HMY - Harmony Gold: Shiny Fundamentals But A Dull 2024 Outlook For Gold

2023-12-04 05:05:34 ET

Summary

- Harmony Gold Mining Company stock warrants a hold rating due to mixed variables impacting its share price.

- The company itself has demonstrated strong growth and profitability, but its profitability is dependent on the commodity price of gold.

- The outlook for the price of gold in 2024 is uncertain, and global gold production is expected to slow, impacting Harmony Gold's revenue.

Investment Thesis

Harmony Gold Mining Company Limited ( HMY ) warrants a hold rating due to multiple mixed variables impacting its share price going into 2024. Key factors buoying the company into next year are its growth, profitability, and valuation metrics. However, the company’s profitability is dependent on the commodity price of gold itself which will see a muted return over the next year. Additionally, global gold production will likely slow in coming years impacting HMY’s ability to generate long-term revenue.

Company Overview and Competitors

Harmony Gold is an international mining company that produces gold in South Africa, Australia, and Papua New Guinea. The company has a $3.93B market capitalization and engages in the exploration, mining, and processing of precious metals. While the company also mines silver and copper, gold represents the preponderance of its revenue. There are numerous international competitors in the gold production industry. For comparison purposes, similarly sized competitors examined are Eldorado Gold Corporation ( EGO ), Equinox Gold Corporation ( EQX ), Kinross Gold Corporation ( KGC ).

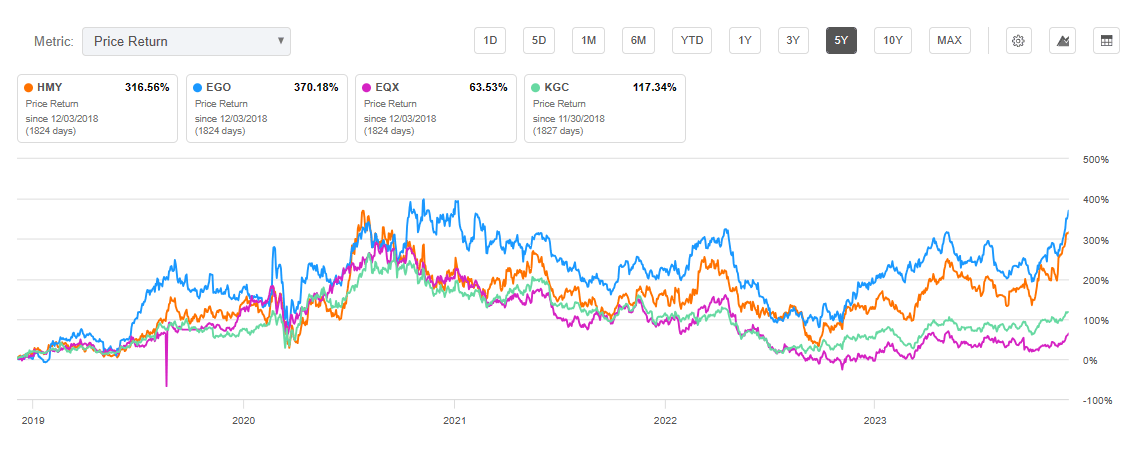

Historically, HMY has demonstrated a 10-year share price CAGR of 9.1% and 5-year share price CAGR of 33.0%. Impressively, HMY is up 78% YTD, outshining most competitors. This recent performance is a credit to the company’s fundamental metrics including growth and profitability. I will cover more on these later.

5-Year Price Return: HMY and Peer Competitors (Seeking Alpha)

