

Management’s preferred explanation is no. 2. They point to the fall in the median age of HL customers from 54 in 2014 to 46 in 2021, see this as reflecting HL’s growing penetration rate, and expect the younger cohorts to follow the same trajectory to having more assets and generating more revenues over time. In prior years management had explicitly guided to costs growing in line with customer numbers and described this as necessary to maintain service quality.

The worst-case scenario will be no. 3, and it could be caused by one or more of HL going into unprofitable segments to maintain volume growth in a mature business, the sector becoming more uncompetitive due to low-cost alternatives, and/or HL finding it necessary to maintain a high-touch, labour-intensive service model to maintain its market share.

On balance, we believe the reason is mostly no. 1, i.e. management doing a bad job. Even if HL customers will become more profitable in the future and it is necessary to provide them with a high-touch service now, maintaining the same employee/customer ratio implies there has been no increase in per-employee productivity, whereas technological advances mean there should be at least some improvement.

Changes Are Starting, But Not Enough

We have started to see changes in HL strategy and management, but not enough.

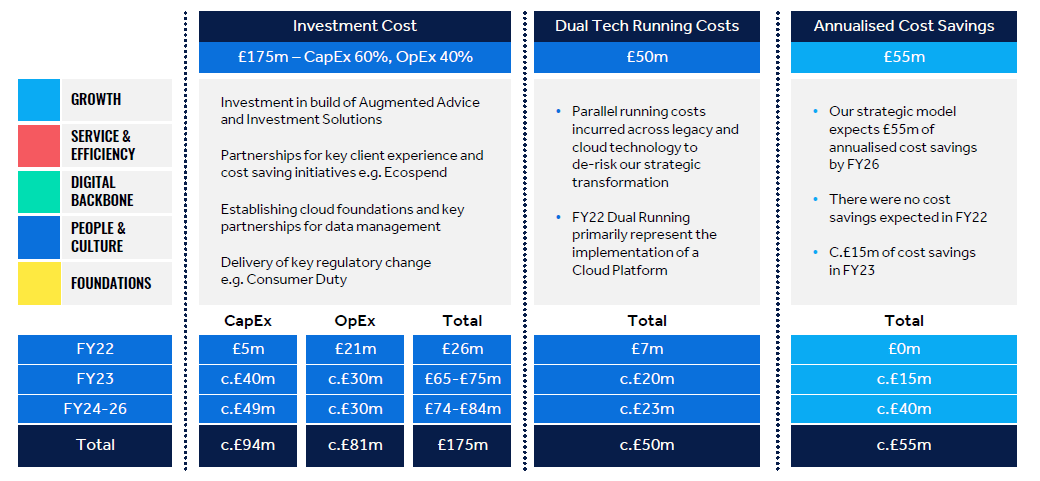

HL finally acknowledged the need to be more efficient at their capital markets day in February 2022, announcing a new technology improvement program that would eventually generate £55m of annualized cost savings, but only in FY26 and after incurring £175m of investment costs and £50m of dual tech running costs:

{kind=link}

However, 8 months later, CEO Chris Hill announced he would be retiring in 2023 at the age of 52 after 7 years in the role. His replacement, Dan Olley, was announced in December. Olley has been a non-executive director on HL’s Board since 2019 and is one year older than Hill; he is also still the CEO of market data company dunnhumby (a role he took up only in January 2022), and he will start as HL CEO “once released from current obligations in 2023”.

It is unclear when Olley will actually start at HL and how much he represents continuity in HL’s strategy.

Hargreaves Lansdown 2023 Guidance

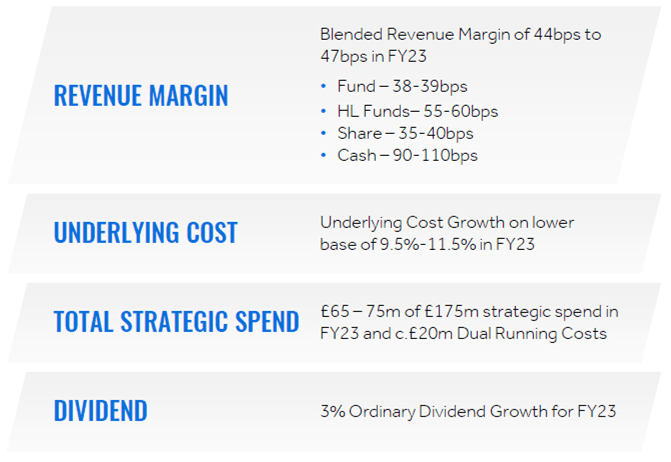

HL’s current guidance for FY23 includes broadly stable revenue margins for each asset class, except a sharp jump in Cash margins after rate hikes and HL not passing on the benefit. Underlying costs are expected to grow at the “lower base of 9.5-11.5%”, and there are £65-75m of additional “strategic costs” and £20m of “dual running costs”:

