HLIT - Harmonic: I'm Still A Buyer

2023-09-13 08:41:03 ET

Summary

- Harmonic's share price has dropped by 36% due to disappointing earnings, but the company is expected to see significant earnings growth by 2024.

- The video segment is the fastest-growing division, driven by a surge in SaaS revenue, highlighting Harmonic's ability to capitalize on the demand for video-related services.

- Harmonic is focusing on securing multi-year contracts to establish stability and predictability in revenue streams, and its collaboration with Charter Communications is a positive step for future growth.

Investment Rundown

Since my last article about Harmonic ( HLIT ), the share price has shrunk by around 36% as the last report from the company shook the price and sent it tumbling. The share price is now trading at a p/e of just 22 on a FWD basis, all the whilst the estimates suggest a significant bump up by 2024 in the earnings, making it trade at a p/e of 11 on 2024 estimates. For me, HLIT is a growing company and one that should be valued as such as well. This means I see them at around 18x - 20x earnings at least. In 2024 that would mean a price target of $16. That indicates a significant markup from the current share price and one that I think is achievable as well. HLIT doesn't hold a significant amount of debt anymore which has greatly helped in avoiding larger interest expenses which would put pressure on the net incomes. Some tailwinds to look for though will be further easing in getting hardware sales out across the segments. For now, though, I still like the business and the healthy balance sheet is making it easier to be bullish on the long term I think.

Company Segments

The company comprises two primary segments : broadband and video. Notably, the video segment stands out as the fastest-growing division, with its impressive performance attributed largely to the substantial YoY increase in SaaS revenue, which has surged by a remarkable 72%. This remarkable growth underscores the company's success in harnessing the burgeoning demand for video-related services and highlights its ability to capitalize on the evolving digital landscape.

HLIT is strategically focusing on securing robust multi-year contracts as a means to establish stability and predictability in the company's future revenue streams. This approach not only enhances revenue predictability but also cultivates reliable cash flows, which can be channeled into the development of new products and technologies. The recent collaboration with Charter Communications ( CHTR ) is a significant step forward for HLIT, solidifying its foothold in the market and paving the way for sustained growth across its two primary segments. This partnership positions HLIT favorably to capitalize on evolving market opportunities and further bolster its market presence. The last quarter may have been a bump in the road as revenues and EPS both missed , but I still think the company looks appealing on a long-term outlook.

Earnings Highlights

As I have mentioned already, last quarter's results showcased some difficulties for the business. There were some challenges that the company had to overcome, like a lack of hardware sales across both the broadband and the video segments of the business.

