HSC - Harsco Corporation: Investing In A Greener Future

2023-05-17 15:33:48 ET

Summary

- HSC’s revenue growth should continue to benefit from higher price realization and healthy demand across both its businesses.

- Margins should benefit from pricing actions and productivity improvements.

- Based on my DCF calculations, I have a buy rating on the stock.

About the company

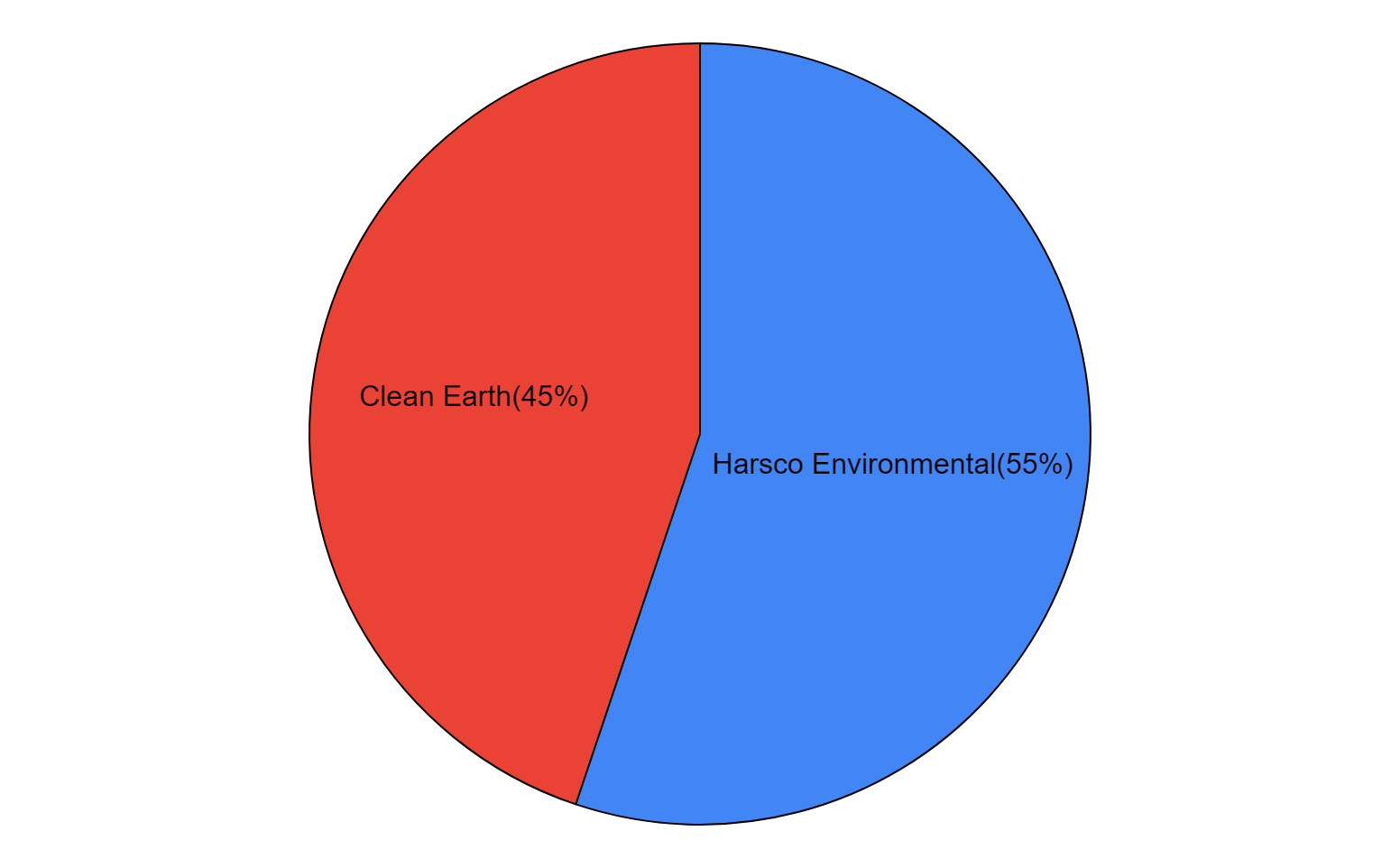

Harsco Corporation ( HSC ) is a renowned global leader in delivering comprehensive environmental solutions tailored to industrial and specialty waste streams. With a strong foothold in the Americas, EMEA, and APAC regions, the company operates through two distinct reporting segments: Harsco Environmental and Clean Earth.