{kind=link}

If we take the mid-point of each guidance range and assume a broadly flat AUA, then FY23 will see a 5.4% growth in revenues, a flattish Underlying EBIT but a reported EBIT that is 30% lower than in FY19:

| HL FY23 Forecasts (Our Estimates) Source: Librarian Capital estimates. |

HL’s trading update for Q3 FY22 showed AUA down 11.0% year-on-year (0.9% quarter-on-quarter) but revenue up 14.6% year-on-year largely thanks to higher Cash revenues on higher interest rates.

Hargreaves Lansdown Valuation

With shares at 879.12p, relative to FY22 financials, HL has a P/E of 17.5x and a Free Cash Flow Yield of 6.3%:

| HL Net Income, Cashflows & Valuation (FY18-22) Source: HL company filings. |

Total dividends declared in FY22 were 39.7p, representing a Dividend Yield of 4.5%.

The 2021 acquisition of Interactive Investors, a close comparable for HL, by U.K. asset manager abrdn plc ( SLFPF ) represented a relatively poor valuation, with abrdn paying £1.49bn for £55bn of AUA. On HL’s September 2022 AUA of £122.7bn, this would imply an enterprise value of just £3.3bn – less than the actual £3.7bn figure today.

Listed comparable AJ Bell has a £1.47bn market capitalization on a September 2022 AUA of £69.2bn, which also implies a lower valuation for HL than it currently has, though AJ Bell has a far higher P/E of 31x.

Activist Investor vs. Key Shareholders?

HL will ordinarily be a likely target for activist investors, with its recurring revenues (allowing more freedom of action on costs), manageable size (£4.1bn in market capitalization) and clear underperformance, but any activist involvement will depend on the consent of three together who control nearly 40% of HL stock.

Co-founder Peter Hargreaves holds 19.8% of HL shares, co-founder Stephen Lansdown holds 7.1% and funds managed by Lindsell Train hold 12.8%, based on available data.

Hargreaves and Lansdown had each offloaded hundreds of millions of pounds’ worth of HL shares in 2020-2021. Peter Hargreaves has now called for cost cuts, but the attitude of the other two key shareholders is unclear. Lindsell Train has been broadly supportive of the business in their monthly fund commentaries.

To complicate matters, Hargreaves has also publicly criticised the current Board, which implies a breakdown in relations:

“The board indulged in completely unnecessary irrelevant programmes, which have distracted the firm from its prime objective. It’s hardly surprising the shares have collapsed.”

Peter Hargreaves, FT Interview (January 8, 2023)

We would be much more comfortable investing in HL if there is an activist investor supported these three key shareholders.

Strategic Sale Requires Self-Help First

A strategic sale is frequently a way for activist investors to unlock value. Unfortunately, until HL has fixed its products and technology, it is unlikely to attract high strategic bids.

Large banks are increasingly interested in retail asset management, for example with Lloyds Banking Group’s ( LYG ) joint venture with Schroders ( SHNWF ) since 2018 and JPMorgan’s ( JPM ) acquisition of Nutmeg in 2021. However, these examples tend to be banks with existing customer bases looking to acquire good products or technologies, whereas HL is a firm with a large existing customer base but weak products and technologies. (HL’s own funds have continued to lost assets, and HL’s consumer website and its investor relations website are both poor-quality.)

Conclusion: Is Hargreaves Lansdown A Buy?

Overall we do not see an investment case now, and prefer to wait until clear evidence of self-help, in the form of either a clear improvement program with well-defined targets from the new CEO, or an activist investor stepping in with the support of the three long-time shareholders.

Our rating on HL is now Hold, meaning the stock should be avoided.

For further details see:

Hargreaves Lansdown: Changes Coming, But Not Clearly Enough