{kind=link}

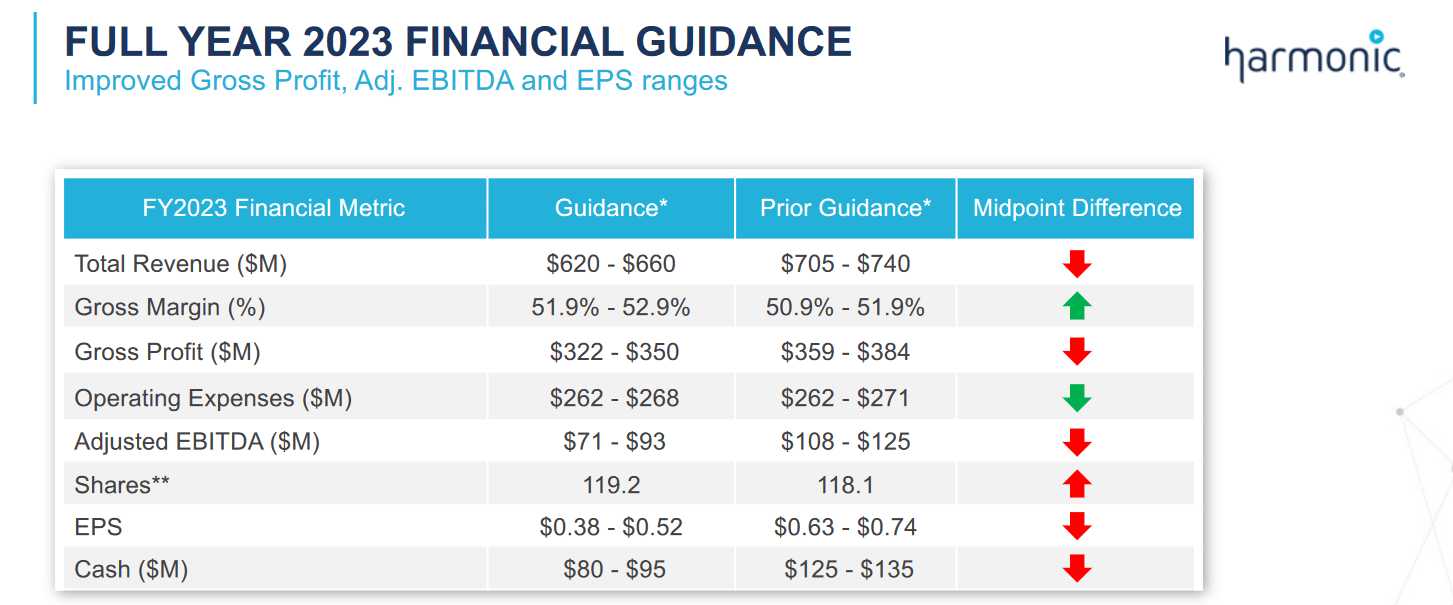

The short-term challenges for HLIT have caused them to be forced to revise the guidance for 2023 downwards. The EPS is estimated to be at $0.38 - $0.52. I would expect that the closer we get to Q4 the better we will know where in that spectrum we will land because it's a little bit broad still. What the company does expect of 2023 though is better gross margins, increasing the guidance by 1% which I think indicates that perhaps better pricing environments are coming along. If HLIT can cut down on the cost of goods and materials then they will be able to perhaps even beat these estimates.