Under the Harsco Environmental segment, the company excels in providing on-site operational support and resource recovery services. Through expert management of customers' primary waste and by-product streams, Harsco Environmental ensures efficient and sustainable solutions. The Clean Earth segment specializes in offering cutting-edge solutions for processing, treating, recycling, and reusing specialty waste. Catering to a diverse range of industries such as industrial, retail, healthcare, and construction, Clean Earth plays a vital role in responsible waste management. With 18 RCRA Part B permitted TSDFs (Treatment, Storage, and Disposal Facilities), wastewater treatment facilities, and 10-day transfer facilities spread across the United States, Clean Earth boasts an extensive infrastructure to handle waste efficiently. This is further supported by a fleet of 700 vehicles, ensuring prompt and reliable service to customers.

Harsco's segment distribution (Created by DzD Analysis by taking data from HSC)

{kind=link}

Q1 FY23 financial overview

HSC recently announced its first-quarter FY23 financial results , surpassing market expectations and leading to a 20% surge in its stock price. Following the earnings release, the company's stock is currently trading at $9.42, representing a noteworthy 48% increase since the beginning of 2023. During the first quarter, HSC achieved a notable 9.4% year-over-year increase in revenue, totaling $496 million. This figure surpassed the consensus estimate of $456 million, underscoring the company's ability to effectively capitalize on market opportunities. The revenue growth can be attributed to a combination of factors, including favorable pricing strategies and heightened demand for environmental services across the Clean Earth and Harsco Environmental segments. However, the positive impact was partially offset by unfavorable foreign exchange translation. Additionally, HSC reported an adjusted loss per share of $0.11 for Q1 2023, outperforming the consensus-estimated loss per share of $0.29. This can be attributed to the company's enhanced adjusted EBITDA margins, which were the result of strategic pricing actions, increased volumes, and cost improvements.

Outlook

Moving forward, my outlook for both of HSC's businesses remains positive, driven by favorable growth characteristics and strategic investments made by the company to bolster expansion. In 2023, I anticipate HSC's Harsco Environmental segment to achieve modest revenue growth surpassing 2022 levels. This growth will be driven by several factors, including the positive impact of higher service pricing, operational improvement initiatives, and increased demand for environmental services and products at select sites, particularly those associated with growth investments. However, these tailwinds should be partially offset by unfavorable currency translations. HSC operates in 25 different countries, with principal foreign exposures in the EU, Brazil, the U.K., and China. The U.S. dollar has strengthened against the British pound sterling, Euro, and Chinese yuan over the last few quarters. I believe the U.S. dollar should remain strong against these currencies over the next few quarters, impacting HSC's revenue growth.

The global steel market has recently experienced volatility due to the Russia-Ukraine conflict, the resulting energy crisis in Europe, inventory management throughout the steel supply chain, and weak macroeconomic conditions, resulting from rising interest rates. In Q1 FY23, HSC's customer sites witnessed a year-on-year decrease of approximately 1% in overall steel output. However, steel production performance varied by region, with weaker production in Europe and Latin America offset by growth in India, China, and North America. I expect the steel production comparisons to ease in the second half of 2023, considering the weak steel environment experienced in H2 of 2022. Additionally, the Harsco Environmental segment's eco-product business, which deals with stainless steel slag, is currently experiencing robust volume growth, which I believe will continue throughout the remainder of 2023.

Once macroeconomic conditions stabilize, I believe that the Harsco Environmental segment will grow in the long run. This should be due to the infrastructure investments supporting higher global steel consumption and ongoing investments and innovation to meet customers' environmental solution needs.