{kind=link}

Outlook for Gold Commodity

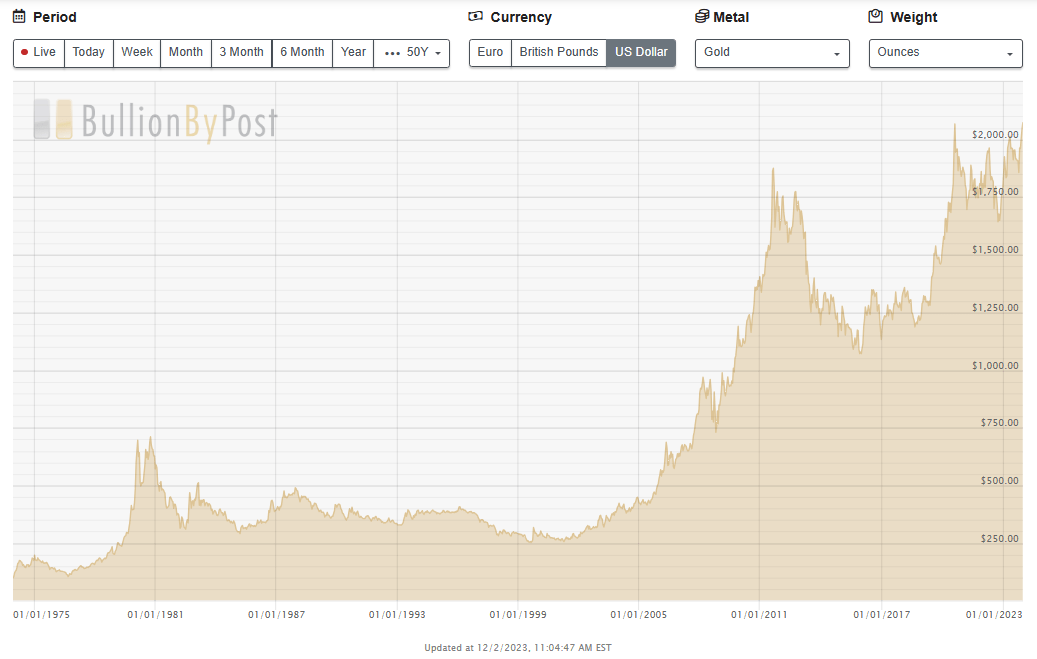

The price of gold has a direct impact on HMY’s returns. The higher the price of gold, the greater the return for Harmony Gold and its competitors. However, the outlook for the price of gold in 2024 is not as bright as one would like. Between 1971 and 2019, gold had an average annual return of 10.6% . Global stocks over the same period returned 11.3% on an average annual basis. Generally, gold and stocks are inversely correlated. The current price per ounce of gold is $2,072. This price represents a 12.2% increase YTD , compared to the S&P 500’s YTD performance of about 20%.

Price Per Ounce of Gold: 1975-Present (Bullionbypost.com)

{kind=link}

Looking forward, a price increase for gold in 2024 is questionable. This is because gold’s price has factors working both for and against it. Because gold is typically treated as a hedge against inflation, the price of gold normally increases in times of high inflation. With elevated interest rates and declining inflation expected into next year, there is no reason to expect a large jump in gold's price based on this factor.

Factors working in favor of an increase in gold’s price are geopolitical instability, recession, and a bear market for equities. Because of these numerous factors, forecasts for gold’s price by the end of 2024 vary largely. While the World Bank predicts that average price will drop to $1,700 per ounce , I am inclined to agree with other forecasts for $2,050 per ounce in 2024, a decline of 1%. With a less than stellar expected increase in gold’s price in 2024, there is no strong reason in my mind for HMY to warrant a buy rating.

HMY's Strong Growth and Profitability

Despite a dubious forecast for gold’s price, Harmony itself has seen growth and profitability that have been superior to competitors. First, the company demonstrated a 59.7% YoY gross profit growth while achieving a 16.3% YoY reduction in its cost of revenues. Second, HMY is expected to see an EBITDA growth FWD of 26.2%, higher than major competitors. Furthermore, Harmony is not only seeing top line growth. Its net income margin is at a solid 9.8%, 66% higher than its sector average.

Growth and Profitability Metrics for Harmony Gold and Peer Competitors

| HMY |

| EGO |

| EQX |

| KGC |

| EBITDA Growth FWD |

| 26.24% |

| 3.64% |

| 9.90% |

| 1.28% |

| Net Income Margin |

| 9.78% |

| 5.88% |

| 4.53% |

| 5.83% |

| Return on Equity |

| 15.03% |

| 1.70% |

| 2.03% |

| 3.93% |

| Return on Assets |

| 11.00% |

| 2.15% |

| 0.00% |

| 2.21% |

| Total Debt to Equity |

| 17.84% |

| 18.04% |

| 47.84% |

| 39.72% |

Source: Seeking Alpha, 2 Dec 23

With $3.04B in total assets compared to $1.19B total liabilities, Harmony has striven to expand operations while not increasing debt. Its return on equity and return on assets are both very strong and higher than major competitors. Recently, Harmony reported a 278% increase in operating free cash flow for Q1FY24.

HMY does offer an annual dividend with 0.63% dividend yield. While HMY has a low payout ratio of 9.49%, its dividend safety is dependent on continued gold production and profitability. HMY has not been consistent in providing a dividend, so reliable income seekers should look elsewhere for a steady yield.

Harmony's Production of Gold and Resource Availability

Harmony’s continued growth is directly dependent on its ability to both produce and explore new gold. Unfortunately, Harmony’s aggregate production of mining operations has declined from 47,755 kg in 2021, down to 46,236 kg in 2022, and further declining to 45,651 kg in 2023. While achieving gross profit growth, HMY’s total revenue growth has not seen a significant increase. This is perhaps due to the increase in gold’s price while production has been muted.

