HOG - Harley-Davidson: Ready To Rumble Electrically

Summary

- The firm's brand continues to resonate with its consumer base, driving high levels of customer loyalty.

- Expansion into new market segments should attract new and younger consumers.

- Hardwire strategic plan beginning to bear fruit through increased profitability in FY22.

- Uncertainty surrounds the sector in general due to macroeconomic headwinds.

- Shares are currently fairly valued, leaving value investors with little to exploit.

Investment Thesis

Harley-Davidson ( HOG ) is currently engaged in a brand new corporate strategy aimed at streamlining operations while simultaneously reinvigorating their brand identity through a new lineup of motorbikes.

Solid profitability and a return to historic levels of unit-economics suggest the company is well on their way to achieving their lofty goals.

However, the high price-tag currently pinned to their shares makes creating a position a difficult argument to make from a pure value perspective.

Company Background

Harley-Davidson is an American motorcycle manufacturer known primarily for their extensive range of motorbikes, biking accessories and apparel. They are headquartered in Milwaukee, Wisconsin.

Harley has an extensive history in the motorcycle manufacturing industry having been founded in 1903 . For decades their core line-up of bikes has been focused in the style of motorbikes known as "choppers". These are usually air-cooled cruiser bikes with a displacement greater than 600cc.

Harley-Davidson "The Fat Boy" Model (Harley Davidson BE)

These bikes are big, smooth and popular among bike enthusiasts having become some of the most identifiable and popular bikes in the world. The company has garnered a brand culture which reflects this macho, bad-boy attitude their bikes command.

Furthermore, the following for the firm's bikes has become almost cult-like with many Harley oriented bikers showing incredible loyalty towards the companies motorcycles.

This brand identity and customer loyalty is currently being maintained through the HOG : Harley Owners Group. The very same acronym that gives rise to the ticker for their stock.

Harley is current engaged in their " Hardwire " strategic plan aimed at enhancing their position as a market-leading motorcycle brand, with a primary focus resting on the development of new bikes including a series of electric motorcycles marketed and sold under the " LiveWire " moniker.

Economic Moat - In Depth Analysis

Harley-Davidson exhibits one of the widest economic moats in the motorcycle manufacturing industry. Their extensive brand identity, customer loyalty combined with a newfound drive for innovation in the electrification of motorbikes provides significant footing for the company to succeed moving into the future.

One of the key strategies in Harley's Hardwire initiative to " rewire " the brand is centered around the customer experience for both motorcycle riders and non-riders. The objective for the firm is to drive brand desirability through emotional responses in consumers.

By further enhancing the ecosystem around their motorcycles through accessories, brand events and marketing campaigns, Harley should be able to tap into the less rational, desire-side of consumers mindsets.

This method of enhancing their already extensive brand identity through emotional connections with consumers has been proven by researchers to be an incredibly powerful method of marketing.

{kind=link}

This focus on more than just bikes culminate in what Harley refers to as the " Harley-Davidson Lifestyle ". The aim for the firm is to focus on expanding into complementary businesses and engage in delivering consumers accessories, apparel and licensed products to become a global lifestyle brand.

Equally, Harley is committed towards building the most technologically advanced motorcycles available on the market. This focus currently materializes through a push to provide an extensive portfolio of electric motorcycles marketed and sold under the LiveWire brand.

Harley established LiveWire as its own motorcycle brand in mid-2021 . This was accompanied by the first company-owned dealership which exclusively sells the new LiveWire brand of electric motorbikes. All other Harley dealerships are independently owned.

LiveWire ONE (Harley-Davidson BE)

The LiveWire range of electric motorcycles are some of the first mass-produced e-bikes being sold on the market. Harley should continue to benefit for another couple years from essentially existing as the sole supplier of electric motorcycles to consumers.

More importantly, Harley most likely harbors a significant technological advantage compared to the competition thanks to their substantial R&D investment towards the electrification of motorcycles. Due to the compact nature of a motorbikes frame, it is a particularly difficult style of vehicle to electrify successfully using current-day battery technologies.