Regarding HSC's Clean Earth segment, I anticipate a substantial improvement in revenues for 2023 compared to the previous year. This growth will be fueled by factors such as higher price realization and a moderate increase in environmental service demand within specific end markets. Notably, the manufacturing and industrial, and healthcare end markets are currently experiencing healthy volume growth compared to the retail market, and I expect this trend to persist throughout 2023. Looking ahead, the Clean Earth segment is positioned to benefit from positive underlying market trends, including increased environmental regulation, further growth opportunities, and its attractive asset position. Additionally, the less cyclical and recurring nature of this business adds to its long-term prospects.

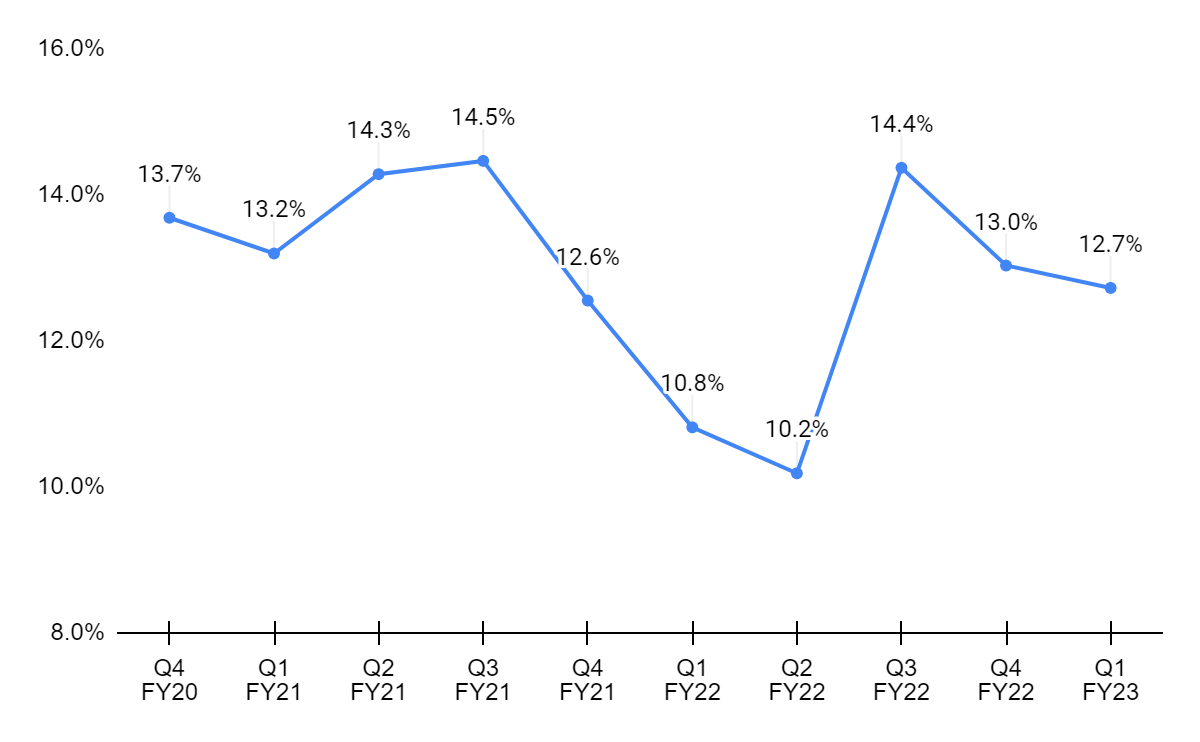

Harsco's adjusted EBITDA margin (Created by DzD Analysis by taking data from HSC)

{kind=link}

In terms of profitability, HSC has experienced a declining trend in margins over the past three quarters due to inflationary cost pressures. However, the company has a proactive strategy in place to address this issue and improve margins. HSC plans to continue implementing higher prices, as it has not been able to fully offset the inflationary pressure. This should help improve margins in 2023. Furthermore, HSC is actively exploring ad hoc services within its Environmental business. This includes processing waste materials into viable products and selling them into markets under HSC's eco-products portfolio. These services require minimal capital investment and have the potential to significantly improve margins. Additionally, the company is witnessing an improvement in labor productivity within this segment, which is expected to further boost margins. In its Clean Earth segment, the company is leveraging its lower overhead structure with higher volumes, which should improve margins. Overall, I am optimistic about HSC's bottom line improvement over the next few quarters.

