MAXN - Harnessing The Sun's Power: Maxeon's Journey Towards A Brighter Future In Solar Energy

2023-06-09 21:13:20 ET

Summary

- Maxeon, a key player in the solar energy market, is known for its high-efficiency IBC module designs and strong distribution network.

- MAXN has strong growth prospects in Europe, and is implementing cost reductions across the supply chain.

- I anticipate margin expansion through a synergistic combination of factors, including the scaling up of Max-6 capacity, securing higher ASPs for utility-scale contracts, and rising residential orders within the US.

Introduction

As a passionate advocate for clean energy solutions, I am always on the lookout for companies that are driving the transition to a sustainable future. One such company that has been on my radar is Maxeon Solar Technologies ( MAXN ). Known for its premium-priced, high-efficiency IBC (Interdigitated Back Contact) module designs, Maxeon has positioned itself as a key player in the solar energy market. In this article, I will delve into Maxeon's strengths, growth prospects, and recent financial performance, shedding light on why I believe MAXN stock is worth considering (and what risk factors to bear in mind).

MAXN was spun off as a separate entity from SunPower Corp ( SPWR ) in Q3 2020 and represents SPWR's former upstream manufacturing operations (which include manufacturing facilities located in the Philippines, Malaysia, Mexico, and France, as well as a 20% stake in an HSPV manufacturing operation in China). MAXN possesses valuable intellectual property related to its proprietary IBC cell technology and proprietary shingling (P-series) technology. The company's headquarters are situated in Singapore.

MAXN is the manufacturer and distributor of the “SunPower” solar modules and has established a solid distribution network for its products. MAXN has a two-year supply agreement with SPWR in the United States, enabling widespread distribution of its modules. In China, the company's P-series modules are distributed through HSPV, a joint venture with TZS. Outside the United States and China, MAXN owns its own distribution line, supplying approximately 1,000 channel partners.

Maxeon's Technology & Differentiated Offerings :