This engineering advantage will no-doubt continue to provide Harley with a sizeable advantage over the competition with regards to electric motorbikes, and should continue to do so for at least the next five years.

While the electric LiveWire brand is an undoubtable departure from the tried and tested +600cc bad-boy cruisers Harley is known for, this diversification is another element of their Hardwire corporate strategy.

The LiveWire branding is aimed particularly at expanding into a sportier market environment with a unique and innovative offering. Harley hopes this will give them a tangible competitive advantage.

The company aims to harness new motorbike segments such as the adventure explorer segment which is currently dominated by BMWs GS lineup of bikes.

This expansion comes with the promise of rejuvenating Harley's ageing consumer base with entirely new customers looking for a different riding experience.

Harley-Davidson Pan America 1250 Adventure Explorer (Harley-Davidson BE)

Simultaneously, the firm is simplifying their line-ups in the sports cruiser and touring market segments to reduce costs and eliminate underperforming models. This should allow the company to increase manufacturing volumes of their best performing models while reducing production complexity.

These technological advantages combined with a vibrant and strong brand identity allow Harley to command a premium price for their motorbikes which is good news for profit margins and shareholders.

Unfortunately, Harley-Davidson does operate in the particularly cyclical and highly competitive global motorcycle manufacturing industry. This means Harley is subject to customers who have continuously changing tastes while simultaneously battling the currently prevailing macroeconomic headwinds.

However, their excellent creation of a Harley lifestyle has created significant social switching costs for consumers, with many having incorporated Harley-Davidson into their lives, thus making a switch to another brand very unlikely.

Furthermore, their strong pricing power should allow the firm to perform reasonably well in an economic slowdown, as consumer should still be willing to pay for a "lifestyle product".

Financial Situation

Harley-Davidson has had a highly profitable history, especially given the prevalent abundance of loss-making firms in the motorcycle industry. However, the past five-years have seen a plateau forming in their revenues, along with a significant decrease in unit-economic efficiency as well as total motorbike deliveries.

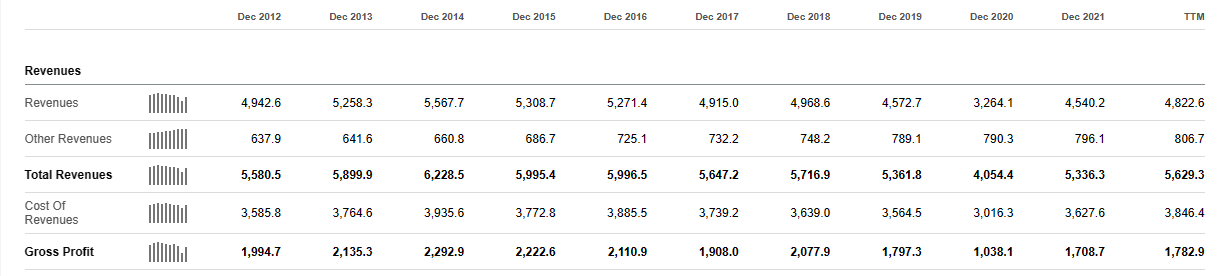

Seeking Alpha - HOG Financials - Income Statement

{kind=link}

From an income statement perspective, the company had a robust gross profit in FY21 of $1.7B. This represented an increase of 65% compared to FY20, but an overall decrease of -16.2% when considered against their 10Y average. Gross profits in FY22 are expected to surpass those of FY21 by around 15%.

Already in the first three quarters of FY22, Harley has achieved a net profit of $699M representing a net margin of 12.8%, compared to a margin of 12% in the whole of FY21. Harley's Motorcycle department sales revenues in Q3 FY22 also grew by 24% compared to Q3 FY21 largely due to the rise in price positioning abilities for the firms products.

Harley-Davidson Q3 Press Release

Harley's operating margins increased significantly in FY22 Q3 compared to the same period last year. This 8.4% improvement to an operating margin of 17.9% was largely attributable to greater manufacturing leverage and lower tariffs.

