AMGN - Harpoon Therapeutics: A T-Cell Engager Platform And A Negative Enterprise Value Makes It A Candidate For My 'Bio Boom' Portfolio

- Harpoon Therapeutics has an intriguing platform that can generate stable bispecific immunotherapies using their TriTAC technology. Their “off-the-shelf” T-cell engagers help T-cells eliminate solid tumors and hematologic cancers.

- The company has several catalysts for its pipeline of four clinical assets this year that can validate the TriTAC platform.

- HARP was not immune to the biotech selloff and popped up on my radar after scanning for small-cap healthcare tickers that have a negative enterprise value.

- Harpoon discontinued the development of their lead asset, HPN424. This does raise concerns about the company’s platform, and the rest of their pipeline programs. Therefore, HARP is a Compounding Healthcare speculative "Bio Boom" candidate.

- I am looking to initiate a small position under $2.00 per share in order to take advantage of the current negative EV valuation.

Over the past few weeks, I have been on the lookout for speculative plays that have been beaten down during the recent selloff and have met the criteria to be in the Compounding Healthcare "Bio Boom" portfolio. Harpoon Therapeutics ( HARP ) popped up on my radar after scanning for small-cap healthcare tickers that have a negative enterprise value "EV". It only took a couple of minutes of performing some due diligence for me to remember my initial research into Harpoon following its IPO in 2019 and my interest in the company's TriTAC platform potential. After some deliberation, I determined that HARP is a candidate for the Bio Boom portfolio thanks to the ticker's valuation and the company's upside potential.

I intend to present some background on Harpoon and the company's platform technology. In addition, I provide my views on Harpoon and its investment opportunity. Finally, I discuss how I intend to initiate a position in HARP and will reveal my strategy for managing that position in the second half of 2022.

Background On Harpoon

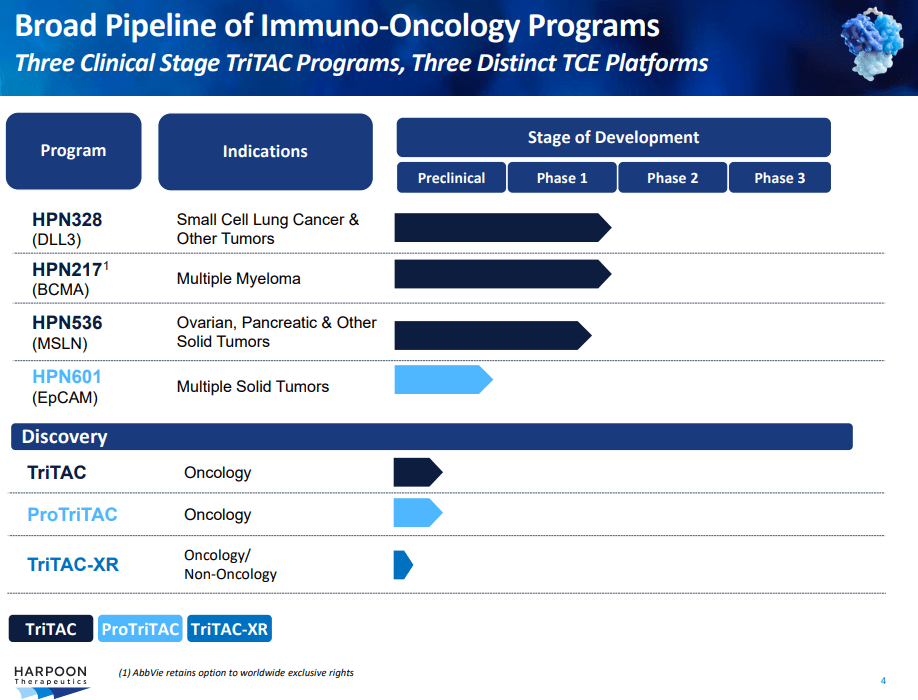

Harpoon Therapeutics is an immunotherapy biotech company that utilizes their TriTAC, ProTriTAC, and TriTAC-XR platforms to discover "off-the-shelf" T-cell engagers that help T-cells eliminate solid tumors and hematologic cancers. With 3 TriTACs in the clinic, along with their pre-clinical assets, Harpoon has the potential to build out a broad pipeline covering numerous oncology indications.