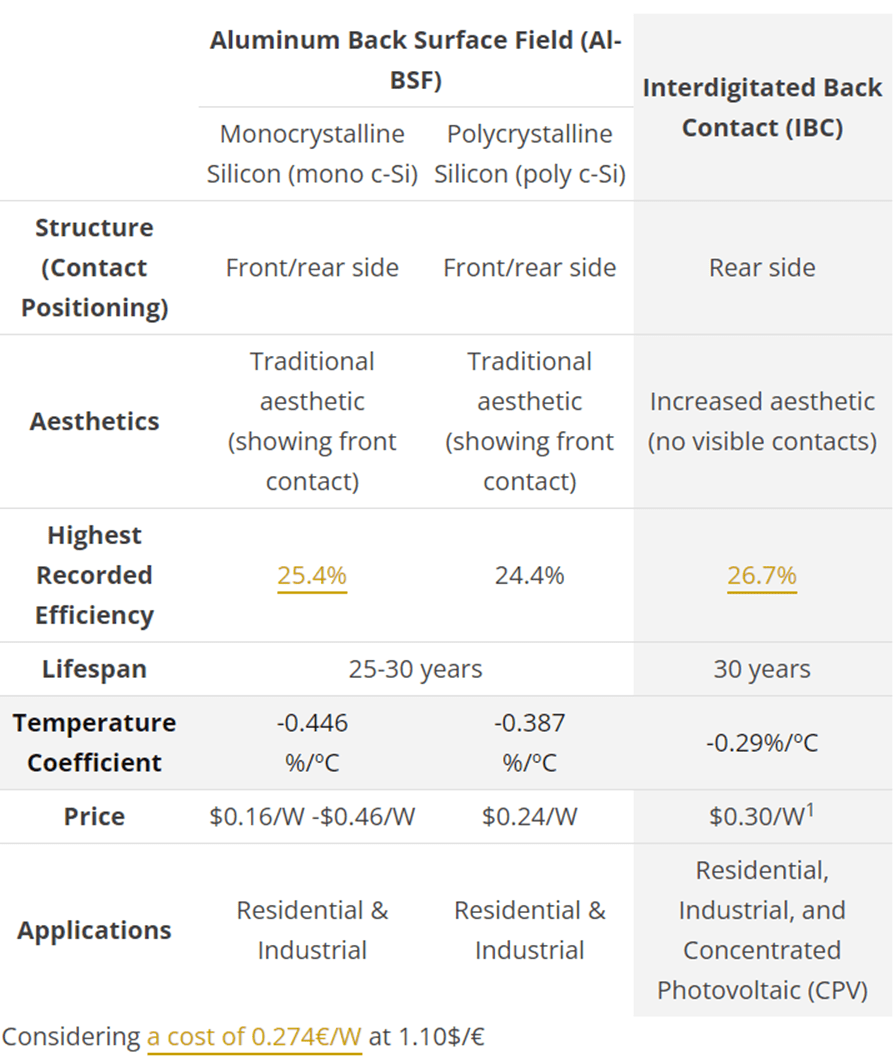

In the quest for solar panels with more power, the solar industry has explored various solar cell technologies aimed at minimizing power losses, boosting efficiency, and lowering production costs for photovoltaic (PV) modules. Among these various technologies, the IBC solar cell technology stands out as a particularly innovative approach that has demonstrated superior efficiencies when utilizing crystalline silicon cells.

Maxeon sets itself apart by offering two distinct solar module designs. Firstly, the company provides an innovative IBC module design, which has received significant praise within the industry. This premium-priced product combines cutting-edge technology with exceptional efficiency of up to 26% , making it highly desirable for consumers seeking optimal performance. Secondly, Maxeon offers a lower-cost P Series shingled product, which, while less differentiated, provides an attractive option for price-conscious customers.

{kind=link}

IBC technology has made remarkable advancements, achieving a noteworthy 26.7% efficiency as its highest record, overtaking traditional technologies by 1.3%. The improved efficiency allows for the production of IBC solar panels without any spacing between the cells. This maximizes the power output per m 2 for each module. These features make IBC solar cells quite attractive for applications in limited space, offering enhanced power generation capabilities in confined environments.

Maxeon’s SunPower panels have a stated degradation rate of 0.2% per year and exhibit an initial energy output that surpasses traditional panels by up to 25% in its initial year. Over 25 years, this margin further amplifies to about 45% more energy, resulting in an average increase of 35% in energy production throughout the first 25 years. Comparing this to the average panel degradation of 0.50% seen in standard PV panels, you can begin to see the appeal of Maxeon’s premium product line.