While total operating expenses were $20 million higher compared to Q3 last year, this was primarily due to the increased spending by the firm on the LiveWire brand.

The increased revenue seen in the first nine-months of FY22 were largely thanks to the 19% increase in global wholesale motorcycle shipments as well as an improvement in their global pricing strength.

Harley-Davidson FY22 Q3 Financial Report

{kind=link}

North America remains Harley's largest market by sales volume and revenues accounting for 65% of total motorcycles sold. However, the largest growing segment by far is the Asia Pacific market where FY22 Q3 sales have increased 18% compared to the prior year.

While North American sales actually decreased 5% in the same period, this was largely due to a lack of inventories at dealerships. This was primarily caused by the two-week shutdown of Harley's production facilities earlier in May of 2022 causing a backlog in parts and motorcycle shipments.

Total volumes have decreased 2% compared to FY21.

Harley-Davidson FY22 Q3 Financial Report

{kind=link}

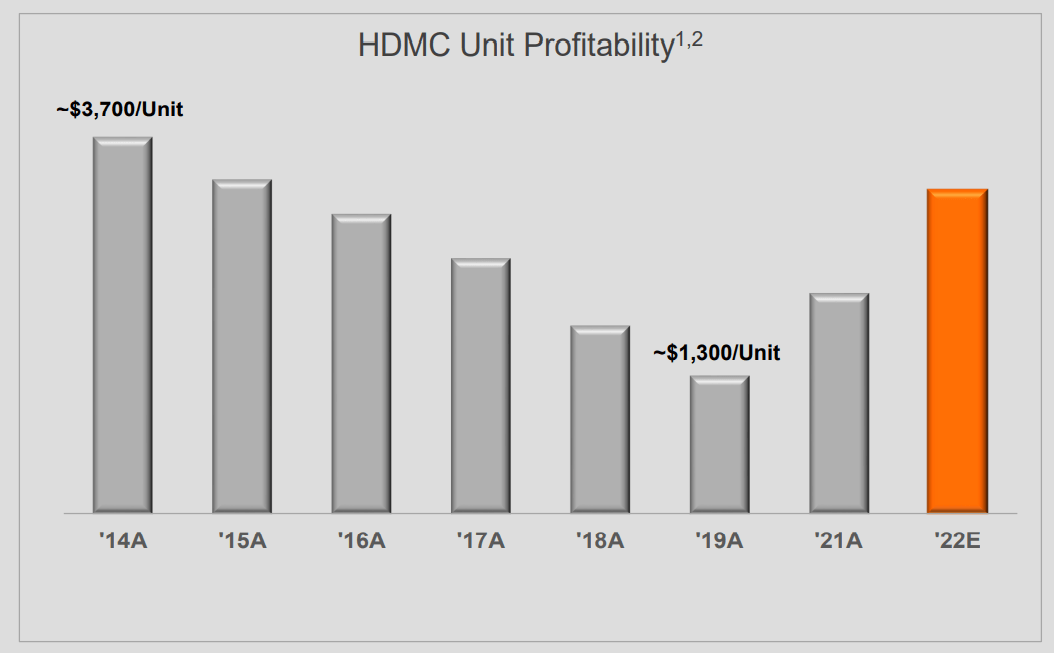

However, the most attractive factor for Harley is the significant overhaul management has managed to achieve in unit profitability. Since 2019, Harley is expecting to have increased unit profitability down from around $1300/unit to over $3000/unit.

This 130% increase will allow Harley to further solidify their profit-making abilities through continued investment into the LiveWire brand of bikes.

This huge increase in unit-economics is largely due to significant model pruning of underperforming bikes (in sales terms) and through improving their cost-structure at the firm.

Considering revenues continued to increase even with a slowing in deliveries, the 2% decrease in sales volumes does not constitute a factor that places the value or future ability to generate shareholder returns into jeopardy.