{kind=link}

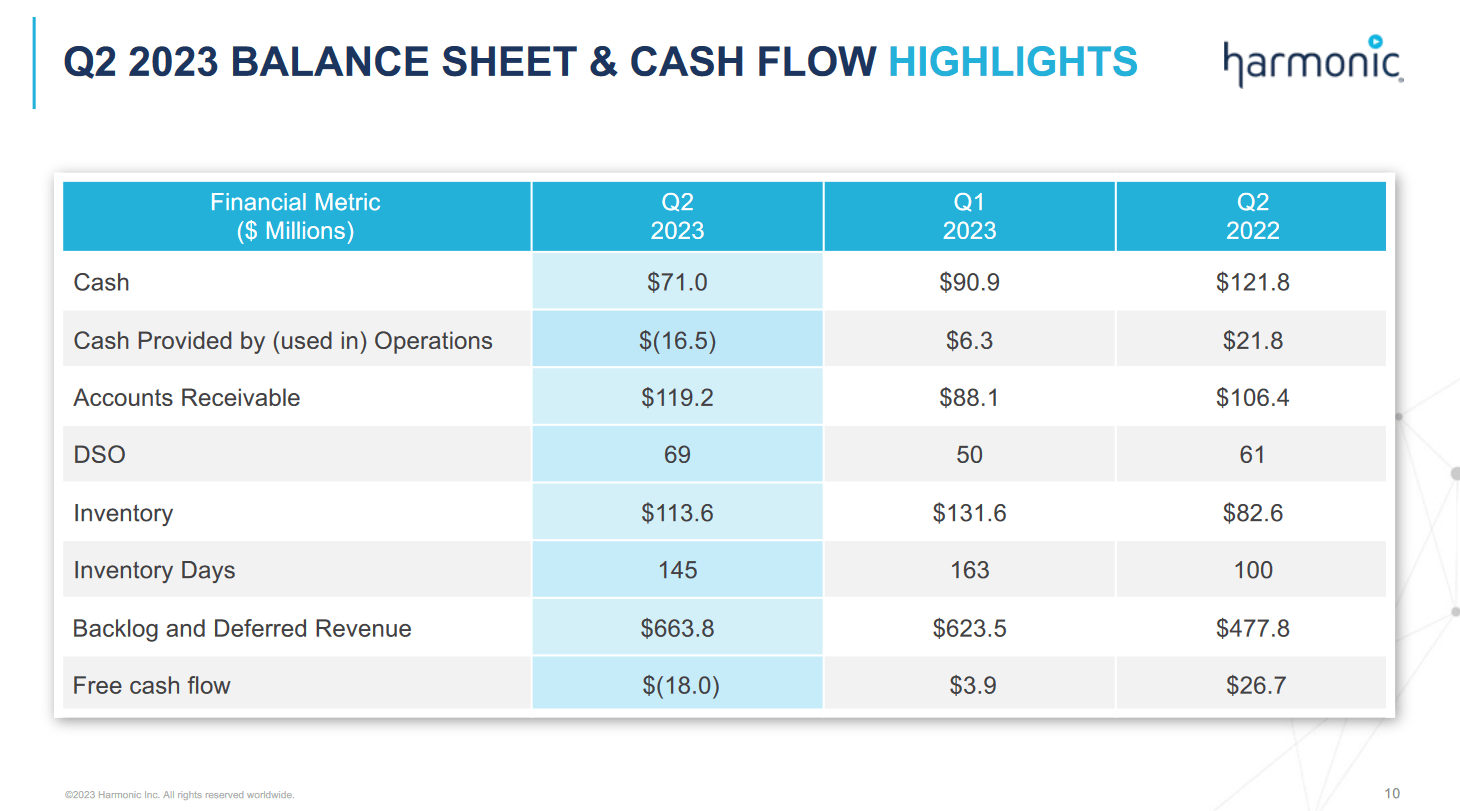

Where I think HLIT continues to excel is the balance sheet. The cash position may have seen a decline YoY, but HLIT has maintained a low amount of debt through the last few years. Back in 2021, the company had over $100 million of debt, but that has since been reduced to around $11 million instead. The inventory levels for the company have been climbing a decent amount, but seeing the lack of revenues is worrisome I have to admit. Seeing inventory levels rise and not be followed by better revenues indicates to me the market conditions aren't perhaps the best and demand is slightly softening. Moreover, though, the backlogs have been climbing very well for HLIT and right now are at the highest levels in the company's history, over $600 million.

Risks

One significant area of concern when considering an investment in HLIT at its current valuation revolves around the potential for a slowdown or disappointment in its SaaS business segment. This segment not only represents the most profitable aspect of HLIT operations but also boasts the highest growth trajectory within the company.

In addition to the concerns mentioned, another factor that warrants attention is the gradual dilution of shares over the years. While the company has been experiencing growth in its business operations, it appears that this growth is primarily offsetting the decline in value per share that investors are experiencing due to share dilution. This situation raises a red flag, especially if the trend of lower EPS growth and ongoing share dilution continues. If these issues persist, it might lead to a reconsideration of my buy rating, possibly downgrading it to a hold recommendation. Therefore, investors must keep a close eye on both the company's EPS performance and its share dilution practices when assessing their investment in HLIT.

SaaS Market (verifiedmarketresearch)

Looking at the last report specifically the company noted some difficulties in getting hardware sales out the door. The delays across the business segments of HLIT caused the revenues to come in lower than expectations. That seems to have caused the share price to fall so quickly. That to me underscores some of the implied volatility of the stock and the fact that on bad news, HLIT can quickly falter.

Final Words

I have covered HLIT before and the last few months have been nothing but unrewarding in terms of the share price, unfortunately. The company failed to meet expectations in the last report and that caused the share price to tumble. I still think the company is very solid and remains to be a buy-in my opinion. The market outlook is solid and HLIT has done a great job in finding a healthy financial position to operate from which limits the need to dilute significant amounts of shares. I continue to be bullish on HLIT stock and will be reiterating my buy rating.

For further details see:

Harmonic: I'm Still A Buyer