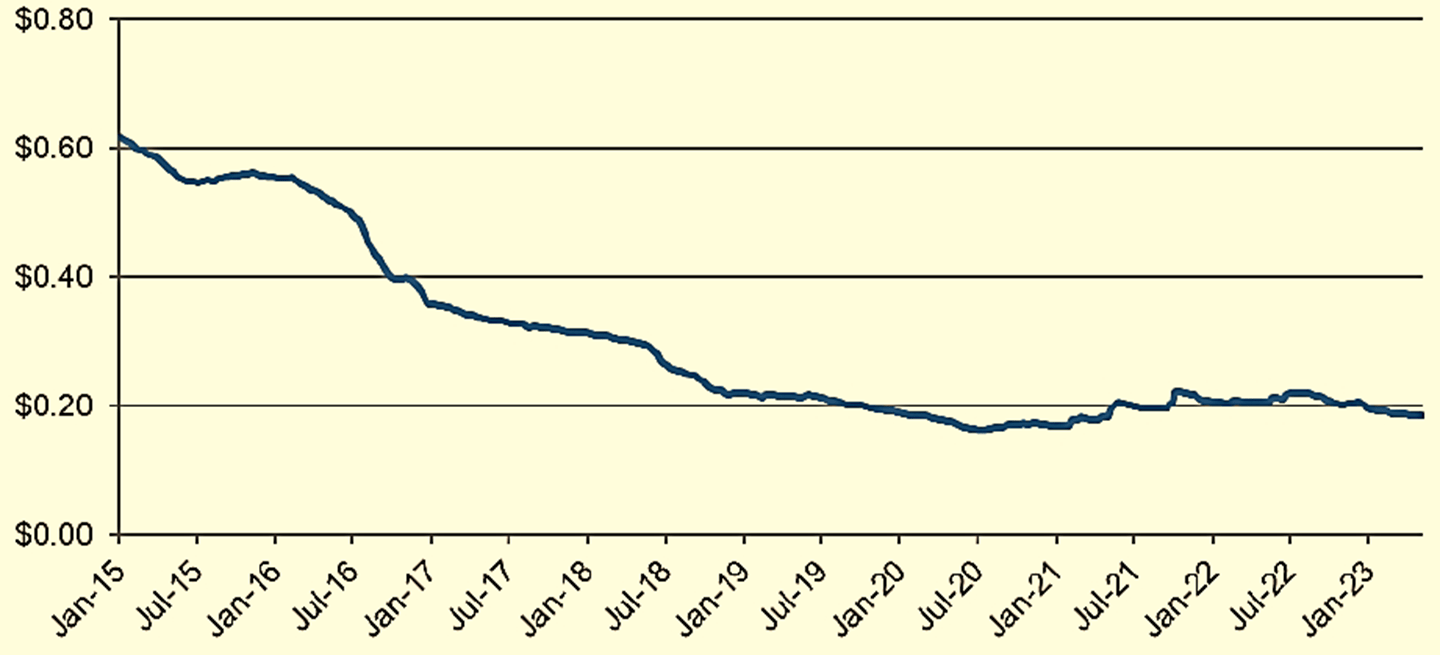

Declining Cost Price of Crystalline Modules

Global Benchmark Price of Crystalline Modules ($/W) (PVinsights.com)

{kind=link}

In addition to the favourable market conditions and growth prospects, Maxeon also benefits from the declining costs of global benchmark crystalline module pricing. The global benchmark price for crystalline modules, currently at $0.184 per watt as of May'23, decreased 4% QoQ and decreased 10% YoY. This downward trend in pricing is a result of various factors, including economies of scale, technological advancements, and increased competition in the solar industry. As the costs of solar modules continue to decline, it not only makes renewable energy more affordable but also enhances Maxeon's competitiveness in the market. The company's ability to offer premium solar modules at competitive prices positions it well to capture a larger share of the growing solar market.

Financial Performance:

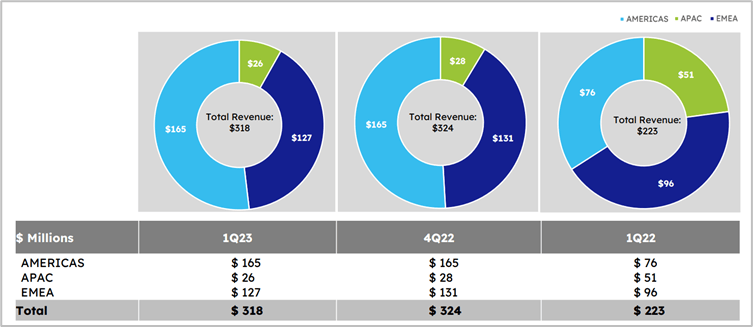

Maxeon's recent financial performance showcases its potential for growth. In the Q1 2023 earnings report, the company achieved positive EBITDA, exceeding both my expectations and the consensus of Wall St. analysts. This milestone underscores the effectiveness of Maxeon's business strategy and its ability to deliver results. Q1 revenue of $318 million, which was within the guidance range of $305-345 million, marked a 43% YoY increase. Gross margin also showed impressive growth, reaching 16.8% and indicating the company's commitment to profitability. Furthermore, adjusted EBITDA of $31 million entering positive territory for the first time in Maxeon's history as an independent entity is a significant accomplishment.