Harpoon is attempting to improve this class of therapies by addressing their stability and half-life in the patient's blood. TriTACs are basically a bispecific bonded to an HSA antibody that permits extended stability, which will help preserve efficacy without the requirement for frequent dosing. TriTACs are expected to sustain their activity despite depressed levels of antigen expression and are not dependent on MHC expression. Moreover, TriTACs are designed to be "off the shelf", which will streamline the manufacturing as well as the dosing procedure.

Harpoon's prodrug TriTAC, termed ProTRiTAC, are T-cell engagers that are designed to activate once it is in close proximity to the tumor. In addition, the company is also testing their TriTAC-XR, which is designed to be an extended-release technology, thus, mitigating cytokine release syndrome "CRS".

This platform has enabled Harpoon to develop clinical assets and close a sizable partnership with AbbVie in 2017 and an expansion of the deal in 2019 .

Harpoon Therapeutics Pipeline (Amgen)

{kind=link}

The company's lead drug candidate from the TriTAC platform, HPN328, is in a Phase I clinical trial targeting DLL3 in small cell lung cancer "SCLC" and neuroendocrine prostate cancer. Harpoon presented interim clinical results from their ongoing Phase I at ASCO in June that revealed anti-tumor activity and a favorable safety profile in SCLC, neuroendocrine prostate cancer, and other neuroendocrine cancers. 39% of subjects had a decrease in the sum of target lesion diameters, with 67% of SCLC patients in the 1.215mg+/week group experiencing a reduction in target lesion diameter. The company highlighted that they saw 1 confirmed partial response with a 53% reduction in lesion diameters at week 10 who had only had stable disease on platinum-based chemo-immunotherapy. An additional SCLC patient treated with 3 prior lines of therapy attained a 65% shrinkage in lesion diameters beyond six months.

In terms of safety and tolerability, the company has reported that there have been no dose-limiting toxicities as well as no stoppages due to adverse events. This includes no grade 3 or higher CRS or instances of ICANS. The company hopes to finish HPN328's dose expansions by the end of this year. Into the bargain, Harpoon entered into a clinical supply agreement with Roche ( OTCQX:RHHBY ) for Tecentriq to be used in planned clinical trials in combination with HPN328 for SCLC.

Harpoon also has HPN536 targeting MSLN in multiple myeloma. The Phase I/IIa dose-escalation trial is ongoing and is estimated to be complete by year-end.

HPN217 targeting has FDA Fast Track designation to HPN217 for relapsed/refractory multiple myeloma. Initial clinical activity was observed in the dose-escalation phase of the ongoing trial. Harpoon expects to start a Phase II dose-expansion trial in the second half of 2022. What is more, Harpoon has a license agreement with AbbVie ( ABBV ) for HPN217 in multiple myeloma and the option for 6 other targets.

The company's leading ProTriTac program, HPN601, is targeting Protease-Activated EpCAM in solid tumors including GI cancers. Harpoon expects to move HPN601 into the clinic with an IND submission in the second half of this year.

My Views

I am incredibly intrigued about Harpoon's platform and their TriTACs designed with 3 components that permit T-cell engagement, extend the drug's half-life and have an antigen-binding domain that could provide a significant advantage over other BiTE technologies. If the company can prove that their assets are operative regardless of MHC expression and are truly modular, we could see Harpoon's TriTACs become a mainstay in numerous treatment paradigms.

If HPN328 is successful in SCLC, it could take advantage of its Orphan Drug Designation in a US market that is expected to have a CAGR of 13.2% through 2030. The Orphan Drugs Designation would allow HPN328 to have up to seven years of market exclusivity in a rapidly growing US market. Obviously, this would be a huge commercial opportunity, while also validating the company's technology and pipeline prospects.