Valuation

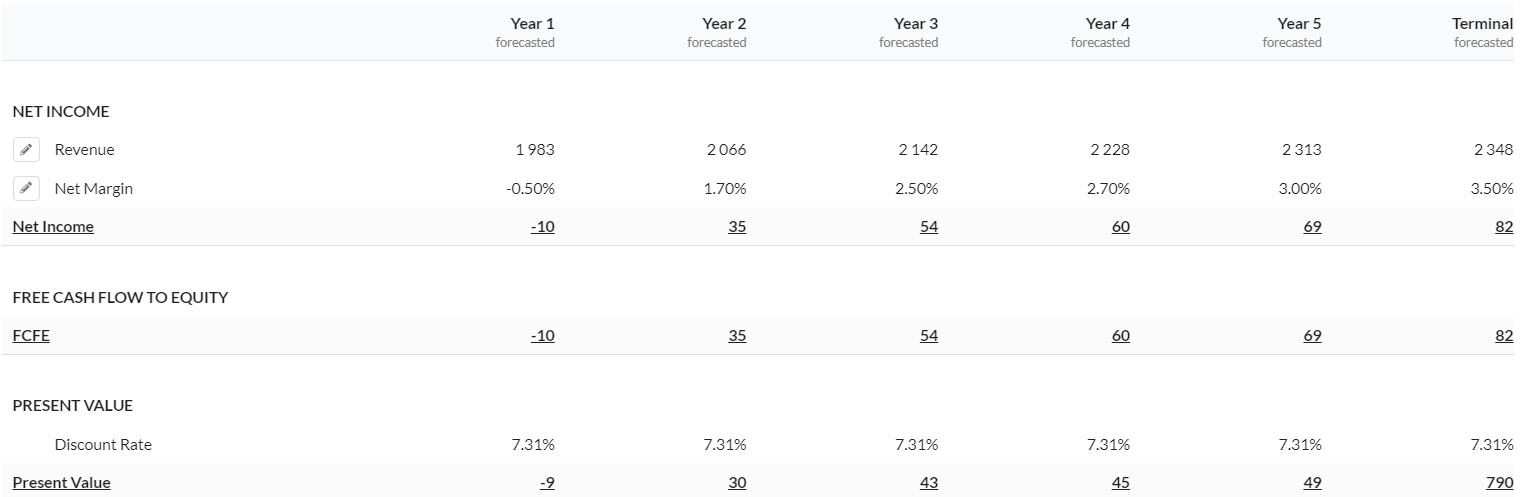

DCF valuation (Created by DzD Analysis using Alpha Spread)

{kind=link}

In my DCF calculations, I am assuming revenue growth to be mid-single-digit Y/Y in 2023, given the healthy demand across both businesses and pricing actions. Beyond 2023, I have assumed growth to be in the low to mid-single digits, with a terminal growth rate in the mid-single digits, as the company will continue to benefit from increased demand for environmental solutions and tight environmental regulations. I used a discount rate of 7.31% and arrived at a fair value of $11.93 for HSC.

Risks

- If the demand in certain end markets weakens, it might impact the company's revenue as HSC's customers might delay or cancel their contracts.

- If the steel production market continues to be under pressure, it might impact the company's topline growth as there will be less waste to process.

- HSC plans to continue raising prices to improve its profitability. Given the intense competition from privately-held businesses in HSC's regional markets, it may lose some of its contracts. This might impact the company's future revenue growth.

Conclusion

In conclusion, HSC's positive outlook is supported by favorable underlying growth characteristics and strategic investments aimed at supplementing future growth. In the Harsco Environmental segment, revenue should grow, driven by higher service pricing and increased demand for environmental services and products. The steel market's recent volatility has impacted HSC's customer sites, but the expectation of improved steel production in the second half of the year provides a positive outlook. The Clean Earth segment should see meaningful revenue improvement in 2023 compared to the previous year, supported by higher price realization and increased demand within specific end markets. Despite recent margin declines due to inflationary cost pressures, HSC has a strategic plan in place to offset these pressures and improve profitability. Overall, HSC's positive outlook and strategic initiatives position the company for sustained growth and profitability. Hence, I have a buy rating on the stock.

For further details see:

Harsco Corporation: Investing In A Greener Future