{kind=link}

Positive Guidance

In the Q1 earnings report , Maxeon's management raised guidance for 2023, projecting a robust 41% increase in revenue and flattish-stable EBITDA from Q1. This revised guidance suggests a strong performance throughout the year. MAXN is fully allocated for utility-scale with 4.2GW cumulative bookings through 2025 and an additional 1.5GW with advance deposits through 2027.

Expansion & Growth

Last month, MAXN announced the pricing of an underwritten public offering , consisting of a total of 7.49 million ordinary shares, which includes 5.62 million ordinary shares offered by Maxeon plus 1.87 million ordinary shares offered by a TotalEnergies SE (TTE) affiliate. The shares are priced at $28.00 per share and the company anticipates receiving about $157.4 million in gross proceeds from the public offering. The proceeds will be used to fund a 50% ICB capacity expansion with the addition of 500MW in annual capacity for Maxeon’s next-gen Maxeon 7 cells and modules. To facilitate the planned expansion of IBC manufacturing capacity, Maxeon estimates total capital expenditures of approximately $200 million. It is worth noting that one of Maxeon's previously closed facilities in the Philippines will be utilized for this purpose.

This increased volume will serve as an opportunity for Maxeon to expand its market share in core Distributed Generation "DG" markets. The company will particularly focus on boosting its supply volume in the newly established U.S. residential channel, where the company sees the highest global ASPs (Average Selling Prices). Maxeon also plans to capitalize on the additional capacity to increase the volume of its IBC cells in the European channel while optimizing the mix of Maxeon and Performance line product sales.

Maxeon is also well-positioned to capture additional market share in the US residential market on the back of LG’s exit from the Solar PV manufacturing business and the launch of the new CED Greentech Renewables distribution channel.

USA’s Inflation Reduction Act as a Catalyst

Maxeon's plans to establish a U.S. manufacturing footprint holds promise for future profitability as it stands to also benefit from the Inflation Reduction Act’s IRC 45X incentive.

The current guideline of IRC's domestic content presents a favourable opportunity for US-based solar panel manufacturers, and I think MAXN is qualified for the 10% manufacturing tax credit, whereas it would be difficult for module producers like Canadian Solar Inc ( CSIQ ) (that only assemble modules in the US) to satisfy the requirement of domestic content.

While the timeline for U.S. production remains uncertain, with 2025 being the earliest possible opportunity, the potential for growth in this market is substantial.

Europe's Energy Transition as a Catalyst:

One of the key factors that excite me about Maxeon is its above-average exposure to the European Union's energy transition story. EMEA already accounts for nearly 40% of Maxeon’s Q1 2023 revenue, and with the region placing increasing emphasis on climate policy and energy security, Maxeon stands to benefit greatly from the growing demand for renewable energy solutions. As governments and businesses strive to meet their sustainability targets, Maxeon's premium offerings and focus on high-quality solar modules position the company for success in this evolving market landscape.

The European Green Deal Industrial Plan announced in March 2020 (part of the European Green Deal) aims to accelerate the transition to a sustainable and climate-neutral economy. As part of this initiative, the EU is actively promoting renewable energy sources, including solar power, and encouraging the development of domestic manufacturing capabilities required to meet Europe’s climate targets. This presents a significant opportunity for Maxeon to potentially revive its European manufacturing footprint.

It is worth noting that Maxeon had to shut down its factory in France in 2022, citing price pressures and an unfavourable tax environment. However, with discussions underway regarding the Green Deal Industrial Plan, I believe there might be a medium-term possibility of reestablishing manufacturing operations in Europe. Such a move would not only align with the EU's renewable energy goals but also strengthen Maxeon's market presence in the region.