The major opportunity here is Harpoon's compelling platform that could generate nearly countless bispecifics that have the potential to outperform monoclonal antibodies and other bispecifics. Furthermore, Harpoon's TriTACs could prove to be operative in combination therapies and take a similar approach as Affimed ( AFMD ) has taken with their NK cell engagers. Affimed's "three-pronged" development strategy has their engagers as a monotherapy, combination NK cells, and checkpoint inhibitors. I believe Harpoon could take a similar approach to demonstrate how their T-cell engagers can work alone or with some of the most cutting-edge oncology agents. Obviously, having the ability as a monotherapy and combination therapy will dramatically improve the commercial potential for these assets.

Considering HARP's market cap is around $63M, one must concede the ticker is trading at discount for its long-term commercial potential. What is more, the company had $112.5M in total cash and short-term investments at the end of Q1, so HARP is currently trading at -$37.5M EV. Indeed, the company is going to burn through that cash as they progress their pipeline, however, that cash position should last long enough to see some initial clinical data from these programs. What is more, Harpoon's clinical and commercial potential should attract additional partnerships that can bring in non-dilutive funding to help keep the pipeline moving forward.

To recap, Harpoon has an intriguing platform technology that can produce both wholly-owned and partnered programs in some of the fastest-growing markets. Furthermore, HARP is trading at a negative EV thanks to an overblown biotech selloff and a healthy cash position. Considering these points, I am bullish on HARP at these current prices.

Notable Risks

As with all pre-commercial healthcare tickers, HARP has a few notable downside risks to consider before establishing a position. Firstly, the company is going to need significant cash infusions to keep the lights on and move the pipeline forward. The company finished Q1 of 2022 with $112.5M in cash and short-term investments but had a -$20.3M in net income and a -$25.2M cash from operations. At that rate, we can't expect that cash position to last through 2023 unless the company can secure some payments from partnerships. Otherwise, investors need to accept there will be a strong likelihood that Harpoon will have to perform some form of dilutive financing to maintain operations.

Another major concern is that Harpoon has used its TriTAC protein engineering platform with their former lead asset, HPN424 for PSMA targets. HPN424 was taking aim at mCRPC and had amazing preclinical data demonstrating that it induced T-cell-dependent cellular cytotoxicity in PSMA-expressing cancer cell lines and an ability to inhibit tumor growth. The company's Phase I dose-escalation update showed a partial response and declines in serum PSA levels. Unfortunately, the company decided to discontinue the development of HPN424. Clearly, canceling your lead asset does raise concerns about the company's platform, and the rest of their pipeline programs. As a result, investors need to accept that HARP's share price could remain under intense selling pressure for a prolonged period of time until the company is able to validate their platform with another asset.

Another notable risk is competition from companies developing t-cell engagers and similar approaches. First and foremost is Amgen ( AMGN ) with their BiTE pipeline.

Amgen BiTE Pipeline (Amgen)

Amgen already has an FDA-approved BiTE, BLINCYTO, for acute lymphoblastic leukemia and has an impressive pipeline that has programs that are going after the same targets as Harpoon. Obviously, competing against Amgen in both the clinic and potentially on the market will be a tough task that could prevent Harpoon from gaining any traction.

Considering the points above, I see HARP as a highly speculative investment opportunity and will be a candidate for the Compounding Healthcare "Bio Boom" Portfolio. I have assigned HARP a conviction grade of 1 out of 5.