Furthermore, the slowdown in deliveries is not unique to Harley-Davidson, and has been experienced by almost all motorcycle manufacturers including BMW ( OTCPK:BMWYY ) and Harley's historic rival, Indian Motorcycle.

Overall, Harley has shown healthy and continued growth on their income statement which has resulted in their TTM ROIC growing to 7.6% compared to only 6.7% in 2021. Their five-year average ROIC is 4.82, which highlights the magnitude of Harley's return to operational efficiency and profitability.

Harley has also been growing their operating margins post-pandemic from just 3.45% in 2020 to a TTM of 16% in December, 2022. The forecast operating margin of 16% in FY22 even trumps Harley's 12.16% 5Y average.

Harley's balance sheet looks to be in healthy shape much akin to their income statement. Their total current assets for the TTM are $5.01B while current liabilities only amount to $3.7B. Harley has a good quick ratio of 1.04 current assets minus inventory divided by current liabilities). Their current ratio is even more attractive at 1.36 (current assets divided by current liabilities).

Harley exhibits healthy fiscal stability and is not currently struggling with any major liquidity risks.

With regards to the LiveWire brand, on September 26, 2022 the planned merger with AEA-Bridges Impact Corp. (ABIC) was completed . ABIC is a special purpose acquisition company.

The deal gave ABIC a 5.7% stake in LiveWire and provided the brand with net proceeds of approximately $294 million. $180 million of that total sum includes investments into the brand made by ABIC.

This strategic merger will allow LiveWire to become the first publicly traded EV motorcycle company. Furthermore, the proceeds should help fund LiveWire's strategic plan to accelerate its go-to-market model, invest in new product development, and enhance global manufacturing & distribution capabilities.

LiveWire itself is now valued pro forma to have an enterprise value approximately $1.77B.

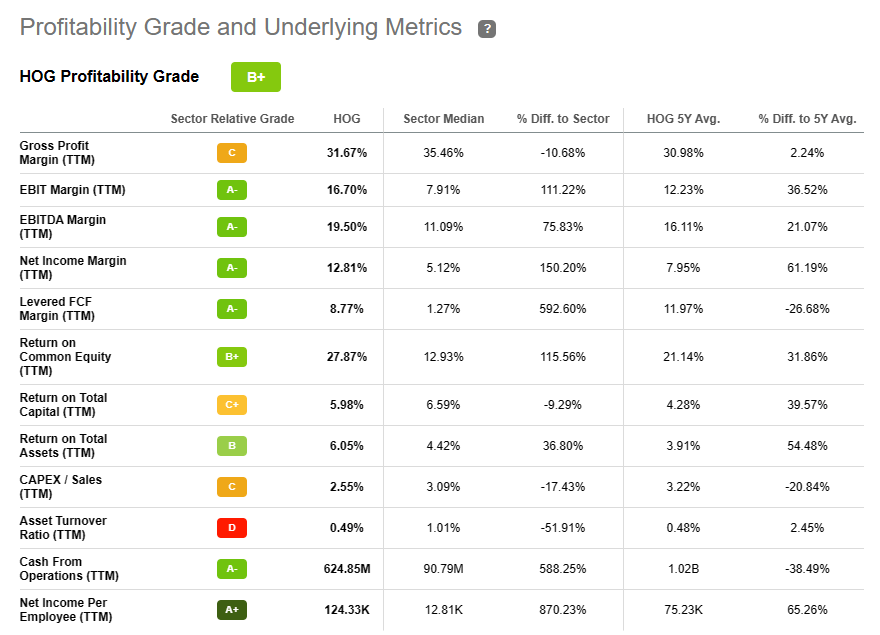

Seeking Alpha HOG - Quant Profitability

{kind=link}

Seeking Alpha's Quant assigns Harley with a profitability grade of B+ which I believe is representative of the cash flow and general value generation abilities of the company. Cash flow from operations amounted to a TTM figure of $625M.