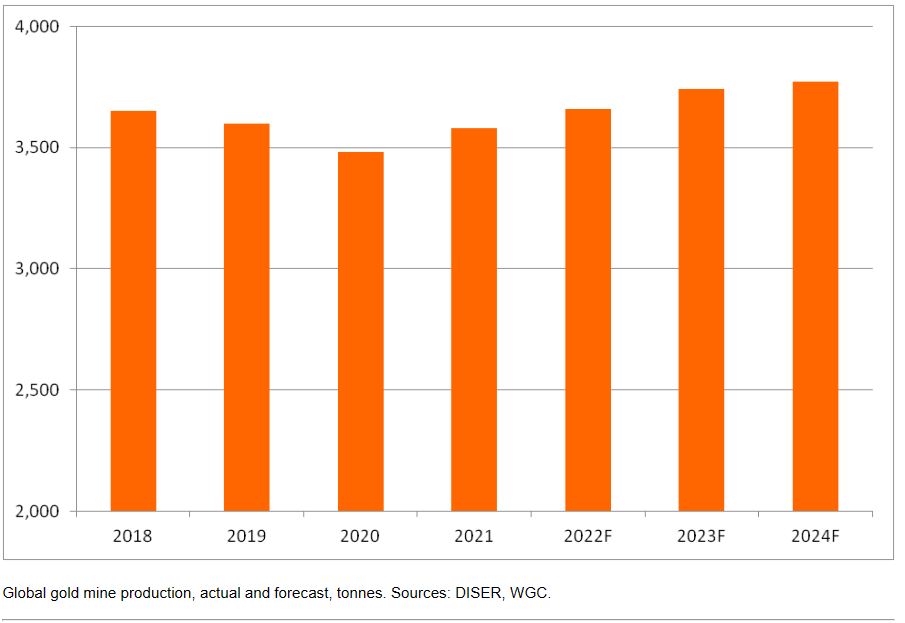

Global Gold Mining Production Forecast Through 2024 (Department of Industry, Science, Energy and Resources of the Government of Australia (DISER))

{kind=link}

On a global scale, gold production also has a murky outlook. Gold mining production is expected to increase until 2024, before starting to decline. While production is expected to see strong growth in China, North America, and Brazil, Australian gold mining production is only expected to grow 6.5% in 2023 and 2024. This is disappointing news to Harmony Gold which has a large portion of its operations in Australia.

Company Outlook and Valuation

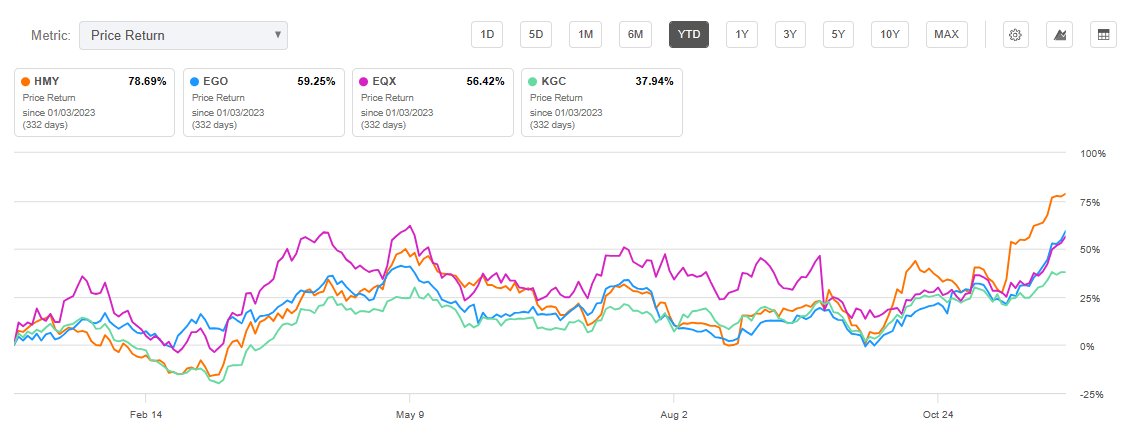

HMY reached an all-time high intraday price of $6.34 just earlier this week. Currently, the stock is at $6.29 at the time of writing this article, just below its all-time high. Additionally, HMY is currently 44.9% above its 200-day simple moving average. Harmony has also seen an extraordinary YTD return of 78.69%, surpassing all peer competitors analyzed.