My Plan

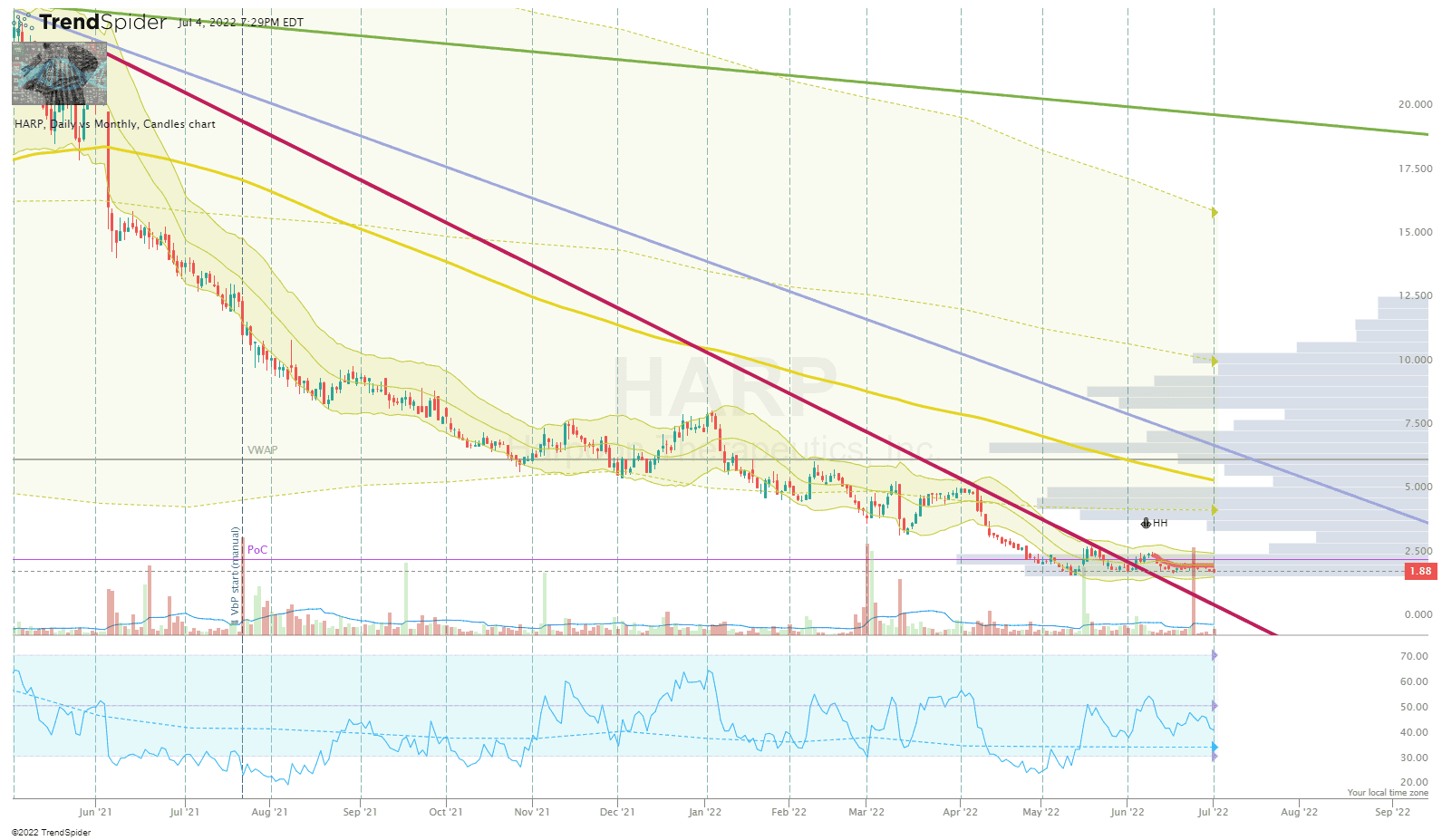

I am looking to initiate a small position under $2.00 per share in order to take advantage of the current negative EV valuation. Once I have established a position, I will look to employ a DCA approach by making additions every couple of weeks as long as the ticker's EV is still negative. If the EV valuation enters positive territory, I will switch to a discretionary strategy where I will look for technical setups before clicking the buy button.

HARP Daily Chart (Trendspider)

{kind=link}

HARP Daily Chart Enhanced View ( Trendspider )

On the other hand, I will set some sell orders to quickly book profits in order to establish a "house money" position. The company has several potential milestones listed for the second half of 2022 that may provide an opportunity to book some profits.

Harpoon Therapeutics Upcoming Milestones (Harpoon Therapeutics)

{kind=link}

I will continue trading HARP over the remainder of 2022 and into 2023 as long as their pipeline programs are able to report positive data and the company is able to complete their 2022 milestone checklist. If the company falls short, I will cease my buying activity and will hold my "house money" position until the company can address the issues and their finances.

Long term, I plan on maintaining a core position in the Bio Boom portfolio for at least five years in anticipation that Harpoon will get one or more of their assets across the finish line.

For further details see:

Harpoon Therapeutics: A T-Cell Engager Platform And A Negative Enterprise Value Makes It A Candidate For My 'Bio Boom' Portfolio