What is particularly noteworthy is the net income per employee figure of $124.33K. This is outstanding and over 850% above the sector median. This highlights the efficiency and restructuring efforts being undertaken at Harley as they seek to rid themselves of excess costs.

Equally, their leveraged FCF margin is healthy at 8.77%. This exceeds the sector median of 1.27% handily and illustrates the return to profitability the company has been trying to achieve post-pandemic.

The evidence of the Hardwire strategic plan beginning to bear its fruit its further highlighted by their EBITDA margin for the TTM growing to 19.5% compared to a historical 5Y average of just 16%.

While their return on total assets and on total capital are a little lower than investors would like to see, this is largely attributable to their large spending on the LiveWire brand and the associated R&D costs.

Harley is undoubtedly on the right tracks from a cashflow perspective which should begin to provide shareholders with real returns.

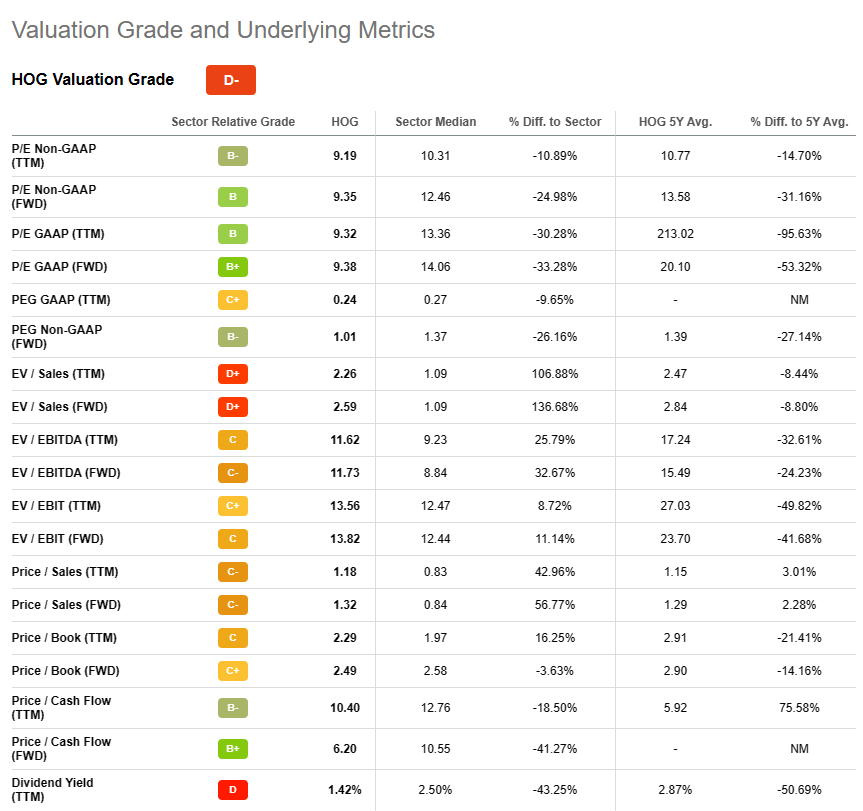

Valuation

Seeking Alpha HOG - Quant Valuation

{kind=link}

Seeking Alpha's quant system has assigned a D- valuation rating for Harley, which I think might be a little harsh as it implies the stock is overvalued. Their FWD P/E GAAP of 9.38 is below the sector median of 14.06 and well below their 5Y average of 20.10.

However, their FWD EV/EBITDA of 11.73 is well above the sector median of 8.84. Equally, their EV/Sales FWD multiple is only 2.59. This is simply poor and suggests the company is valued well above their sales potential.

I believe these metrics illustrate that shares are currently trading approximately at their intrinsic market value. While the underpinnings of Harley-Davidson are strong and the fruits of their Hardwire strategic plan are beginning to surface, the share prices are simply well above the deep-value levels we look for here at The Value Corner.

In the short term (3-10 months) it is difficult to say what the stock will do. I believe the stock price will exhibit some bearish tendencies due to the difficult macroeconomic environment combined with an associated sell-off after the recent rally Harley has seen.