YTD Price Return: HMY and Competitors (Seeking Alpha)

{kind=link}

Despite this massive return YTD, Harmony demonstrates multiple favorable valuation metrics. HMY has a P/E GAAP FWD of only 8.56, 49.25% lower than its sector and lower than all competitors examined. Harmony also has an EV/EBITDA FWD below all competitors examined and 40.9% below its sector. Finally, HMY’s EV/sales FWD is only 1.38, lower than competitors and 10% lower than its sector.

Harmony Gold and Major Competitor Forward-Looking Valuation Metrics

| HMY |

| EGO |

| EQX |

| KGC |

| P/E GAAP FWD |

| 8.56 |

| 38.08 |

| 37.73 |

| 32.05 |

| EV/EBITDA FWD |

| 4.82 |

| 6.26 |

| 9.52 |

| 5.41 |

| EV/Sales FWD |

| 1.38 |

| 2.75 |

| 2.20 |

| 2.27 |

Source: Seeking Alpha, 2 Dec 23

Despite strong fundamentals and favorable valuation metrics, the macro factors for gold represent headwinds for the stock. I expect HMY’s price to remain relatively flat going into 2024 and see less than average returns compared to its historic CAGR. This is consistent with low growth in both the expected price of gold and global gold production.

Volatility and Risks to Investors

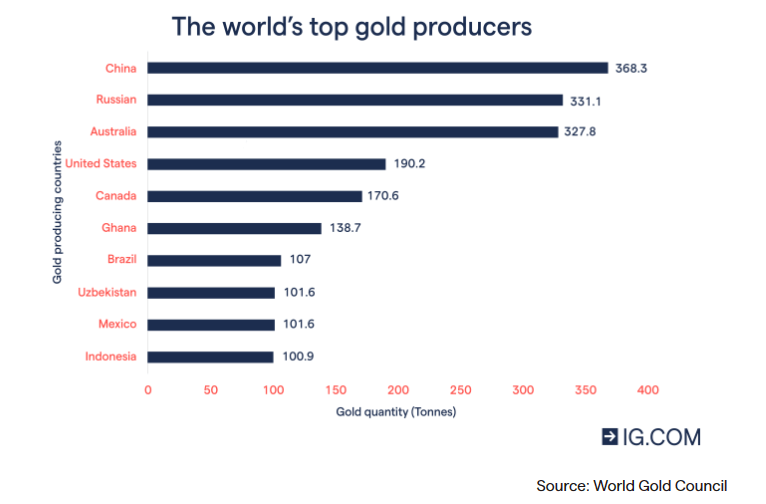

Numerous risk factors impact the gold industry, and therefore Harmony Gold, including reduction in gold demand, the strength of the U.S. dollar, inflation, and interest rates. Given Harmony’s strong recent fundamentals, the largest risk factor for investors is a drop in the price of gold. While Harmony’s aggregate production of mining operations has been relatively flat, production in China is increasing. China’s gold output rose 13.1% YoY in 2022 . A strong increase in supply without a notable increase in demand will lower gold’s price, thereby negatively impacting Harmony’s profits.

Annual Metric Tons of Gold Produced by Country (World Gold Council)

{kind=link}

Beyond supply and demand concerns, infrastructure requirements for gold mining are costly. Inflation and increasing prices of production squeeze profits for gold mining companies forcing some to close unprofitable mines. Theft and illegal mining both represent additional threats to a mining company’s profitability due to the need for increased security.

Ending Harmony’s risk analysis on a positive note, gold itself has held its value for thousands of years. While the commodity has seen price fluctuations similar to equities, it will likely continue to be a valuable asset for a very long time. Additionally, HMY is not a particularly volatile stock with a 24M beta of 1.31 and a 60M beta of 0.90. Investors seeking to reduce risk may find greater diversification in gold ETFs such as VanEck Gold Miners ETF ( GDX ), VanEck Junior Gold Miners ETF ( GDXJ ), or VanEck Africa Index ETF ( AFK ) which all have HMY as a holding.

Concluding Summary

Harmony Gold warrants a hold rating as there are multiple factors working in favor, and against, returns for the company. While HMY has demonstrated solid fundamentals including strong YoY gross profit growth and net income margin, there are multiple factors working against the price of gold going into 2024. Additionally, global gold production is expected to be limited in the coming years with an exception for countries such as China. For Harmony specifically, we have already seen a drop in production over the past three years.

While HMY has seen impressive share price returns YTD, the company has favorable valuation metrics. Global instability, inflation, interest rates, and the strength of the U.S. dollar all have direct impacts on HMY’s ability to remain profitable. There are therefore simply too many factors that prevent me from considering HMY a buy and recommend a hold for investors.

For further details see:

Harmony Gold: Shiny Fundamentals, But A Dull 2024 Outlook For Gold