Valuation and Investment Opportunity:

Considering Maxeon's position as an Asia-based hardware pure-play in a rapidly expanding industry, I believe it deserves a valuation range of 10-14x adjusted EBITDA. This range aligns with the company's long-term revenue growth projection of 10-15% and an estimated EBITDA growth rate of approximately 1.5x. Based on these factors, my target price for Maxeon's stock is $34, reflecting a valuation of 13x 2024E adj. EBITDA of $130 million. This valuation represents an upside potential and makes Maxeon an attractive investment opportunity. Additionally factoring in the estimated NPV of the planned 3.3GW expansion project in the U.S. contributes ~$8/share to the subsequent valuation on a per-share basis.

Factors that could potentially lead to shares deviating from our price target to the upside include (1) a higher-than-expected increase in demand for solar modules; or (2) a higher-than-anticipated demand for back-contact and shingled modules.

Conversely, factors that could potentially result in shares deviating downwards from our price target include (1) an unanticipated increase in polysilicon pricing; or (2) weaker-than-expected global policy support for solar projects.

I set my Bear case scenario at $21, based on 8x 2024E adj. EBITDA and a LT revenue growth of 5-10%. My Bull case of $40 is based on 16x 2024E adj. EBITDA, representing LT revenue growth of 15-20%.

Share Price Performance:

I believe that much of the stock's strong YTD performance, even prior to Q1 results, can be attributed to the market's anticipation of a DOE loan guarantee approval for MAXN. This approval is expected to pave the way for MAXN's planned 3.3GW P-series expansion in the U.S. with highly favourable economics. However, I also believe that this focus on the future prospects of the loan guarantee approval has caused the market to overlook the ongoing turnaround in MAXN's fundamental legacy operations, particularly in relation to the premium IBC line. The company has been taking the IBC line to the next level with Maxeon 7, which resulted in a strong Q1 performance. Consequently, both the impressive Q1 results and the IBC capacity expansion were somewhat unexpected developments.

Key Risks

International trade tariffs:

Several countries have either levied or are considering the possibility of levying tariffs on various components in the solar value chain. These tariffs (such as the US Safeguard measure) represent a risk to MAXN’s business as the company sources materials and supplies modules globally. While IBC components are exempted, Maxeon's panels using other technologies (such as its mono-facial Performance Line modules assembled in Mexico) are not yet exempt.

Subsidy Dependency:

MAXN has significant module sales in the U.S. through its supply agreement with SPWR which makes it vulnerable to changes in government policies and subsidies. Reductions or eliminations of solar subsidies could substantially reduce demand for MAXN's modules and adversely impact its core business.

Exchange/Currency Fluctuations:

As almost half of MAXN's sales occur outside the U.S., exchange rate fluctuations pose a risk to the company's net profit margins due to revenue and cost exposure to different currencies.

Supply Chain Disruptions:

MAXN's production of solar cells and modules relies on intricate supply chains, some of which may be linked to Xinjiang province in China. Disruptions caused by factors such as labour claims, the COVID-19 pandemic, or costly tariffs could impede MAXN's planned operations.

Customer Concentration:

MAXN's former parent company, SPWR, is its largest customer through an exclusive supply agreement in the U.S. Any challenges faced by SPWR in selling MAXN's modules could significantly impact the company's share performance due to the relatively high degree of customer concentration.

Conclusion

Maxeon's premium solar module designs, exposure to Europe's energy transition, and potential for future profitability from its manufacturing expansion plans make it an enticing stock for investors. With a strong financial performance, positive guidance, and a clear focus on sustainable solutions, Maxeon is poised for growth in the rapidly evolving clean energy market.

Bearing in mind some of the risks associated with Maxeon, I consider the company as a Buy and set a PT of $41.

All in all, I am looking forward to the new CEO & management building on the current momentum and successfully guiding Maxeon towards a new chapter in its journey.

For further details see:

Harnessing The Sun's Power: Maxeon's Journey Towards A Brighter Future In Solar Energy