However, the much-awaited Q4 and FY2022 reports could even bring a boost to the share price if results are as positive as we are expecting.

In the long-term (2-4 years) their strong position as a profitable motorcycle manufacturer mega- combined with a new efficiency-focused operations model should allow Harley to continue generating meaningful shareholder value.

Considering that share prices currently reflect the firm's intrinsic value, the stock would have to drop closer to the $30 mark before an investment argument could be made from a deep value perspective.

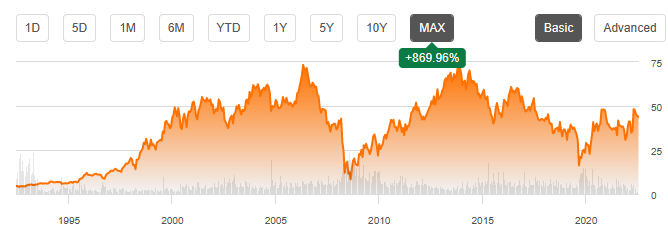

Risks Facing Harley-Davidson

The primary risks facing Harley-Davidson arise from the highly cyclical industry in which it operates as well as from their ageing consumer base. Careful consideration of global economic factors is critical when investing in such companies.

Harley-Davidson Historical Share Prices - Seeking Alpha

{kind=link}

Harley's sales and historical share prices have been closely tied to the prevailing macroeconomic conditions. The fear and very real reality of a potential recession impacting markets in 2023 could hamper their Hardwire strategy and limit spending on crucial R&D for the LiveWire bikes.

This potential economic slowdown could be further hampered by Harley's ageing consumer base with a majority of customers being in the over-35 demographic.

The risks associated with a maturing consumer base is the potential for a sales slowdown as more mature demographics tend to be more conservative with spending. Furthermore, the risk of the brands identity becoming antiquated would threaten Harley's entire strategy of ensuring a "lifestyle" around their bikes.

Harley's homepage Christmas advert (Harley-Davidson BE)

{kind=link}

If this lifestyle is to be associated with an older demographic, the brand could begin losing interest in younger consumers mindsets, a situation which arguably has been the case for the past five years.

Harley of course aims to change this with their LiveWire brand and push for more sporty, youthful motorbikes. However, the success of this strategy in and of itself is highly uncertain. Harley could fail in the execution of their electric motorcycles as well as in the subtle rebranding towards a younger generation.

Furthermore, the company could risk alienating current customers if they begin to neglect the rumbling cruisers the firm has built their image on.

From an ESG perspective, Harley only really faces one threat; quality control. The shutdown of their manufacturing facilities in May of 2022 due to a "regulatory compliance matter relating to a third-party supplier's component part".

Clearly, this component issue must have been truly significant since it halted all deliveries, sales and manufacturing for two entire weeks. Interestingly, the LiveWire bikes were not impacted by this part, suggesting it may have had something do with Harley's combustion engine technology.

Should Harley continue to face such significant component quality issues, they may begin to feel the very real fiscal consequences that follow. However, such a large-scale issue does seem to be a unique event and most likely should not replicate itself any time in the near future.

Summary

Harley-Davidson has had a rough couple of years leading-up to 2022. However, solid business fundamentals, strong brand strength and a new focus on efficiency have allowed the company to grow sales revenues significantly while remaining profitable throughout.

Unfortunately, share prices are approximately fairly valued leaving potential value investors with little to base a strong investment thesis on.

While The Value Corner does not see Harley-Davidson as a good value opportunity at its current valuation, it will be interesting to re-evaluate the situation should shares drop to a more budget-oriented price point.

If you are looking to immediately increase your portfolio exposure towards the consumer cyclical sector, it may be prudent to consider other alternatives such as Volkswagen ( OTCPK:VWAGY ) or even BMW ( OTCPK:BMWYY ).

For further details see:

Harley-Davidson: Ready To Rumble, Electrically